Quick Navigation

Report Overview

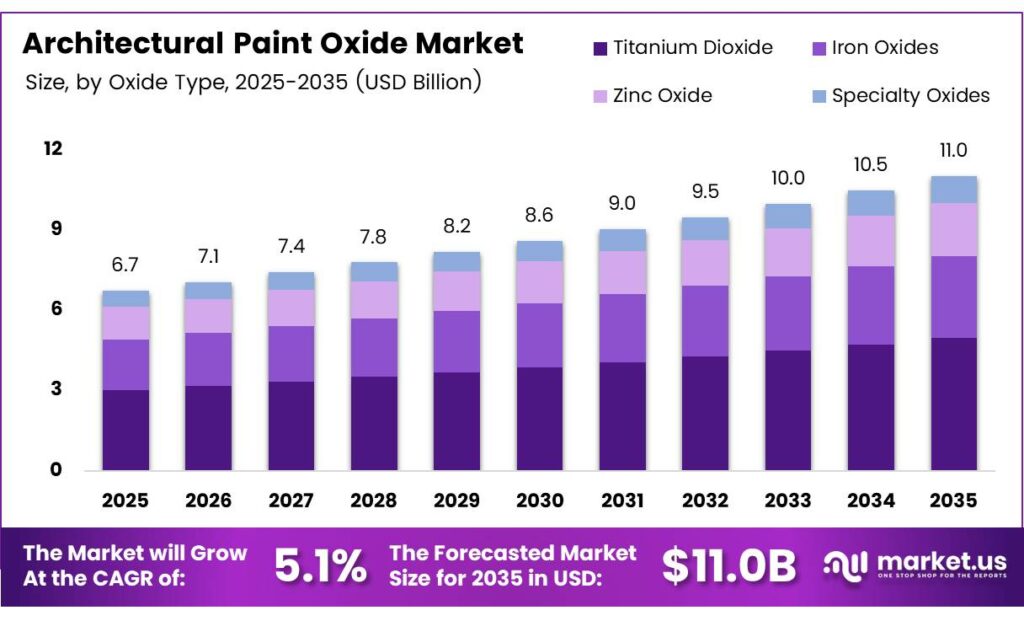

The Global Architectural Paint Oxide Market size is expected to be worth around USD 11.0 billion by 2035 from USD 6.7 billion in 2025, growing at a CAGR of 5.1% during the forecast period 2026 to 2035.

Architectural paint oxides are inorganic pigments — primarily titanium dioxide, iron oxides, zinc oxide, and specialty oxides — used to deliver color, opacity, durability, and weather resistance in paints applied to residential, commercial, and infrastructure surfaces. Their performance characteristics make them the preferred pigment base for high-volume architectural coating formulations globally.

Urban housing expansion and large-scale construction activity in emerging economies directly fuel bulk consumption of oxide-based pigments. Contractors and coating manufacturers prioritize oxides for their high tinting strength and cost efficiency at scale. This structural demand link between construction output and pigment consumption makes the architectural paint oxide market closely tied to macroeconomic building cycles.

Iron oxide pigments under the Bayferrox Scopeblue range achieve approximately 35% lower product carbon footprint compared to conventional grades, verified through life-cycle assessment. This reduction, enabled by renewable-energy-based raw materials, signals that low-carbon pigment technology is no longer a niche offering — it is becoming a procurement criterion for specification-driven buyers in regulated markets.

Performance data further validates the commercial case for advanced oxide pigments. Colorants and Coatings, cool pigmented coatings can reduce peak roof surface temperatures by 20–25°C and deliver building cooling energy savings of 10–30% in hot climates. This positions architectural paint oxides not just as aesthetic products but as functional building performance components — a shift that expands the addressable market beyond decorative coatings into energy-efficiency solutions.

Key Takeaways

- The Global Architectural Paint Oxide Market was valued at USD 6.7 billion in 2025 and is forecast to reach USD 11.0 billion by 2035 at a CAGR of 5.1% during the forecast period 2026–2035.

- Titanium Dioxide leads with a 59.6% market share in 2025.

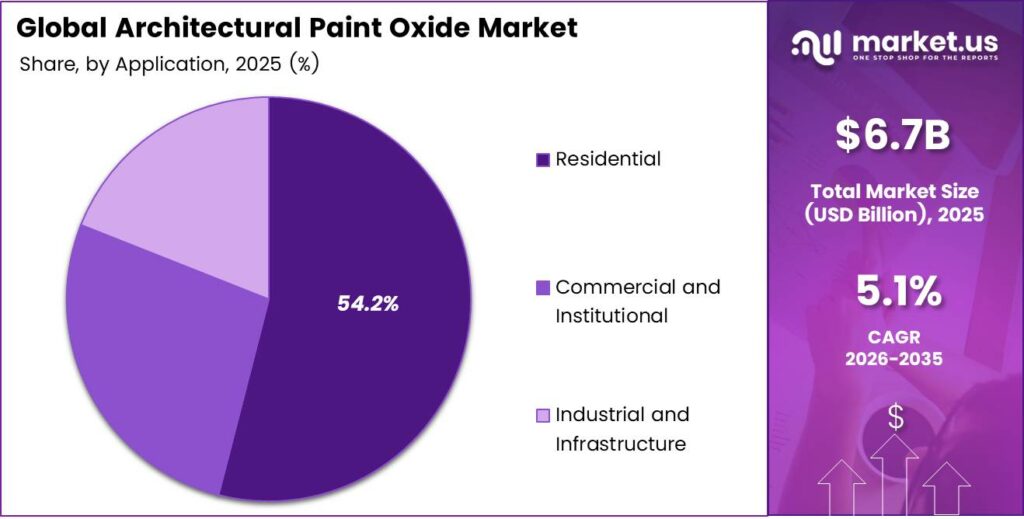

- Residential holds the dominant share at 54.2% in 2025.

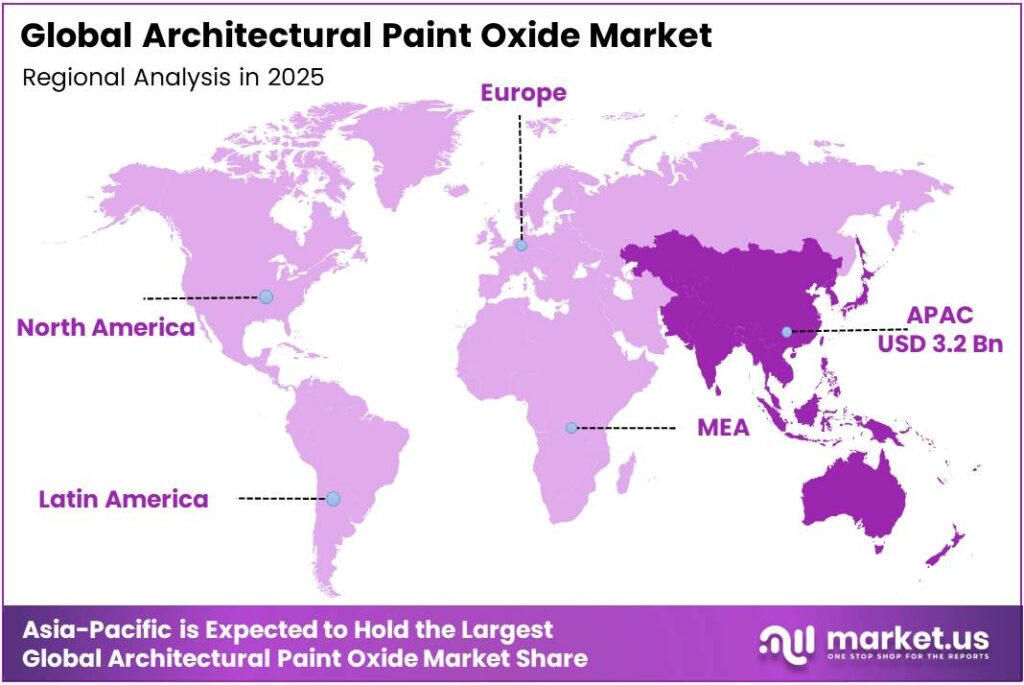

- Asia-Pacific dominates regionally with a 48.1% share, valued at USD 3.2 billion.

Product Analysis

Titanium Dioxide dominates with 59.6% due to unmatched opacity and weather resistance performance.

In 2025, Titanium Dioxide held a dominant market position in the By Oxide Type segment of the Architectural Paint Oxide Market, with a 59.6% share. Its superior whiteness index and light-scattering efficiency mean formulators require lower pigment volumes per liter of paint, reducing unit cost while maintaining coverage. This cost-performance ratio makes it the default choice across residential and commercial coating specifications.

Iron Oxides serve as the primary colorant solution for earth-tone and natural-finish architectural paints, two aesthetic categories showing consistent specification growth. Their chemical stability across UV exposure cycles and alkaline surfaces makes them reliable in exterior applications. Additionally, iron oxides carry a sustainability advantage — natural grades have inherently lower processing emissions, supporting low-carbon formulation strategies.

Application Analysis

Residential dominates with 54.2% due to high-volume, recurring repainting cycles.

In 2025, Residential held a dominant market position in the By Application segment of the Architectural Paint Oxide Market, with a 54.2% share. Homeowners and property developers prioritize oxide-based paints for exterior facades due to their durability against weathering and UV degradation. Renovation and repainting cycles in mature housing markets sustain this demand independently of new construction output, providing structural demand stability.

Commercial and Institutional applications serve as the higher-specification demand channel, where architects and project specifiers mandate performance standards around chemical resistance, coverage uniformity, and extended service life. This segment concentrates purchasing into fewer, larger procurement decisions, which advantages suppliers with technical sales teams and strong specification relationships. Margin per ton tends to be higher than in residential volume segments.

Key Market Segments

By Oxide Type

- Titanium Dioxide

- Iron Oxides

- Zinc Oxide

- Specialty Oxides

By Application

- Residential

- Commercial and Institutional

- Industrial and Infrastructure

Emerging Trends

Sustainable Pigments, Digital Color Tools, and Multifunctional Coatings Redefine Architectural Paint Oxide Demand

Architectural paint oxide producers face a structural shift as buyers prioritize sustainable, recyclable pigment solutions. Colorants and Coatings, optimized blends of titanium dioxide and metal-oxide pigments can raise solar reflectance from approximately 0.25 to 0.50–0.65, cutting roof heat flux by roughly 40–60%. This performance data converts sustainability positioning into a measurable energy efficiency argument for specifiers.

Digital color-matching technologies are changing how pigment consumption patterns form. Retailers and contractors now use AI-assisted color tools that match architectural finishes to precise oxide pigment compositions, reducing waste and narrowing the acceptable pigment variance in formulations.

Multifunctional coatings that combine aesthetic appeal with thermal, antimicrobial, or protective properties represent the fastest-moving formulation category. Earth-tone and natural-finish paints, which rely heavily on iron oxide pigments, are gaining sustained architectural specification interest.

Drivers

Urban Construction Expansion and Performance Standards Drive Bulk Consumption of Oxide-Based Pigments

Rapid urban housing growth and large-scale commercial infrastructure development directly expand the volume of architectural coatings required per construction cycle. Emerging economies in Asia, Africa, and Latin America are building at a pace that demands high-tinting-strength pigments in bulk. Oxide-based pigments meet this need at the cost-efficiency levels that large-scale architectural projects require, making substitution by alternative pigment systems commercially impractical at this volume.

Formulation performance standards are rising in parallel with construction volumes. Architects and developers now specify coatings that demonstrate measurable weather resistance, UV stability, and extended service life. Fe/Co-doped Zn₂SiO₄ black oxide pigments achieved near-infrared solar reflectance values as high as 62%, compared to typical black pigments at only 5–10% NIR reflectance. This tenfold performance gap creates a compelling substitution case for advanced oxide systems in high-specification projects.

Additionally, pigment paste formulations using Bayferrox Scopeblue iron oxides reduce overall coating formulation carbon footprint by at least 20%, depending on pigment loading. For commercial and institutional buyers operating under corporate sustainability commitments, this measurable footprint reduction makes oxide-based systems a procurement advantage, not just a performance choice.

Restraints

Raw Material Price Volatility and VOC Regulations Compress Margins and Constrain Formulation Flexibility

Titanium dioxide, iron, and zinc commodity prices fluctuate with mining output, energy costs, and trade policy — factors entirely outside the control of paint oxide manufacturers. When raw material costs rise sharply, producers face a margin compression choice: absorb the cost or pass it to formulators. Large coating manufacturers absorb short-term shocks by renegotiating supplier contracts, which transfers price pressure downward to mid-sized pigment producers with less negotiating leverage.

Environmental regulations impose a second cost layer. The U.S. EPA AIM Rule sets VOC limits at 50 g/L for flat architectural coatings and 100 g/L for non-flat coatings. These limits push oxide-pigmented paint systems toward water-borne and low-VOC reformulations, which require new dispersant chemistry and process changes. Reformulation carries a direct R&D cost and can temporarily disrupt product performance consistency.

Certain synthetic oxide pigments face outright use restrictions in European and, increasingly, in Asian regulatory frameworks due to concerns around heavy metal content and processing emissions. Producers relying on these pigments for specific color ranges must either qualify alternative chemistries or exit those segments. This regulatory pressure narrows the formulation toolkit and concentrates demand toward a smaller set of compliant pigment grades — reducing competitive differentiation options for mid-tier suppliers.

Growth Factors

Eco-Friendly Pigment Innovation, Smart City Expansion, and Renovation Demand Create New Revenue Channels

Low-VOC and eco-friendly oxide pigment development is moving from an R&D priority to a commercial product line requirement. TiO₂-P25 enhanced thermochromic coatings on roof tiles delivered annual HVAC energy savings between 12% and 25% across simulated residential buildings. This verified energy performance creates a value argument that supports premium pricing for advanced oxide-based coating systems.

Smart city infrastructure programs across Asia-Pacific, the Middle East, and parts of Europe are specifying architectural coatings with functional properties — thermal management, air purification, and durability under high-traffic conditions. These projects create concentrated, high-volume procurement windows that favor suppliers with both scale and technical application support.

Renovation and remodeling activity in mature markets — particularly in Western Europe and North America — sustains replacement demand independent of new construction cycles. Property owners upgrading aging buildings increasingly specify performance coatings rather than standard decorative paints.

Regional Analysis

Asia-Pacific Dominates the Architectural Paint Oxide Market with a Market Share of 48.1%, Valued at USD 3.2 Billion

Asia-Pacific holds a 48.1% share of the global architectural paint oxide market, valued at USD 3.2 billion. China and India drive this concentration through sustained government-backed housing construction programs and rapid commercial real estate development. The region’s manufacturing base for titanium dioxide and iron oxide pigments also supports domestic supply chains, reducing input costs and reinforcing regional production advantages.

North America maintains a mature but high-value market position, driven by strict EPA VOC regulations that accelerate formulation upgrades toward compliant, performance-grade oxide pigments. The U.S. renovation and remodeling sector sustains replacement demand in residential and commercial segments. Specification-driven purchasing by commercial contractors supports premium pricing for technically verified pigment systems.

Europe’s architectural paint oxide demand is shaped by stringent environmental compliance requirements and a strong renovation market. EU sustainability directives are pushing formulators toward low-carbon, water-borne pigment systems. Germany, France, and the UK anchor regional consumption, with specification standards in commercial and infrastructure projects setting quality benchmarks that influence supplier product development across the value chain.

Latin America represents a volume-growth opportunity driven by urbanization in Brazil and Mexico, where residential housing programs are expanding. Oxide pigments serve high-volume, cost-sensitive formulations in this region. However, currency volatility and import dependency for titanium dioxide grades create procurement risk that limits the pace at which premium pigment products penetrate the market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

AkzoNobel positions itself at the intersection of sustainability and scale, using its global distribution network to push low-VOC, oxide-pigmented architectural coatings into both mature and emerging markets. Its investment in water-borne formulation technology directly aligns with tightening EPA and EU VOC regulations, giving it a compliance-readiness advantage that supports specification wins in regulated commercial and institutional projects.

PPG Industries leverages its integrated raw material sourcing and formulation R&D to maintain margin control in a commodity-pressured market. Its architectural coatings portfolio spans residential through infrastructure segments, which reduces its exposure to any single demand cycle. PPG’s technical service model — providing formulation support to large coating applicators — creates stickiness that generic pigment suppliers cannot easily replicate.

Sherwin-Williams controls one of the largest direct retail networks in North America, giving it unmatched visibility into residential repaint demand trends. This distribution ownership allows Sherwin-Williams to respond to consumer color preference shifts — particularly toward earth-tones and natural finishes — faster than wholesale-dependent competitors. Its vertical integration from pigment sourcing through retail sale compresses lead times and protects margin at multiple chain points.

BASF approaches the architectural paint oxide segment primarily through high-performance and specialty pigment chemistry, targeting the premium and functional coating tiers where margin is highest. Its R&D investment in nano-oxide pigments and cool-coating formulations positions it to capture specification demand from smart city and energy-efficient building programs. BASF’s strength is in technical differentiation, not volume competition — a defensible position as performance standards tighten across the industry.

Key Players

- AkzoNobel

- PPG Industries

- Sherwin-Williams

- BASF

- RPM International

- Asian Paints

- Kansai Paint

- DuluxGroup

Recent Developments

- In 2025, BASF started a new production line in Dilovası, Türkiye, for dispersions used in architectural coatings and construction materials, producing low-VOC and low-CO₂ dispersions. BASF’s Dilovası site implemented a Mass Balance approach and green electricity use to support reduced-carbon-footprint dispersions for architectural coatings.

- In 2025, Sherwin-Williams launched its first-ever 2025 Color Capsule of the Year, expanding from one Color of the Year to nine curated architectural paint colors. Sherwin-Williams’ 2025 Colormix Forecast included 48 trend-forward hues across four palettes, supporting architectural and interior design color specification.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 6.7 Billion |

| Forecast Revenue (2035) | USD 11.0 Billion |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Oxide Type (Titanium Dioxide, Iron Oxides, Zinc Oxide, Specialty Oxides), By Application (Residential, Commercial and Institutional, Industrial and Infrastructure) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AkzoNobel, PPG Industries, Sherwin-Williams, BASF, RPM International, Asian Paints, Kansai Paint, DuluxGroup |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |