Quick Navigation

Report Overview

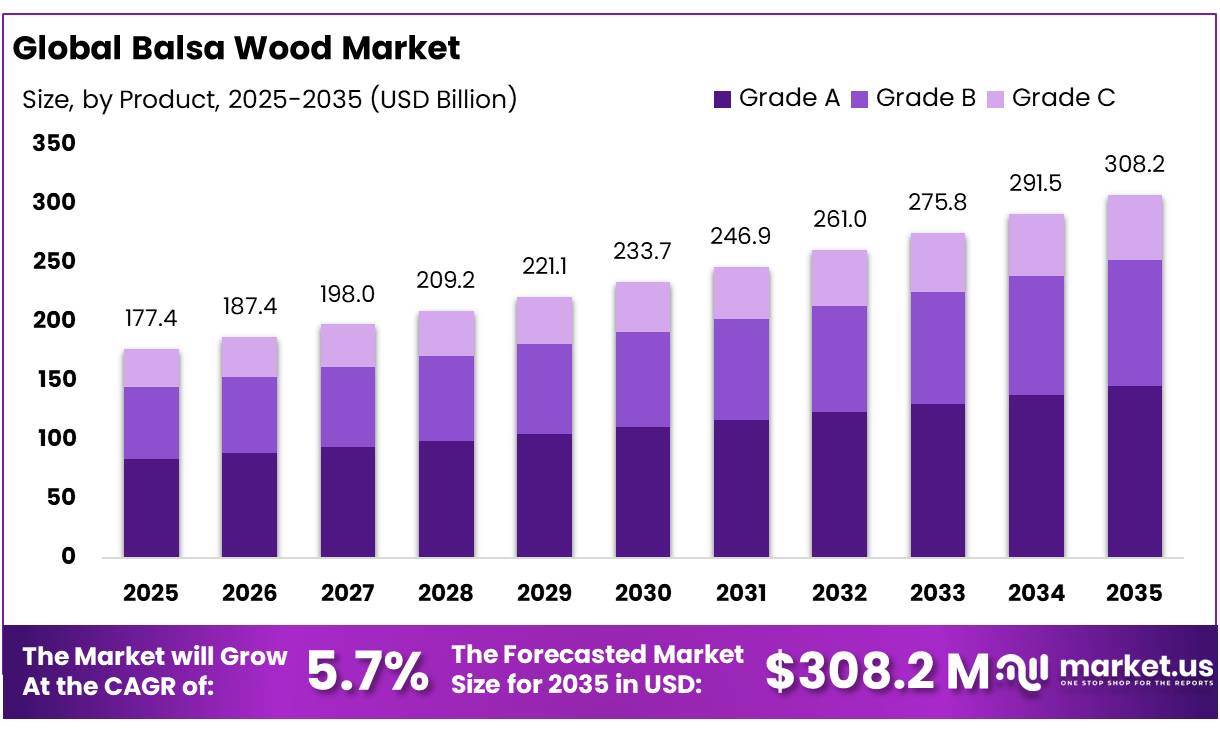

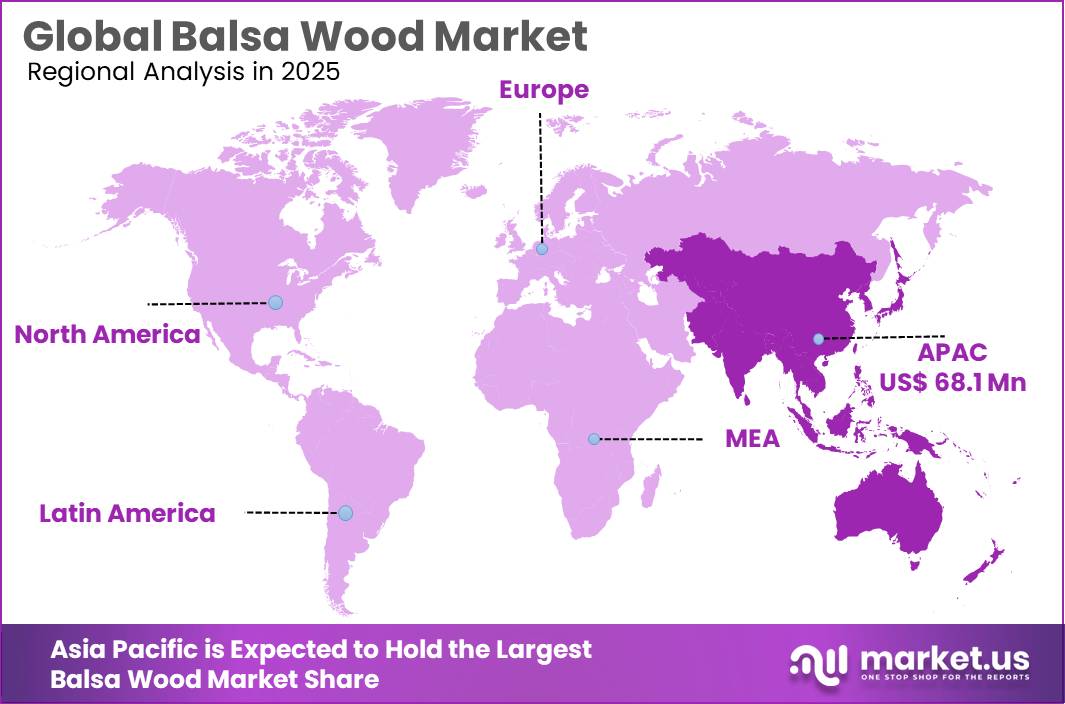

The Global Balsa Wood Market size is expected to be worth around USD 308.2 Million by 2035, from USD 177.4 Million in 2025, growing at a CAGR of 5.7% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 38.4% share, holding USD 68.1 Million revenue.

Balsa wood is positioned as a lightweight industrial core material used mainly in wind turbine blades, marine panels, transport, construction, aerospace and composite sandwich structures. Industrial demand is supported by its high strength-to-weight ratio, renewability and use as a substitute for heavier structural materials. Ecuador remains the largest supply base: in 2024, it exported US$146.2 million of HS 440723 sawn balsa/related woods, ahead of Poland at US$24.9 million and the U.S. at US$15.0 million, according to World Bank WITS/UN Comtrade data. Ecuador remains the central supply base: official 2025 reporting cited Ecuador’s 68% share of the international balsa market and USD 161.3 million of balsa exports in 2024.

Key Takeaways

- Balsa Wood Market size is expected to be worth around USD 308.2 Million by 2035, from USD 177.4 Million in 2025, growing at a CAGR of 5.7%.

- Grade A held a dominant market position, capturing more than a 47.4% share.

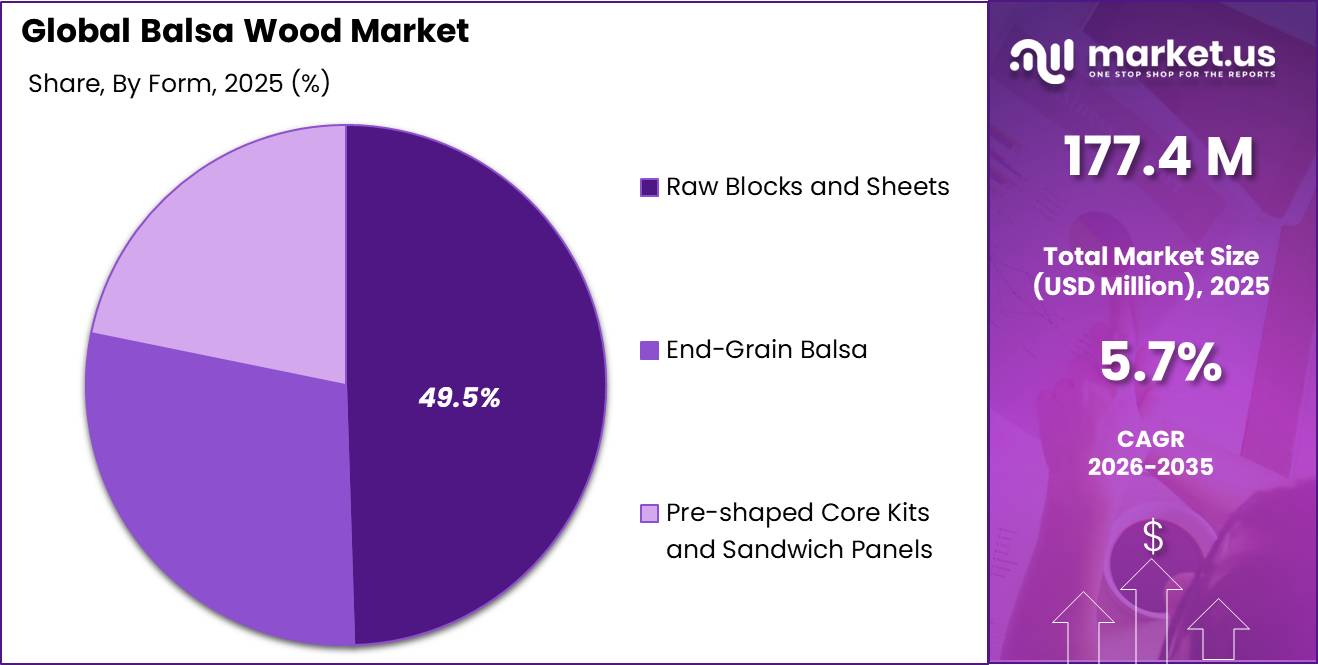

- Raw Blocks and Sheets held a dominant market position, capturing more than a 49.5% share of the global balsa wood market.

- Wind Energy held a dominant market position, capturing more than a 48.2% share of the global balsa wood market.

- Asia-Pacific emerged as the dominant region in the global balsa wood market, accounting for 38.4% of the total market share and generating approximately USD 68.1 million.

The industrial scenario is closely tied to renewable energy. GWEC reported a record 117 GW of new global wind capacity installed in 2024, while IEA expects renewable electricity generation to rise from 9,900 TWh in 2024 to 16,200 TWh by 2030, with wind contributing almost one-third of growth. This directly supports demand for balsa core materials in blade structures.

Key driving factors include wind energy blade manufacturing, sustainable lightweighting, and regulated timber sourcing. FAO reported that global wood and paper product exports reached US$486 billion in 2024, rising 1.4% after a 14% drop in 2023, showing recovery in forest-product trade. The EU Deforestation Regulation is also reshaping procurement, requiring operators to prove covered commodities such as wood are deforestation-free; the European Commission states the regulation targets at least 32 million tonnes of carbon-emission reductions per year.

Government and institutional support is linked to forestry-plantation development and productivity. Ecuador’s PROFORESTAL program recorded 48,533 hectares of forest plantations in 2016, including 8,518 hectares of balsa, while academic field research sampled 2,161 plots across 7 provinces, supporting better plantation-yield planning.

In 2025, Schweiter Technologies reported first-half net sales of CHF 493.7 million, EBITDA of CHF 43.4 million, and free operating cash flow of CHF 21.3 million. Its Core Materials business recorded solid global growth and “strong business performance with balsa solutions,” despite wind-sector regulatory headwinds in the U.S. and China.

By Product Analysis

Grade A dominates with 47.4% share due to its superior strength, smooth finish, and wide use across premium applications.

In 2025, Grade A held a dominant market position, capturing more than a 47.4% share of the global balsa wood market. The strong performance of this segment was mainly supported by its high quality, lightweight structure, and excellent durability compared to lower-grade alternatives. Grade A balsa wood is widely preferred in applications where precision, strength, and consistency are essential, including aerospace components, wind turbine blades, marine construction, architectural modeling, and premium hobby products.

Manufacturers and end users continued to favor Grade A material because of its uniform grain pattern and better mechanical properties, which help improve product performance while reducing overall weight. The growing demand for lightweight and sustainable materials across industrial sectors further strengthened the adoption of Grade A balsa wood during 2025.

By Form Analysis

Raw Blocks and Sheets dominate with 49.5% share due to their versatility and strong demand across manufacturing applications.

In 2025, Raw Blocks and Sheets held a dominant market position, capturing more than a 49.5% share of the global balsa wood market. This leadership was driven by their broad use across industries that require lightweight, easy-to-shape, and structurally reliable materials.

Raw blocks and sheets are widely utilized as primary input materials for producing components used in marine construction, wind energy, aerospace structures, model making, and specialized industrial applications. Their popularity stems from the flexibility they offer manufacturers, allowing further cutting, shaping, and customization according to specific project requirements.

By End Use Analysis

Wind Energy dominates with 48.2% share driven by rising demand for lightweight and high-performance turbine blades.

In 2025, Wind Energy held a dominant market position, capturing more than a 48.2% share of the global balsa wood market. The segment’s strong position was largely supported by the extensive use of balsa wood as a core material in wind turbine blade manufacturing. Due to its exceptional strength-to-weight ratio, balsa wood helps improve blade performance while keeping overall turbine weight low, making it a preferred material for renewable energy projects.

During 2025, investments in wind power infrastructure continued to support demand for high-quality balsa wood, particularly for larger and more efficient turbine designs. Manufacturers favored balsa wood because of its durability, natural stiffness, and ability to enhance structural stability in composite blade construction.

Key Market Segments

By Product

- Grade A

- Grade B

- Grade C

By Form

- Raw Blocks and Sheets

- End-Grain Balsa

- Pre-shaped Core Kits and Sandwich Panels

By End Use

- Aerospace & Defense

- Marine

- Wind Energy

- Others

Emerging Trends

Larger Wind Turbine Blades Are Increasing the Need for Lightweight Balsa Wood Materials

One of the latest trends shaping the balsa wood market is the growing use of larger wind turbine blades designed to improve renewable energy generation efficiency. As wind energy projects expand worldwide, turbine manufacturers are focusing on producing longer and lighter blades that can capture more wind and generate higher electricity output. This trend is creating stronger demand for lightweight core materials such as balsa wood.

According to the International Renewable Energy Agency (IRENA), global renewable power capacity reached 4,448 GW in 2024 after adding a record 585 GW during the year. Wind energy remained one of the leading contributors to this growth. At the same time, wind turbine technology is moving toward larger blade structures, particularly for offshore projects where efficiency is a major priority. Balsa wood continues to gain attention because it provides high strength while keeping blade weight low, helping manufacturers improve turbine performance.

Sustainability and Renewable Material Adoption Are Becoming Industry Priorities

Another important trend in the balsa wood market is the increasing preference for sustainable and renewable materials across industrial manufacturing sectors. Governments and energy organizations are encouraging industries to reduce environmental impact by using eco-friendly raw materials in production processes. Balsa wood is benefiting from this shift because it is naturally renewable, biodegradable, and suitable for lightweight composite applications. According to IRENA, renewables represented around 46% of global installed power capacity by the end of 2024, highlighting the growing focus on sustainable development worldwide.

In addition, the International Energy Agency (IEA) projects that global renewable power capacity could expand by nearly 4,600 GW between 2025 and 2030. This rapid growth is encouraging manufacturers to adopt materials that align with sustainability goals while maintaining strong performance standards. The trend is visible not only in wind energy but also in marine construction, transportation components, and engineered composite products.

Drivers

Rising Wind Energy Projects Are Increasing Demand for Lightweight Balsa Wood

One of the major factors driving the balsa wood market is the rapid expansion of the global wind energy sector. Balsa wood is widely used inside wind turbine blades because it is lightweight, strong, and capable of improving structural performance without adding extra weight. As countries continue investing in renewable energy projects, the demand for turbine blades has increased significantly, creating a direct need for high-quality balsa wood materials.

According to the International Renewable Energy Agency (IRENA), global installed wind energy capacity reached 1,131 GW in 2024, compared to just 7.5 GW in 1997, showing how rapidly the industry has expanded over the past two decades. In 2024 alone, wind energy added around 113 GW of new capacity worldwide. This strong growth has encouraged turbine manufacturers to secure reliable raw materials that can support larger and more efficient blade designs. Since balsa wood offers an excellent strength-to-weight ratio, it continues to be one of the preferred materials used in advanced wind energy infrastructure.

Government Renewable Energy Targets Supporting Long-Term Market Growth

Government policies focused on clean energy development are also creating strong opportunities for the balsa wood market. Many countries have introduced renewable energy expansion programs to reduce carbon emissions and improve energy security. These initiatives are encouraging large-scale wind farm installations, which directly support the use of balsa wood in turbine manufacturing. According to IRENA’s Renewable Capacity Statistics 2025, global renewable power capacity increased by 585 GW during 2024, representing a record annual growth rate of 15.1%.

Renewables accounted for more than 92% of all new power capacity added worldwide during the year. Wind and solar energy remained the leading technologies behind this expansion. In addition, the International Energy Agency (IEA) expects global onshore wind capacity additions to increase by 45% between 2025 and 2030, reaching nearly 732 GW. As governments continue funding renewable energy projects and strengthening climate commitments, the requirement for lightweight construction materials such as balsa wood is expected to remain strong across the energy sector.

Restraints

Limited Availability of High-Quality Balsa Wood Is Creating Supply Challenges

One of the major factors restraining the growth of the balsa wood market is the limited availability of high-quality forest resources. Balsa wood mainly comes from tropical regions, particularly countries such as Ecuador, which remains one of the largest producers globally. However, increasing pressure on forest ecosystems and restrictions on harvesting activities have made raw material supply more challenging. According to the World Bank, forest area in Ecuador accounted for around 49.5% of total land area in 2023, reflecting the importance of forest resources to the country’s economy.

At the same time, environmental regulations and sustainable forestry programs have tightened the control of timber extraction to prevent excessive forest degradation. These measures are important for long-term environmental protection but can limit the immediate availability of balsa wood for industrial use. Manufacturers often face difficulties in securing a stable supply of premium-grade wood, particularly when demand from industries such as wind energy rises rapidly. This imbalance between supply and demand can lead to longer procurement cycles and increased production pressure across the value chain.

Rising Deforestation Concerns Are Increasing Pressure on Wood-Based Industries

Growing concerns over deforestation and forest conservation are also acting as a restraint on the balsa wood market. Governments, environmental organizations, and international agencies are introducing stricter sustainability standards for timber sourcing, which can affect harvesting and trade activities. The Food and Agriculture Organization (FAO) estimates that nearly 10 million hectares of forest are lost globally every year due to deforestation.

In addition, Global Forest Watch reported that Ecuador lost around 37 thousand hectares of natural forest in 2024 alone. These figures have increased attention on responsible forest management and sustainable sourcing practices. While these initiatives support environmental protection, they also create additional compliance requirements for producers and exporters. Companies are increasingly required to prove legal sourcing, maintain certification standards, and invest in traceability systems, which can raise operational costs.

Opportunity

Expanding Renewable Energy Infrastructure Creates Strong Growth Opportunities for Balsa Wood

One of the biggest growth opportunities for the balsa wood market comes from the continued expansion of renewable energy infrastructure, particularly wind power projects. Balsa wood is widely used as a lightweight core material in wind turbine blades because it provides excellent strength while keeping blade weight low. As governments and energy companies invest in clean energy, the need for larger and more efficient turbines is increasing.

According to the International Renewable Energy Agency (IRENA), global renewable power capacity reached 4,448 GW in 2024 after adding a record 585 GW of new capacity during the year. Wind energy remained one of the key contributors to this growth. Many countries are introducing renewable energy targets, financial incentives, and carbon reduction programs that encourage the construction of new wind farms. These projects require advanced turbine blades, creating a long-term demand for high-performance materials such as balsa wood.

Sustainable Material Adoption Across Industrial Applications Opens New Markets

Another important opportunity lies in the increasing use of sustainable and natural materials across manufacturing industries. Governments and industrial organizations are encouraging the adoption of environmentally responsible materials to reduce carbon footprints and improve resource efficiency. Balsa wood fits well within this trend because it is renewable, biodegradable, and lightweight. According to the International Energy Agency (IEA), global investment in clean energy technologies and infrastructure is expected to exceed USD 2 trillion in 2025.

In addition, the European Union’s Green Deal and similar sustainability initiatives in North America and Asia are promoting the use of eco-friendly materials in industrial production. As manufacturers look for alternatives to heavier synthetic materials, balsa wood is gaining attention for applications in marine structures, transportation components, construction panels, and engineered composites. This broadening range of end-use industries presents significant opportunities for future market expansion.

Regional Insights

Asia-Pacific Dominates the Balsa Wood Market with 38.4% Share, Reaching USD 68.1 Million

In 2025, Asia-Pacific emerged as the dominant region in the global balsa wood market, accounting for 38.4% of the total market share and generating approximately USD 68.1 million in revenue. The region’s leadership is primarily supported by the rapid expansion of renewable energy projects, growing industrial manufacturing activities, and increasing demand for lightweight composite materials. Countries such as China, India, Japan, and South Korea have significantly increased investments in wind energy infrastructure, where balsa wood is widely used as a core material in turbine blade production due to its high strength-to-weight ratio.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

3A Composites GmbH is a leading manufacturer of balsa wood and PET foam core materials used in wind energy, marine, transportation, and industrial composites. The company operates through approximately 35 locations globally with around 4,100 employees and generates nearly CHF 1.0 billion in annual net sales. Its Core Materials division focuses on BALTEK® balsa and AIREX® PET foam solutions, supported by more than 75 years of sandwich composite expertise. The company also maintains FSC-certified balsa plantations to strengthen raw-material security and sustainability initiatives.

Schweiter Technologies AG is the parent company of 3A Composites and a major participant in the global lightweight composites sector. In the first half of 2025, the company reported net sales of CHF 493.7 million, while maintaining profitability despite challenging industrial markets. The Core Materials segment benefited from integrated balsa sourcing and expanding PET foam capabilities in Asia. Schweiter reported approximately 4,598 employees globally and continues investing in recycled PET solutions and wind-energy composite applications.

DIAB International AB is one of the world’s largest structural core-material suppliers serving wind energy, marine, aerospace, and transportation industries. The company operates 7 production facilities and reported SEK 1.686 billion in net sales during 2023, supported by a workforce of approximately 742 employees. DIAB manufactures advanced PET, PVC, and structural foam materials and maintains production operations across Sweden, Italy, China, the United States, and Ecuador. The company continues expanding PET core-material capacity to meet growing renewable-energy demand.

Top Key Players Outlook

- 3A Composites GmbH

- Schweiter Technologies AG

- DIAB International AB

- CoreLite Inc.

- Gurit Holding AG

- Carbon-Core Corp.

- Pacific Coast Marine

- Pontus Wood Group

- BALTEK Corporation

Recent Industry Developments

In new product development, CoreLite’s PC11 Pro coated balsa can reduce resin uptake by up to 76%, helping customers lower weight and resin cost. For partnership activity, CoreLite’s distribution agreement with Biesterfeld, signed in 2018, continued to support access to 4 core material groups, including BALSASUD Core, PET, PVC foam, and board products. For 2025–2026, no public balsa-focused merger, acquisition, or major new investment was found, but CoreLite’s long product history since 1939, certified balsa range, and coated balsa technology show steady expansion in lightweight composite materials.

In 2025, Gurit Holding AG reported CHF 319.6 million in net sales in 2025, with Wind Materials contributing CHF 190.1 million, showing that wind energy remained its key demand area. Gurit also operated across 5 continents, with 27 sites and 1,961 employees at the end of 2025. In product development, Gurit continued to promote Balsaflex in 110 kg/m³, 155 kg/m³, and 250 kg/m³ density grades, with sheet sizes of 610 x 1220 mm and thickness options from 6–50 mm. In 2026, Gurit signed a major 5-year supply agreement with a leading wind turbine OEM, expected to generate around CHF 250 million in net sales, using its OptiCore core-kit technology.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 177.4 Mn |

| Forecast Revenue (2035) | USD 308.2 Mn |

| CAGR (2026-2035) | 5.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Grade A, Grade B, Grade C), By Form (Raw Blocks and Sheets, End-Grain Balsa, Pre-shaped Core Kits and Sandwich Panels), By End Use (Aerospace And Defense, Marine, Wind Energy, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | 3A Composites GmbH, Schweiter Technologies AG, DIAB International AB, CoreLite Inc., Gurit Holding AG, Carbon-Core Corp., Pacific Coast Marine, Pontus Wood Group, BALTEK Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |