Quick Navigation

Report Overview

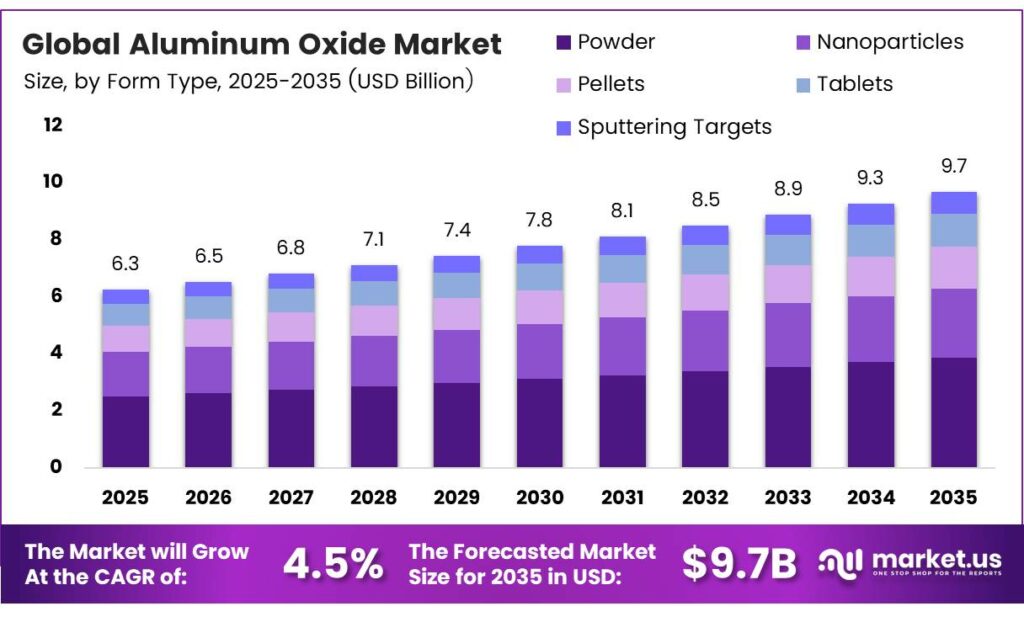

The Global Aluminum Oxide Market size is expected to be worth around USD 9.7 billion by 2035 from USD 6.3 billion in 2025, growing at a CAGR of 4.5% during the forecast period 2026 to 2035.

Aluminum oxide, also known as alumina, serves as the foundational raw material for primary aluminum production. Beyond aluminum smelting, it functions as an abrasive, refractory material, ceramic component, and chemical intermediate. This breadth of industrial utility makes alumina demand a direct proxy for industrial output health across multiple sectors.

The U.S. alumina imports reached 906,000 metric tons in the first half of 2025, marking a 49.3% increase year-over-year. This reflects refinery disruptions onshore, forcing buyers toward imported supply — a structural gap that creates sustained procurement volumes for global alumina exporters well into 2026.

China increased alumina imports to 338,315 tons in March 2026 alone, signaling rapid supply chain rebalancing across the world’s largest aluminum-producing nation. When China shifts from net exporter to active importer at this scale, it compresses global alumina availability and strengthens pricing leverage for producers outside the Chinese jurisdiction.

The market reflects accelerating industrial consumption across electric vehicles, aerospace, semiconductors, and water treatment. These are not cyclical end markets — they represent structural, decade-long investment programs. Alumina producers with diversified application portfolios stand to capture disproportionate revenue as each segment scales independently.

Key Takeaways

- The Global Aluminum Oxide Market was valued at USD 6.3 billion in 2025 and is forecast to reach USD 9.7 billion by 2035 at a CAGR of 4.5% during the forecast period 2026 to 2035.

- Powder leads with a 57.2% share, driven by broad industrial compatibility across abrasives, ceramics, and chemical processing.

- Aluminum Smelting holds the largest share at 42.5%, reflecting alumina’s primary role as a feedstock for primary aluminum production.

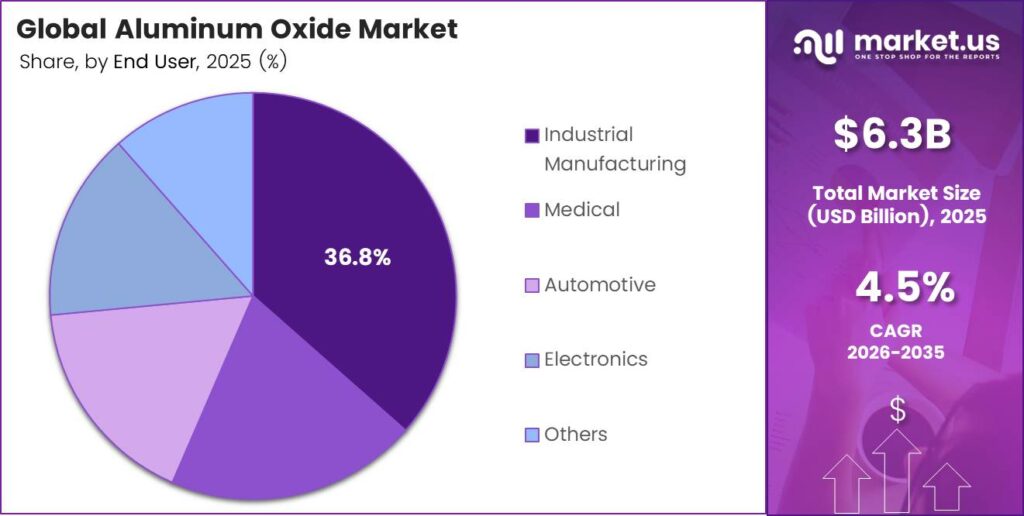

- Industrial Manufacturing dominates with 36.8%, anchored by consistent procurement volumes across smelting, refining, and precision manufacturing.

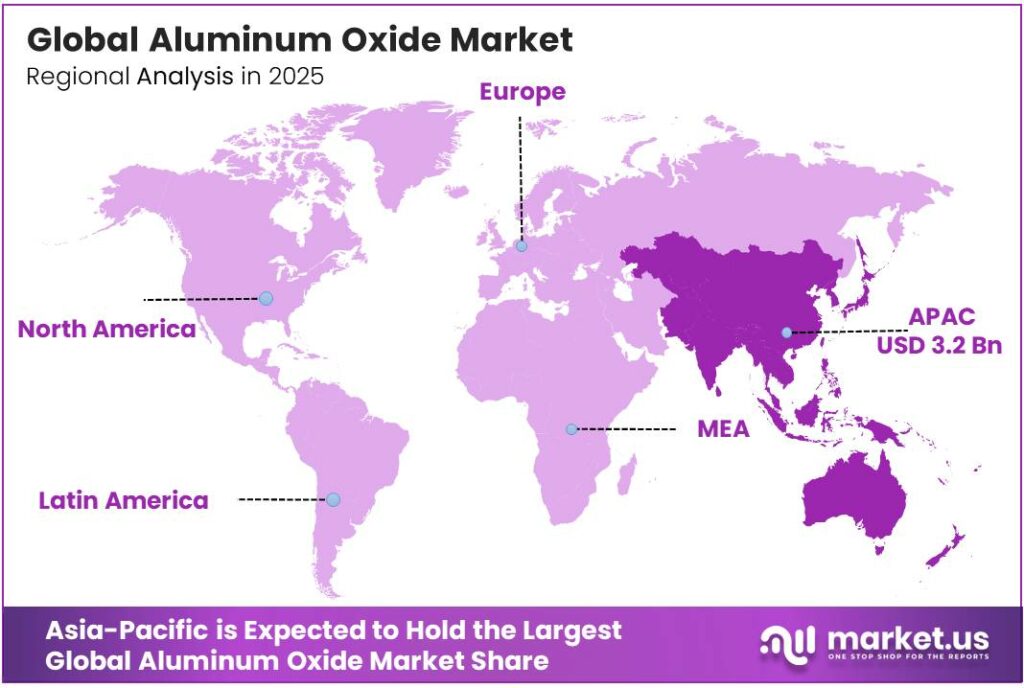

- Asia-Pacific leads regional demand with 51.3% share, valued at USD 3.2 billion, driven by China’s combined production and consumption scale.

Product Analysis

Powder dominates with 57.2% due to universal compatibility across industrial processing applications.

In 2025, Powder held a dominant market position in the By Form Type segment of the Aluminum Oxide Market, with a 57.2% share. Its fine-particle structure makes it suitable for abrasives, ceramics, catalyst carriers, and chemical intermediates. This multi-application utility removes the demand dependency risk that single-use materials carry, giving powder-grade alumina stable, diversified procurement volumes year-round.

Nanoparticles serve as the high-margin frontier of alumina form types. Their sub-100-nanometer particle size unlocks performance characteristics — thermal conductivity, surface area, and hardness — that macro-grade powders cannot match. Consequently, nanoparticle alumina commands premium pricing in electronics, battery separators, and biomedical applications, making it the fastest-scaling grade by revenue per kilogram.

Application Analysis

Aluminum Smelting dominates with 42.5% due to alumina’s irreplaceable role as primary feedstock.

In 2025, Aluminum Smelting held a dominant market position in the By Application segment of the Aluminum Oxide Market, with a 42.5% share. This fixed process ratio means smelting demand scales mechanically with aluminum output — creating a demand floor that no technology substitution can displace in the near term.

Abrasive applications occupy the second-largest position and serve the broadest range of end industries. Alumina’s hardness — rated 9 on the Mohs scale — makes it the standard abrasive grain in grinding wheels, coated abrasives, and polishing compounds across metal fabrication, automotive finishing, and electronics. This breadth insulates abrasive-grade alumina demand from single-sector slowdowns.

End User Analysis

Industrial Manufacturing dominates with 36.8% due to consistent multi-application procurement across smelting and refining.

In 2025, Industrial Manufacturing held a dominant market position in the By End User segment of the Aluminum Oxide Market, with a 36.8% share. Industrial buyers source alumina across multiple form types and applications simultaneously — combining abrasives, refractories, and chemical intermediates within a single facility.

Medical end users purchase alumina primarily for biomedical implants, dental ceramics, and laboratory consumables. Alumina’s biocompatibility, corrosion resistance, and hardness make it suitable for load-bearing orthopedic and dental applications. This segment grows independently of commodity cycles, driven instead by aging demographics and expanding access to elective surgical procedures across developed and emerging economies.

Key Market Segments

By Form Type

- Powder

- Nanoparticles

- Pellets

- Tablets

- Sputtering Targets

By Application

- Aluminum Smelting

- Abrasive

- Aluminum Chemicals

- Engineered Ceramics

- Refractories

By End User

- Industrial Manufacturing

- Medical

- Automotive

- Electronics

- Others

Emerging Trends

Ultra-High Purity Alumina and Nano-Scale Production Reshape the Electronics and Battery Supply Chain

Manufacturers of lithium-ion batteries and next-generation electronics now specify ultra-high purity alumina grades that standard refinery output cannot supply without additional processing. This purity requirement creates a two-tier alumina market — commodity-grade for smelting and specialty-grade for technology applications — with meaningfully different pricing dynamics and supplier qualifications in each tier.

The U.S. alumina imports in Q2 2025 ran 40% above Q2 2023 levels, reflecting multi-year procurement expansion that tracks closely with domestic battery manufacturing investment. This sustained import growth confirms that U.S. buyers are building strategic supply positions in alumina, not simply covering short-term gaps — a signal that specialty-grade demand has moved from project-level to program-level procurement.

Technological advances in nano-alumina surface modification now enable producers to engineer particle characteristics — surface area, reactivity, dispersibility — for specific end-use performance targets. Simultaneously, producers and buyers across the alumina value chain are increasing strategic collaborations and capacity expansions to secure supply for high-growth applications. These structural shifts give early movers in nano-alumina a durable technical differentiation advantage.

Drivers

EV Battery Demand and Aerospace Applications Pull High-Performance Alumina Into Structural Growth Trajectories

Electric vehicle manufacturers require alumina-based ceramic separators and thermal management materials that must withstand repeated charge cycles without degradation. This technical requirement ties alumina specification directly into EV platform design — meaning procurement commitments are locked years ahead of production.

Aerospace buyers specify alumina components for high-temperature stability in engine housings, thermal barriers, and structural ceramics — applications where no substitute material meets the combined weight, temperature, and mechanical stress requirements. Alumina refining and aluminum smelting together consume roughly 4.5 exajoules of energy annually, representing approximately 64% of all non-ferrous metals energy use globally.

The Aughinish Alumina refinery demonstrated that modernization projects can expand nominal capacity from 600,000 to over 1,000,000 tonnes per year — a greater than 66% increase — while simultaneously reducing site-level emissions. This precedent signals to industrial buyers that alumina supply can scale without proportional environmental liability, removing a procurement risk that had previously slowed long-term supply agreements with some buyers.

Restraints

Energy-Intensive Refining Processes and Bauxite Supply Volatility Create Structural Cost Ceilings

Alumina refining draws heavily on fossil fuels, with approximately 90% of its energy demand still sourced from non-renewable sources. This fossil fuel dependency exposes producers to both energy price volatility and escalating carbon compliance costs as emissions regulations tighten across major producing regions.

Bauxite supply concentration amplifies this cost pressure. Disruptions at a small number of mining jurisdictions — Guinea, Australia, Brazil — can tighten global alumina feedstock availability within weeks. Producers without diversified bauxite sourcing absorb supply shocks directly into their cost base, limiting their ability to hold pricing stable for downstream customers during stress periods.

Environmental compliance requirements at alumina refineries carry significant capital cost burdens. In China’s aluminum production sector, aluminum must now be sourced from renewables, and recycled aluminum output targets reached 11.5 million tonnes — directly reducing feedstock requirements for primary alumina and restructuring demand toward high-purity specialty grades.

Growth Factors

Biomedical, Additive Manufacturing, and Renewable Energy Applications Open High-Value Revenue Channels for Alumina Producers

Biomedical implant manufacturers increasingly select alumina-based ceramics for orthopedic and dental applications because of their established biocompatibility and long clinical track record. This end market grows independently of industrial cycles, driven by demographic aging and expanding surgical access. Producers who develop medical-grade alumina capabilities gain entry into a segment where specifications — not price — determine supplier selection.

Advanced 3D printing and additive manufacturing technologies now process alumina ceramics into complex geometries that traditional machining cannot produce cost-effectively. The World Economic Forum expects that by 2025, 30% of China’s aluminum production capacity must comply with national efficiency benchmarks, and 25% of electricity consumed must come from renewable sources.

Renewable energy infrastructure creates direct alumina demand through solar panel anti-reflection coatings, wind turbine ceramic components, and LED lighting substrates that use high-purity alumina. The Aughinish Alumina refinery completed a modernization program that expanded nominal production capacity from 600,000 to over 1,000,000 tonnes per year — a capacity increase exceeding 66% — while simultaneously delivering substantial reductions in site-level greenhouse gas emissions.

Regional Analysis

Asia-Pacific Dominates the Aluminum Oxide Market with a Market Share of 51.3%, Valued at USD 3.2 Billion

Asia-Pacific commands 51.3% of global aluminum oxide demand, valued at USD 3.2 billion, anchored by China’s combined role as the world’s largest aluminum producer and consumer. China’s Bayer process refinery network feeds directly into its smelter base, creating an integrated domestic demand loop that no other region can replicate.

North America’s alumina market is undergoing a supply reorientation. EV battery investment and semiconductor manufacturing expansion in the United States continue to build structural alumina demand that domestic production currently cannot satisfy without import supplementation.

Europe’s alumina consumption centers on engineered ceramics, refractories, and specialty chemicals, where the region maintains competitive manufacturing depth. Carbon compliance regulation within the EU creates procurement pressure on alumina-intensive industries to source from lower-emission suppliers or invest in domestic decarbonization.

Middle East and Africa consume alumina primarily through aluminum smelting in Gulf Cooperation Council nations, where low-cost energy historically supported large-scale smelter investment. However, as global carbon pricing mechanisms extend toward energy-intensive industries, GCC smelters face pressure to decarbonize their alumina supply chains.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Alcoa Corporation anchors its market position on integrated bauxite-to-alumina-to-aluminum operations across multiple continents. This vertical integration insulates Alcoa from spot market price volatility that affects pure-play alumina refiners. In a market where bauxite supply concentration creates procurement risk for downstream buyers, Alcoa’s mine-to-refinery control functions as a durable structural advantage — particularly for buyers who prioritize supply security over spot price optimization.

Aluminum Corporation of China Limited (Chalco) operates within China’s policy-driven industrial framework, giving it privileged access to domestic smelting capacity and government infrastructure programs. Chalco’s position at the intersection of domestic production and import coordination makes it a central actor in China’s supply rebalancing. Its scale enables procurement volumes that independent refiners cannot match.

CeramTec GmbH focuses on high-performance alumina ceramics for medical, industrial, and electronic applications, occupying the premium end of the downstream alumina market. Rather than competing on commodity refinery volume, CeramTec competes on materials science expertise and application engineering. This positioning concentrates revenue in segments where technical qualification — not price — determines supplier selection.

Evonik Industries AG leverages specialty chemical processing capabilities to produce high-purity and surface-modified alumina grades for catalysis, electronics, and pharmaceutical applications. Evonik’s customer base consists primarily of industrial buyers who embed Evonik’s alumina into their own qualified processes — creating long-duration supply relationships that are difficult to displace without requalification costs.

Key players

- Alcoa Corporation

- Aluminum Corporation of China Limited

- CeramTec GmbH

- Evonik Industries AG

- Grace Haozan Applied Material Co., Ltd.

- Honeywell International Inc.

- Huber Engineered Materials

- Merck Life Science

- Norsk Hydro ASA

- Otto Chemie Pvt. Ltd

- RusAL

- Schunk Technical Ceramics

- Sumitomo Chemical Co., Ltd

Recent Developments

- In 2025, Alcoa permanently closed its Kwinana alumina refinery in Western Australia, after earlier curtailment, and booked about $890m in restructuring-related charges. It also advanced a gallium project co-located at the Wagerup alumina refinery, supported by U.S. and Australian government initiatives; Australia’s PM said the project could produce about 10% of global gallium and receive A$200m concessional equity finance.

- In 2025, CeramTec expanded its electronic-components portfolio with Rubalit 798, a ceramic substrate containing 98% aluminum oxide, aimed at power electronics. It also showcased advanced ceramic solutions for semiconductor manufacturing at SEMICON Europa 2025, including materials such as Al₂O₃ for precision, chemical stability, thermal resistance, and wear resistance.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 6.3 Billion |

| Forecast Revenue (2035) | USD 9.7 Billion |

| CAGR (2026-2035) | 4.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form Type (Powder, Nanoparticles, Pellets, Tablets, Sputtering Targets), By Application (Aluminum Smelting, Abrasive, Aluminum Chemicals, Engineered Ceramics, Refractories), By End User (Industrial Manufacturing, Medical, Automotive, Electronics, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Alcoa Corporation, Aluminum Corporation of China Limited, CeramTec GmbH, Evonik Industries AG, Grace Haozan Applied Material Co., Ltd., Honeywell International Inc., Huber Engineered Materials, Merck Life Science, Norsk Hydro ASA, Otto Chemie Pvt. Ltd, RusAL, Schunk Technical Ceramics, Sumitomo Chemical Co., Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |