Quick Navigation

Report Overview

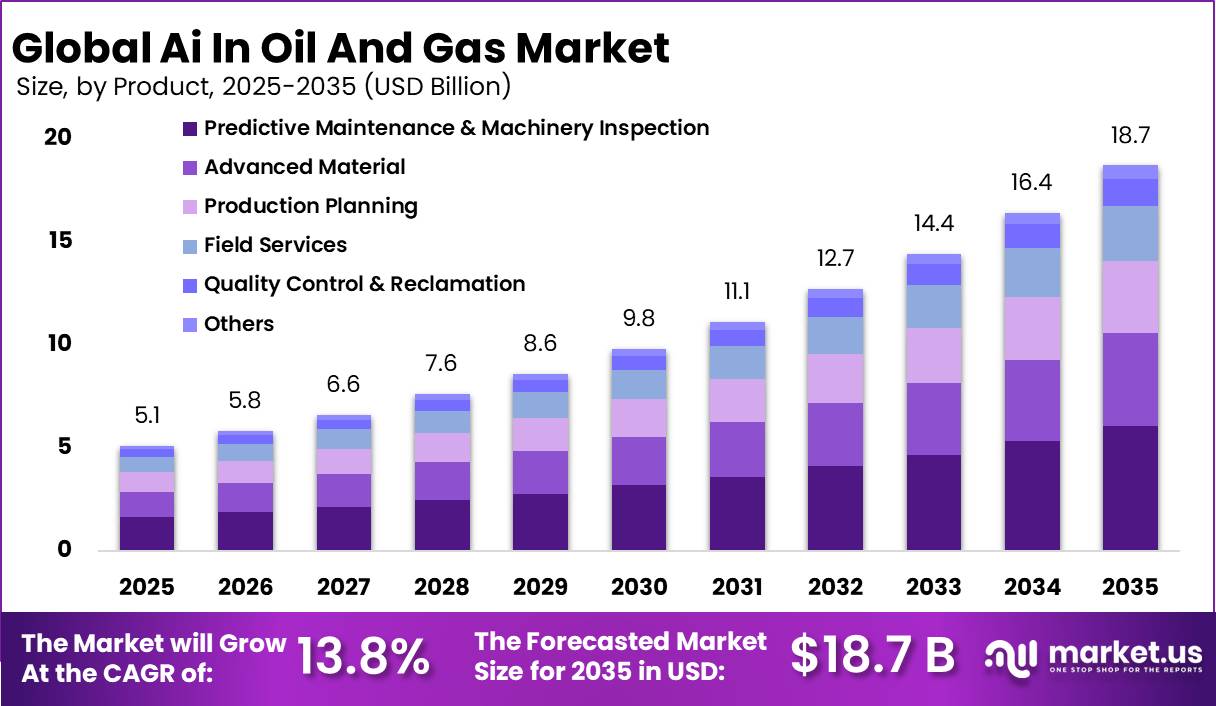

The Global AI in Oil and Gas Market size is expected to be worth around USD 18.7 Billion by 2035, from USD 5.1 Billion in 2025, growing at a CAGR of 13.8% during the forecast period from 2026 to 2035.

AI in oil and gas is entering a practical deployment phase, as operators use machine learning, digital twins, predictive maintenance, computer vision and generative AI to improve exploration, drilling, production, asset integrity, emissions control and supply-chain decisions. The industrial scenario is supported by continued hydrocarbon demand: the IEA forecast global oil demand growth of 730 kb/d in 2025, while EIA projected global demand growth of 0.2 million b/d in 2026 and 105.6 million b/d demand in 2027.

Key Takeaways

- The global AI in Oil and Gas Market is estimated to reach USD 18.7 billion by 2035, with a strong 13.8% Compound Annual Growth Rate (CAGR) from 2026 to 2035.

- Hardware held a dominant market position, capturing more than a 43.40% share in the AI in Oil and Gas market

- Predictive Maintenance & Machinery Inspection held a dominant market position, capturing more than a 32.40% share in the AI in Oil and Gas market.

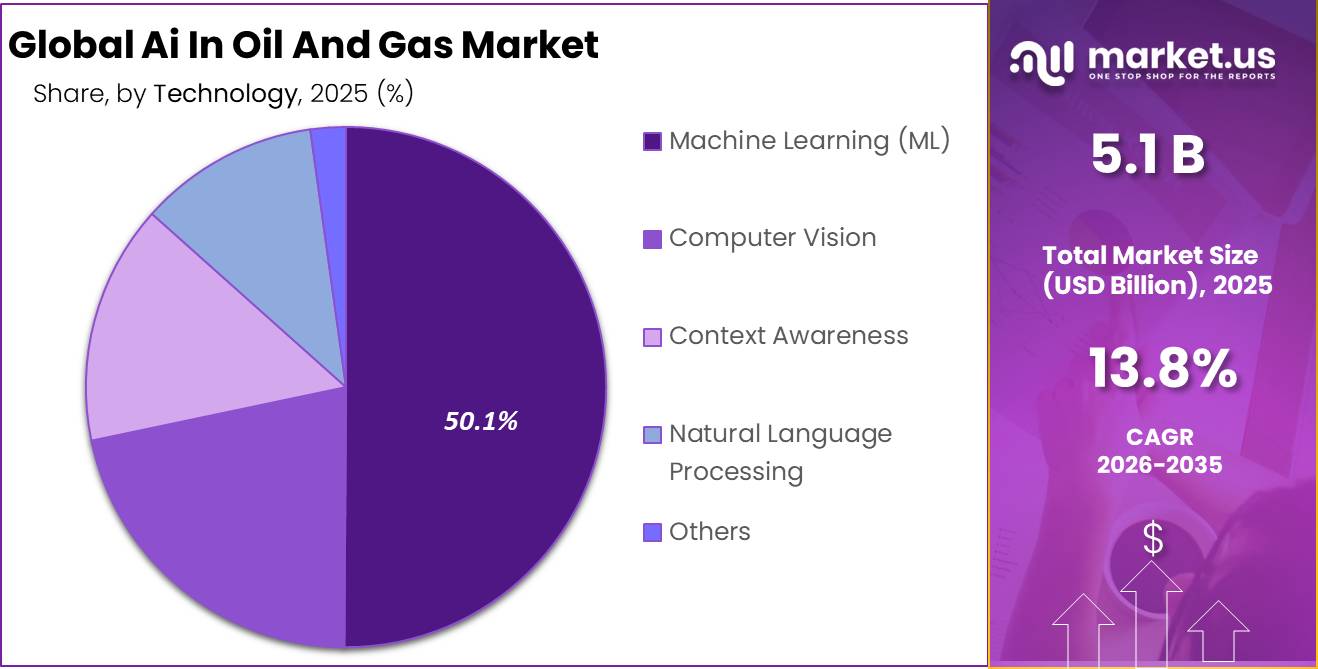

- Machine Learning (ML) held a dominant market position, capturing more than a 50.10% share in the AI in Oil and Gas market.

- Upstream held a dominant market position, capturing more than a 51.80% share in the AI in Oil and Gas market.

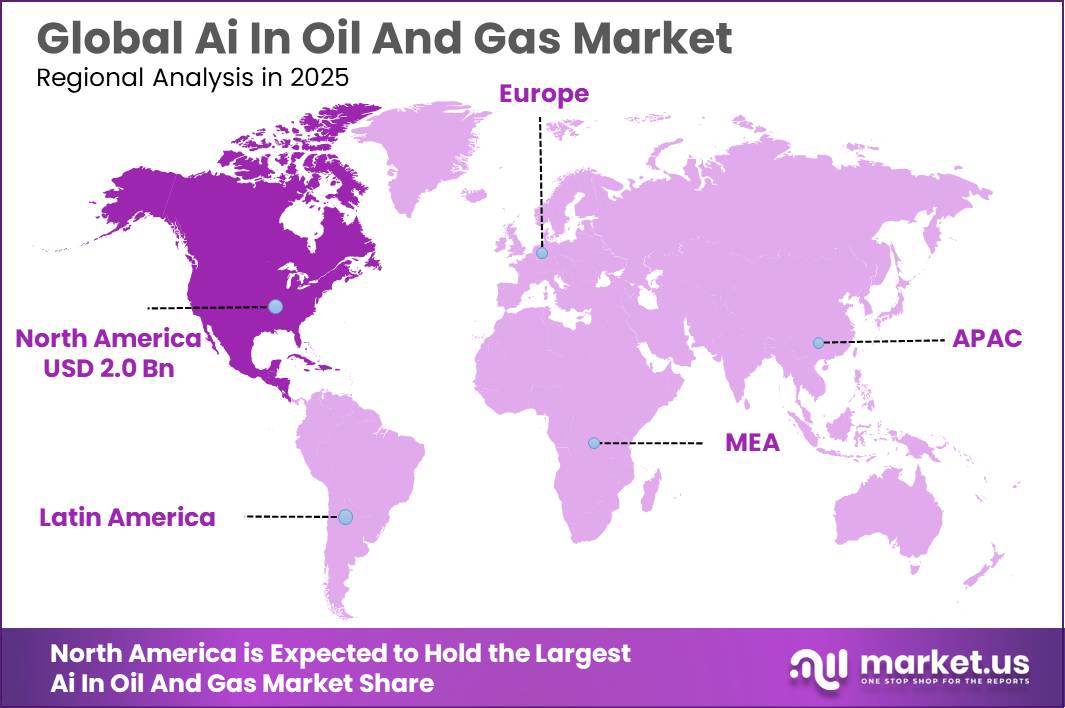

- North America dominated the market in 2023, with over 40.6% market share.

- 92% of oil and gas enterprises worldwide are investing in AI or planning to do so within the next two years.

- 50% of oil and gas executives have already adopted AI-powered solutions to address business challenges.

- AI-driven demand forecasting and pricing optimization solutions contributed to a 10% increase in revenue in the oil and gas sector in 2023.

Adoption is being driven by aging assets, volatile prices, methane regulation and the need to reduce unplanned shutdowns. In methane control, IEA estimated that only around 5% of global oil and gas production meets a near-zero emissions standard, equal to nearly 3 million b/d of oil and 130 bcm of natural gas, creating strong scope for AI-enabled leak detection, satellite analytics and predictive maintenance.

Government and trusted-industry initiatives are reinforcing this shift. The U.S. EPA and DOE announced US$850 million to cut methane pollution from oil and gas, while the Global Methane Pledge targets a 30% methane reduction by 2030. The EU also requires importers, from contracts signed or renewed after 5 August 2030, to prove crude oil, gas or coal methane intensity is below a Commission-set limit.

The oil and gas industry has been embracing artificial intelligence (AI) technologies at a rapid pace. A recent report from Market.us indicates that 92% of oil and gas enterprises worldwide have either started investing in AI or have plans to do so within the next two years. This highlights the industry’s recognition of the potential benefits AI can bring.

In fact, 50% of executives in the oil and gas sector have already implemented AI-powered solutions to address various business challenges. One area where AI has made a significant impact is predictive maintenance, which saw a 28% increase in adoption in 2023. By using AI algorithms to analyze data, companies have been able to detect maintenance issues in equipment and machinery before they lead to costly breakdowns, resulting in substantial cost savings and reduced downtime.

Supply chain management and logistics optimization have also benefited from AI integration in the oil and gas sector. In 2023, the use of AI in these areas resulted in a 12% reduction in operational costs. AI algorithms can analyze complex data sets, optimize routes, and improve inventory management, leading to streamlined operations and cost savings.

In 2025 developments, C3.ai Inc. and Baker Hughes renewed and expanded their joint venture on May 28, 2025, extending a multi-year collaboration to accelerate AI transformation in energy and industrial sectors. C3 AI also reported fiscal 2025 revenue of $389.1 million and projected $447.5 million–$484 million for the next fiscal year, supported by strategic partnerships.

By Component Analysis

Hardware dominates with 43.40% share driven by expanding deployment of AI-enabled field and operational infrastructure

In 2025, Hardware held a dominant market position, capturing more than a 43.40% share in the AI in Oil and Gas market by component. The strong position of hardware was mainly supported by growing investments in physical infrastructure required to run artificial intelligence applications across upstream, midstream, and downstream operations. Oil and gas companies increasingly adopted advanced sensors, edge devices, industrial processors, smart cameras, and high-performance computing systems to collect and process large volumes of operational data in real time.

By Product Analysis

Predictive Maintenance & Machinery Inspection dominates with 32.40% share as operators focus on reducing downtime and improving equipment reliability

In 2025, Predictive Maintenance & Machinery Inspection held a dominant market position, capturing more than a 32.40% share in the AI in Oil and Gas market by product. This leadership was mainly supported by the growing need to improve operational continuity and reduce unexpected equipment failures across oil and gas facilities. Companies increasingly adopted AI-powered monitoring systems to track machinery performance, detect early signs of wear, and schedule maintenance activities before critical breakdowns occurred.

By Technology Analysis

Machine Learning (ML) dominates with 50.10% share as oil and gas companies expand data-driven operational decisions

In 2025, Machine Learning (ML) held a dominant market position, capturing more than a 50.10% share in the AI in Oil and Gas market by technology. The strong position of this segment was driven by the increasing use of data analytics to improve operational performance, reduce inefficiencies, and support faster decision-making across oil and gas activities. Companies adopted machine learning models to process large volumes of operational and geological data, helping teams identify patterns and generate practical insights in less time.

Application Analysis

Upstream dominates with 51.80% share as AI adoption accelerates across exploration and production activities

In 2025, Upstream held a dominant market position, capturing more than a 51.80% share in the AI in Oil and Gas market by application. This leading position was mainly driven by the growing use of artificial intelligence across exploration, drilling, reservoir analysis, and production operations. Oil and gas companies increasingly focused on improving discovery rates, reducing operational uncertainty, and maximizing output from existing assets through intelligent data analysis.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Product

- Advanced Material

- Predictive Maintenance & Machinery Inspection

- Production Planning

- Field Services

- Quality Control & Reclamation

- Others

By Technology

- Machine Learning (ML)

- Computer Vision

- Context Awareness

- Natural Language Processing

- Others

By Application

- Upstream

- Midstream

- Downstream

Emerging Trends

AI for Faster Drilling Decisions

A major latest trend in AI in oil and gas is the use of AI to make drilling faster and more accurate. Operators are using machine learning to watch rig data in real time, study seismic information and guide teams on better drilling choices. In 2025, Reuters reported that Devon Energy achieved a 15% improvement in drilling efficiency by using machine learning models across its U.S. oil rigs.

BP also said AI helped review Gulf of Mexico seismic data in only 8 to 12 weeks, compared with the earlier 6 to 12 months. This shows that AI is no longer only a back-office tool. It is now helping field teams make quicker decisions, reduce delays and lower the risk of expensive drilling mistakes.

Trusted Push from Energy Policy and Technology

This trend is also supported by trusted energy and government action. The International Energy Agency said in 2025 that AI can help improve energy operations, but it also warned that a typical AI-focused data center can use as much electricity as 100,000 households, while the largest ones being built may use 20 times more. This makes efficient AI use very important for oil and gas companies.

In the U.S., the Department of Energy’s Genesis Mission was launched to connect national labs, industry and universities for AI-based breakthroughs in energy, science and security. For oil and gas, this creates a stronger base for digital twins, drilling analytics and safer asset operations.

Drivers

Rising Need to Improve Operational Efficiency and Reduce Equipment Downtime

One of the major driving factors for the AI in Oil and Gas market is the growing pressure on operators to improve operational efficiency while reducing unplanned downtime and production losses. Oil and gas operations generate massive amounts of data every day through drilling systems, pipelines, compressors, processing units, and field equipment. Traditional monitoring methods often make it difficult to convert this data into timely operational decisions.

According to the International Energy Agency (IEA), artificial intelligence is being applied in oil and gas to optimize and automate production processes, detect leaks, and support predictive maintenance activities. These capabilities allow operators to improve asset utilization and reduce unnecessary operational interruptions. The shift is becoming more important as facilities age and companies focus on producing more efficiently from existing assets rather than expanding infrastructure.

AI Adoption Accelerates Due to Emissions Reduction and Regulatory Pressure

Another important factor supporting AI adoption in oil and gas is the growing need to lower emissions and meet environmental performance targets without affecting production output. Operators are increasingly using AI tools for methane monitoring, leak detection, predictive inspection, and process optimization. These technologies help companies identify problems earlier and respond faster across large operational networks.

- According to the International Energy Agency, methane emissions from fossil fuel operations reached nearly 120 million tonnes globally in 2023, making emissions management a priority area for oil and gas companies. The IEA also notes that national oil companies have the potential to reduce methane emissions by up to 30 million tonnes annually by 2030 through faster deployment of monitoring and operational improvements.

Restraints

High Initial Investment and Complex Infrastructure Integration Limit AI Adoption

One of the major restraining factors for the AI in Oil and Gas market is the high upfront investment required to integrate artificial intelligence into existing oil and gas infrastructure. Many operators still rely on aging facilities, legacy control systems, and equipment that were not originally designed for digital connectivity. Moving these operations toward AI-supported environments often requires investment in sensors, edge devices, data platforms, industrial networks, cloud infrastructure, and workforce training, which increases implementation complexity and cost.

- According to the International Energy Agency (IEA), digitalization in oil and gas can reduce production costs by around 10% to 20% and improve operational outcomes, but achieving these gains requires substantial modernization and deployment of connected technologies across field operations. For many operators, especially those managing mature assets, the transition period can slow AI adoption because returns may take time to materialize and operational disruptions must be minimized during deployment.

Data Quality, Operational Reliability, and Emissions Compliance Create Additional Challenges

AI systems depend heavily on continuous and accurate information, but oil and gas operations often involve fragmented datasets collected across multiple systems and facilities. Inconsistent reporting, equipment limitations, and incomplete monitoring reduce the effectiveness of AI-driven decisions.

According to the International Energy Agency’s Global Methane Tracker, fossil fuel operations released more than 120 million tonnes of methane in 2023, showing that monitoring and operational transparency remain difficult despite industry commitments. The report also highlighted that companies and countries continue to under-report actual methane emissions compared with observed estimates. These conditions create uncertainty for AI systems that depend on verified operational inputs and real-time measurements. Until data collection standards and infrastructure become more consistent, AI deployment across oil and gas operations may continue to face slower adoption.

Opportunity

AI-Based Methane Detection and Emission Control

One major growth opportunity for AI in oil and gas is methane detection and emission control. This area is becoming important because methane leakage directly affects safety, operating cost and climate performance.

- The International Energy Agency estimated that the energy sector released about 145 million tonnes of methane in 2024, with oil operations contributing around 45 million tonnes and natural gas operations nearly 35 million tonnes.

AI can help operators read satellite images, sensor data and field equipment signals faster, so leaks can be found before they become larger problems. The IEA also noted that only around 5% of global oil and gas production currently meets a near-zero emissions standard, showing a large gap for digital monitoring and AI-led maintenance tools.

Government Push and Commercial Value

Government and international pressure is making this opportunity more practical. The IEA stated that existing methane pledges could cut fossil-fuel methane emissions by 40% by 2030, although only half are supported by detailed policies and regulations. This creates demand for trusted AI systems that can measure, report and verify emissions. In the U.S., the Department of Energy is also promoting AI through national-lab computing power, scientific data and advanced AI capabilities, which can support better energy-sector analytics.

For oil and gas companies, the benefit is not only compliance. Captured methane can be sold instead of wasted, while fewer leaks can reduce shutdowns and repair costs. This makes AI-based methane management a clear growth opportunity, especially for operators trying to run cleaner and more efficient assets.

Regional Analysis

North America Dominates the AI in Oil and Gas Market (40.6% Share | USD 2.0 Billion)

North America accounted for the dominant position in the AI in Oil and Gas market, representing 40.6% of the global market and valued at USD 2.0 billion. The region’s leadership is supported by strong digital infrastructure, large-scale oil and gas production capacity, and early adoption of industrial artificial intelligence technologies across exploration, drilling, production, refining, and pipeline operations.

The United States remains the major growth engine for regional adoption. According to the U.S. Energy Information Administration (EIA), the country produced an average of 13.2 million barrels per day of crude oil in 2024, maintaining its position among the largest oil-producing nations globally. In addition, U.S. dry natural gas production reached approximately 113 billion cubic feet per day in 2024, creating extensive operational datasets that support AI deployment for predictive maintenance, drilling optimization, asset monitoring, and production forecasting.

Government initiatives continue to strengthen market development. The U.S. Department of Energy (DOE) is expanding AI capabilities through energy innovation programs and national laboratory initiatives focused on industrial efficiency and advanced analytics. Environmental regulations are also encouraging adoption, particularly for methane detection and emissions management. According to the International Energy Agency (IEA), global energy-sector methane emissions reached around 145 million tonnes in 2024, increasing demand for AI-enabled monitoring solutions across North American oil and gas infrastructure.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Microsoft remains one of the largest technology providers supporting AI adoption in oil and gas through cloud computing, industrial data platforms, analytics, and generative AI services. For fiscal year 2025, Microsoft reported USD 281.7 billion in annual revenue, while cloud and AI investments continued expanding globally.

SparkCognition, now operating under the Avathon brand, has strengthened its position in industrial AI with solutions focused on predictive maintenance, asset reliability, industrial autonomy, and operational intelligence for energy-intensive sectors including oil and gas. Founded in 2013, the company operates with an estimated workforce of 201–500 employees and has been associated with industrial AI deployments across critical infrastructure environments.

Top Market Leaders

- IBM Corporation

- C3.ai Inc.

- SparkCognition Inc.

- Uptake Technologies Inc.

- Tachyus Corporation

- Akselos SA

- Microsoft Corporation

- FuGenX Technologies Pvt. Ltd

- Royal Dutch Shell PLC

- PJSC Gazprom Neft

Recent Developments

In January 2025, Tachyus appointed Dr. Jeff Spath as Chairman of the Board, bringing 40 years of energy-sector experience to support its AI-driven reservoir management strategy. In February 2025, Tachyus signed a contract with GeoPark for its Aurion GHG emissions platform, and in April 2025, it signed another agreement with INEOS USA Oil & Gas to deploy Aurion for carbon accounting, monitoring, forecasting and reporting. Its Aurion platform is built around EPA GHGRP and GHG Protocol models, while EPA’s GHGRP covers reporting from over 10,000 facilities, giving Tachyus a strong compliance-focused use case.

In May 2025, Akselos and ABS completed a technical assessment for structural digital twins on FPSOs, supporting safer offshore asset management and real-time integrity decisions. In September 2025, Akselos launched SPM for FPSO 4.0, stating that its structural twin approach could unlock up to 35% OPEX reduction and multi-million-dollar savings for offshore operators. For investment and expansion, GRO completed a follow-on investment in Akselos in September 2025 to expand its SPM platform across oil and gas, offshore wind and large infrastructure.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 5.1 Bn |

| Forecast Revenue (2035) | USD 18.7 Bn |

| CAGR (2026-2035) | 13.8% |

| Base Year for Estimation | 2026 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Hardware, Software, Services), By Product (Advanced Material, Predictive Maintenance And Machinery Inspection, Production Planning, Field Services, Quality Control And Reclamation, Others), By Technology (Machine Learning (ML), Computer Vision, Context Awareness, Natural Language Processing, Others), By Application (Upstream, Midstream, Downstream) |

| Regional Analysis | North America – The U.S. & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands & Rest of Europe; APAC- China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- South Africa, Saudi Arabia, UAE & Rest of MEA |

| Competitive Landscape | IBM Corporation, C3.ai Inc., SparkCognition Inc., Uptake Technologies Inc., Tachyus Corporation, Akselos SA, Microsoft Corporation, FuGenX Technologies Pvt. Ltd, Royal Dutch Shell PLC, PJSC Gazprom Neft |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |