Quick Navigation

Report Overview

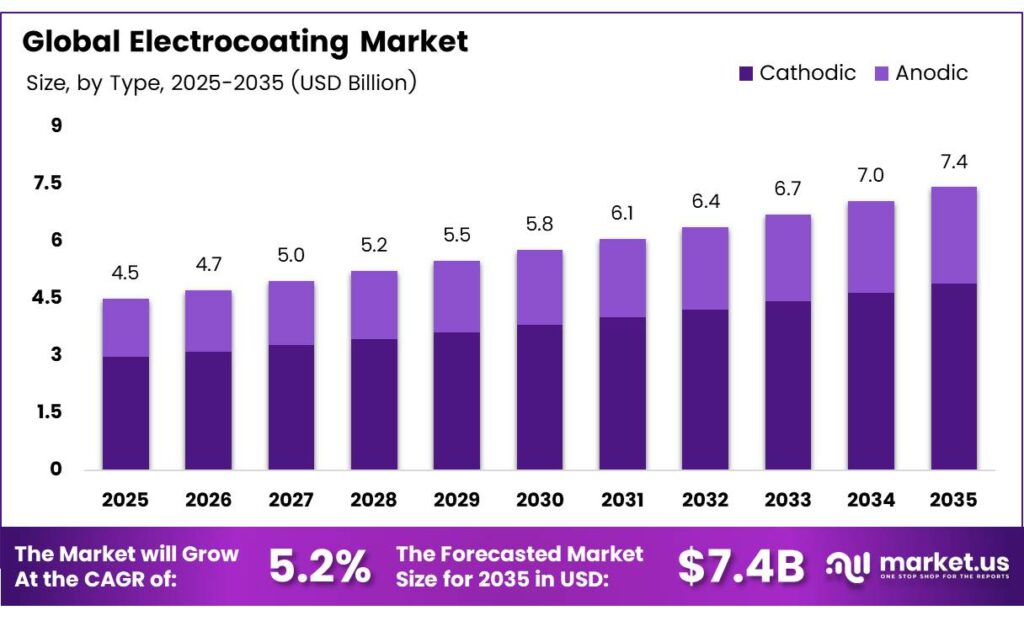

The Global Electrocoating Market size is expected to be worth around USD 7.4 billion by 2035 from USD 4.5 billion in 2025, growing at a CAGR of 5.2% during the forecast period 2026 to 2035.

Electrocoating — also known as e-coating or electrophoretic deposition — applies paint to metal and multi-material substrates using electrical current. The process delivers uniform coverage across complex geometries, making it the preferred finishing method for automotive bodies, industrial equipment, and increasingly, electric vehicle structural components.

Regulatory pressure on volatile organic compound (VOC) emissions is reshaping procurement decisions across North America, Europe, and East Asia. Manufacturers face tightening thresholds that make waterborne and low-HAP electrocoat technologies not optional, but operationally mandatory. This compliance pressure is one of the clearest structural forces pushing industrial buyers toward e-coat adoption.

The process efficiency of electrocoating is a key differentiator that drives its retention across high-volume manufacturing environments. Industrial electrocoat systems achieve around 98% material transfer efficiency — significantly higher than most spray and dip technologies — due to the closed-loop, highly automated immersion process. This figure matters because it directly reduces raw material waste costs at scale.

E-coating transfer efficiency reaches 95–97%, compared with 60–70% for powder coating and 30–35% for spray coating. This performance gap gives e-coat a structural cost advantage in high-throughput facilities, where material waste compounds rapidly. Buyers in competitive manufacturing environments use this efficiency gap to justify capital investment in full e-coat line conversions.

Key Takeaways

- The Global Electrocoating Market was valued at USD 4.5 billion in 2025 and is forecast to reach USD 7.4 billion by 2035 at a CAGR of 5.2% during the forecast period 2026–2035.

- Cathodic electrocoating leads with a 69.4% share due to superior corrosion resistance.

- Epoxy Coating Technology holds a dominant 66.2% share of the market.

- Metal accounts for the largest share at 73.1% of total electrocoating applications.

- Conventional Electrocoating holds 47.5% share, reflecting its widespread industrial adoption.

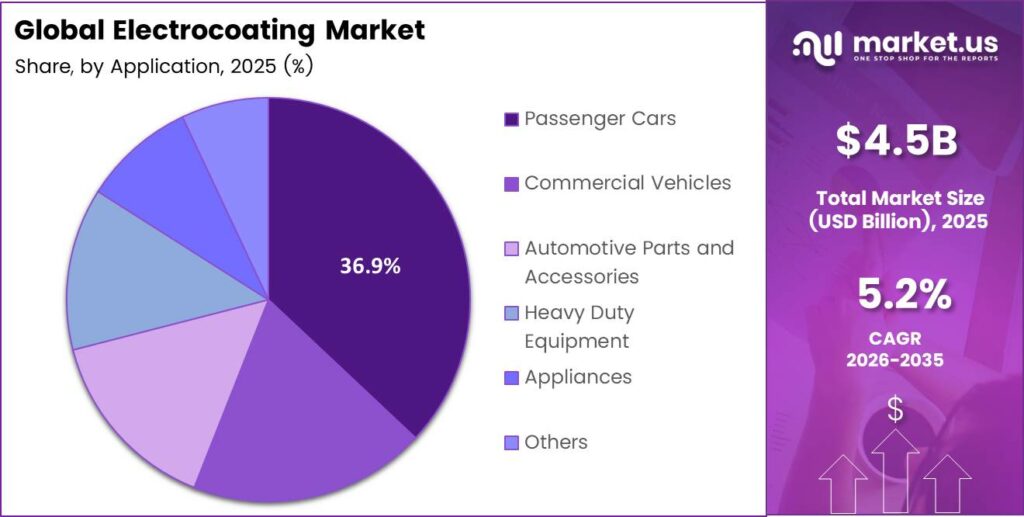

- Passenger Cars represent the top end-use segment with a 36.9% share.

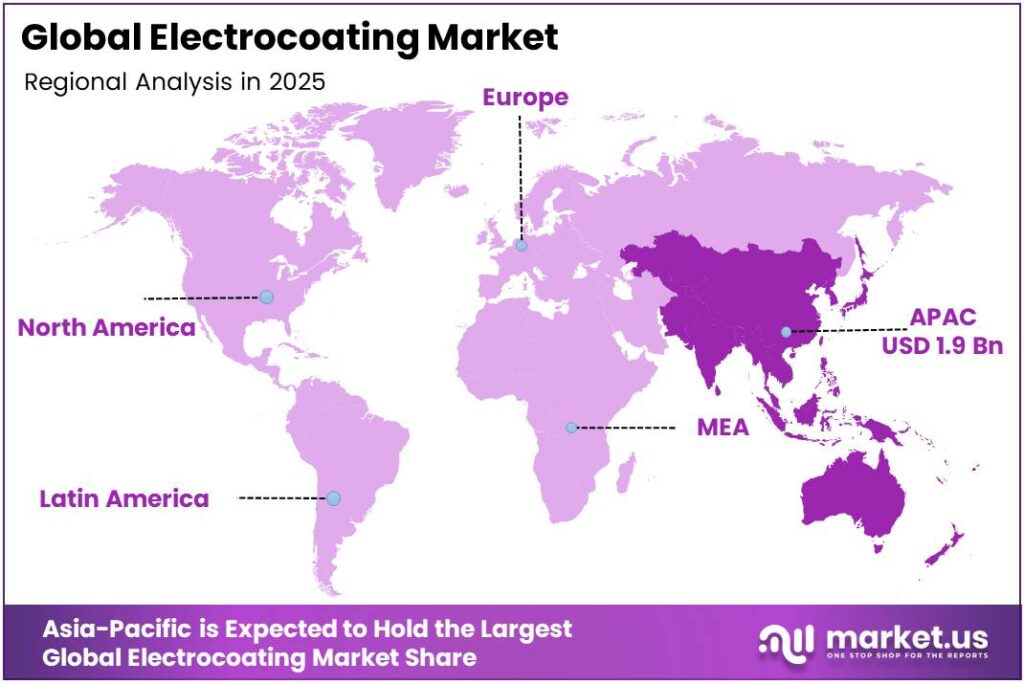

- Asia-Pacific dominates regional markets with a 43.6% share, valued at approximately USD 1.9 billion.

Type Analysis

Cathodic electrocoating dominates with 69.4% due to superior corrosion resistance and EV compatibility.

In 2025, Cathodic electrocoating held a dominant market position in the By Type segment of the Electrocoating Market, with a 69.4% share. Cathodic systems deposit coating onto negatively charged substrates, producing denser film layers with fewer pinholes. This structural advantage delivers the corrosion resistance benchmarks that automotive OEMs and EV manufacturers require for body-in-white and structural component protection.

Anodic electrocoating serves niche applications where decorative finish quality outweighs maximum corrosion protection requirements. It operates at lower process temperatures and offers faster color development, making it viable for aluminum-intensive applications in consumer goods and architectural components. However, its market position remains secondary as automotive and industrial buyers consistently prioritize cathodic performance specifications.

Coating Technology Analysis

Epoxy Coating Technology dominates with 66.2% due to proven corrosion barrier performance.

In 2025, Epoxy Coating Technology held a dominant market position in the By Coating Technology segment of the Electrocoating Market, with a 66.2% share. Epoxy-based formulations bond tightly to metal substrates, creating a chemically resistant primer layer that supports topcoat adhesion. Automotive assembly plants worldwide have standardized on epoxy electrocoat as the first corrosion-protection layer, embedding this technology deeply into existing production infrastructure.

Acrylic Coating Technology differentiates through UV stability and color retention, targeting applications where topcoat appearance and outdoor durability matter more than pure corrosion resistance. Agricultural equipment, outdoor infrastructure, and consumer appliances represent its primary end markets. Acrylic’s share expansion depends on the buyer’s willingness to accept its lower corrosion threshold in exchange for superior finish aesthetics.

Substrate Type Analysis

Metal dominates with 73.1% due to automotive and industrial structural component volume.

In 2025, Metal held a dominant market position in the By Substrate Type segment of the Electrocoating Market, with a 73.1% share. Steel and aluminum body panels, chassis components, and structural assemblies represent the largest volume of electrocoated parts globally. The automotive industry’s preference for metal substrates aligns directly with electrocoating’s technical strengths — uniform film thickness across weld seams, holes, and recessed cavities that other coating methods cannot reach consistently.

Plastic substrates carry the second-largest share, driven by expanding use of engineering polymers in automotive fascias, interior brackets, and electronic enclosures. Electrocoating plastic requires specialized conductive primers and pretreatment steps, which add process complexity. However, plastics’ weight reduction benefits in EV platforms are pushing manufacturers to invest in these expanded pretreatment capabilities.

Process Technology Analysis

Conventional Electrocoating dominates with 47.5% due to established infrastructure and proven line reliability.

In 2025, Conventional Electrocoating held a dominant market position in the By Process Technology segment of the Electrocoating Market, with a 47.5% share. Conventional systems operate at established voltage and current parameters that most industrial facilities have optimized over decades. Replacement cycles are long and capital-intensive, which means installed conventional lines continue generating production volume even as newer process variants emerge.

High-Speed Electrocoating serves high-throughput manufacturing environments where cycle time reduction directly improves line profitability. Automotive stamping plants and major appliance manufacturers represent its core adopter base. Its share growth depends on facilities reaching production volumes where the capital premium for high-speed equipment is recoverable within acceptable payback periods.

Application Analysis

Passenger Cars dominate with 36.9% due to high-volume body-in-white corrosion protection requirements.

In 2025, Passenger Cars held a dominant market position in the By Application segment of the Electrocoating Market, with a 36.9% share. Every passenger vehicle body shell passes through an e-coat bath as the first corrosion protection step after pretreatment. Global passenger car production volumes — concentrated in China, Europe, and North America — translate directly into electrocoating consumption at automotive assembly plants.

Commercial Vehicles generate demand through truck cab assemblies, trailer frames, and chassis components requiring heavier film thickness and longer corrosion protection cycles than passenger cars. Fleet operators and commercial vehicle buyers apply stricter total-cost-of-ownership criteria, which makes electrocoating’s durability advantage a purchase driver rather than just a specification compliance requirement.

Key Market Segments

By Type

- Cathodic

- Anodic

By Coating Technology

- Epoxy Coating Technology

- Acrylic Coating Technology

By Substrate Type

- Metal

- Plastic

- Ceramic

- Glass

By Process Technology

- Conventional Electrocoating

- High-Speed Electrocoating

- Pulse Electrocoating

- Reverse Electrocoating

By Application

- Passenger Cars

- Commercial Vehicles

- Automotive Parts and Accessories

- Heavy Duty Equipment

- Appliances

- Others

Emerging Trends

Waterborne Technologies and Digital Automation Redefine Electrocoating Line Economics

Waterborne and high-solid electrocoat technologies now achieve up to 20% VOC emission reduction versus conventional solvent-borne systems. This performance level crosses regulatory thresholds in key markets, making waterborne conversion a compliance-driven capital decision rather than an elective upgrade. Manufacturers who delay conversion face permit risk and operational disruption.

Digitalized and automated e-coat lines improve production efficiency by approximately 8%. This figure underestimates long-term impact: automated bath monitoring eliminates technician variability in chemistry management, reduces off-specification output, and compresses the data loop between quality detection and process correction. For high-volume automotive lines, an 8% efficiency gain translates directly into millions in annual cost reduction.

Electrocoating applications now extend into complex multi-material assemblies combining steel, aluminum, and engineered polymers. Continuous resin chemistry innovation supports adhesion across substrate interfaces that earlier formulations could not reliably bridge. Early movers who qualify multi-substrate e-coat processes for EV platform assemblies will hold a process capability advantage as mixed-material vehicle architectures become standard.

Drivers

VOC Regulations and EV Platform Requirements Create Simultaneous Pull for Advanced Electrocoating Systems

Regulatory bodies across the EU, the United States, and East Asia are enforcing stricter VOC emission ceilings on industrial coating operations. Electrocoating’s waterborne chemistry positions it as the compliant default for automotive and industrial manufacturers facing these mandates. This regulatory mechanism converts what was previously a cost-optimization decision into a legal compliance requirement, accelerating line conversions.

Electric vehicle manufacturing introduces new corrosion protection requirements that conventional spray methods cannot consistently satisfy. Battery enclosures, structural aluminum extrusions, and multi-metal chassis components demand uniform coverage across complex geometries — precisely where electrocoating’s immersion-based deposition excels. E-coating labor costs run up to 50% lower than alternative coating methods, which means EV manufacturers face simultaneous cost and performance incentives to standardize on electrocoating for structural components.

Industrial automation expansion strengthens the economic case for electrocoating by improving process consistency and throughput. Automated e-coat lines reduce human variability in bath management, film thickness control, and quality inspection. Additionally, energy-efficient electrocoat systems with optimized cure schedules reduce per-unit energy consumption, directly supporting manufacturing sustainability targets that major automotive OEMs now embed in supplier qualification criteria.

Restraints

Alternative Coating Technologies and Regulatory Compliance Complexity Limit Electrocoating Expansion

Powder coating and advanced liquid coating systems offer competitive corrosion protection with lower wastewater generation than electrocoating. Facilities operating under strict water discharge regulations face additional treatment costs when running e-coat lines. This wastewater management burden gives powder coating a localized advantage in regions with stringent effluent standards, particularly for smaller-volume production environments.

Chemical handling requirements for electrocoating pretreatment — including phosphating, degreasing, and rinse stage management — create operational complexity that smaller manufacturers often lack the technical staff to manage consistently. Achieving the 98% transfer efficiency benchmark requires precisely controlled bath chemistry, meaning any compliance gap in pretreatment directly degrades the process performance advantage that justifies electrocoating’s capital investment.

The capital intensity of electrocoating line installation creates a structural barrier for mid-size manufacturers considering adoption. E-coat systems require immersion tanks, rectifiers, ultrafiltration units, and cure ovens operating as an integrated system. Consequently, facilities with insufficient production volume to justify this capital outlay — or insufficient floor space for full system installation — remain locked out of electrocoating’s process efficiency advantages regardless of regulatory incentives.

Growth Factors

EV Investment, Smart Monitoring, and Sustainable Formulations Open New Revenue Channels for Electrocoating Providers

Electric vehicle manufacturers are investing heavily in battery enclosure and structural component protection, creating new application volume for electrocoating outside the traditional automotive body-in-white workflow. Properly cured e-coat achieves up to 97% paint adhesion to the surface — a performance level that makes electrocoating the technically credible choice for battery component protection where adhesion failure has safety consequences.

IoT-based monitoring integration with electrocoating lines enables real-time film thickness measurement, bath chemistry tracking, and quality alert systems. This capability converts electrocoating from a batch-verified process to a continuously monitored one.

Bio-resin and sustainable electrocoat formulations represent the next chemistry development cycle. Formulators reducing solvent content and replacing petroleum-derived resin components with bio-based alternatives extend electrocoating’s regulatory compliance window and reduce environmental liability exposure.

Regional Analysis

Asia-Pacific Dominates the Electrocoating Market with a Market Share of 43.6%, Valued at USD 1.9 Billion

Asia-Pacific commands a 43.6% share of the global Electrocoating Market, valued at approximately USD 1.9 billion. China’s position as the world’s largest vehicle producer and South Korea’s electronics manufacturing concentration create structural, volume-driven electrocoating demand. These production fundamentals — not just market size — explain why Asia-Pacific’s lead is durable rather than cyclical.

North America maintains a strong market position underpinned by established automotive assembly infrastructure in the United States and Canada. Regulatory pressure from the EPA on VOC emissions strengthens the structural case for the adoption of waterborne electrocoat among Midwest and Southern auto manufacturing clusters. EV platform investments by domestic and foreign OEMs are expanding the addressable volume for advanced e-coat systems.

Europe’s electrocoating market operates within one of the strictest regulatory frameworks for industrial coating emissions globally. EU VOC directives and REACH chemical regulations mandate compliant electrocoat chemistry as a non-negotiable operational requirement. Germany and France — as the region’s dominant automotive production centers — anchor electrocoating consumption and set specification standards that other European markets follow.

Latin America’s electrocoating market develops alongside its expanding automotive assembly base, particularly in Brazil and Mexico. Both countries host major OEM facilities serving North American and domestic markets, creating consistent demand for body-in-white corrosion protection. However, lower regulatory stringency on VOC emissions means the technology mix favors conventional over advanced waterborne systems compared to more regulated regions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

B.L. Downey Company LLC positions itself as a specialized electrocoating chemistry supplier serving industrial and automotive finishing operations. Its focus on custom bath formulations and process support services — rather than broad product commoditization — creates stickiness with manufacturing customers who rely on technical support to maintain bath performance and regulatory compliance documentation.

BASF SE leverages its global chemical manufacturing scale to supply electrocoat resin systems and additive packages across automotive, appliance, and industrial markets. Its R&D investment in sustainable resin chemistry aligns with the industry shift toward bio-based and low-VOC formulations. This positions BASF to benefit from regulatory-driven reformulation cycles that force manufacturers to qualify new electrocoat chemistries.

Dymax Corporation differentiates through light-cure and specialty coating technologies that complement conventional electrocoating in precision assembly applications. Its target markets — medical devices, electronics, and aerospace components — require coating solutions that deliver both functional protection and dimensional precision. This specialization insulates Dymax from direct commodity pricing pressure in the broader automotive electrocoating market.

Electro Coatings Inc. operates as a contract electrocoating service provider, giving manufacturers access to e-coat corrosion protection without capital investment in proprietary line infrastructure. This model addresses the adoption barrier created by high line installation costs. For mid-size manufacturers producing insufficient volume to justify dedicated systems, contract coating partnerships convert electrocoating from a capital decision into an operational expense.

Key Players

- B.L. Downey Company LLC

- BASF SE

- Dymax Corporation

- Electro Coatings Inc.

- Greenkote

- H.E. Orr Company

- Hawking Electrotechnology Limited

- Henkel AG & Co. KGaA

- Lippert Components Inc.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries Inc.

- The Sherwin-Williams Company

Recent Developments

- In 2025, BASF expanded its e-coat manufacturing facility in Mangalore, India, to serve automotive OEM demand in India, South Asia, and ASEAN; the site can make newer e-coats such as CathoGuard 800 RE. BASF agreed to sell its coatings business to Carlyle. BASF Coatings’ CathoGuard 800RE cathodic electrodeposition coating won a Green Impact Pioneer Award in China.

- In 2025, Dymax Corporation is not primarily an electrocoating supplier, but it is related through coatings and masking materials. Its SpeedMask products are positioned for use during painting, some e-coating, and powder coating. Dymax announced electronics-assembly coatings/adhesives, including TPO-free UV/LED-curable materials for battery and PCB assemblies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.5 Billion |

| Forecast Revenue (2035) | USD 7.4 Billion |

| CAGR (2026-2035) | 5.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Cathodic, Anodic), By Coating Technology (Epoxy Coating Technology, Acrylic Coating Technology), By Substrate Type (Metal, Plastic, Ceramic, Glass), By Process Technology (Conventional Electrocoating, High-Speed Electrocoating, Pulse Electrocoating, Reverse Electrocoating), By Application (Passenger Cars, Commercial Vehicles, Automotive Parts and Accessories, Heavy Duty Equipment, Appliances, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | B.L. Downey Company LLC, BASF SE, Dymax Corporation, Electro Coatings Inc., Greenkote, H.E. Orr Company, Hawking Electrotechnology Limited, Henkel AG & Co. KGaA, Lippert Components Inc., Nippon Paint Holdings Co., Ltd., PPG Industries Inc., The Sherwin-Williams Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |