Quick Navigation

Report Overview

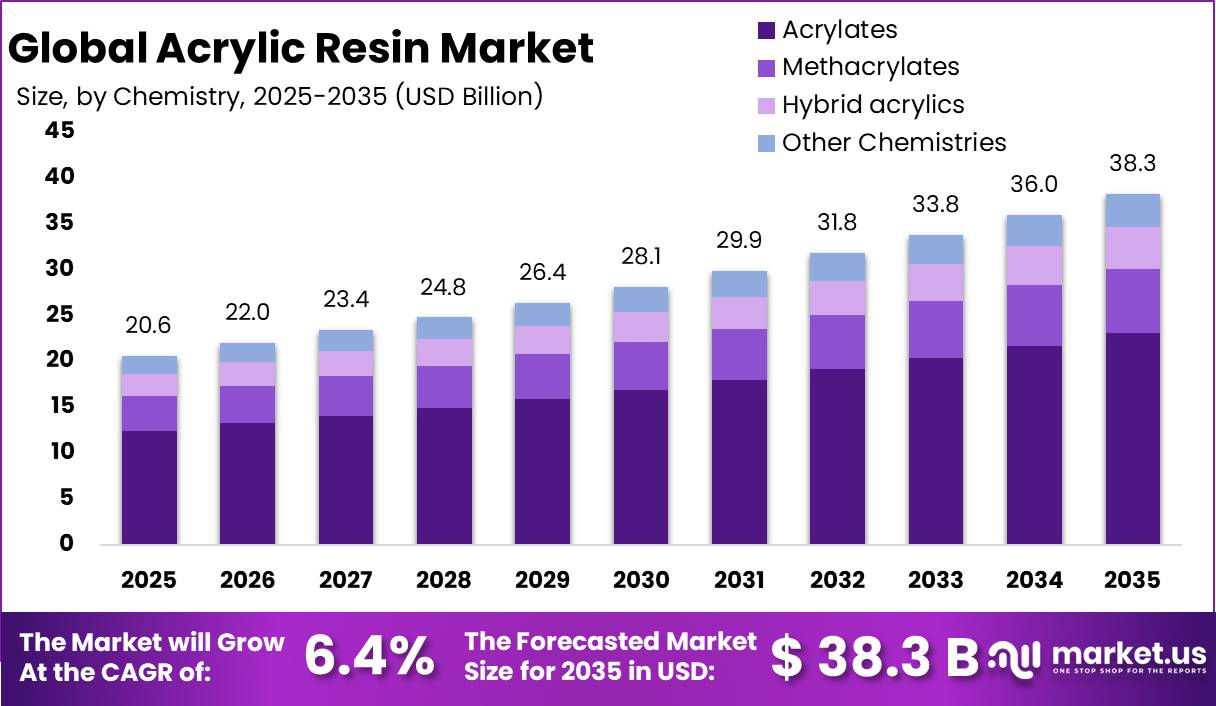

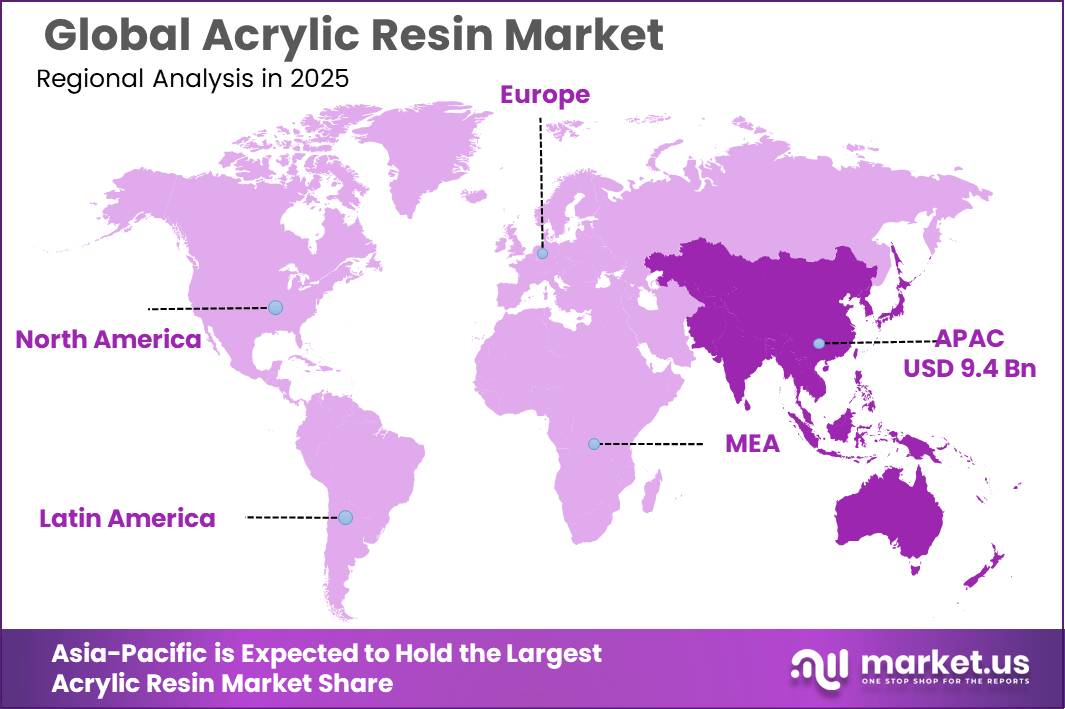

The Global Acrylic Resin Market size is expected to be worth around USD 38.3 Billion by 2035, from USD 20.6 Billion in 2025, growing at a CAGR of 6.4% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 39.8% share, holding USD 22.3 Billion revenue.

Acrylic resin is a high-performance polymer used in architectural coatings, industrial paints, adhesives, sealants, plastics, inks, and specialty films because it offers strong weather resistance, gloss retention, hardness, clarity, and fast-drying performance. The industry is moving toward waterborne, low-VOC, bio-based, and UV-curable systems as coatings producers respond to tighter environmental rules and customer demand for durable, lower-carbon materials.

- Regulatory pressure is a major shift: the EU Renovation Wave aims to renovate 35 million buildings by 2030, which supports demand for protective and decorative acrylic coating systems in Europe. Regulatory pressure is also shaping demand, as the U.S. EPA’s architectural coating VOC rule is estimated to reduce VOC emissions by 103,000 Mg per year, encouraging wider use of cleaner coating technologies.

Key Takeaways

- Acrylic Resin Market size is expected to be worth around USD 38.3 Billion by 2035, from USD 20.6 Billion in 2025, growing at a CAGR of 6.4%.

- Acrylates held a dominant market position, capturing more than a 60.20% share in the Acrylic Resin Market.

- Water-based Acrylic Resins held a dominant market position, capturing more than a 58.90% share in the Acrylic Resin Market.

- Thermoplastic Acrylic Resins held a dominant market position, capturing more than a 61.10% share in the Acrylic Resin Market.

- Paints & Coatings held a dominant market position, capturing more than a 60.10% share in the Acrylic Resin Market.

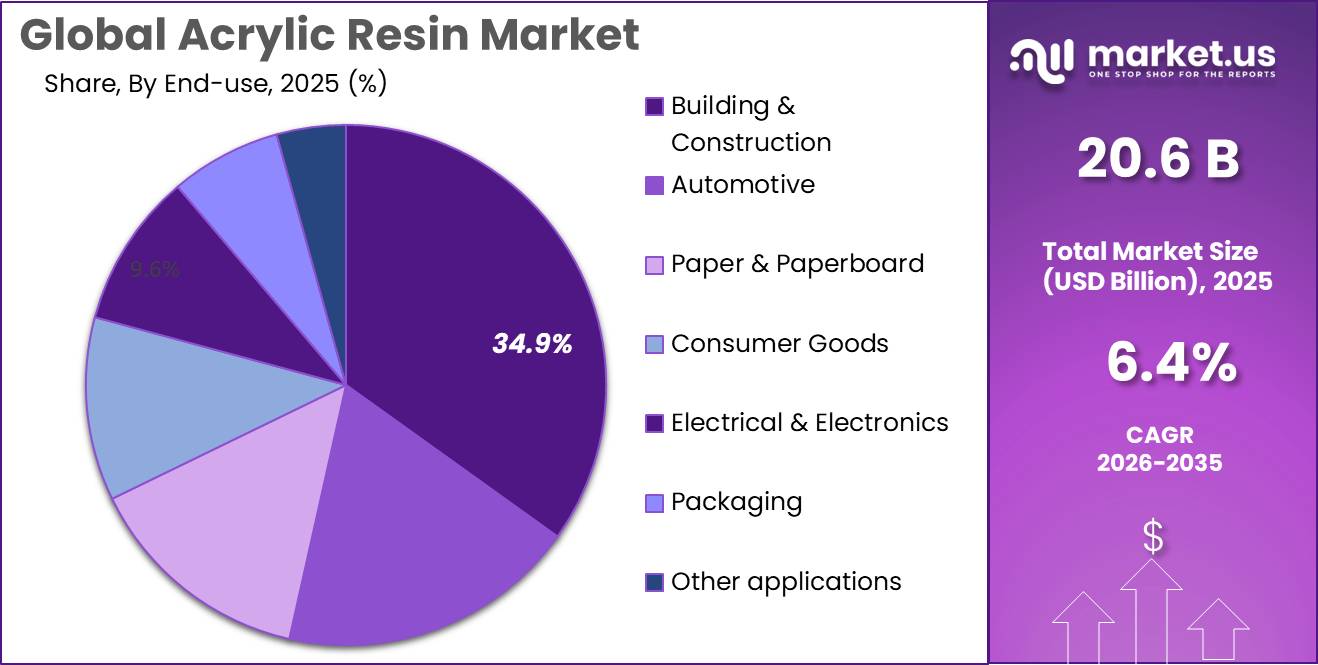

- Building & Construction held a dominant market position, capturing more than a 34.90% share in the Acrylic Resin Market.

- Asia-Pacific emerged as the leading regional market in the Acrylic Resin industry, accounting for a dominant 45.80% share and reaching a market value of USD 9.4 billion.

The market environment remains linked to construction, renovation, automotive refinishing, packaging, and electronics. In Europe, the chemical industry remains a major supply base, with €635 billion turnover and 1.2 million employees, although its global market share has fallen to 13%, while China accounts for 46% of global chemical sales. This shows that acrylic resin producers are operating in a competitive but high-volume industrial ecosystem. In the U.S., chemical output was expected to rise only 0.3% in 2025, reflecting slower demand in several chemical-consuming sectors, but acrylic resin continues to benefit from its role in sustainable coatings and performance materials.

Key driving factors include stricter environmental regulations mandating low-VOC, bio-based, and recyclable resin systems. Consumer preferences for sustainable, cost-effective coating materials are accelerating demand, with the acrylic coatings market expected to reach over $10 billion in 2025. Technological advancements in methacrylates, the largest market segment, alongside emerging acrylates as the fastest-growing segment, further propel expansion.

Arkema S.A. has a strong position in acrylic monomers, coating resins, additives, and specialty materials. In 2024, Arkema reported total sales of €9.5 billion, with EBITDA of €1.532 billion and a 16.1% EBITDA margin. Its Coating Solutions segment recorded €2.455 billion in sales, with around 30% linked to acrylic monomers, showing its direct relevance to acrylic resin value chains.

By Chemistry Analysis

Acrylates Dominated with 60.20% Share Driven by Broad Industrial Adoption

In 2025, Acrylates held a dominant market position, capturing more than a 60.20% share in the Acrylic Resin Market by chemistry. This leadership was supported by the strong balance of performance, processing flexibility, and cost efficiency offered by acrylate-based resin systems across multiple end-use industries. Acrylates continued to remain the preferred chemistry for architectural coatings, industrial coatings, adhesives, construction materials, and specialty surface applications because they provide excellent weather resistance, color retention, transparency, and long-term durability.

By Solvency Analysis

Water-based Acrylic Resins dominated with 58.90% share supported by rising preference for cleaner and efficient coating technologies.

In 2025, Water-based Acrylic Resins held a dominant market position, capturing more than a 58.90% share in the Acrylic Resin Market by solvency. The segment maintained its leadership due to growing industry preference for environmentally responsible formulations and improved application efficiency across coatings, adhesives, construction materials, and surface finishing solutions. Water-based systems continued to gain stronger acceptance because they provide lower odor, easier handling, and reduced dependence on solvent-intensive processing methods.

By Property Analysis

Thermoplastic Acrylic Resins dominated with 61.10% share due to their versatility and ease of processing across industries.

In 2025, Thermoplastic Acrylic Resins held a dominant market position, capturing more than a 61.10% share in the Acrylic Resin Market by property. The segment maintained its leading position because of its broad usability across coatings, inks, adhesives, construction materials, and industrial finishing applications. Thermoplastic acrylic resins continued to gain preference due to their ability to soften when heated and reform without major loss of performance, making them suitable for efficient manufacturing and flexible processing requirements.

By Application Analysis

Paints & Coatings dominated with 60.10% share driven by strong demand for durable and decorative surface solutions.

In 2025, Paints & Coatings held a dominant market position, capturing more than a 60.10% share in the Acrylic Resin Market by application. The segment continued to lead due to the extensive use of acrylic resins in decorative, protective, industrial, and architectural coating systems. Acrylic resins remained highly preferred because they provide strong weather resistance, color stability, gloss retention, and long-term surface protection across a wide range of applications.

By End-use Analysis

Building & Construction dominated with 34.90% share supported by continuous demand for durable and efficient building materials.

In 2025, Building & Construction held a dominant market position, capturing more than a 34.90% share in the Acrylic Resin Market by end-use industry. The segment remained the largest consumer of acrylic resin products due to their extensive use in architectural coatings, sealants, adhesives, waterproofing systems, and decorative surface applications. Acrylic resins continued to gain preference because they provide strong weather resistance, durability, color retention, and long-lasting performance across residential, commercial, and infrastructure projects

Key Market Segments

By Chemistry

- Acrylates

- Methacrylates

- Hybrid acrylics

- Other Chemistries

By Solvency

- Water-based Acrylic Resins

- Solvent-based Acrylic Resins

- Other solvencies

By Property

- Thermoplastic Acrylic Resins

- Thermosetting Acrylic Resins

- Other properties

By Application

- Paints & Coatings

- Adhesives & Sealants

- Elastomers

- DIY / Decorative Coatings

- Other applications

By End-use

- Building & Construction

- Automotive

- Paper & Paperboard

- Consumer Goods

- Electrical & Electronics

- Packaging

- Other applications

Market Dynamics

Driver Analysis - Growing Packaged Food Demand Accelerates Acrylic Resin Usage

One of the major driving factors for the Acrylic Resin market is the continuous expansion of packaged food production and modern food packaging requirements. Acrylic resins are increasingly used in food packaging coatings, labels, laminates, inks, and protective layers because they offer clarity, durability, chemical resistance, and strong surface performance. As food manufacturers focus more on product safety, shelf appeal, and longer storage periods, the demand for advanced resin materials continues to increase.

The food packaging industry has become an important consumption area supporting acrylic resin adoption. According to industry estimates, the global food packaging market reached approximately USD 533.22 billion in 2025 and is expected to continue expanding as packaged and convenience food consumption rises globally. This growth creates additional demand for coating and resin technologies that improve packaging appearance, protection, and operational efficiency.

Government and international organizations are also highlighting long-term growth in food production and supply systems. According to the OECD–FAO Agricultural Outlook 2025–2034, global agricultural and fish production is projected to increase by around 14% over the next decade, supported mainly by productivity improvements and rising food demand from growing urban populations. Higher food output directly supports additional packaging needs, creating favorable conditions for acrylic resin consumption across food-related applications.

Restraint Analysis - Rising Environmental Regulations Limit Acrylic Resin Expansion

One major restraining factor for the Acrylic Resin market is the growing pressure from environmental regulations related to plastic use, packaging waste, emissions control, and material sustainability. Acrylic resins are widely used in coatings, packaging, food-contact materials, and protective applications, but stricter global policies are increasing compliance costs and creating pressure to redesign products and manufacturing processes.

- According to the United Nations Environment Programme (UNEP), approximately 36% of all plastics produced globally are used in packaging applications, and nearly 85% of single-use plastic packaging eventually ends up in landfills or becomes mismanaged waste. This growing waste burden is pushing governments and industries to accelerate restrictions on conventional packaging materials and promote circular solutions.

Government initiatives are also increasing pressure across the value chain. The European Union approved stronger packaging reduction measures that target lower packaging waste generation, improved recyclability, and tighter controls on single-use plastic formats by 2030. Packaging waste in Europe increased by 25% between 2009 and 2021 and reached around 84 million tonnes, encouraging stricter material standards that directly affect resin producers supplying food and consumer packaging sectors.

At the same time, food waste and packaging efficiency are becoming linked policy priorities. UNEP’s Food Waste Index Report 2024 estimated that the world generated 1.05 billion tonnes of food waste in 2022, equal to nearly 19% of food available to consumers. Governments increasingly expect packaging materials to support both food preservation and environmental performance at the same time, creating additional technical and cost challenges for acrylic resin manufacturers.

Opportunity Analysis - Expanding Sustainable Food Packaging Creates Acrylic

One major growth opportunity for the Acrylic Resin market is the rapid expansion of sustainable food packaging and advanced food protection solutions. Acrylic resins are increasingly being adopted in food packaging coatings, labels, laminates, and barrier applications because they help improve appearance, extend product shelf life, and support lower-emission packaging technologies. As food producers and governments focus on reducing waste while improving packaging performance, demand for acrylic-based materials continues to open new opportunities across the value chain.

The food industry is becoming a strong growth platform for resin innovation. According to the Food and Agriculture Organization (FAO), nearly one-third of food produced globally for human consumption is lost or wasted each year, equal to around 1.3 billion tonnes annually. Better packaging technologies are increasingly recognized as an important tool to reduce product damage and preserve food quality during transportation and storage. This creates opportunities for acrylic resin producers to develop protective and functional packaging systems.

Government initiatives are also encouraging packaging modernization. The European Commission’s Packaging and Packaging Waste Regulation supports increased recyclability, packaging reduction targets, and greater use of circular material systems across food applications. These policies are encouraging manufacturers to invest in coating and resin technologies that combine product protection with environmental performance.

- According to the United Nations Environment Programme (UNEP), global municipal solid waste generation is expected to rise from 2.3 billion tonnes in 2023 to 3.8 billion tonnes by 2050. This has increased interest in packaging materials that improve resource efficiency and reduce product loss. Acrylic resin technologies are positioned to benefit because they support durability, coating performance, and evolving sustainability requirements across food packaging applications.

Emerging Trend Analysis - Water-Based Food Packaging Solutions Reshape Acrylic Demand

One major latest trend shaping the Acrylic Resin market is the growing shift toward water-based and sustainable packaging materials in the food industry. Acrylic resins are increasingly being selected for food packaging coatings, labels, protective layers, and surface finishing applications because they support lower emissions, improved appearance, and better packaging functionality. As food producers focus on reducing environmental impact while maintaining product quality, water-based acrylic technologies are gaining wider acceptance across packaging operations.

The food packaging industry continues to evolve under changing consumer and regulatory expectations. According to the Food and Agriculture Organization (FAO), approximately 14% of food produced globally is lost before reaching retail markets each year. This has increased attention on packaging technologies that improve product preservation, reduce damage during transport, and extend shelf life. Acrylic resin-based coatings and barrier systems are becoming increasingly relevant because they support packaging performance while helping reduce product losses across supply chains.

Government initiatives are also accelerating this trend. The European Union introduced updated packaging sustainability measures through the Packaging and Packaging Waste Regulation to encourage recyclable and lower-impact packaging solutions. The regulation promotes reduced packaging waste and improved circular use of materials, encouraging packaging manufacturers to adopt advanced coating technologies and environmentally aligned resin systems.

- According to the United Nations Environment Programme (UNEP), households generated around 631 million tonnes of food waste in 2022, making food preservation and efficient packaging a growing focus area worldwide. This has encouraged greater investment in protective coatings and material technologies that can improve storage efficiency and reduce spoilage.

Regional Insights

Asia-Pacific Dominated the Acrylic Resin Market with a 45.80% Share, Valued at USD 9.4 Billion

Asia-Pacific emerged as the leading regional market in the Acrylic Resin industry, accounting for a dominant 45.80% share and reaching a market value of USD 9.4 billion. The region maintained its leadership due to strong industrial activity, expanding construction output, rising manufacturing investments, and growing demand across coatings, adhesives, packaging, and infrastructure applications. Acrylic resins continued to witness broad adoption because of their durability, weather resistance, and compatibility with high-volume industrial production.

The region’s market strength was supported by rapid urban expansion and large-scale construction development across major economies. Demand for architectural coatings, protective surfaces, decorative finishes, and industrial materials remained strong, creating stable consumption of acrylic resin products. Growth in residential and commercial building activity further strengthened regional demand for acrylic-based technologies used in paints, sealants, waterproofing systems, and construction materials.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE remains one of the major participants in the acrylic resin market through its broad portfolio of acrylic dispersions, binders, and performance materials used across coatings, construction, and industrial applications. In 2025, the company continued focusing on efficiency and advanced material development across its global production network. BASF reported revenue of approximately €65.3 billion in 2024 and continued investment in specialty materials and sustainable solutions.

Arkema S.A. holds a strong position in acrylic resin through advanced coating materials, water-based resin systems, and specialty acrylic solutions. The company continued strengthening production capabilities and expanding sustainable product offerings across industrial and construction sectors. In 2024, Arkema recorded approximately €9.5 billion in sales and continued directing investment toward specialty materials.

The Dow Chemical Company continued expanding its presence in acrylic resin applications through coating materials, binders, and advanced formulation technologies. Its product portfolio supports industries including packaging, construction, transportation, and consumer markets. In 2024, Dow generated approximately USD 43 billion in net sales while maintaining broad manufacturing operations globally.

Top Key Players Outlook

- BASF SE

- Arkema S.A.

- The Dow Chemical Company

- Mitsubishi Chemical Holdings Corporation

- Evonik Industries AG

- Nippon Shokubai Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Allnex Group

- LG Chem Ltd.

- Asahi Kasei Corporation

- Mitsui Chemicals, Inc.

- Solvay S.A.

- Huntsman Corporation

- DIC Corporation

Recent Developments

Nippon Shokubai Co., Ltd. plays an important role in the acrylic resin value chain through acrylic acid, acrylates, special acrylates, acrylic copolymers, and paint-resin raw materials, which are used in coatings, adhesives, construction materials, electronics, and hygiene products. In FY2025 ended March 31, 2025, its Materials Business revenue increased 3.6% to ¥294,092 million, supported by higher sales volume and selling prices for acrylic acid and acrylates; operating profit rose 1.3% to ¥12,900 million.

In 2025 Sumitomo Chemical’s updates included acquisition-related moves in electronics and advanced materials, including a South Korean wireless communication module company acquisition and an LCP resin business intangible asset acquisition, supporting its broader specialty materials shift. Financially, Sumitomo Chemical reported ¥2,606.3 billion sales revenue in FY2024, while Q1 FY2025 sales revenue was ¥526.1 billion; this gives the company a strong base to scale recycled acrylic resin solutions in premium applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 20.6 Bn |

| Forecast Revenue (2035) | USD 38.3 Bn |

| CAGR (2026-2035) | 6.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Chemistry (Acrylates, Methacrylates, Hybrid acrylics, Other Chemistries), By Solvency (Water-based Acrylic Resins, Solvent-based Acrylic Resins, Other solvencies), By Property (Thermoplastic Acrylic Resins, Thermosetting Acrylic Resins, Other properties), By Application (Paints And Coatings, Adhesives And Sealants, Elastomers, DIY / Decorative Coatings, Other applications), By End-use (Building And Construction, Automotive, Paper And Paperboard, Consumer Goods, Electrical And Electronics, Packaging, Other applications) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | BASF SE, Arkema S.A., The Dow Chemical Company, Mitsubishi Chemical Holdings Corporation, Evonik Industries AG, Nippon Shokubai Co., Ltd., Sumitomo Chemical Co., Ltd., Allnex Group, LG Chem Ltd., Asahi Kasei Corporation, Mitsui Chemicals, Inc., Solvay S.A., Huntsman Corporation, DIC Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |