Quick Navigation

Report Overview

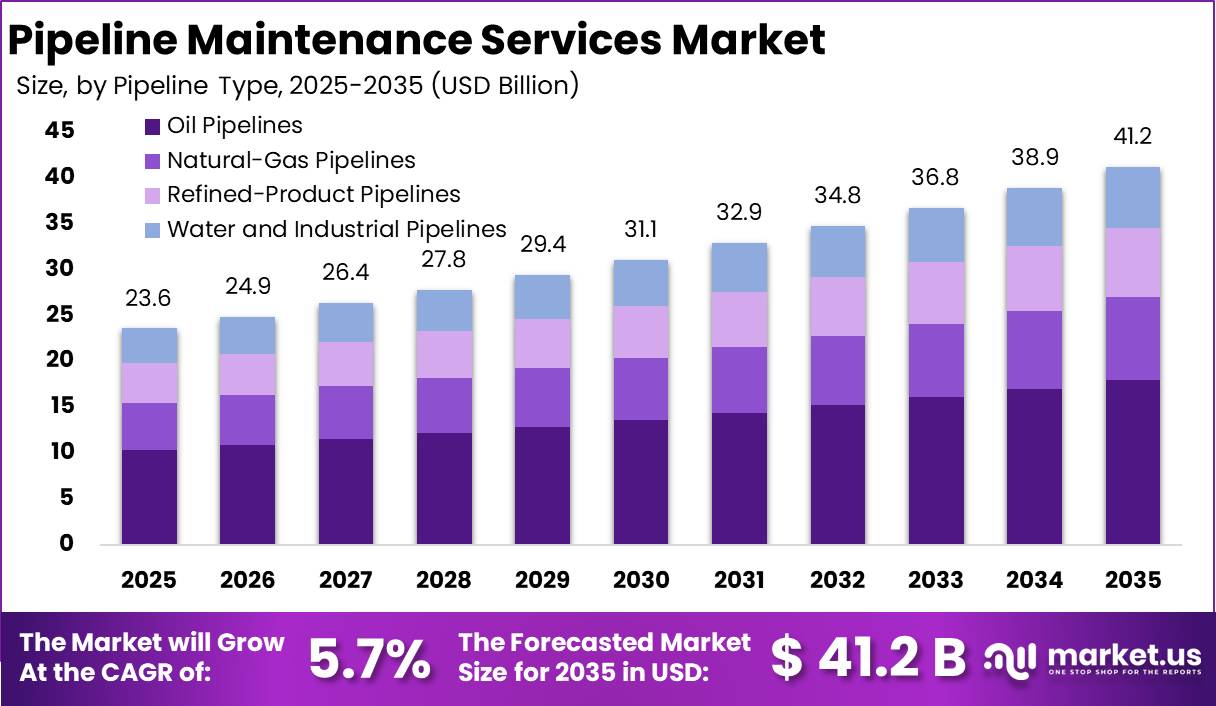

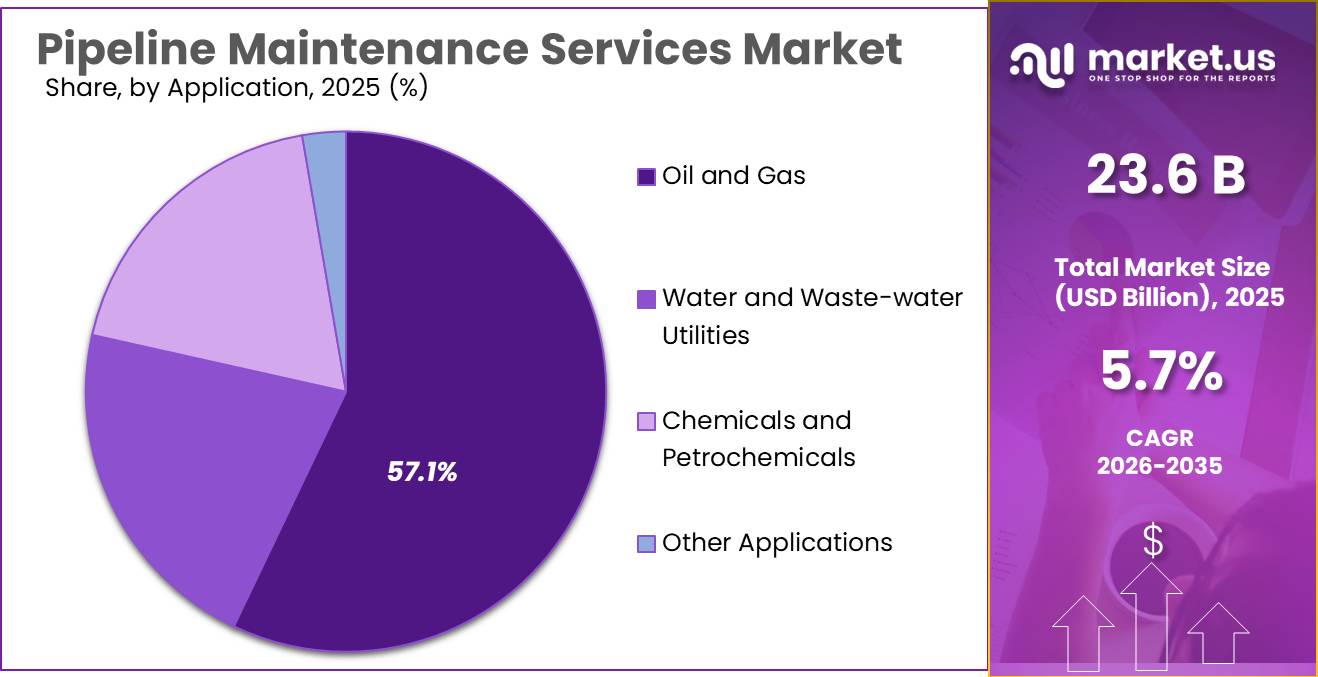

The Global Pipeline Maintenance Services Market size is expected to be worth around USD 41.2 Billion by 2035, from USD 23.6 Billion in 2025, growing at a CAGR of 5.7% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 42.6% share, holding USD 10.0 Billion revenue.

Pipeline maintenance services support the inspection, cleaning, repair, corrosion control, integrity assessment and lifecycle reliability of oil, gas, LNG, water and industrial pipeline networks. The industry is becoming more critical as pipeline systems age and operators face stricter safety, methane-emission and uptime requirements. In the U.S., PHMSA regulates about 3.3 million miles of pipelines, while EIA notes the natural gas network alone is about 3 million miles, with roughly half of mainline transmission pipelines installed in the 1950s–1960s.

The industrial scenario is being shaped by aging assets, LNG expansion, methane regulation and energy-security investments. PHMSA reported 411,827 miles of U.S. natural-gas transmission and gathering systems in 2024, while U.S. agencies state pipelines move about 64% of U.S. energy commodities. This creates recurring demand for pigging, inline inspection, leak detection, hydrotesting, valve maintenance, emergency repair and digital integrity management. In 2025, U.S. natural-gas transmission and gathering systems covered 413,021 miles, including 300,017 transmission miles and 113,005 gathering miles.

Driving factors include corrosion risk, third-party damage, higher throughput, offshore complexity and emission-reduction targets. The IEA’s Global Methane Tracker 2025 highlights leak detection and repair as a proven policy tool, and EU Regulation 2024/1787 requires mandatory methane measurement, reporting, verification and LDAR across oil and gas facilities.

These rules are expected to increase demand for inspection tools, repair crews and data-led preventive maintenance. The IEA states that only around 5% of global oil and gas production currently meets a near-zero methane-emissions standard, while the sector must cut upstream methane intensity from about 1% in 2024 to 0.2% by 2030 under its pathway.

Government support is also strengthening the market. PHMSA announced $86 million in FY2025 grants, including $82 million for Pipeline Safety State Base Grants and $4 million for underground natural-gas storage grants. Such funding supports inspection capacity, state oversight and safer pipeline operations, indirectly expanding demand for specialist maintenance providers.

Baker Hughes Co. remains relevant through its Process & Pipeline Services portfolio, which includes inline inspection, pipeline integrity, pre-commissioning and maintenance services. In March 2025, Baker Hughes received its first technology agreement with Petrobras to develop next-generation flexible pipes targeting a 30-year service life in high-CO₂ environments, directly supporting corrosion-risk mitigation. In July 2025, Baker Hughes also announced a $13.6 billion agreement to acquire Chart Industries at $210 per share, strengthening LNG, hydrogen and carbon-capture infrastructure capabilities.

Key Takeaways

- Pipeline Maintenance Services Market size is expected to be worth around USD 41.2 Billion by 2035, from USD 23.6 Billion in 2025, growing at a CAGR of 5.7%.

- Maintenance held a dominant market position, capturing more than a 56.3% share in the Pipeline Maintenance Services Market.

- Onshore held a dominant market position, capturing more than a 68.2% share in the Pipeline Maintenance Services Market.

- Oil Pipelines held a dominant market position, capturing more than a 43.7% share in the Pipeline Maintenance Services Market.

- Oil and Gas held a dominant market position, capturing more than a 57.1% share in the Pipeline Maintenance Services Market.

- North America held a dominant position in the Pipeline Maintenance Services Market, accounting for 42.6% of the global market and reaching a value of USD 10.0 Billion.

By Type Analysis

Maintenance dominates with 56.3% share due to its essential role in ensuring continuous pipeline performance and reducing operational disruptions.

In 2025, Maintenance held a dominant market position, capturing more than a 56.3% share in the Pipeline Maintenance Services Market. The strong position of this segment was mainly supported by the increasing need to maintain aging pipeline infrastructure, improve operational efficiency, and reduce the risk of unplanned shutdowns. Pipeline operators across oil, gas, water, and industrial networks continued to prioritize regular maintenance activities to extend asset life and meet safety and compliance requirements. Preventive and scheduled maintenance remained widely adopted because it helped lower long-term repair costs and minimized service interruptions.

By Location of Deployment Analysis

Onshore dominates with 68.2% share driven by extensive pipeline networks and consistent maintenance requirements across land-based infrastructure.

In 2025, Onshore held a dominant market position, capturing more than a 68.2% share in the Pipeline Maintenance Services Market. This leading position was supported by the large concentration of pipeline infrastructure located on land, where regular maintenance activities are necessary to ensure uninterrupted operations and asset reliability. Onshore pipelines are widely used across oil, gas, water, and industrial applications, creating steady demand for inspection, cleaning, repair, and monitoring services throughout their operating lifecycle.

By Pipeline Type Analysis

Oil Pipelines dominates with 43.7% share supported by continuous transportation demand and strong focus on pipeline integrity management.

In 2025, Oil Pipelines held a dominant market position, capturing more than a 43.7% share in the Pipeline Maintenance Services Market. This leading share was mainly driven by the extensive use of oil transportation networks and the critical need to maintain uninterrupted flow across production, storage, and distribution systems. Oil pipelines require continuous monitoring and maintenance due to long operating distances, exposure to environmental conditions, and the need to prevent leaks, corrosion, and operational failures.

By Application Analysis

Oil and Gas dominates with 57.1% share driven by continuous pipeline operations and growing focus on asset reliability.

In 2025, Oil and Gas held a dominant market position, capturing more than a 57.1% share in the Pipeline Maintenance Services Market. This strong market presence was supported by the extensive use of pipeline infrastructure across upstream, midstream, and downstream operations, where uninterrupted transportation and operational safety remain essential. Maintenance services continued to play a critical role in ensuring stable flow, preventing leaks, minimizing corrosion, and reducing the risk of unexpected downtime across oil and gas networks.

Key Market Segments

By Type

- Maintenance

- Repair

- Replacement

By Location of Deployment

- Onshore

- Offshore

By Pipeline Type

- Oil Pipelines

- Natural-Gas Pipelines

- Refined-Product Pipelines

- Water and Industrial Pipelines

By Application

- Oil and Gas

- Water and Waste-water Utilities

- Chemicals and Petrochemicals

- Other Applications

Emerging Trends

Adoption of Smart Monitoring and Predictive Maintenance is Emerging as a Major Trend in Pipeline Maintenance Services

One of the latest trends shaping the Pipeline Maintenance Services Market is the rapid adoption of smart monitoring and predictive maintenance technologies. Pipeline operators are increasingly using connected sensors, automated inspection systems, real-time monitoring platforms, and data analytics to identify maintenance needs before failures occur. This approach helps reduce emergency repairs, lower operating costs, and improve infrastructure reliability over long operating periods.

One of the latest trends shaping the Pipeline Maintenance Services Market is the rapid adoption of smart monitoring and predictive maintenance technologies. Pipeline operators are increasingly using connected sensors, automated inspection systems, real-time monitoring platforms, and data analytics to identify maintenance needs before failures occur. This approach helps reduce emergency repairs, lower operating costs, and improve infrastructure reliability over long operating periods.

Expansion of Integrity Management Programs is Changing Long-Term Maintenance Strategies

Another important trend is the growing focus on pipeline integrity management programs supported by government oversight and stricter operational standards. Pipeline operators are increasingly treating maintenance as a continuous process rather than a periodic activity. Integrity management includes regular assessment of pipeline condition, corrosion control, leak prevention, and long-term asset performance tracking.

According to the U.S. Pipeline and Hazardous Materials Safety Administration (PHMSA), the United States pipeline network includes more than 3.3 million miles of pipelines, demonstrating the scale of infrastructure that requires ongoing maintenance and monitoring. With networks operating across long distances and varied environments, companies are expanding preventive maintenance strategies to maintain safety and operational continuity.

Drivers

Growing Food Processing and Cold Chain Infrastructure is Increasing Demand for Pipeline Maintenance Services

One major factor supporting growth in the Pipeline Maintenance Services sector is the rapid expansion of the food processing and cold chain industry, where pipelines are used to move water, steam, dairy liquids, edible oils, beverages, cleaning chemicals and refrigeration fluids. As food production scales up, companies need reliable pipeline systems to avoid leakage, contamination and production stoppages. According to the Food and Agriculture Organization, global food production must increase by around 60% by 2050 to meet future demand.

At the same time, the Government of India reported that the country’s food processing sector contributes nearly 13% of manufacturing Gross Value Added (GVA) and about 8% of total industrial output, creating larger processing networks that depend on regular pipeline inspection and maintenance. Expansion of industrial food plants means more cleaning cycles, corrosion checks, leak testing and preventive servicing. For pipeline maintenance providers, this creates long-term service demand because food facilities cannot risk downtime or product quality issues.

Government Investment in Water and Food Supply Networks is Expanding Maintenance Needs

Another strong driver is rising public investment in water transport and food-support infrastructure, which directly increases the need for pipeline maintenance services. Modern food industries rely heavily on stable water delivery systems, wastewater pipelines and utility networks. According to the World Bank, nearly US$114 billion per year is needed globally to meet water infrastructure requirements.

In India, the Government’s Jal Jeevan Mission aims to provide tap water access across rural households and has already connected more than 15 crore (150 million+) households. Larger pipeline networks automatically increase the requirement for inspection, cleaning, leak detection and repair services throughout the operating life of these systems. Maintenance is becoming a planned operating activity instead of a reactive cost because governments and industries want uninterrupted supply and lower water losses.

Restraints

High Maintenance Cost and Skilled Labour Shortage

One major restraint for the pipeline maintenance services market is the high cost of inspection, repair and replacement work. Pipeline operators cannot delay maintenance, but the work often needs advanced tools, trained technicians and shutdown planning. This makes service spending heavy, especially for aging networks. PHMSA states that the U.S. regulated pipeline system includes more than 3.4 million miles of pipelines, showing how large the maintenance burden can become.

It also reported 413,021 miles of natural gas transmission and gathering pipelines in 2025. At this scale, even small repair delays can increase safety risk and operating cost. Skilled manpower is another pressure point because corrosion checks, pigging, welding, leak detection and integrity testing need certified workers, not general labour. This makes pipeline maintenance expensive and sometimes slow, especially in remote or offshore areas.

Stricter Safety and Methane Rules Increase Compliance Pressure

Pipeline maintenance companies are also restrained by stricter safety and emissions rules. These rules are needed, but they raise the cost of monitoring, documentation and repair. The International Energy Agency reported that global upstream oil and gas methane intensity was around 1% in 2024, but it must fall to about 0.2% by 2030 in its pathway. This means operators must spend more on leak detection, repair systems, methane monitoring and faster response teams.

PHMSA also moved in 2025 to seek feedback on repair criteria for hazardous liquid and gas transmission pipelines, showing that regulation is still tightening. For service providers, this creates opportunity, but for buyers it becomes a restraint because every repair must meet higher technical and reporting standards. Smaller operators may delay non-urgent work due to budget limits, which can slow service adoption.

Opportunity

Food Processing Expansion Creates New Maintenance Work

A major growth opportunity for Pipeline Maintenance Services is the fast expansion of food processing plants, where pipelines carry water, steam, milk, edible oils, beverages, cleaning fluids and wastewater. These lines must stay clean and safe because one leak or blockage can stop production and affect food quality.

The Food and Agriculture Organization says global food production may need to rise by about 70% by 2050 to feed 9.1 billion people. This means more factories, more utility lines and more planned pipeline servicing. In India, the food processing sector contributed 7.93% of manufacturing GVA and 20.4% of agri-food exports in 2024–25. This gives maintenance companies a clear opening in inspection, cleaning, corrosion checks and leak detection.

Government Food Infrastructure Schemes Add Long-Term Service Demand

Government spending on food parks, cold chains and processing units is another strong opportunity. India’s PM Kisan SAMPADA Yojana is expected to bring Rs. 11,095.93 crore of investment, benefit 28,49,945 farmers, and create 5,44,432 direct and indirect jobs by 2025–26. These projects need hygienic pipelines for chilled water, refrigeration, steam, processing liquids and wastewater. As these assets get older, they need regular inspection, flushing, pressure testing and repair, which creates repeat business for pipeline maintenance firms.

The opportunity is not only during construction; it continues for years because food plants must meet safety rules and avoid shutdowns. For service providers, the best growth area is preventive maintenance contracts with cold chain units, dairy plants, beverage makers and food parks.

Regional Insights

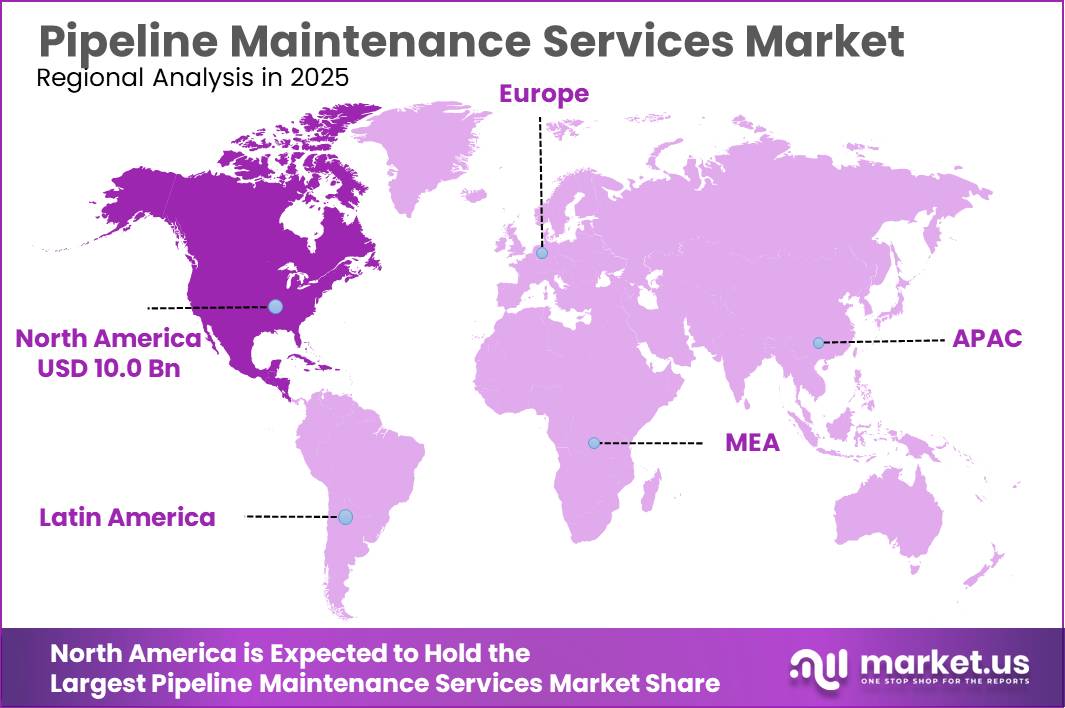

North America dominated the Pipeline Maintenance Services Market with a 42.6% share, valued at USD 10.0 Billion.

In 2025, North America held a dominant position in the Pipeline Maintenance Services Market, accounting for 42.6% of the global market and reaching a value of USD 10.0 Billion. The region’s leadership was supported by its extensive pipeline infrastructure, mature energy network, and continuous investment in maintaining operational efficiency and pipeline integrity. North America remains one of the largest markets for oil and gas transportation, creating steady demand for inspection, cleaning, corrosion management, repair, and integrity assessment services.

The United States contributed significantly to regional growth due to its large pipeline network and strong focus on infrastructure reliability. According to government pipeline records, the U.S. operates more than 3.3 million miles of pipeline infrastructure covering natural gas, hazardous liquids, and other transportation systems. Such a large installed base requires ongoing maintenance programs to reduce leak risks, prevent unplanned outages, and comply with evolving safety standards. In addition, regulatory oversight and regular inspection requirements continue to encourage long-term service adoption across operators.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Baker Hughes Co. maintains a strong position in the pipeline maintenance services market through pipeline integrity management, inspection technologies, asset performance monitoring, turbomachinery solutions and digital diagnostics. The company supports operators in reducing downtime and extending pipeline life cycles. In 2025, Baker Hughes reported US$27.7 billion revenue, operated across 120+ countries, and employed approximately 56,000 employees, demonstrating strong operational scale for maintenance and industrial service deployment. The company continues expanding energy technology and infrastructure capabilities through strategic portfolio development.

Shell Plc plays an important role in pipeline maintenance through integrated upstream, LNG, transportation and asset reliability operations. The company focuses on predictive maintenance, digital monitoring and infrastructure optimization to improve flow assurance and reduce operational risk across pipeline assets. In 2025, Shell generated approximately US$266.9 billion revenue, reported US$18.1 billion net income, employed around 96,000 people, and maintained operations across 70+ countries, supporting long-term maintenance and integrity requirements globally.

Top Key Players Outlook

- Baker Hughes Co.

- Shell Plc

- ExxonMobil Corp.

- BP Plc

- TD Williamson Inc.

- STATS Group

- Rosen Group

- EnerMech Ltd

- IKM Gruppen AS

- Kinder Morgan Inc.

- TransCanada

- Enbridge Inc.

- Pure Technologies

- NDT Global

- Chevron Corp.

- Quest Integrity

- Intertek Group Plc

- Dacon Inspection Services

Recent Industry Developments

In 2026, EnerMech won a Saipem Whiptail subsea pre-commissioning contract in Guyana, covering flooding, cleaning, hydrotesting and umbilical testing, while adding new equipment such as remote flooding units and subsea test pumps. Company data shows about $510.9 million revenue, 1,000–5,000 employees, and operations across major global energy hubs.

2025: ExxonMobil Pipeline Company worked on pipeline safety through its Integrity Management Program, which covers inspection, repair, risk control and preventive action, and it partnered with the Mississippi State Fire Academy for CO₂ pipeline emergency-response training; the company also agreed with Enterprise Products to buy a 40% stake in the 550-mile Bahia NGL pipeline and expand capacity from 600,000 barrels/day to 1 million barrels/day.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 23.6 Bn |

| Forecast Revenue (2035) | USD 41.2 Bn |

| CAGR (2026-2035) | 5.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Maintenance, Repair, Replacement), By Location of Deployment (Onshore, Offshore), By Pipeline Type (Oil Pipelines, Natural-Gas Pipelines, Refined-Product Pipelines, Water and Industrial Pipelines), By Application (Oil and Gas, Water and Waste-water Utilities, Chemicals and Petrochemicals, Other Applications) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Baker Hughes Co., Shell Plc, ExxonMobil Corp., BP Plc, TD Williamson Inc., STATS Group, Rosen Group, EnerMech Ltd, IKM Gruppen AS, Kinder Morgan Inc., TransCanada, Enbridge Inc., Pure Technologies, NDT Global, Chevron Corp., Quest Integrity, Intertek Group Plc, Dacon Inspection Services |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |