Quick Navigation

Report Overview

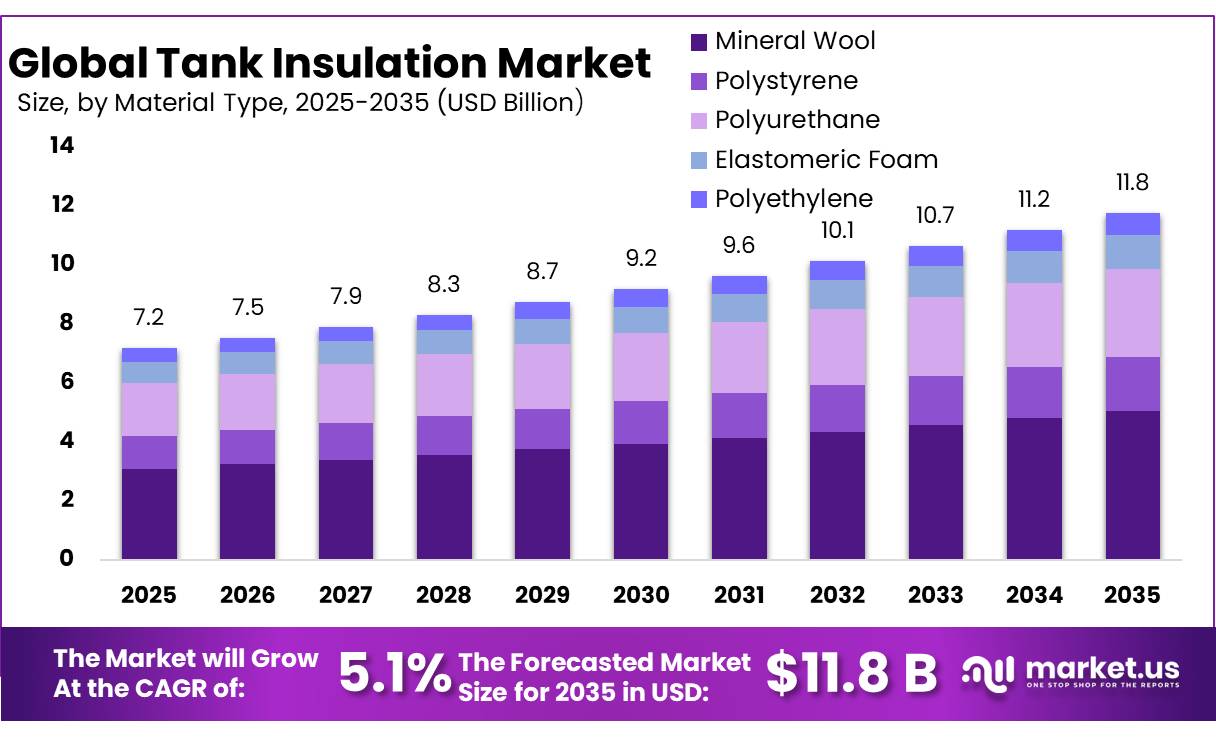

The Global Tank Insulation Market size is expected to be worth around USD 11.8 Billion by 2035, from USD 7.2 Billion in 2025, growing at a CAGR of 5.1% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 46.8% share, with USD 2.1 Billion in revenue.

The tank insulation market is shaped by the need to maintain thermal stability in storage and transportation systems handling liquids and gases across a wide temperature spectrum, from cryogenic hydrogen and LNG to moderately heated industrial fluids. Demand is closely tied to energy infrastructure expansion, chemical processing, and regulated sectors such as food, pharmaceuticals, and water treatment. Insulation systems are applied across storage tanks and transport tanks, supporting both new installations and retrofit projects aimed at improving efficiency and compliance.

- The International Energy Agency reports that around 345 billion cubic metres per year (bcm/yr) of new LNG export capacity is expected to become operational between 2025 and 2030, representing the largest capacity expansion phase on record.

Material selection spans mineral wool, polystyrene, polyurethane, elastomeric foams, polyethylene, and emerging high-performance options such as aerogels and cellular glass. These materials are chosen based on operating temperature, mechanical durability, and energy efficiency requirements. Increasing focus on energy conservation and emissions reduction is reinforcing the adoption of advanced insulation solutions that minimize heat loss and operational costs.

- According to the International Energy Agency (IEA), global hydrogen demand increased to almost 100 million tons (Mt) in 2024, up 2% from 2023 and in line with overall energy demand growth.

Asia Pacific remains a dominant demand center, driven by large-scale hydrogen deployment and LNG infrastructure development, particularly in China and Southeast Asia. Growing investments in clean energy storage, alongside expansion in oil & gas and chemical industries, continue to underpin long-term requirements for efficient and durable tank insulation systems globally.

- According to the IEA’s World Energy Investment 2025 report, global energy investment is set to reach a record US$3.3 trillion in 2025, with clean energy capturing US$2.2 trillion double the investment in fossil fuels, US$ 1.1 trillion).

Key Takeaways

- The global tank insulation market was valued at USD 7.2 billion in 2024.

- The global tank insulation market is projected to grow at a CAGR of 5.1% and is estimated to reach USD 11.8 billion by 2034.

- On the basis of material type, mineral wool dominated the market, constituting 42.9% of the total market share.

- Based on the temperature range, medium temperature insulation (0°C to 100°C) dominated the tank insulation market, with a substantial market share of around 34.1%.

- Based on the installation type, new installations of tank insulation led the market, comprising 64.6% of the total market.

- Among the applications, storage tanks held a major share in the tank insulation market, with 70.3% of the market share.

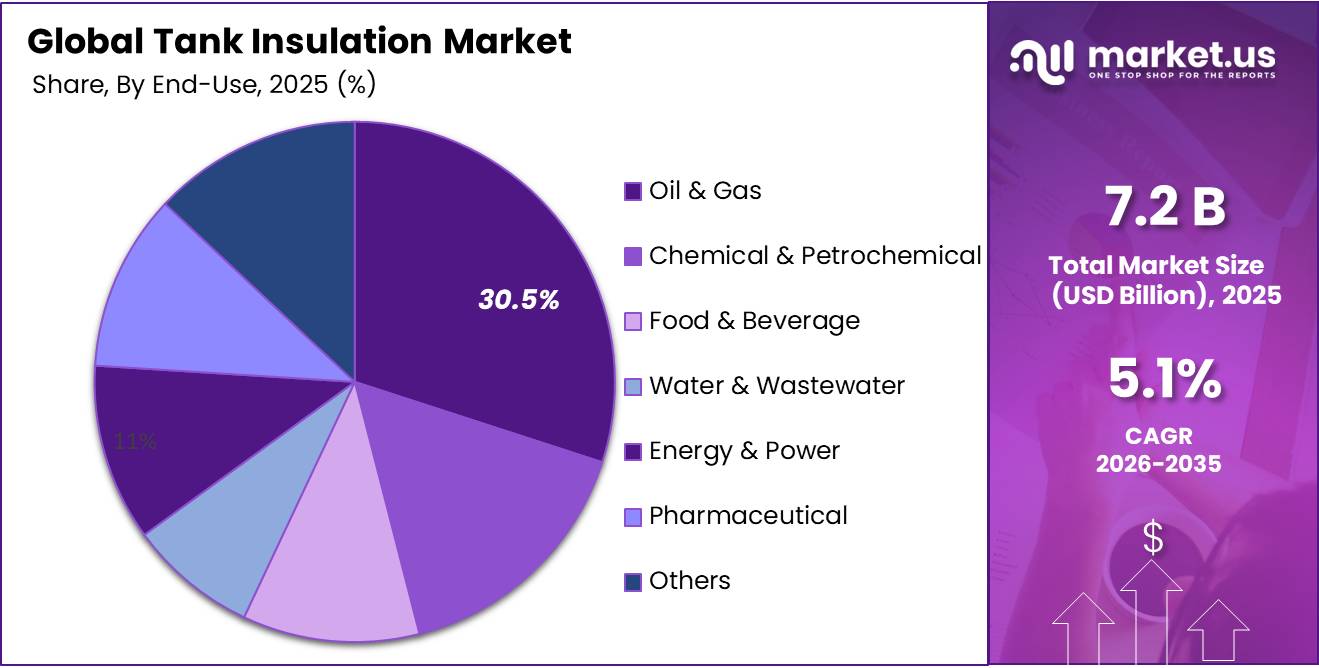

- Among the end-uses, the oil & gas industry is the most considerable within the market, accounting for around 30.5% of the revenue.

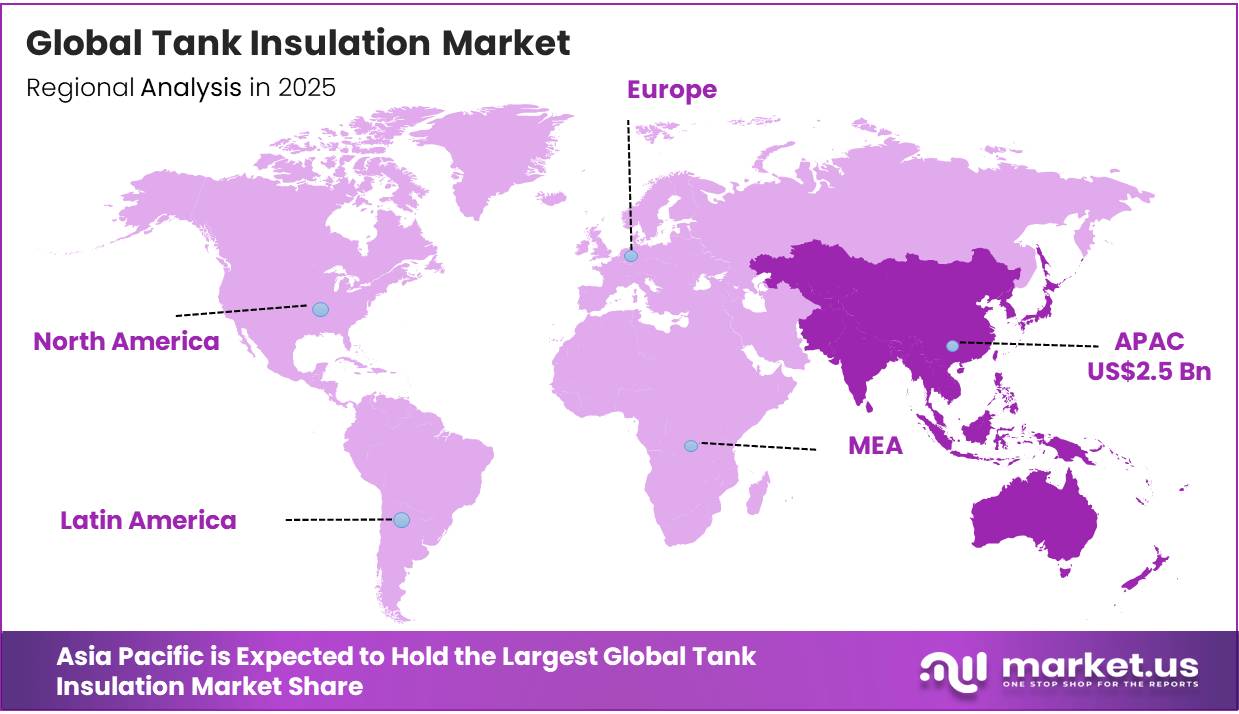

- In 2025, the Asia Pacific was the most dominant region in the tank insulation market, accounting for 34.8% of the total global consumption.

Material Type Analysis

Mineral Wool is a Prominent Segment in the Market.

Mineral wool holds a dominant position in the tank insulation market, accounting for approximately 42.9% share of total material demand. This leadership is primarily attributed to its strong thermal stability, non-combustible nature, and suitability across a wide operating temperature range, making it widely applicable in storage and transportation tank systems.

Both stone wool and glass wool contribute significantly to usage, with stone wool preferred in high-temperature industrial environments such as oil & gas and petrochemical facilities, while glass wool is more commonly adopted in medium-temperature and general-purpose insulation applications. The material’s inherent resistance to fire, moisture, and chemical exposure enhances its reliability in harsh operating conditions.

Temperature Range Analysis

Medium Temperature Insulation (0°C to 100°C) Dominated the Tank Insulation Market.

Medium temperature insulation (0°C to 100°C) represents the dominant segment in the tank insulation market, accounting for approximately 34.1% share of total demand. This segment benefits from widespread application across industries where process fluids, chemicals, and stored materials must be maintained within controlled but non-extreme temperature ranges.

It is extensively utilized in chemical processing, food & beverage storage, water treatment systems, and certain oil & gas operations. The segment’s strong position is supported by its operational versatility, as it accommodates both heating and cooling requirements without the need for highly specialized cryogenic or high-temperature systems.

Materials such as mineral wool, polyurethane, and polyethylene are commonly used due to their cost-efficiency and reliable thermal performance within moderate conditions. Additionally, increasing emphasis on energy efficiency and process stability in industrial operations continues to reinforce demand. Its applicability across both new installations and retrofit projects further consolidates its leading market share globally.

Installation Type Analysis

Tank Insulations Are Mostly Utilized for New Installations.

New installations account for the dominant share of the tank insulation market, representing approximately 64.6% of total demand. This segment is primarily driven by the ongoing expansion of industrial infrastructure, including new storage terminals, processing facilities, and energy transport systems.

Large-scale investments in LNG terminals, chemical plants, and emerging hydrogen infrastructure are key contributors to sustained installation activity, where insulation systems are integrated during initial construction to ensure optimal thermal performance and regulatory compliance.

New installation projects allow for design-optimized insulation integration, enabling the use of advanced materials such as polyurethane, mineral wool, and high-performance composites tailored to specific temperature and safety requirements. The segment further benefits from engineering standardization in modern industrial facilities, which enhances installation efficiency and system reliability.

Application Analysis

Storage Tanks Held a Major Share of the Tank Insulation Market.

Storage Tank applications dominate the tank insulation market, accounting for approximately 70.3% of total demand. This dominance is driven by the extensive use of stationary storage systems across industries such as oil & gas, chemicals, water treatment, food & beverage, and emerging energy applications, including LNG and hydrogen.

Storage tanks require continuous thermal stability to preserve product integrity, minimize evaporation losses, and maintain safety across varying operating conditions. The segment benefits from large-scale infrastructure investments in refineries, petrochemical complexes, and energy terminals, where insulated tanks are essential for long-term operational efficiency.

Demand is further reinforced by the growing deployment of cryogenic and low-temperature storage systems, which require highly specialized insulation solutions. Additionally, increasing retrofit activities in aging industrial facilities contribute to sustained insulation requirements. The scale, permanence, and critical operational role of storage tanks collectively position this segment as the primary driver of insulation material consumption globally.

End-Use Analysis

Tank Insulation is Mostly Utilized in the Oil & Gas Industry.

Oil & gas represents the dominant end-use segment in the tank insulation market, accounting for approximately 30.5% of total demand. This leadership is driven by extensive upstream, midstream, and downstream infrastructure that relies heavily on insulated storage and transportation tanks to maintain product stability and operational safety.

Crude oil, refined petroleum products, and liquefied gases require controlled thermal environments to minimize losses, prevent phase changes, and ensure compliance with safety standards. The segment benefits from large-scale deployment of storage terminals, pipelines, LNG facilities, and refining complexes, all of which incorporate insulation systems as critical operational components.

Harsh operating conditions, including exposure to extreme temperatures and volatile substances, further reinforce the need for high-performance insulation materials such as mineral wool and polyurethane systems. Continuous investments in energy infrastructure modernization and expansion of LNG trade networks sustain strong insulation demand within this sector globally.

Key Market Segments

By Material Type

- Mineral Wool

- Stone Wool

- Glass Wool

- Polystyrene

- Polyurethane

- Elastomeric Foam

- Polyethylene

- Others

By Temperature Range

- Cold Insulation (Below 0°C)

- Medium Temperature Insulation (0°C to 100°C)

- High Temperature Insulation (Above 100°C)

- Cryogenic Insulation (Below -50°C)

By Installation Type

- New Installation

- Retrofit / Replacement

By Application

- Storage Tank

- Transportation Tank

By End-Use

- Oil & Gas

- Chemical & Petrochemical

- Food & Beverage

- Water & Wastewater

- Energy & Power

- Pharmaceutical

- Others

Challenges

The tank insulation market depends on a highly specialized workforce for spray foam application, cryogenic insulation, cellular glass installation, and weatherproofing systems. The U.S. construction sector alone faces a shortage of approximately 500,000 skilled workers, while 91% of construction and industrial firms report difficulty filling qualified positions. Developing industrial insulation expertise typically requires 18–36 months of apprenticeship and technical training.

Workforce demographics further intensify the challenge, with nearly one-third of skilled industrial trade workers aged over 55, implying annual retirement attrition of 8%–12% over the next 5–8 years. As a result, contractors are reporting project mobilization delays of 6–12 weeks on refinery and LNG projects, generating cost overruns of roughly USD 15,000–40,000 per delayed project week.

Mitigation will require expanded apprenticeship programs, stronger trade-school partnerships, and greater adoption of prefabricated pre-insulated modules that can reduce on-site labor requirements by 25%–35%. Increased use of robotic spray application systems can also help shift labor demand from manual installation toward machine supervision.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| MDI/TDI Raw Material Supply Concentration & Price Volatility | ~−0.9% | Global; acute in APAC import corridors, EU & North America | Medium term (2–4 years) |

| HFO/Low-GWP Blowing Agent Transition Cost Burden | ~−0.7% | North America core, EU regulatory hubs, APAC emerging compliance zones | Medium term (2–4 years) |

| Specialized Installation Workforce Deficit | ~−0.8% | North America, EU, Middle East project sites | Long term (≥ 4 years) |

| Cryogenic/LNG Technical Application Complexity | ~−0.6% | LNG corridors: Middle East, APAC, North America, Europe | Long term (≥ 4 years) |

| Smart Monitoring & Digital Integration Adoption Gap | ~−0.5% | APAC (emerging); North America & EU (mid-tier operators) | Medium term (2–4 years) |

| Multi-Jurisdictional Environmental Compliance Divergence | ~−0.7% | EU (REACH/F-Gas hubs), North America, divergent APAC regimes | Long term (≥ 4 years) |

Opportunity

CCUS infrastructure represents a largely underrecognized growth opportunity for the tank insulation industry as global CCUS investment is projected to grow at more than 20% annually through 2035. Liquid CO₂ storage tanks used in transport and sequestration typically operate at approximately -30°C to -50°C, requiring advanced insulation systems with thermal performance beyond conventional petroleum storage applications, while remaining less demanding than liquid hydrogen systems.

Large-scale CO₂ storage facilities require vacuum-assisted insulation panels and closed-cell foam composites capable of achieving ≤0.025 W/(mK) effective thermal conductivity. A single utility-scale CCUS project can generate approximately USD 4–9 million in insulation CAPEX, creating a substantial value opportunity for suppliers with cryogenic expertise.

The IEA estimates that more than 200 large-scale CCUS projects must be operational globally by 2030 to support a 1.5°C pathway, implying a potential USD 800 million–1.8 billion insulation procurement pipeline through 2032. For manufacturers that secure technical certifications and specification influence with CCUS developers in Europe and North America, this emerging segment could contribute roughly +1.0 percentage point of CAGR upside over the next 3–5 years.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Green Hydrogen & Liquid Hydrogen (LH₂) Cryogenic Tank Insulation | +2.8% | EU, North America, East Asia (Japan, South Korea, Australia) | Medium term (2–4 years) |

| Aerogel-Based Advanced Insulation Penetration in High-Value Tanks | +1.5% | North America core, EU, APAC emerging | Short term (≤ 2 years) |

| Insulation-as-a-Service (INSaaS) / Performance-Linked Contracting | +1.2% | North America, EU, India | Medium term (2–4 years) |

| Cryogenic CO₂ Storage & CCUS Infrastructure Insulation | +1.0% | EU, North America, Southeast Asia | Medium term (2–4 years) |

| IoT-Integrated Smart Tank Insulation Systems (Digital Upside) | +1.8% | North America, EU, China, GCC | Short-to-Medium term (1–3 years) |

| APAC / GCC Greenfield Industrial Buildout — Uninsulated Tank Retrofit | +1.3% | India, Southeast Asia (Vietnam, Indonesia), GCC | Medium-to-Long term (3–6 years) |

Drivers

The tightening European regulatory framework is emerging as a major growth driver for tank insulation demand. Under the EU Energy Efficiency Directive (EED), companies consuming more than 10 TJ annually must complete independent energy audits by October 2026, while those exceeding 85 TJ must implement ISO 50001-certified energy management systems by October 2027. These requirements are expected to affect more than 300,000 European manufacturing facilities, increasing focus on process tank and vessel insulation as part of documented energy-efficiency measures.

EU member states are additionally required to achieve 1.5% annual final energy savings during 2026–2027, rising to 1.9% annually during 2028–2030. Combined with similar energy-efficiency initiatives such as California’s 2025 Title 24 updates, these regulations are accelerating retrofit and new-installation activity for industrial insulation systems and are estimated to contribute approximately +1.2 percentage points to market CAGR.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LNG Infrastructure Surge: Cryogenic tank buildout from global LNG export/import terminal expansion | +1.8% | APAC core (China, India, Japan, South Korea); North America (U.S. Gulf Coast); Middle East spill-over | Short–Medium term (1–4 years) |

| Energy Efficiency Mandates: EU Energy Efficiency Directive & EPBD recast driving compulsory industrial insulation audits | +1.2% | EU core (Germany, France, Spain, Italy); UK; select North America (California Title 24) | Short term (≤ 2 years) |

| Pharma & Food-Grade Compliance: Stringent FDA/cGMP & EU Regulation (EC) 1935/2004 driving temperature-controlled tank upgrades | +0.9% | North America; EU; APAC (India, China pharma corridors) | Medium term (2–4 years) |

| Aerogel & Advanced Material Adoption: High-performance insulation displacing conventional PUF/mineral wool in critical applications | +0.8% | North America (dominant); APAC (fastest-growing); EU (regulatory push) | Medium–Long term (2–5+ years) |

| Chemical & Petrochemical Capex Expansion: New chemical plant buildouts in Asia, Middle East, and Americas requiring insulated process tanks | +1.0% | China; India; GCC; Southeast Asia; Brazil spill-over | Medium term (2–4 years) |

| Green Hydrogen & Renewable Energy Storage: Cryogenic liquid hydrogen tanks and large-scale thermal energy storage (TES) infrastructure | +0.6% | EU (Germany, Netherlands); North America; APAC (Japan, South Korea, Australia) | Long term (≥ 4 years) |

Restraints

Tank insulation systems are increasingly exposed to the revised U.S. Section 232 tariff framework, particularly following the April 2026 policy change that shifted tariff calculations from the value of steel or aluminum content to the full customs value of finished derivative products. Under the new rules, derivative products containing more than 15% foreign metal content are subject to a 25% tariff on the entire customs value, while certain steel pipe, tubing, and mill products used in tank shells and cryogenic vessel skins face 50% tariffs on full customs value.

The cost impact is amplified by earlier policy changes, including the increase in U.S. aluminum tariffs from 10% to 25% in March 2025 and the suspension of tariff exclusion processing in February 2025. For North American EPC contractors constructing insulated chemical storage tanks and LNG facilities, these measures can increase landed costs for imported steel shells and metal jacketing by approximately 15%–30%. Since insulation cladding and metal components typically represent 25%–40% of the installed cost of an above-ground insulated storage tank, the financial impact can be significant.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical Feedstock Price Volatility (MDI/TDI Surge) | –1.4% | Global; severe in India, SE Asia, EU import-dependent corridors | Short term (≤ 2 years) |

| REACH & Evolving Chemical Regulatory Compliance Burden | –0.8% | EU core; cascading into UK, Ukraine, GCC via harmonization | Medium term (2–4 years) |

| Section 232 Tariffs on Metal & Derivative Inputs | –0.6% | North America core; secondary impact on export-oriented APAC suppliers | Short term (≤ 2 years) |

| Skilled Labor Shortage for Specialized Installation | –0.7% | North America, Western Europe; emerging in Middle East LNG corridors | Medium term (2–4 years) |

| LNG CapEx Deceleration & Project FID Slowdown | –0.5% | Global; concentrated in Australia, North America, APAC offtake corridors | Medium term (2–4 years) |

| High Unit Cost Barrier of Advanced Insulation (Aerogel/VIP) | –0.4% | Global; cost-sensitive APAC and Latin American markets most exposed | Long term (≥ 4 years) |

Trends

Shift Toward High-Performance and Sustainable Insulation Materials.

The advancements in high-performance and environmentally aligned insulation materials are increasingly influencing material selection in tank insulation applications, particularly where thermal efficiency and lifecycle performance are critical. For instance, aerogels exemplify this shift, with reported thermal conductivity values of 0.013-0.015 W/m·K, compared with 0.03-0.04 W/m·K for mineral wool, enabling equivalent insulation performance at significantly reduced thickness.

The reduction in material thickness is operationally relevant for storage and transport tanks where space and weight constraints directly affect design efficiency. Similarly, aerogels consist of up to 99.8% air by volume, contributing to extremely low heat transfer and improved thermal resistance per unit thickness. In industrial contexts, such properties allow enhanced insulation performance under cryogenic and elevated temperature conditions without proportionate increases in material mass.

Geopolitical Impact Analysis

Geopolitical Supply Chain Disruptions and Cost Pressures in AI-Driven Sports Camera Systems.

Ongoing geopolitical tensions are exerting measurable effects on energy supply chains, with direct implications for tank insulation demand through their influence on LNG trade flows, storage requirements, and infrastructure resilience. Natural gas markets have remained structurally sensitive to disruptions. Since 2020, repeated geopolitical events have altered supply patterns and reinforced LNG’s role as a balancing mechanism in global energy systems.

In 2024, Asian LNG benchmark prices (JKM) fluctuated between USD 8.40 and USD 14.90 per MMBtu, while European TTF prices ranged from USD 7.87 to USD 14.83 per MMBtu, with spikes in the second half of the year explicitly linked to geopolitical tensions in Europe and supply uncertainty. Such volatility increases the need for strategic storage, reinforcing reliance on insulated tanks to manage inventory and buffer supply shocks.

Simultaneously, structural shifts in sourcing are evident. European gas imports declined by 18% between 2021 and 2024, accompanied by a sharp increase in LNG imports, with the United States supplying nearly 45% of LNG volumes. This reconfiguration elevates the importance of storage and regasification infrastructure, where insulation systems are integral to maintaining thermal stability under fluctuating and often constrained supply conditions.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Tank Insulation Market.

In 2025, the Asia Pacific dominated the global tank insulation market, holding about 34.8% of the total global consumption. The region’s position in tank insulation demand is closely linked to the scale and concentration of energy transition infrastructure, particularly in hydrogen and LNG systems that require temperature-controlled storage.

Electrolytic hydrogen capacity reached 2 GW globally in 2024, with more than 1 GW added by July 2025, indicating rapid buildout of facilities requiring insulated storage and transport systems. Within this, China accounts for 65% of global installed electrolyser capacity and projects reaching final investment decision, alongside nearly 60% of global manufacturing capacity, reflecting a high concentration of hydrogen production assets that depend on thermal management systems for storage and handling.

Regional demand is further supported by Southeast Asia, where hydrogen consumption reached 4 million tons per annum in 2024, led by Indonesia at 35%, followed by Malaysia, Viet Nam, and Singapore. These volumes imply extensive use of storage tanks across refining, chemicals, and emerging clean energy applications. The region’s industrial base inherently drives sustained deployment of high-performance tank insulation systems across both stationary and transport applications.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of tank insulation focus on continuous material innovation, particularly developing solutions with lower thermal conductivity, improved fire resistance, and better performance under cryogenic and high-temperature conditions. Companies further emphasize customization capabilities to meet sector-specific requirements in oil & gas, LNG, chemicals, and pharmaceuticals, where operating conditions vary significantly.

Strengthening installation services and technical support is another priority, as proper application directly affects insulation efficiency and lifecycle performance. Many players integrate engineering and design assistance to secure early involvement in large infrastructure projects.

Expansion of production capacity and localization of supply chains support cost efficiency and faster delivery. Additionally, sustainability initiatives, including recyclable materials and reduced-emission manufacturing processes, are increasingly used to align with industrial decarbonization goals and improve customer preference in regulated end-use sectors.

The Major Players in The Industry

- Saint-Gobain

- Rockwool A/S

- Owens Corning

- Armacell

- Knauf Insulation

- Johns Manville

- Kingspan Group

- Murphy Insulation Company

- Huamei Energy-Saving Technology Group Co., Ltd.

- L’ISOLANTE K-FLEX S.p.A.

- Insultherm, Inc.

- Röchling

- LNT Marine Pte., Ltd.

- Batimat Isoliertechnik GmbH

- Sailer GmbH

- Other Key Players

Key Development

- In May 2025, Saint-Gobain announced a multi-million-pound investment to build a low-carbon stone wool insulation manufacturing plant in Melton Mowbray, Leicestershire, UK.

- In April 2025, Knauf Insulation announced the expansion of its Performance+ portfolio with new pipe and tank fiberglass insulation.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 7.2 Bn |

| Forecast Revenue (2035) | USD 11.8 Bn |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Mineral Wool, Polystyrene, Polyurethane, Elastomeric Foam, Polyethylene, and Others), By Temperature Range (Cold Insulation (Below 0°C), Medium Temperature Insulation (0°C to 100°C), High Temperature Insulation (Above 100°C), and Cryogenic Insulation (Below -50°C)), By Installation Type (New Installation and Retrofit / Replacement), By Application (Storage Tank and Transportation Tank), By End-Use (Oil & Gas, Chemical & Petrochemical, Food & Beverage, Water & Wastewater, Energy & Power, Pharmaceutical, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Saint-Gobain, Rockwool A/S, Owens Corning, Armacell, Knauf Insulation, Johns Manville, Kingspan Group, Murphy Insulation Company, Huamei Energy-Saving Technology Group Co., Ltd., L’ISOLANTE K-FLEX S.p.A., Insultherm, Inc., Röchling, LNT Marine Pte., Ltd., Batimat Isoliertechnik GmbH, Sailer GmbH, and Other Players. |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |