Quick Navigation

- Report Overview

- Key Takeaways

- Grade Analysis

- Product Type Analysis

- Application Analysis

- Reinforcement Material Analysis

- Installation Technology Analysis

- End-User Analysis

- Key Market Segments

- Emerging Trends

- Drivers

- Restraints

- Growth Factors

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

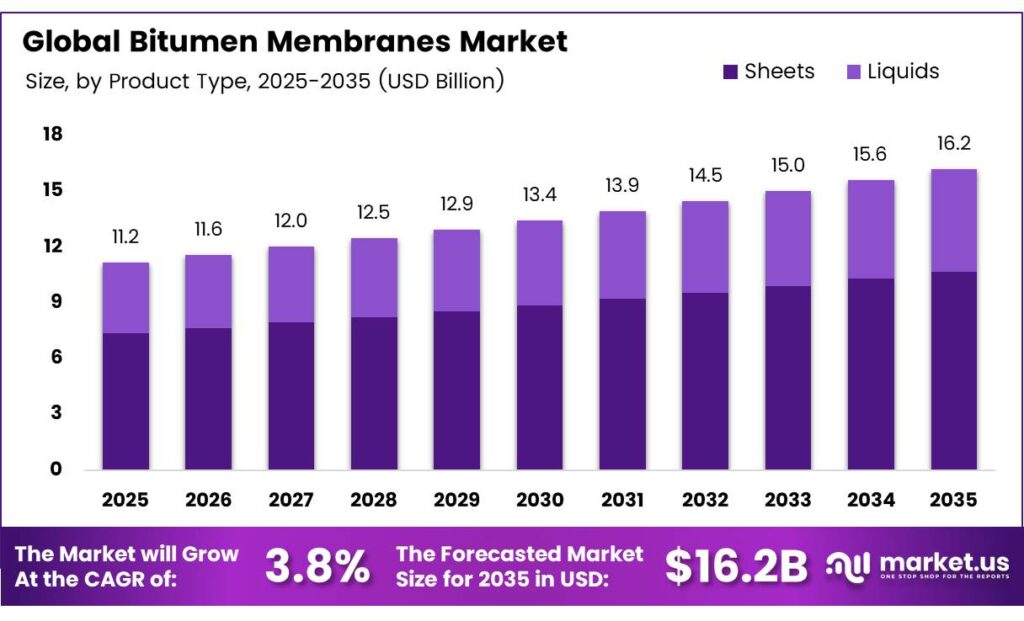

The Global Bitumen Membranes Market size is expected to be worth around USD 16.2 billion by 2035 from USD 11.2 billion in 2025, growing at a CAGR of 3.8% during the forecast period 2026 to 2035.

Bitumen membranes are polymer-modified waterproofing sheets and liquid coatings used across roofing, below-grade waterproofing, bridge decks, and parking structures. Their core advantage lies in combining flexibility, tensile strength, and resistance to water penetration — properties that make them the default choice in construction waterproofing globally.

Modified bitumen grades — specifically APP and SBS — dominate over conventional oxidized bitumen because they deliver measurably superior performance under thermal cycling and mechanical stress. Sheet-form membranes hold a 67.3% product share, reflecting contractor preference for proven, torch- and self-adhesive-applied systems over liquid alternatives that require more controlled application conditions.

Energy performance standards are reshaping product specifications across key markets. The GAF SBS bright-white modified bitumen cap sheet delivers an initial solar reflectance of 0.67 and an initial Solar Reflectance Index of 82. This positions reflective membrane products as compliance tools for green building codes — not merely performance upgrades — giving suppliers with certified products a direct procurement advantage.

Sustainability credentials are becoming a procurement filter, not a differentiator. Production-stage emissions for bituminous membranes stand at 1.54 kg CO₂ eq. (A1–A3). This figure gives specifiers a measurable benchmark, and manufacturers who reduce below this threshold will gain credibility with green-building project owners who require documented lifecycle data.

Key Takeaways

- The Global Bitumen Membranes Market was valued at USD 11.2 billion in 2025 and is forecast to reach USD 16.2 billion by 2035 at a CAGR of 3.8% from 2026 to 2035.

- By Grade, Atactic Polypropylene (APP) holds the largest share at 41.2%.

- By Product Type, Sheets dominate with 67.3% of total product demand.

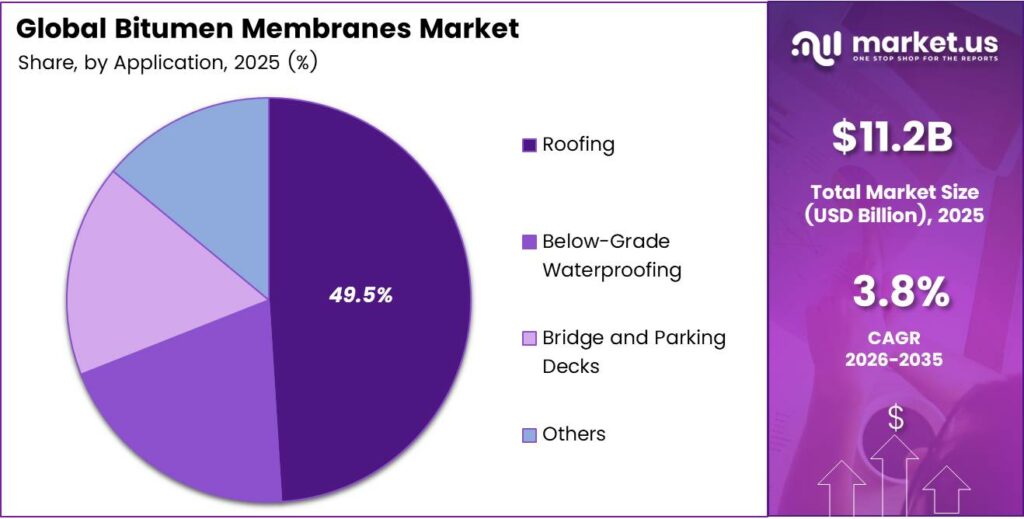

- By Application, Roofing leads with 49.5% market share.

- By Reinforcement Material, Polyester accounts for 44.7% share.

- By Installation Technology, Torch-Applied holds 38.1% of the market.

- By End-User, Residential buyers represent 52.6% of total demand.

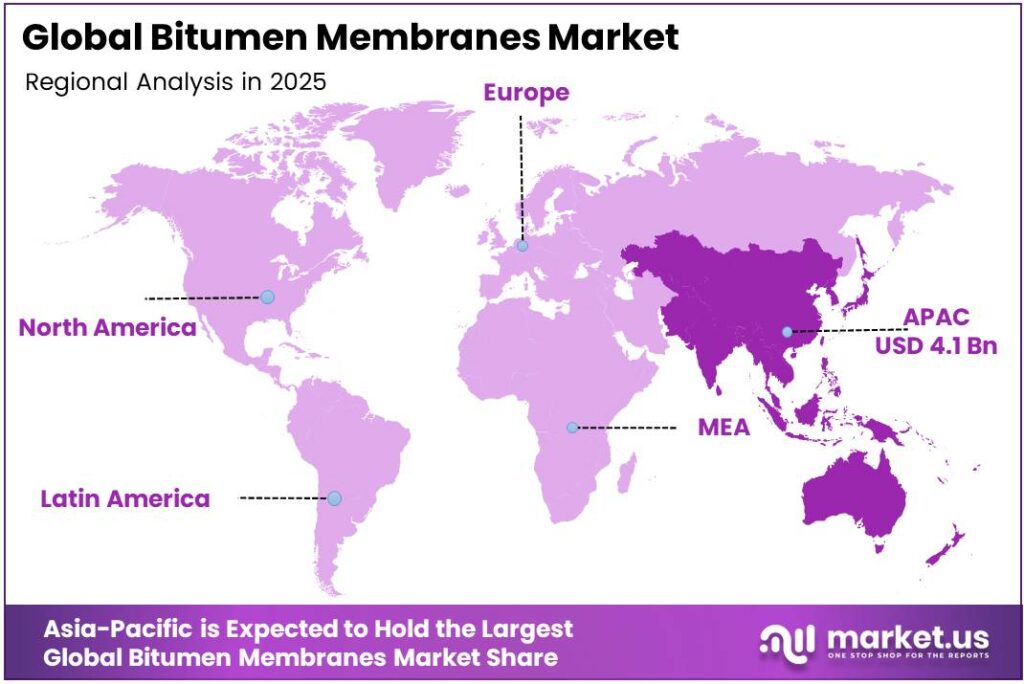

- Asia-Pacific dominates regionally with 36.8% share, valued at USD 4.1 billion.

Grade Analysis

Atactic Polypropylene (APP) dominates with 41.2% due to superior heat resistance and torch-application compatibility.

In 2025, Atactic Polypropylene (APP) held a dominant market position in the By Grade segment of the Bitumen Membranes Market, with a 41.2% share. APP-modified membranes withstand higher installation and service temperatures, making them the preferred grade for torch-applied systems — the leading installation technology globally. This thermal compatibility locks APP into the largest application and installation segments simultaneously.

Styrene-Butadiene-Styrene (SBS) modified membranes carry a critical performance advantage in cold-climate markets. SBS polymers provide superior flexibility at low temperatures, reducing crack propagation risk in freeze-thaw cycles. This elastomeric behavior makes SBS the specified grade for self-adhesive systems.

Product Type Analysis

Sheets dominate with 67.3% due to established installation infrastructure and contractor familiarity.

In 2025, Sheets held a dominant market position in the By Product Type segment of the Bitumen Membranes Market, with a 67.3% share. Sheet membranes deliver consistent thickness, predictable performance, and compatibility with multiple installation technologies — from torch-applied to self-adhesive. Their dominance reflects decades of contractor training investment and the reliability of sheet-based systems on complex roofing geometries.

Liquids serve as the secondary format, addressing penetrations, details, and areas where sheet application is impractical. Liquid-applied systems offer seamless coverage without laps or seams, reducing failure points in high-risk areas. However, liquid membranes require controlled application conditions and skilled labor, which limits their share compared to sheets in volume construction markets.

Application Analysis

Roofing dominates with 49.5% due to high volume in both new construction and retrofit activity.

In 2025, Roofing held a dominant market position in the By Application segment of the Bitumen Membranes Market, with a 49.5% share. Flat and low-slope roofing on commercial and residential buildings creates the largest and most consistent demand pool. Membrane replacement cycles of 15–25 years ensure recurring procurement volumes independent of new construction rates, providing revenue stability for membrane producers.

Below-Grade Waterproofing addresses foundations, basements, tunnels, and underground structures. This application requires membranes with high hydrostatic pressure resistance and long service life under constant moisture exposure. Infrastructure investment programs in emerging markets — particularly in Asia-Pacific — are expanding below-grade waterproofing volumes as metro rail and underground commercial developments accelerate.

Reinforcement Material Analysis

Polyester dominates with 44.7% due to high elongation and puncture resistance under mechanical stress.

In 2025, Polyester held a dominant market position in the reinforcement material segment of the Bitumen Membranes Market, with a 44.7% share. Polyester nonwoven carriers provide higher elongation at break compared to fiberglass, making them better suited for substrates subject to structural movement. This mechanical advantage supports polyester’s position in roofing and below-grade applications where substrate cracking is a real-world risk.

Fiberglass reinforcement delivers dimensional stability and higher tensile strength in the longitudinal direction. Fiberglass-reinforced membranes resist elongation, making them the preferred choice for applications requiring tight tolerances and minimal creep — such as parking deck systems and bridge deck waterproofing, where movement is controlled but load is high.

Installation Technology Analysis

Torch-Applied dominates with 38.1% due to strong bonding performance and contractor skill base.

In 2025, Torch-Applied held a dominant market position in the By Installation Technology segment of the Bitumen Membranes Market, with a 38.1% share. Torch application fuses membranes to substrates through direct heat, creating a monolithic bond that outperforms mechanically fastened or cold-applied systems in wind uplift resistance. The existing contractor training base and equipment availability reinforce this technology’s position as the default in commercial roofing markets.

Self-Adhesive membranes eliminate open-flame application, reducing fire risk on occupied buildings and simplifying regulatory compliance. Their adoption rate rises in urban renovation projects and interior waterproofing, where torch access is restricted. The self-adhesive format also shortens installation time, creating a labor cost advantage that appeals to contractors working under tight project schedules.

End-User Analysis

Residential dominates with 52.6% due to high construction volume and recurring replacement cycles.

In 2025, Residential buyers held a dominant market position in the By End-User segment of the Bitumen Membranes Market, with a 52.6% share. Housing construction and re-roofing activity generate the largest procurement volumes for bitumen membranes globally.

Commercial buyers specify membranes for flat-roof office buildings, retail centers, and logistics facilities. Commercial projects drive demand for premium-grade, energy-efficient membranes with certified solar reflectance and thermal emittance values — requirements that push buyers toward APP and reflective-coated SBS products. This segment rewards suppliers with third-party certified performance data.

Key Market Segments

By Grade

- Atactic Polypropylene (APP)

- Styrene-Butadiene-Styrene (SBS)

- Others

By Product Type

- Sheets

- Liquids

By Application

- Roofing

- Below-Grade Waterproofing

- Bridge and Parking Decks

- Others

By Reinforcement Material

- Polyester

- Fiberglass

- Composite (Polyester/Fiberglass)

- Others

By Installation Technology

- Torch-Applied

- Self-Adhesive

- Cold-Applied

- Heat-Welded and Hot-Mop

By End-User

- Residential

- Commercial

- Industrial

- Infrastructure

- Automotive

- Others

Emerging Trends

Reflective Coatings, PCM Integration, and Cold-Applied Systems Redefine Bitumen Membrane Performance Standards

Self-adhesive membrane formats gain traction as contractors prioritize speed and safety over traditional torch-applied methods. Open-flame elimination on occupied or renovation sites reduces project risk and insurance liability. This shift favors suppliers who have invested in pressure-sensitive adhesive technology compatible with both APP and SBS polymer grades.

Reflective coating integration transforms bitumen membranes from passive waterproofing into active energy management tools. SBS/bitumen/beeswax composite roofing reduced building heat load by 9.3% compared to conventional SBS binders. This measurable thermal benefit positions phase-change material roofing as a compliance solution for energy codes — not merely a sustainability preference.

Polymer-modified bitumen formulations continue to advance in both elongation and cold-temperature flexibility. Cold-applied membrane systems reduce heat exposure for installation crews and expand the range of enclosed environments where waterproofing work can proceed safely. Suppliers who certify cold-applied products against international standards capture specification-driven contracts in underground infrastructure and safety-regulated worksites.

Drivers

Commercial and Residential Construction Expansion Sustains Volume Demand for Modified Bitumen Waterproofing

Commercial and residential roofing projects across emerging economies generate consistent procurement volumes for bitumen membrane systems. Flat-roof and low-slope construction — predominant in commercial real estate — requires waterproofing systems with proven long-term performance. Modified bitumen membranes fulfill this requirement at a cost per square meter that remains competitive with thermoplastic alternatives in most markets.

Infrastructure projects — bridges, tunnels, and parking structures — demand waterproofing materials with documented tensile and puncture resistance. The Basekim 3 mm bitumen membrane achieves tensile strength of 800/600 N per 5 cm (longitudinal/transverse) with water absorption below 0.15%. These figures demonstrate the performance threshold that infrastructure procurement teams specify — a standard that drives product development investment across the membrane supplier base.

Rising adoption of polymer-modified membranes for weather resistance directly displaces conventional oxidized bitumen in specification-driven markets. APP-modified systems withstand high installation temperatures, while SBS grades accommodate structural movement and cold-climate cycling. This performance differentiation creates a clear migration pathway from commodity to modified grades, expanding revenue per unit volume for manufacturers who have invested in polymer modification capacity.

Restraints

Crude Oil Price Volatility and Environmental Compliance Costs Compress Margins Across the Bitumen Membrane Supply Chain

Bitumen is a petroleum derivative, which means membrane production costs move directly with crude oil price cycles. When crude prices spike, raw material costs rise faster than contract pricing allows manufacturers to pass through, compressing operating margins. This dynamic is most acute for producers without long-term supply agreements or vertical integration into bitumen refining.

Environmental compliance adds a second layer of cost pressure. Production-stage emissions for bituminous membranes reach 1.54 kg CO₂ eq. (A1–A3), While a recycling scenario delivers a climate benefit of -3.20 kg CO₂ eq. under Module D, this gap between production impact and end-of-life benefit signals that manufacturers who invest in recycling-compatible formulations face near-term cost increases that may not convert to pricing power until green procurement mandates tighten.

Stringent regulations on bitumen-based products — particularly in Europe — restrict certain application methods and require third-party environmental certification for public procurement. Smaller manufacturers without certification budgets or reformulation capabilities face effective market exclusion from regulated project categories. This regulatory filter consolidates volume toward large, certified suppliers and raises the barrier to entry for regional producers.

Growth Factors

Recyclable Membrane Technologies, Green Roofing Investment, and Smart City Infrastructure Unlock New Demand Pools

Eco-friendly bitumen membrane development addresses the single largest procurement barrier in European and North American institutional markets: lifecycle environmental documentation. Derbigum bitumen membranes contain up to 25% recycled material, with the Derbicoat NT underlayer reaching up to 30% recycled content. This positions recycled-content membranes as specification-ready products for green building projects that require documented material sustainability.

Green roofing systems create incremental demand for high-performance waterproofing membranes that also function as root barriers. Institutional and municipal building owners invest in green roofs to meet urban heat island mitigation targets and stormwater management requirements. Bitumen membranes with root-resistant formulations and certified durability profiles serve as the waterproofing layer in these assemblies — expanding membrane use beyond basic waterproofing into broader building performance systems.

Smart city infrastructure programs drive procurement of advanced waterproofing across transportation, utilities, and public buildings. Metro expansions, underground utility corridors, and elevated highways all require below-grade and deck waterproofing at scale. This infrastructure-led demand pool operates on multi-year procurement cycles, providing membrane suppliers with longer-horizon revenue visibility than residential construction activity.

Regional Analysis

Asia-Pacific Dominates the Bitumen Membranes Market with a Market Share of 36.8%, Valued at USD 4.1 Billion

Asia-Pacific holds a 36.8% share of the global bitumen membranes market, valued at USD 4.1 billion. China, India, and Southeast Asian nations sustain this position through active urbanization programs, metro rail expansion, and large-scale residential construction. Public infrastructure investment in the region consistently specifies waterproofing for tunnels, bridges, and below-grade structures — creating procurement volumes that dwarf other regions.

North America benefits from a large installed base of aging flat-roof commercial buildings that require membrane replacement on predictable cycles. Energy code requirements in the US — particularly for cool roofs — push commercial buyers toward reflective SBS membranes with certified solar reflectance values. This specification-driven demand supports premium pricing and product differentiation.

Europe’s market centers on sustainability compliance and product certification. The EU’s construction product regulations and green building standards require environmental product declarations and recycled-content documentation. Suppliers who meet BBA, CE marking, and EPD requirements have access to the institutional and public infrastructure segments, which represent the highest-value procurement categories in European construction.

Latin America presents volume growth driven by residential and commercial construction in Brazil and Mexico. Infrastructure investment from development banks supports bridge and road waterproofing procurement. However, price sensitivity in the region favors torch-applied APP membranes over premium self-adhesive or cold-applied systems, keeping average selling prices lower than in North America or Europe.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

ARDEX Group positions itself in the bitumen membranes market through integrated waterproofing system solutions rather than standalone membrane products. This systems approach — combining membranes with compatible primers, adhesives, and detailing products — creates higher switching costs for contractors and specifiers. ARDEX’s technical support infrastructure reinforces loyalty in commercial and infrastructure project segments where multi-product compatibility is a procurement requirement.

BASF SE leverages its polymer chemistry expertise to supply both modified bitumen membrane products and the SBS and APP polymer inputs that competitors use. This vertical positioning provides raw material cost intelligence and formulation capability that pure-play membrane manufacturers cannot match. BASF’s ability to develop next-generation polymer modifiers — including those supporting recycled-content and low-emission formulations — gives it a long-term product development advantage.

BMI Group operates as one of Europe’s largest flat-roofing system suppliers, with bitumen membrane products forming the core of its waterproofing portfolio. BMI’s pan-European distribution network and local brand presence in multiple countries reduce procurement friction for construction firms operating across borders. Its scale allows investment in product certification across multiple EU regulatory frameworks simultaneously — a capability that smaller regional producers cannot replicate cost-effectively.

Bondall serves the residential and light-commercial waterproofing segment with accessible, contractor-friendly bitumen membrane products. Its strategic positioning targets volume markets rather than high-specification institutional projects, allowing it to compete on price and availability rather than certification depth. This focus on ease of application and distribution reach gives Bondall a defensible position in markets where installation simplicity is a stronger purchasing driver than performance specification.

Key players

- ARDEX Group

- BASF SE

- BMI Group

- Bondall

- Derbigum

- Firestone Building Products Company, LLC

- GAF Materials LLC

- IKO PLC

- Isoltema SpA

- Johns Manville

- Oriental Yuhong

- RENOLIT SE

- Sika AG

Recent Developments

- In 2025, ARDEX WPM 3000X is positioned as a self-adhesive bituminous waterproofing membrane for below-ground/foundation uses, with cold application where flames are not permitted. ARDEX also issued 2024 flood-testing guidance covering torch-on and self-adhesive bituminous sheet membranes.

- In 2025, BASF is active upstream through asphalt/bitumen additives: Butonal MB 5126 was introduced as a biomass-balance asphalt modifier with 100% cradle-to-gate CO₂-footprint reduction claim; BASF also lists asphaltic waterproof-coating raw materials such as BUTONAL NS 175 for below-grade asphaltic waterproofing.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 11.2 Billion |

| Forecast Revenue (2035) | USD 16.2 Billion |

| CAGR (2026-2035) | 3.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Grade (Atactic Polypropylene (APP), Styrene-Butadiene-Styrene (SBS), Others), By Product Type (Sheets, Liquids), By Application (Roofing, Below-Grade Waterproofing, Bridge and Parking Decks, Others), By Reinforcement Material (Polyester, Fiberglass, Composite, Others), By Installation Technology (Torch-Applied, Self-Adhesive, Cold-Applied, Heat-Welded and Hot-Mop), By End-User (Residential, Commercial, Industrial, Infrastructure, Automotive, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | ARDEX Group, BASF SE, BMI Group, Bondall, Derbigum, Firestone Building Products Company LLC, GAF Materials LLC, IKO PLC, Isoltema SpA, Johns Manville, Oriental Yuhong, RENOLIT SE, Sika AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |