Quick Navigation

Report Overview

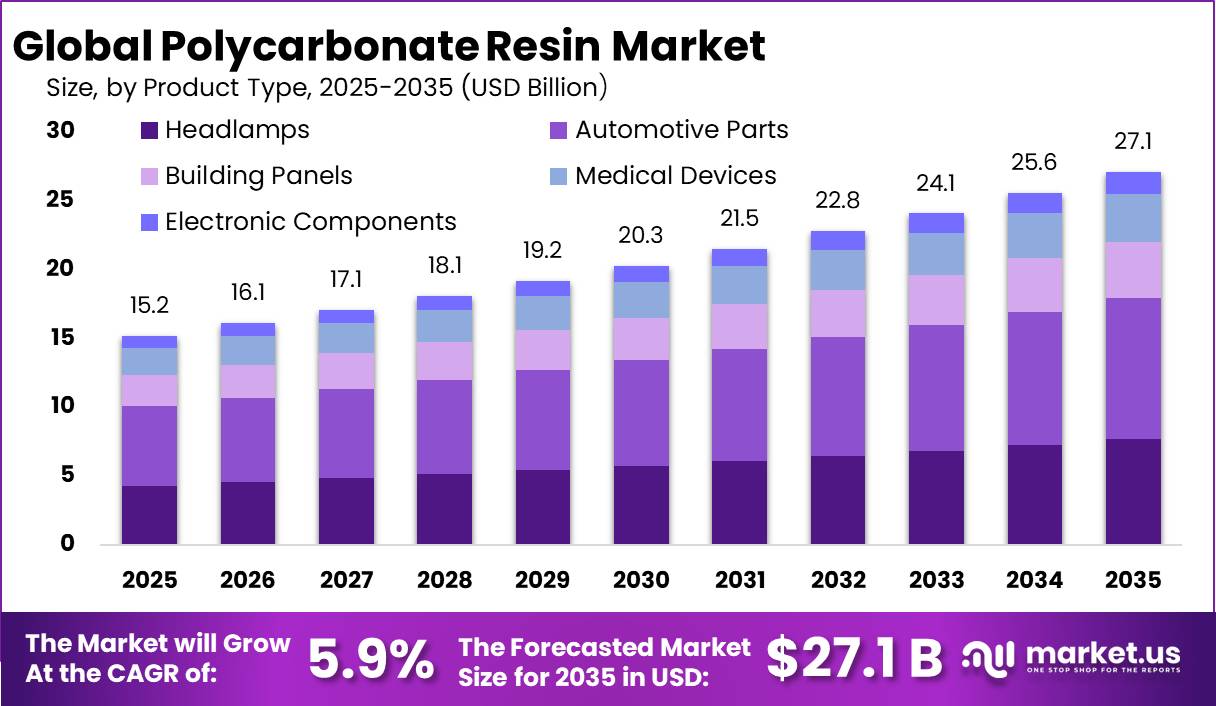

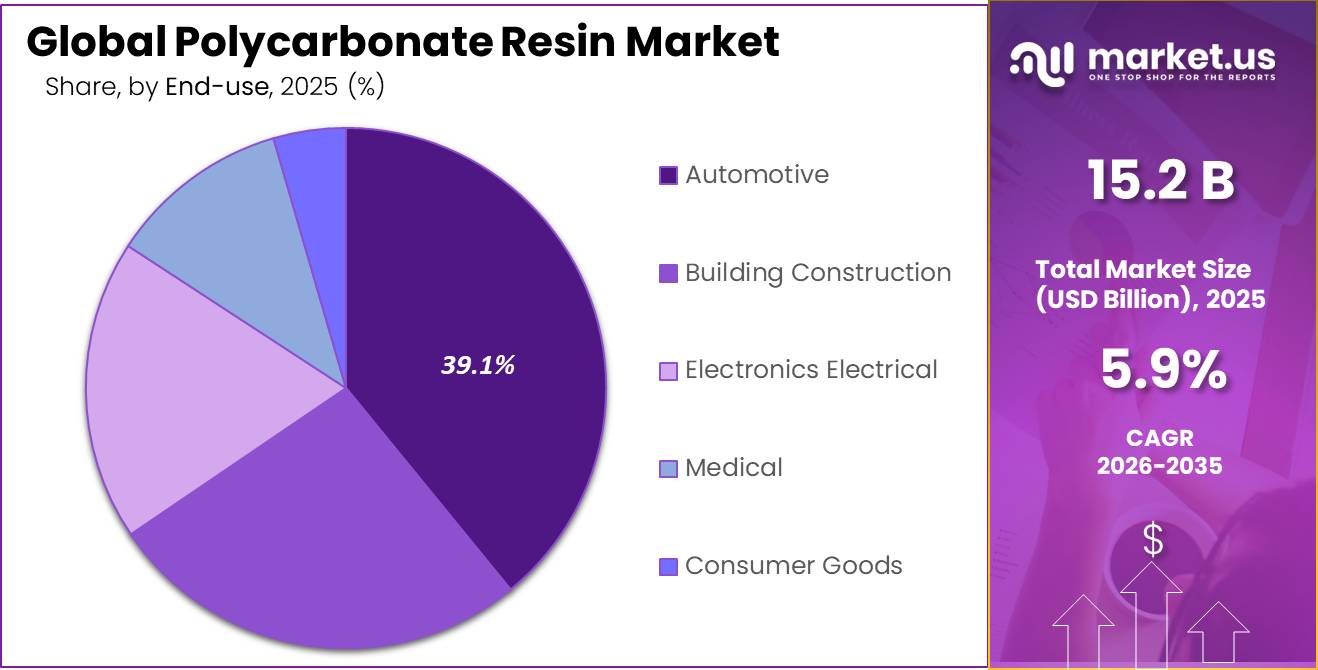

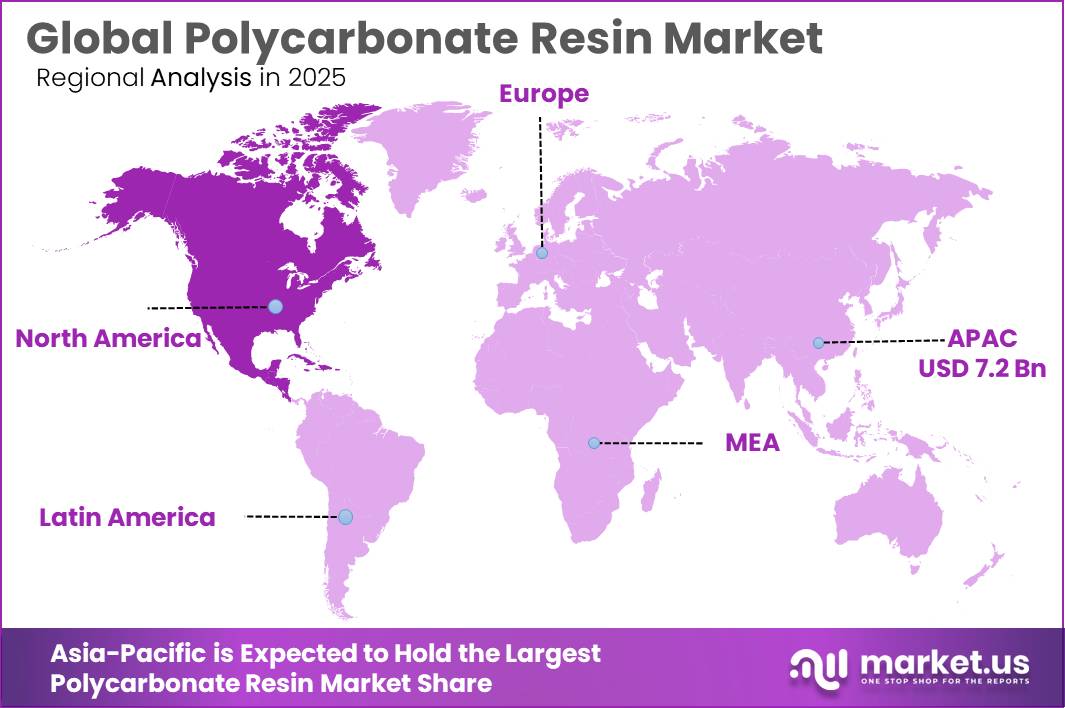

The Global Polycarbonate Resin Market size is expected to be worth around USD 27.1 Billion by 2035, from USD 15.2 Billion in 2025, growing at a CAGR of 5.9% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 46.80% share, holding USD 2.1 Billion revenue.

Polycarbonate resin is a high-performance engineering plastic valued for impact strength, optical clarity, heat resistance, and light weight. It is widely used in automotive glazing and lighting, electrical housings, medical devices, safety equipment, construction sheets, and consumer electronics. In Europe, polycarbonate remains a strategic material: about 730,000 tons of annual demand was recorded in the EEA, while EU facilities had around 1.24 million tons/year of production capacity across Germany, the Netherlands, Spain, and Belgium.

Key Takeaways

- Polycarbonate Resin Market size is expected to be worth around USD 27.1 Billion by 2035, from USD 15.2 Billion in 2025, growing at a CAGR of 5.9%.

- Engineering Plastic held a dominant market position, capturing more than a 74.80% share of the global Polycarbonate Resin market.

- Automotive Parts held a dominant market position, capturing more than a 37.90% share of the global Polycarbonate Resin market.

- Automotive held a dominant market position, capturing more than a 39.10% share of the global Polycarbonate Resin market.

- Asia-Pacific region held the dominant position in the global Polycarbonate Resin market, accounting for 47.80% of the total market and reaching a value of USD 7.2 billion.

The industrial scenario for polycarbonate resin remains linked to mobility, electronics, construction and healthcare. Electric vehicles are a strong demand driver because global electric car sales crossed 20 million units in 2025, up around 20% from 2024, and EVs need lighter, durable materials for lighting, charging systems, displays and battery protection. Electronics also supports demand, as global semiconductor sales reached USD 791.7 billion in 2025, up 25.6% from 2024, helping demand for flame-retardant and dimensionally stable plastic parts in devices, servers and electrical systems.

A key growth driver is the shift toward electric vehicles and lightweight design. The IEA reported that electric car sales exceeded 17 million units in 2024, supporting higher use of flame-retardant, impact-resistant plastics in battery modules, connectors, sensors, display panels, and charging equipment. Circular economy policy is also shaping demand: the European Commission wants all packaging on the EU market to be recyclable in an economically viable way by 2030, while OECD data shows global plastic use could almost triple by 2060, making recyclable and lower-carbon polymers a major long-term opportunity.

Construction is another important outlet, especially for roofing sheets, glazing, safety panels and energy-efficient building materials. The UNEP GlobalABC report states that buildings and construction consume 32% of global energy and account for 34% of global CO₂ emissions, which is pushing material suppliers toward lighter, longer-life and recyclable solutions. This gives polycarbonate resin future growth opportunities in durable glazing, LED lighting, smart buildings and lower-carbon material grades.

Bayer AG is important historically because Bayer MaterialScience became Covestro in 2015; therefore, Bayer is no longer treated as a direct polycarbonate resin producer in the same way Covestro is. Bayer’s 2025 group sales were €45.6 billion, with EBITDA before special items of €9.7 billion, but its current core focus is healthcare and crop science rather than polycarbonate resin.

By Type Analysis

Engineering Plastic dominates with 74.80% share due to its broad industrial adoption and strong performance across automotive, electronics, and construction applications.

In 2025, Engineering Plastic held a dominant market position, capturing more than a 74.80% share of the global Polycarbonate Resin market by type. This leadership was supported by the material’s strong balance of mechanical strength, heat resistance, transparency, and dimensional stability, making it suitable for high-value engineering applications. Polycarbonate engineering plastics continued to gain preference across sectors where lightweight materials with long service life are becoming increasingly important.

By Application Analysis

Automotive Parts dominates with 37.90% share as vehicle manufacturers continue shifting toward lightweight and durable material solutions.

In 2025, Automotive Parts held a dominant market position, capturing more than a 37.90% share of the global Polycarbonate Resin market by application. The segment maintained its leading position due to the growing use of polycarbonate resin in vehicle manufacturing, where material performance, weight reduction, and design flexibility continue to influence purchasing decisions. Polycarbonate resin has become an important engineering material for automotive applications because it combines impact resistance, heat stability, and optical clarity while supporting modern production requirements.

By End-Use Analysis

Automotive dominates with 39.10% share as demand for lightweight, durable, and high-performance materials continues to rise across vehicle manufacturing.

In 2025, Automotive held a dominant market position, capturing more than a 39.10% share of the global Polycarbonate Resin market by end-use. The segment remained the leading consumer of polycarbonate resin as vehicle manufacturers continued adopting advanced materials that support lightweight construction, improved durability, and greater design flexibility. Polycarbonate resin became increasingly important in automotive production due to its ability to combine strength with lower weight compared to traditional materials used in selected vehicle components.

Key Market Segments

By Type

- Engineering Plastic

- Commodity Plastic

By Application

- Headlamps

- Automotive Parts

- Building Panels

- Medical Devices

- Electronic Components

By End-Use

- Automotive

- Building Construction

- Electronics Electrical

- Medical

- Consumer Goods

Emerging Trends

Growing Adoption of Reusable and Circular Packaging Models

One of the latest trends influencing the Polycarbonate Resin market is the growing movement toward circular material use and reusable packaging systems. Industries are increasingly moving away from short-life packaging formats and adopting durable materials that can support repeated use cycles while maintaining performance.

This trend is supported by growing concern around food loss and packaging efficiency. According to the United Nations Environment Programme (UNEP), the world generated approximately 1.05 billion tonnes of food waste in 2022, equivalent to nearly 19% of food available to consumers. As industries focus more on reducing waste across supply chains, durable packaging materials are becoming part of long-term sustainability planning.

Government Policies Accelerating Material Innovation and Recycling

Another important trend is stronger government support for circular economy programs and plastic reduction frameworks that encourage innovation in engineering materials. Manufacturers are increasingly investing in recyclable and longer-life plastic solutions instead of relying only on single-use applications.

National plastic action programs and environmental frameworks have introduced measurable targets for reducing plastic waste and improving recycling systems. For example, policy initiatives highlighted by UNEP include targets such as 30% reduction in plastic waste from industrial and service sectors by 2025 and stronger recycling and recovery mechanisms for durable plastic products.

Drivers

Growing Shift Toward Lightweight Vehicle Manufacturing

One of the major factors supporting growth in the Polycarbonate Resin market is the increasing demand for lightweight yet durable materials across transportation and industrial sectors. Polycarbonate resin continues to gain attention because it combines high impact resistance, transparency, heat stability, and lower weight compared with conventional materials used in selected applications. These characteristics help manufacturers improve product efficiency while reducing overall material load.

The automotive industry remains a key demand center. According to the International Energy Agency (IEA), global electric car sales exceeded 17 million units in 2024, showing continued expansion of vehicle electrification and stronger demand for lightweight component materials. As automakers focus on improving energy efficiency and extending driving range, engineering materials such as polycarbonate resin are increasingly adopted in lighting systems, interior modules, electronic housings, glazing applications, and protective components.

Government Support and Expansion of Advanced Manufacturing Applications

Government policies promoting sustainable manufacturing and energy-efficient mobility are further strengthening polycarbonate resin demand. Across developed economies, industrial initiatives continue encouraging lower-emission production systems and material innovation. Polycarbonate fits these goals because of its long service life, recyclability potential, and ability to replace heavier materials in selected applications.

Beyond transportation, growth in electronics and industrial equipment manufacturing is also creating additional opportunities. Polycarbonate is widely used because of its insulation performance, dimensional stability, and resistance to impact under demanding operating conditions. Industry sources indicate that polycarbonate materials can transmit more than 90% of light, making them suitable for optical and advanced industrial uses where transparency and strength are both required.

Restraints

Tightening Regulations Around Bisphenol-Based Materials

One of the major restraining factors affecting the Polycarbonate Resin market is the growing regulatory focus on bisphenol-based materials and stricter compliance requirements across consumer and industrial applications. Polycarbonate resin is widely valued for strength, transparency, and durability, but regulatory attention on chemical safety is creating additional pressure for manufacturers operating in global markets.

A significant development came from Europe, where authorities introduced stricter measures for food-contact materials containing Bisphenol A (BPA). In 2023, the European Food Safety Authority (EFSA) revised its safety assessment and reduced the tolerable daily intake level for BPA from 4 µg/kg body weight per day to 0.2 ng/kg body weight per day, representing a 20,000-fold reduction in exposure guidance. This regulatory shift later supported broader policy action across food-contact applications.

Higher Transition Costs and Material Substitution Pressure

Another challenge is the rising cost associated with adapting to changing material regulations and replacing established formulations. In December 2024, the European Commission adopted rules restricting BPA use in food-contact materials and introduced an 18-month transition period for industry adaptation. The regulation created additional requirements for product validation, supply chain adjustments, and investment in alternative material development.

For polycarbonate resin producers, this environment may slow adoption in selected applications where compliance standards are becoming more demanding. Manufacturers are increasingly balancing performance advantages with evolving regulatory expectations and long-term sustainability goals. Moving into 2026, continued investment in safer formulations, recycling technologies, and material innovation will remain necessary to maintain competitiveness while meeting changing global requirements.

Opportunity

Rising Demand for Durable and Lightweight Food Packaging Solutions

One of the strongest growth opportunities for the Polycarbonate Resin market is the increasing investment in durable, lightweight, and resource-efficient packaging systems used across food and beverage industries. Food producers and packaging manufacturers continue looking for materials that improve product protection, extend usage cycles, and reduce material consumption.

According to the Food and Agriculture Organization (FAO), approximately 1.05 billion tonnes of food were wasted globally in 2022, equal to nearly 19% of food available to consumers. This growing concern around food loss is increasing attention on stronger packaging materials and improved supply chain efficiency. Polycarbonate-based solutions support this transition by helping maintain product protection and reducing replacement frequency in commercial applications.

Government-Led Circular Economy Programs Supporting Material Innovation

Another major opportunity comes from circular economy policies and investments in advanced manufacturing technologies. Governments and industrial organizations are increasing support for recyclable materials, efficient production systems, and reduced packaging waste. Polycarbonate resin manufacturers are responding by improving recyclability pathways and introducing more sustainable processing methods.

The United Nations Environment Programme (UNEP) reported that global municipal solid waste generation is projected to rise from 2.3 billion tonnes in 2023 to 3.8 billion tonnes by 2050 if current trends continue. This projection is encouraging industries to move toward durable and reusable material platforms that reduce waste intensity over time. Polycarbonate resin aligns with these goals because of its long service life and potential for circular use in selected applications.

Regional Insights

Asia-Pacific dominates the Polycarbonate Resin market with a 47.80% share, reaching USD 7.2 billion due to strong manufacturing activity and expanding end-use industries.

The Asia-Pacific region held the dominant position in the global Polycarbonate Resin market, accounting for 47.80% of the total market and reaching a value of USD 7.2 billion. The region continued to lead because of its large industrial base, strong manufacturing output, expanding automotive production, and growing electronics and construction sectors. Countries across Asia-Pacific have built extensive production ecosystems that support the demand for engineering plastics and advanced polymer materials.

Automotive manufacturing remained one of the strongest contributors to regional growth. Vehicle producers across Asia-Pacific increasingly adopted lightweight materials to improve efficiency, reduce component weight, and support next-generation vehicle development. Polycarbonate resin gained broader acceptance in automotive lighting, interior systems, electronic housings, and transparent structural applications because of its durability and flexibility.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Bayer AG maintains a historical presence in the polycarbonate value chain through its legacy materials business and continued focus on advanced material applications. In 2025, the company continued emphasizing resource efficiency, advanced manufacturing, and technology-driven production models across multiple industrial sectors. Bayer reported group sales of approximately EUR 46.6 billion in 2025, reflecting broad industrial and technology operations.

Covestro AG remains one of the leading global producers of polycarbonate materials and advanced polymer solutions. In 2025, Covestro continued expanding sustainability-focused production and alternative raw material initiatives. The company reported annual sales of approximately EUR 14.2 billion, while operating manufacturing facilities across multiple regions to support global material demand and supply efficiency.

Chi Mei Corporation is an established producer of engineering plastics with strong capabilities in polycarbonate and specialty resin manufacturing. In 2025, Chi Mei continued strengthening production efficiency and expanding value-added material offerings. The company maintained annual revenue exceeding TWD 100 billion, supported by integrated manufacturing operations and export-oriented industrial supply across Asia and international markets.

Top Key Players Outlook

- Bayer AG (DE)

- Covestro AG (DE)

- Chi Mei Corporation (TW)

- SABIC (SA)

- Teijin Limited (JP)

- LG Chem (KR)

- Trinseo S.A. (US)

- Royal DSM (NL)

- Dow Chemical Company

- Asahi Kasei Corporation

- Huntsman Corporation

Recent Industry Developments

LG Chem reported 2025 consolidated revenue of KRW 45.9322 trillion and operating profit of KRW 1.1809 trillion, showing stronger profit recovery despite lower sales. In 2025, its Advanced Materials business remained important, while the company also moved toward restructuring its petrochemical operations under South Korea’s industry-efficiency push.

In 2025, Trinseo S.A. move was an investment and agreement in China, where Trinseo signed a project in Zhangjiagang for a recycled polycarbonate project worth about USD 20 million, with Phase I planned at 5,000 tons per year capacity. In financial terms, Trinseo reported Engineered Materials net sales of USD 293 million in Q2 2025, while Q1 2025 adjusted EBITDA included USD 26 million from polycarbonate technology licensing income.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 15.2 Bn |

| Forecast Revenue (2035) | USD 27.1 Bn |

| CAGR (2026-2035) | 5.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Engineering Plastic, Commodity Plastic), By Application (Headlamps, Automotive Parts, Building Panels, Medical Devices, Electronic Components), By End-Use (Automotive, Building Construction, Electronics Electrical, Medical, Consumer Goods) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Bayer AG, Covestro AG, Chi Mei Corporation, SABIC, Teijin Limited, LG Chem, Trinseo S.A., Royal DSM, Dow Chemical Company, Asahi Kasei Corporation, Huntsman Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |