Quick Navigation

Report Overview

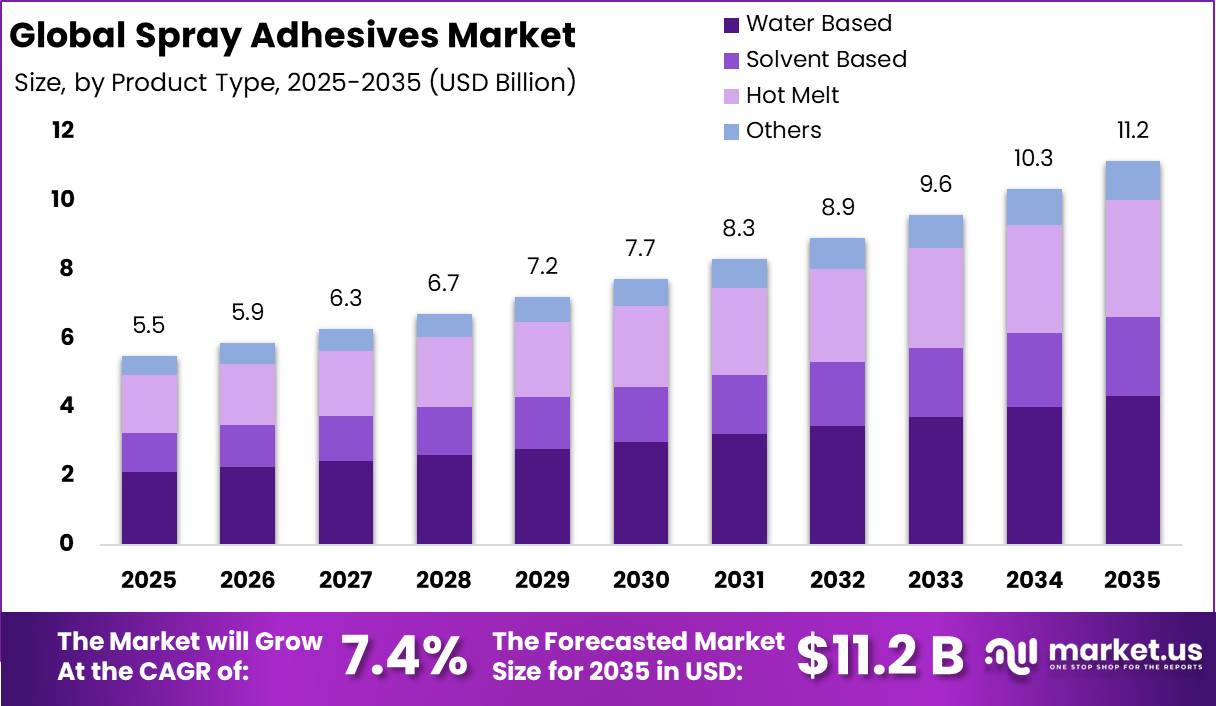

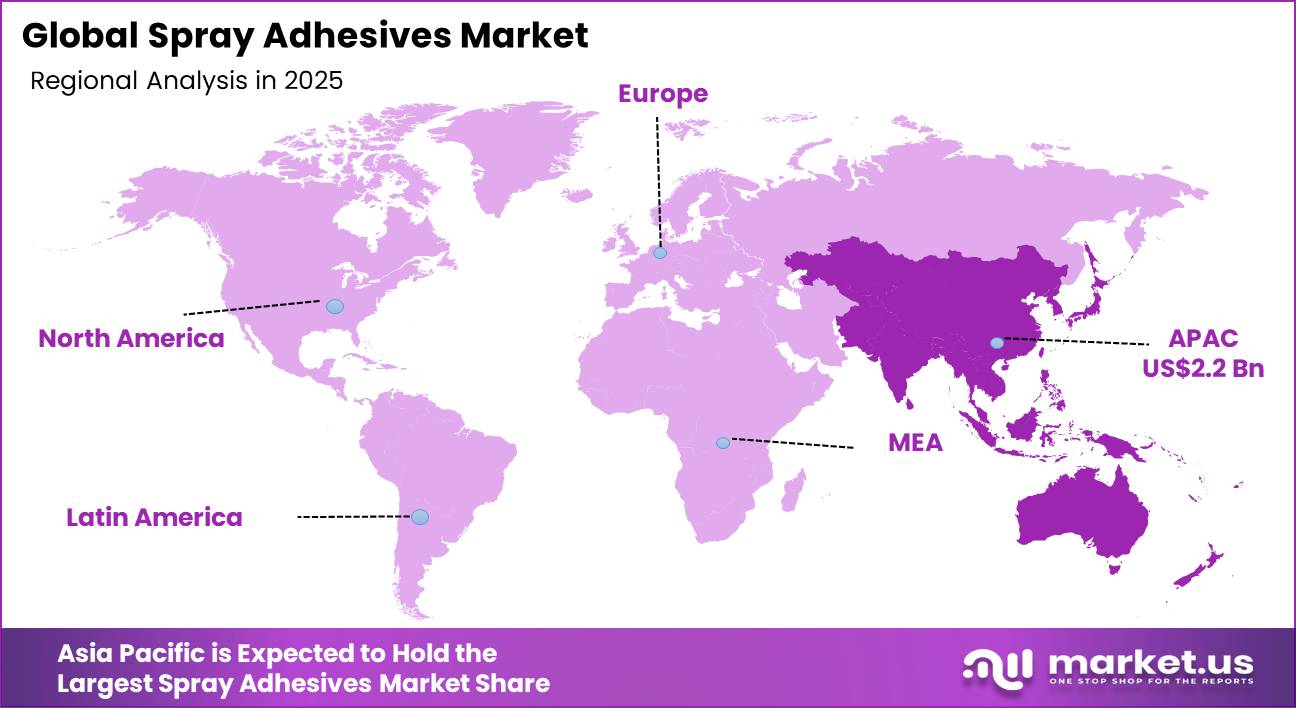

The Global Spray Adhesives Market size is expected to be worth around USD 11.2 Billion by 2035, from USD 5.5 Billion in 2025, growing at a CAGR of 7.4% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 39.8% share, holding USD 22.3 Billion revenue.

Spray adhesives have emerged as versatile bonding solutions across construction, automotive, furniture, packaging, textile, and leather industries due to their ease of application, uniform coverage, and compatibility with diverse materials. Product innovation, including water-based, solvent-based, and hot-melt formulations, is increasingly driven by regulatory compliance with VOC limits and environmental standards, as well as the demand for sustainable and high-performance bonding.

Key Takeaways

- The global spray adhesives market was valued at USD 5.5 billion in 2025.

- The global spray adhesives market is projected to grow at a CAGR of 7.4% and is estimated to reach USD 11.2 billion by 2035.

- On the basis of product type, water-based spray adhesives dominated the market, constituting 38.7% of the total market share.

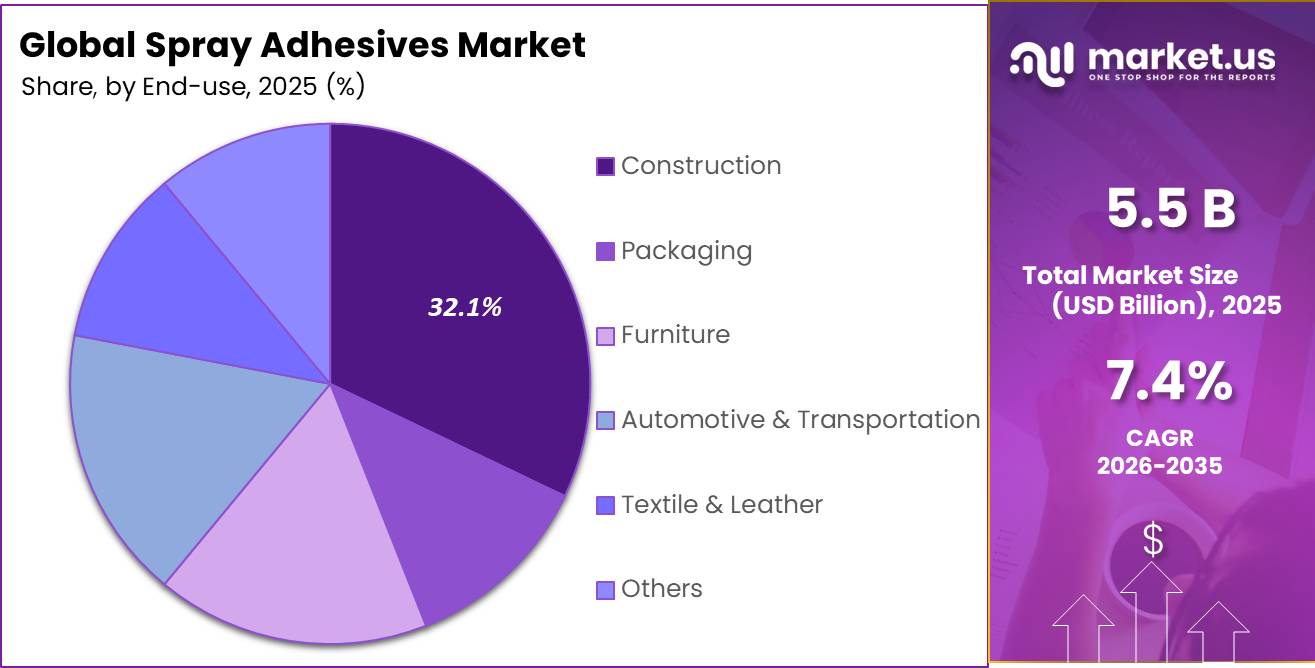

- Among the applications, the construction sector held a major share in the spray adhesives market, 32.1% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the spray adhesives market, accounting for 39.8% of the total global consumption.

Rapid urbanization and industrial growth in the Asia-Pacific, alongside rising automotive production and modular construction initiatives, have positioned the region as a key adopter. Geopolitical tensions and supply chain disruptions affecting raw materials, such as solvents and polymer precursors, have prompted manufacturers to adjust sourcing, reformulation, and inventory strategies.

Adoption of automation and precision dispensing technologies, combined with tailored client solutions and technical support, strengthens operational efficiency and customer loyalty. Collectively, regulatory alignment, technological innovation, and emerging market expansion define the current landscape and strategic direction of the spray adhesives sector.

Product Type Analysis

Water-Based Spray Adhesives are a Prominent Segment in the Market.

Water-based spray adhesives hold a dominant position, accounting for 38.7% of the market, driven by their versatility, environmental compliance, and performance across multiple applications. These adhesives are preferred in construction, furniture, packaging, and textile sectors due to their low volatile organic compound (VOC) content, aligning with stringent regulatory frameworks such as the U.S. EPA and European Union VOC standards.

Their ability to bond diverse substrates, including laminates, foams, fabrics, and lightweight panels, without compromising indoor air quality, makes them especially suitable for residential, commercial, and industrial projects. In addition, water-based formulations offer ease of handling, reduced flammability, and efficient cleanup compared to solvent-based alternatives. Increasing adoption in modular construction, automotive interior assembly, and environmentally conscious manufacturing initiatives reinforces their prominence, positioning water-based spray adhesives as the preferred solution for companies balancing performance, sustainability, and regulatory compliance.

Application Analysis

Spray Adhesives Are Widely Utilized in the Construction Sector.

The construction segment represents the largest share at 32.1%, reflecting the critical role of spray adhesives in modern building and infrastructure projects. These adhesives are widely employed for bonding insulation panels, laminates, wall claddings, and lightweight composite materials, improving both structural integrity and installation efficiency. Their rapid application and uniform coverage reduce labor time while enabling precise assembly in modular and prefabricated construction, which is increasingly adopted in urban development projects.

Compliance with environmental regulations, including low VOC emissions, makes spray adhesives suitable for indoor and commercial spaces where air quality standards are stringent. Government initiatives in emerging markets, such as India’s Smart Cities Mission, and the expansion of urban infrastructure in China and Southeast Asia, have further accelerated adoption. The combination of performance, sustainability, and operational efficiency positions the construction segment as a key driver of spray adhesive demand globally.

Key Market Segments

By Product Type

- Water Based

- Solvent Based

- Hot Melt

- Others

By Application

- Construction

- Packaging

- Furniture

- Automotive & Transportation

- Textile & Leather

- Others

Market Dynamics

Driver Analysis - Advanced Spray Adhesives Improve Structural Performance Efficiency

Increasing adoption of spray adhesives in construction, automotive, and furniture sectors is linked to the need for lightweight and durable bonding solutions. According to the U.S. Department of Energy, the transportation sector has reduced vehicle curb weight by 10-15% over the past decade through the use of composite panels and lightweight assemblies, which require adhesives capable of strong yet flexible bonding.

The U.S. General Services Administration (GSA) notes that modular furniture and panel systems in federal facilities increasingly utilize spray-applied adhesives to ensure structural integrity while allowing rapid installation.

In construction, the National Institute of Standards and Technology (NIST) highlights the use of adhesives in bonding insulation panels and laminated timber, improving energy efficiency and mechanical performance. Water-based and hot-melt sprays are frequently specified due to their reduced VOC emissions and compatibility with polymer composites, reflecting a convergence of functional durability and environmental compliance across multiple sectors.

Restraint Analysis - Managing VOC Regulations in Advanced Spray Adhesive Solutions

Regulatory restrictions on volatile organic compounds (VOCs) present operational challenges for spray adhesive manufacturers. The U.S. Environmental Protection Agency (EPA) limits VOC content in architectural coatings and aerosol adhesives to 250 g/L for consumer products and 380 g/L for industrial adhesives under the National Volatile Organic Compound Emission Standards.

- Similarly, the European Union’s Solvents Emissions Directive (2010/75/EU) requires industrial adhesives to maintain VOC emissions below 50 g/m² for wood-based panels, imposing reformulation requirements on solvent-based sprays. Compliance necessitates substituting traditional solvents with water-based or low-VOC alternatives, which can alter adhesive viscosity, open time, and bonding strength, impacting suitability for heavy-duty applications.

The California Air Resources Board (CARB) reports that over 40% of industrial aerosol adhesive products were non-compliant prior to 2019 VOC regulations, prompting extensive product reformulation. These regulatory frameworks drive a shift toward environmentally compatible formulations while increasing technical and operational complexity for manufacturers across multiple sectors.

Opportunity Analysis - Utilizing Urbanization and Industrial Growth to Advance Adhesives

Rapid urbanization and industrialization in emerging economies are creating significant opportunities for the adoption of spray adhesives across multiple sectors. According to the United Nations, the urban population in Asia is projected to reach 3.9 billion by 2030, representing a substantial increase in construction activity and demand for lightweight building materials. The Ministry of Housing and Urban Affairs, Government of India, reports that over 1,000 smart city projects are underway, emphasizing modular construction, prefabricated panels, and interior fixtures, which rely on adhesives for rapid assembly and durability.

In automotive manufacturing, China’s Ministry of Industry and Information Technology (MIIT) indicates that electric vehicle production grew by 45% in 2022, with lightweight composite components requiring precision adhesives. Similarly, Brazil’s National Institute of Metrology, Quality, and Technology (INMETRO) highlights increasing use of bonded furniture and laminates in urban housing projects. These developments collectively point to enhanced material adoption and operational efficiency through spray adhesive integration.

Trend Analysis - Promoting Sustainable Bonding with Water-Based Low-VOC Adhesives

Increasing regulatory pressure and environmental awareness have driven a shift toward water-based and low-VOC spray adhesives. The U.S. Environmental Protection Agency (EPA) sets VOC limits of 250 g/L for consumer aerosol adhesives and 380 g/L for industrial aerosol adhesives under the National Volatile Organic Compound Emission Standards, encouraging manufacturers to reformulate traditional solvent-based products. Similarly, the European Union’s Solvents Emissions Directive (2010/75/EU) mandates VOC content below 50 g/m² for adhesive applications in wood-based panels.

Water-based adhesives also support application in sensitive environments such as schools, hospitals, and indoor construction projects due to lower emissions of hazardous air pollutants. Additionally, the U.S. Department of Energy notes that low-VOC adhesives maintain performance in bonding composite materials and laminates while reducing environmental impact, aligning functional efficiency with sustainability objectives.

Geopolitical Impact Analysis

Navigating Supply Chain Disruptions Amid Geopolitical Tensions in Adhesive Production.

Geopolitical tensions have influenced the supply and distribution of raw materials essential for spray adhesive production. The U.S. Department of Commerce reports that imports of critical solvents and polymer precursors from Eastern Europe and East Asia faced delays of up to 30% during 2022–2023 due to trade restrictions and logistical bottlenecks.

The European Chemicals Agency (ECHA) highlights that restrictions on certain chemical exports from Russia affected the availability of styrene-based resins, commonly used in solvent-based adhesives. In addition, the U.S. Energy Information Administration (EIA) noted that fluctuations in natural gas and crude oil supply, partly driven by geopolitical instability, led to variations in ethylene and propylene feedstock availability, which underpin many hot-melt and solvent-based adhesives.

Transportation and logistics have also been impacted. The United Nations Conference on Trade and Development (UNCTAD) reported a 15% increase in shipping delays for chemical shipments in 2022 due to regional port congestions linked to international sanctions. These disruptions have necessitated adjustments in sourcing strategies, reformulation planning, and inventory management to maintain operational continuity across construction, automotive, and furniture sectors.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Spray Adhesives Market.

In 2025, the Asia Pacific dominated the global spray adhesives market, holding about 39.8% of the total global consumption. The region demonstrates significant adoption of spray adhesives across construction, automotive, furniture, and packaging sectors. The United Nations reports that Asia accounts for nearly 60% of the global urban population, with 2.3 billion people residing in urban areas as of 2020, driving demand for residential and commercial construction materials that utilize adhesives for paneling, laminates, and insulation.

China’s Ministry of Industry and Information Technology (MIIT) indicates that vehicle production reached 26.1 million units in 2022, with increasing use of lightweight composites and interior assemblies requiring precision adhesive bonding. India’s Ministry of Housing and Urban Affairs (MoHUA) notes over 1,000 smart city initiatives emphasizing modular construction and furniture systems that incorporate spray adhesives. Additionally, Japan’s Ministry of Economy, Trade, and Industry (METI) reports extensive use of adhesive-based laminates in electronics and packaging applications. Collectively, rapid urbanization, industrialization, and the adoption of lightweight materials underscore the region’s central role in spray adhesive consumption.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of spray adhesives focus on several strategic activities to strengthen their competitive positioning and enhance market share. A primary approach is product innovation, including the development of water-based, low-VOC, and high-performance formulations suitable for diverse substrates across construction, automotive, furniture, and packaging applications. Operational efficiency is emphasized through automation and precision dispensing technologies, reducing waste and ensuring consistent bonding quality.

Companies also prioritize regulatory compliance by aligning formulations with environmental and safety standards such as VOC limits under the EPA, CARB, and EU directives. Geographic expansion into emerging economies with growing industrial and urban infrastructure allows access to new customer bases. Collaboration with industrial clients for customized adhesive solutions enhances application-specific adoption, while technical support and training programs help end-users optimize product performance, thereby reinforcing brand loyalty and long-term retention.

The Major Players in The Industry

- Henkel Corporation.

- 3M

- B. Fuller Company.

- Avery Dennison Corporation

- Bostik

- ND Industries

- Adhesive Solutions India Pvt.Ltd

- MAAX SOLUTIONS INC

- Great Eastern Resins Industrial Co. Ltd.

- Gemini Adhesives Group

- Fixon Chemical

- Other Key Players

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 5.5 Bn |

| Forecast Revenue (2035) | USD 11.2 Bn |

| CAGR (2026-2035) | 7.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Water Based, Solvent Based, Hot Melt, and Others), By Application (Construction, Packaging, Furniture, Automotive & Transportation, Textile & Leather, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Henkel Corporation, 3M, H.B. Fuller Company, Avery Dennison Corporation, Bostik, ND Industries, Adhesive Solutions India Pvt.Ltd, MAAX SOLUTIONS INC., Great Eastern Resins Industrial Co. Ltd., Gemini Adhesives Group, Fixon Chemical, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |