Quick Navigation

Report Overview

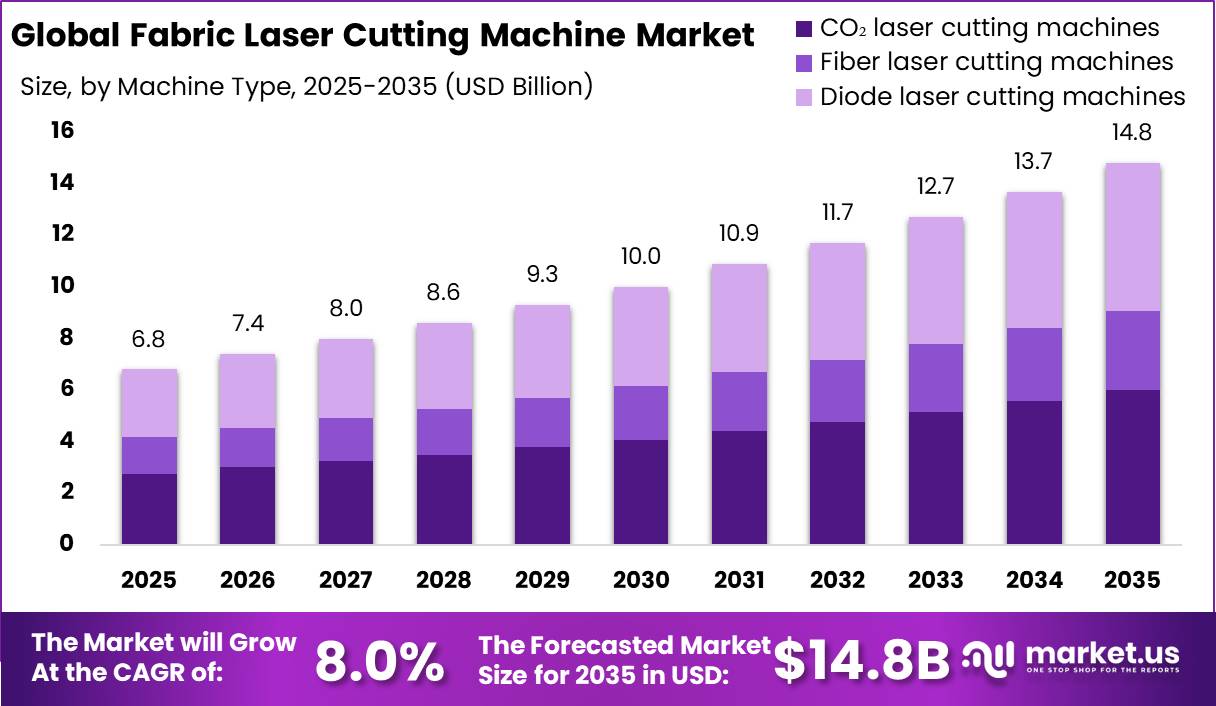

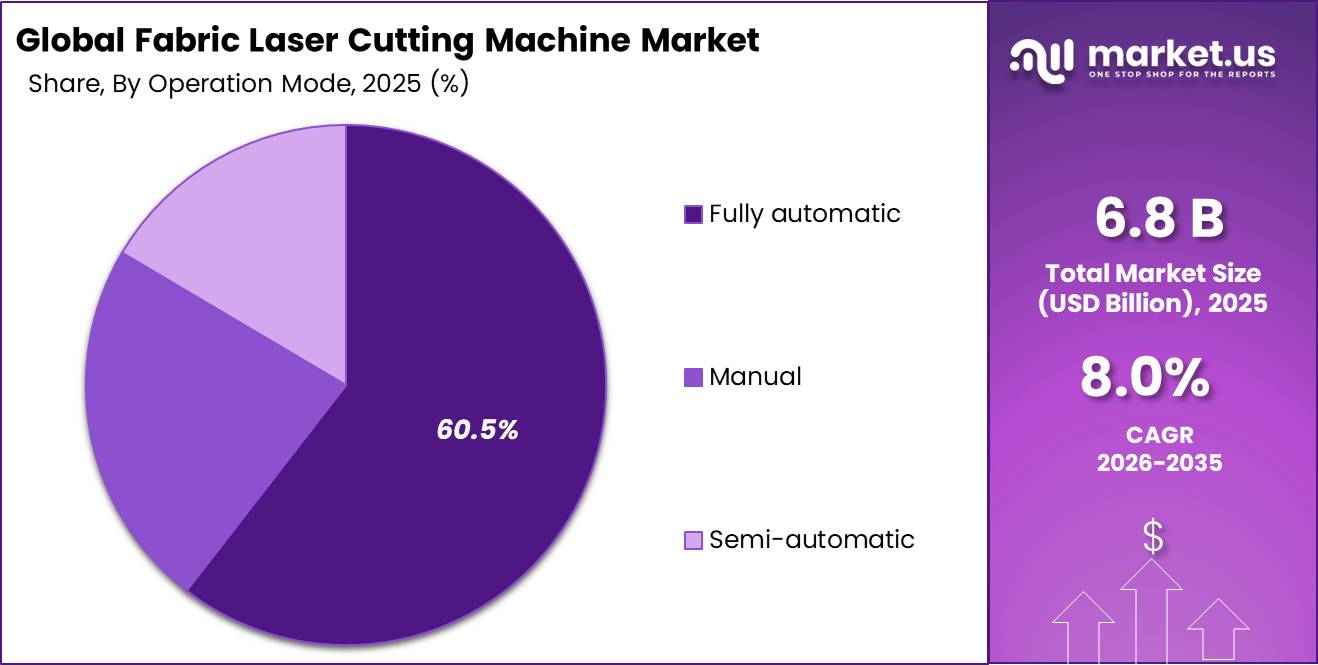

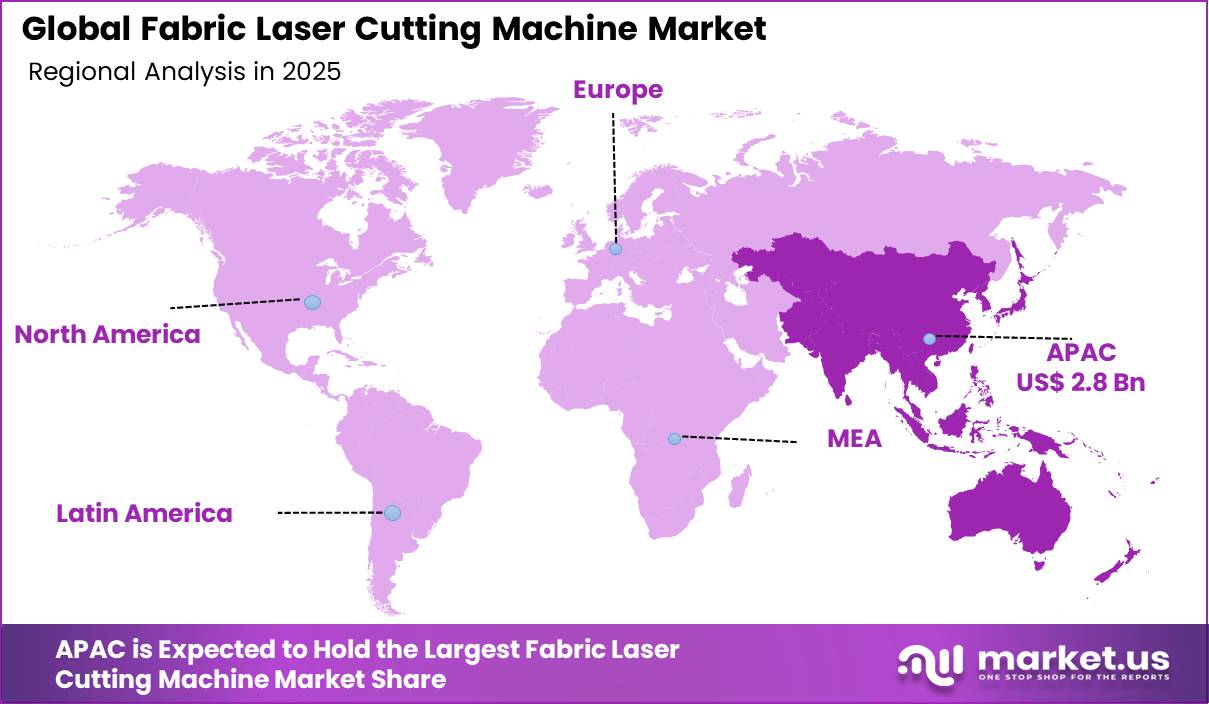

The Global Fabric Laser Cutting Machine Market size is expected to be worth around USD 14.8 Billion by 2035, from USD 6.8 Billion in 2025, growing at a CAGR of 8.0% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 40.5% share, holding USD 68.1 Million revenue.

The fabric laser cutting machine market is shaped by the increasing shift toward precision-based and digitally controlled textile manufacturing. These systems utilize focused laser technology to cut, engrave, and process fabrics with high accuracy, reducing material wastage and eliminating reliance on traditional mechanical tooling.

Adoption is strongly linked to the growing need for design flexibility, rapid production cycles, and consistent output quality across apparel, home textiles, and technical fabric applications. CO₂ laser systems remain widely used due to their compatibility with both natural and synthetic fabrics, while medium-power machines dominate because of their balanced efficiency and operational versatility.

Fully automatic systems are increasingly preferred as manufacturers integrate CAD/CAM platforms and smart production workflows to enhance productivity and reduce labor dependency. Synthetic fabrics form a major application base due to their suitability for sealed-edge laser cutting. The textile industry remains the primary end-use sector, supported by demand for customization, fast fashion production, and scalable manufacturing capabilities.

Key Takeaways

- The global fabric laser cutting machine market was valued at USD 6.8 billion in 2025.

- The global fabric laser cutting machine market is projected to grow at a CAGR of 8.0% and is estimated to reach USD 14.8 billion by 2035.

- On the basis of machine types, CO₂ laser cutting machines dominated the market, constituting 40.6% of the total market share.

- Based on the laser power, medium fabric laser cutting machines dominated the market, with a substantial market share of around 42.3%.

- Based on the fabric type, synthetic fabrics led the market, comprising 56.7% of the total market.

- Among the operation modes, fully automatic fabric laser cutting machines held a major share in the market, 60.5% of the market share.

- Among the end use industries, textile sector is the most considerable within the market, comprising for around 50.6% of the revenue.

- In 2025, the Asia Pacific was the most dominant region in the fabric laser cutting machine market, accounting for 40.5% of the total global consumption.

Machine Type Analysis

CO₂ Laser Cutting Machines are a Prominent Segment in the Market.

CO₂ laser cutting machines account for the dominant share of the fabric laser cutting machine market, contributing approximately 40.6% of total machine type demand. Their leadership is primarily driven by strong compatibility with a wide range of textile materials, including natural fibers such as cotton and silk as well as synthetic fabrics like polyester.

CO₂ laser systems are widely preferred in apparel and home textile manufacturing due to their ability to deliver smooth edge finishing, high cutting precision, and reduced fabric fraying without requiring additional post-processing. Their relatively mature technology base, coupled with lower operational complexity compared to advanced fiber-based alternatives, supports widespread adoption across both large-scale industrial units and small to mid-sized workshops. Additionally, their efficiency in handling intricate design patterns and multi-layer fabric cutting applications further reinforces their continued relevance in high-volume textile production environments.

Laser Power Analysis

Medium Power Fabric Laser Cutting Machines Dominated the Market.

Medium laser power systems hold the dominant position in the fabric laser cutting machine market, accounting for approximately 42.3% of total demand. This segment is widely preferred due to its balanced performance characteristics, offering an optimal combination of cutting efficiency, precision, and energy consumption. Medium-power systems are particularly suitable for processing a broad range of textile materials, including natural fabrics, synthetics, and blended textiles, making them highly versatile across apparel, upholstery, and technical textile applications.

Their ability to handle both intricate designs and moderate-thickness materials without excessive thermal damage enhances their operational reliability. In addition, these systems provide better productivity compared to low-power machines while avoiding the higher operational costs and energy intensity associated with high-power units. This balance of cost efficiency and functional flexibility has positioned medium-power laser systems as the preferred choice for mainstream industrial textile processing environments.

Fabric Type Analysis

Synthetic Fabrics Are the Most Widely Utilized Fabric.

Synthetic fabrics represent the dominant segment in the fabric laser cutting machine market, accounting for approximately 56.7% of total demand. This leadership is primarily attributed to the extensive use of synthetic materials such as polyester, nylon, and acrylic across apparel, automotive interiors, home furnishings, and industrial textiles. Synthetic fabrics are particularly well-suited for laser cutting due to their thermoplastic properties, which allow for clean, sealed edges that minimize fraying and eliminate the need for additional finishing processes.

This enhances production efficiency and consistency, especially in high-volume manufacturing environments. Additionally, the growing adoption of performance textiles in sportswear and technical applications further strengthens demand, as laser systems enable precise pattern execution on complex synthetic blends. The compatibility of synthetic fabrics with automated cutting processes also supports their widespread use in digitally driven textile manufacturing setups.

Operation Mode Analysis

Fully Automatic Fabric Laser Cutting Machines Held a Major Share of the Market.

Fully automatic operation mode dominates the fabric laser cutting machine market, accounting for approximately 60.5% of total demand. This leadership is driven by the increasing shift toward high-efficiency, digitally integrated textile manufacturing systems. Fully automated laser cutting machines are capable of executing end-to-end operations, including pattern loading, material alignment, cutting, and output handling with minimal human intervention. This significantly reduces labor dependency while improving production consistency and throughput.

Their integration with CAD/CAM software and smart manufacturing platforms enables real-time adjustments, enhancing precision in complex and high-volume fabric cutting applications. These systems are particularly favored in large-scale apparel manufacturing and technical textile production, where speed, accuracy, and repeatability are critical. Additionally, reduced operational errors and improved material utilization further reinforce their adoption in modern, efficiency-driven production environments.

End Use Industry Analysis

Fabric Laser Cutting Machine is Mostly Utilized in the Textile Sector.

The textile industry holds the dominant position in the fabric laser cutting machine market, accounting for approximately 50.6% of total end-use demand. This dominance is driven by the extensive application of laser cutting technology in apparel manufacturing, home textiles, and fashion accessories, where precision and design flexibility are critical. Textile producers increasingly rely on laser systems to achieve intricate pattern cutting, clean edge finishing, and rapid prototyping, which are essential for fast fashion and short production cycles.

The technology further supports efficient handling of diverse materials, including natural, synthetic, and blended fabrics, making it highly adaptable across textile sub-segments. Rising demand for customized and small-batch production further strengthens adoption, as laser cutting enables quick design modifications without additional tooling costs. The scalability and efficiency of these systems make them integral to modern textile production ecosystems globally.

Key Market Segments

By Machine Type

- CO₂ laser cutting machines

- Fiber laser cutting machines

- Diode laser cutting machines

By Laser Power

- Low

- Medium

- High

By Fabric Type

- Natural

- Synthetic

By Operation Mode

- Manual

- Semi-automatic

- Fully automatic

By End Use Industry

- Textile

- Automotive

- Aerospace

- Others

Drivers

Rising Demand for Precision and Customization in Textile Manufacturing Drives the Fabric Laser Cutting Machine Market.

Rising requirements for dimensional accuracy and design flexibility in textile manufacturing are materially strengthening the case for fabric laser cutting systems. Laser-based processes achieve tolerances as fine as 0.1 mm, enabling consistent replication of intricate geometries that are difficult to maintain with mechanical cutting methods. This level of precision is particularly relevant in applications such as technical textiles and performance apparel, where minor deviations can lead to product rejection.

The capability to process complex contours without physical contact eliminates material distortion and reduces waste, supporting high-value, design-intensive production. The studies indicate that laser cutting minimizes material loss while enabling highly accurate, repeatable cuts across diverse fabrics, including synthetics and composites. Similarly, automated nesting and digital design integration improve material utilization and compress product development cycles from weeks to days in certain apparel applications.

Moreover, customization requirements further reinforce adoption. Digital control allows rapid modification of patterns without tooling changes, aligning with demand for short production runs and personalized products.

Restraints

High Initial Investment and Integration Costs Pose Challenges to the Fabric Laser Cutting Machine Market.

Capital intensity associated with fabric laser cutting machines remains a measurable constraint on adoption, particularly for small and mid-scale textile units. Entry-level CO₂ textile systems are typically priced between USD 3,000 and USD 15,000, while more advanced industrial configurations incorporating higher power and automation can exceed USD 25,000 for textile-grade systems and extend beyond USD 60,000-150,000 in broader industrial contexts.

This wide cost dispersion reflects dependencies on laser source, bed size, and automation features, which directly influence production scalability but raise acquisition thresholds. Beyond acquisition, integration-related expenditures introduce additional financial burden. For instance, installation packages often require auxiliary infrastructure such as chillers, air compressors, and ventilation systems, which are frequently excluded from base pricing.

Moreover, software licensing and operator training further add to upfront costs, while operational readiness may necessitate facility modifications for safety compliance. Similarly, energy and operating requirements contribute to lifecycle cost pressures. High-power systems can draw 20-50 kW of electricity, and consumables such as assist gases may add USD 3,000-12,000 annually depending on usage intensity. These cost layers extend payback periods and limit adoption in cost-sensitive manufacturing environments.

Opportunity

Expansion into Technical Textiles and High-Performance Applications Create Opportunities in the Fabric Laser Cutting Machine Market.

The expansion of technical textiles into advanced application domains is increasingly shaping material processing requirements where conventional cutting methods show limitations in repeatability and edge integrity. Technical textiles, such as those used in sectors like automotive interiors, filtration systems, medical fabrics, protective wear, and aerospace components, are engineered for functional performance rather than aesthetics, requiring highly controlled fabrication processes to maintain structural consistency under demanding conditions.

For instance, in automotive applications alone, laser systems are used for seat covers, insulation layers, and interior trims where dimensional precision directly affects assembly fit and durability. Similarly, across industrial use cases such as filters, PPE, and composite reinforcements, demand for contactless cutting is reinforced by the need to avoid fiber distortion and maintain material integrity, particularly in synthetics and multilayer fabrics.

The technical textiles segment is widely associated with rapid adoption of engineered fabrics across functional applications, with multiple fiber categories, including high-performance synthetics and composites, forming a significant share of inputs used in these materials. As product architectures become more specialized, laser cutting enables fine tolerances and programmable pattern flexibility, including in advanced protective materials such as aramids and composite laminates used in aerospace and defense-related applications.

Growing reliance on digitally controlled fabrication further aligns with the increasing complexity of engineered textile structures, where multi-layer assemblies and smart textile integration require micro-level precision and adaptability, supporting broader adoption across high-performance manufacturing ecosystems.

Trends

Integration of Automation and Smart Manufacturing Technologies.

The integration of automation and smart manufacturing technologies is increasingly redefining operational structures in fabric laser cutting systems, where digital control and connectivity are central to production efficiency. Modern laser cutting setups are frequently embedded with CAD/CAM software, IoT-enabled sensors, and automated material handling units, enabling real-time synchronization between design input and execution. In several industrial configurations, conveyor-fed laser systems support continuous cutting of roll fabrics, reducing manual intervention and enabling uninterrupted workflows in apparel and technical textile production environments.

Adoption is closely linked with Industry 4.0 frameworks, where interconnected production systems use data-driven decision-making and machine-to-machine communication to optimize output. Reports on smart factory models indicate that such digitalized manufacturing environments can deliver 10-30% cost efficiencies in production processes and similar improvements in logistics and quality management, driven largely by automation and system integration. Within fabric processing units, laser systems increasingly incorporate intelligent vision modules capable of detecting fabric patterns and automatically adjusting cutting parameters such as speed, focus, and power, improving consistency across varied textile types.

Operational advancements further include multi-head laser configurations and automated nesting algorithms, which enhance throughput by enabling simultaneous cutting of multiple components while optimizing material utilization. Some industrial setups demonstrate multi-layer fabric processing capabilities, allowing stacked cutting with maintained accuracy, thereby reducing cycle time per unit output.

Integration with centralized production software further enables predictive maintenance and remote monitoring, reducing downtime risks and improving equipment lifecycle management. As manufacturing environments shift toward digitally coordinated ecosystems, fabric laser cutting machines are increasingly functioning as connected nodes within broader smart textile production networks rather than standalone equipment.

Geopolitical Impact Analysis

Fragmented Trade Architectures and Their Influence on Advanced Textile Laser Equipment Flows.

Heightened geopolitical friction across major manufacturing blocs is increasingly influencing the procurement and deployment of industrial laser systems used in fabric processing. Trade restrictions and tariff actions between major economies, particularly involving China, the United States, and parts of Europe, have contributed to reconfiguration of machinery sourcing routes.

China remains a dominant exporter of industrial machinery, accounting for a significant share of global machine tool exports, while the U.S. continues to rely on imported equipment for advanced manufacturing applications, including textile automation systems. This interdependence creates exposure when tariffs or export controls are introduced, often translating into higher landed costs and delayed capital investment decisions for end users.

Supply chain fragmentation has further been observed in textile-linked manufacturing corridors, where geopolitical disputes and sanctions have disrupted raw material and equipment flows, extending lead times and increasing procurement uncertainty across multi-stage production systems. Consequently, manufacturers of fabric laser cutting machines are increasingly adjusting production footprints and component sourcing strategies, with partial relocation toward China+1 ecosystems to mitigate policy risk exposure.

Similarly, shifting trade routes and export realignments are creating uneven access to advanced automation technologies, particularly in cost-sensitive textile hubs. This has resulted in delayed adoption cycles for capital-intensive laser systems, especially where import duties and compliance costs escalate total system acquisition expenses. The cumulative effect is a more regionally segmented market structure, where technology diffusion is increasingly shaped by trade policy alignment rather than purely industrial demand dynamics.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Fabric Laser Cutting Machine Market.

In 2025, Asia Pacific dominated the global fabric laser cutting machine market, holding about 40.5% of the total global consumption, supported by its deeply embedded textile and apparel manufacturing ecosystem. The region contributes nearly half of global textile output, with China alone producing majority of worldwide textile and apparel goods. Similarly, India also maintains a strong position, with textile exports exceeding USD 34 billion in FY2023-24 as reported by the Ministry of Textiles, reflecting sustained investment in production modernization and automation-led processing lines.

The concentration of large-scale garment clusters in China, Bangladesh, Vietnam, and India has accelerated deployment of laser-based cutting systems to replace conventional blade-based methods, particularly in export-oriented production units. Operational advantages such as cutting accuracy within sub-millimeter tolerance levels and material utilization improvements in automated fabric processing lines have further supported adoption across high-volume apparel production. The combination of cost-competitive manufacturing, export dependency, and ongoing mechanization continues to reinforce Asia Pacific’s structural dominance in this equipment category.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of fabric laser cutting machines concentrate on continuous product differentiation through improvements in precision, cutting speed, and multi-material compatibility to address diverse textile applications. Significant emphasis is placed on integrating advanced control systems, including CAD/CAM compatibility, AI-assisted pattern recognition, and automated nesting software to enhance operational efficiency and reduce material wastage.

Expansion of after-sales service networks, including remote diagnostics, predictive maintenance, and rapid spare-part supply chains, is a key focus to strengthen customer retention. Companies further invest in modular machine designs that allow scalability from semi-automatic to fully automated configurations, catering to both SMEs and large industrial users. In parallel, efforts to improve energy efficiency and compliance with industrial safety standards support broader acceptance across regulated manufacturing environments, reinforcing long-term equipment adoption.

The Major Players in The Industry

- Trotec Laser

- Epilog Laser

- Han’s Laser Technology Industry Group

- Golden Laser

- GCC LaserPro

- Gravotech

- TRUMPF Group

- Amada Co., Ltd.

- Bystronic AG

- Coherent Corp.

- IPG Photonics

- Bodor Laser

- HSG Laser

- Eurolaser GmbH

- Sahajanand Laser Technology Ltd.

- Other Key Players

Key Developments

- In September 2025, Trotec Laser and Lindenmeyr Munroe announced a partnership, with Lindenmeyr Munroe adding Trotec’s Speedy laser systems and premium laserable materials to its portfolio, providing customers across multiple U.S. regions access to advanced laser technology.

- In March 2026, Epilog Laser added the Fusion Ascent Laser Series to its product lineup. The company showcased the new system during the ISA Sign Expo in Orlando, Florida.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 6.8 Bn |

| Forecast Revenue (2035) | USD 14.8 Bn |

| CAGR (2026-2035) | 8.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Machine Type (CO₂ laser cutting machines, Fiber laser cutting machines, and Diode laser cutting machines), By Laser Power (Low, Medium, and High), By Fabric Type (Natural and Synthetic), By Operation Mode (Manual, Semi-automatic, and Fully automatic), By End-Use Industry (Textile, Automotive, Aerospace, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Trotec Laser, Epilog Laser, Han’s Laser Technology Industry Group, Golden Laser, GCC LaserPro, Gravotech, TRUMPF Group, Amada Co., Ltd., Bystronic AG, Coherent Corp., IPG Photonics, Bodor Laser, HSG Laser, Eurolaser GmbH, Sahajanand Laser Technology Ltd., and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |