Quick Navigation

Report Overview

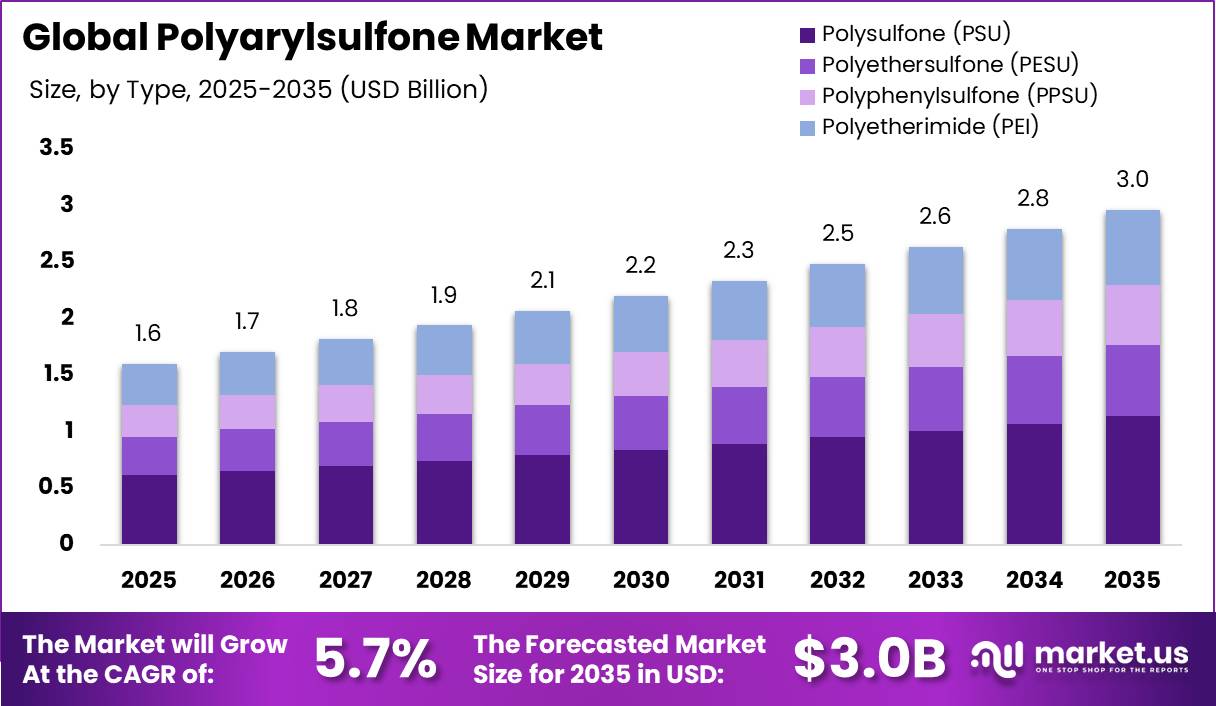

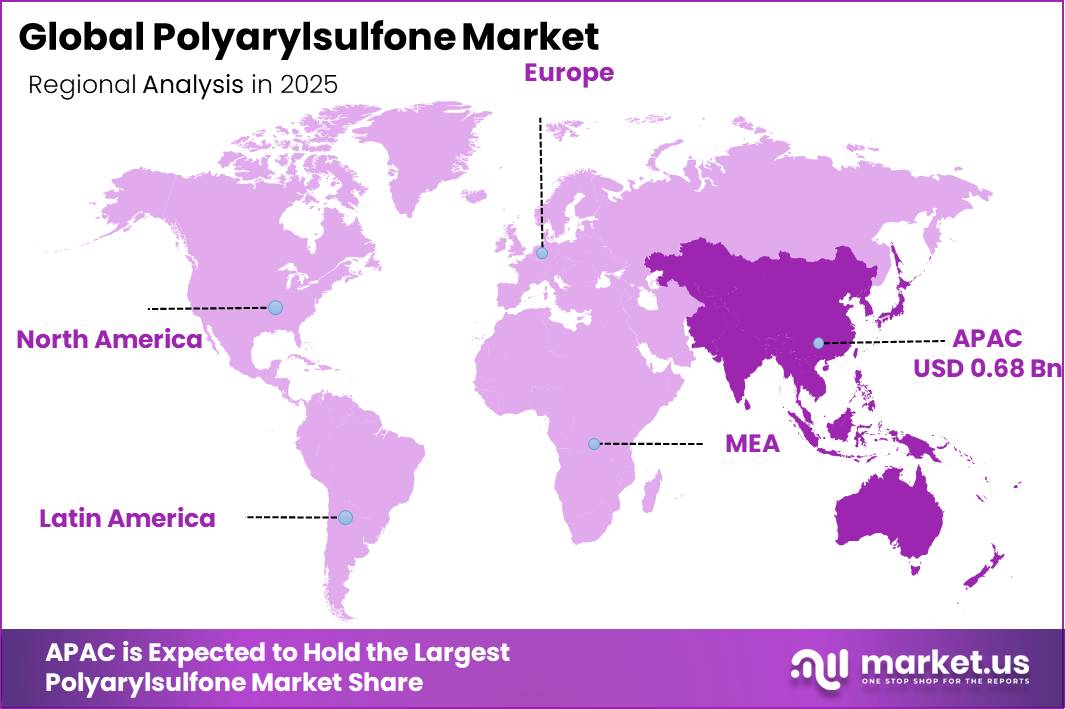

The Global Polyarylsulfone Market was valued at USD 1.6 billion in 2025 and is expected to grow to USD 3.0 billion in 2035. Between 2025 and 2035, this market is estimated to register a CAGR of 5.7%. In 2025, Asia Pacific led the market, achieving over 42.5% share with a revenue of USD 0.68 billion.

The polyarylsulfone market represents a specialized segment of the global high-performance engineering thermoplastics industry, offering materials with continuous service temperatures above 180°C, excellent mechanical strength, hydrolytic stability, and superior chemical resistance. These characteristics make polyarylsulfones suitable for demanding applications across aerospace, automotive, electronics, medical devices, and industrial processing equipment where conventional polymers cannot deliver long-term performance.

The industrial landscape is being shaped by the growing replacement of metal components with lightweight engineering polymers to improve fuel efficiency, design flexibility, and equipment durability. Polyarylsulfones are increasingly utilized in components requiring dimensional stability, flame resistance, and repeated sterilization, particularly in high-value manufacturing sectors focused on operational reliability and product longevity.

Government initiatives are further supporting industry expansion through advanced manufacturing and semiconductor investments. The U.S. CHIPS and Science Act allocates USD 52.7 billion to strengthen domestic semiconductor manufacturing, while the European Chips Act aims to mobilize EUR 43 billion and increase Europe’s share of global semiconductor production to 20% by 2030. These initiatives are expected to accelerate demand for high-performance engineering polymers used in semiconductor processing equipment and precision electronic components.

Future growth opportunities are anticipated from expanding aerospace production, medical sterilization technologies, electric mobility, advanced water treatment systems, and next-generation electronics manufacturing. Additionally, modern hybrid electric vehicles incorporate up to 3,500 semiconductor chips, increasing the need for durable, heat-resistant polymer materials that support long-term performance under demanding operating conditions.

Key Takeaways

- The global polyarylsulfone market was valued at USD 1.6 billion in 2025.

- The global polyarylsulfone market is projected to grow at a CAGR of 5.7% during the forecast period and is estimated to reach USD 3.0 billion by 2035.

- On the basis of type, Polysulfone (PSU) dominated the global polyarylsulfone market, accounting for 38.3% of the total market share in 2025.

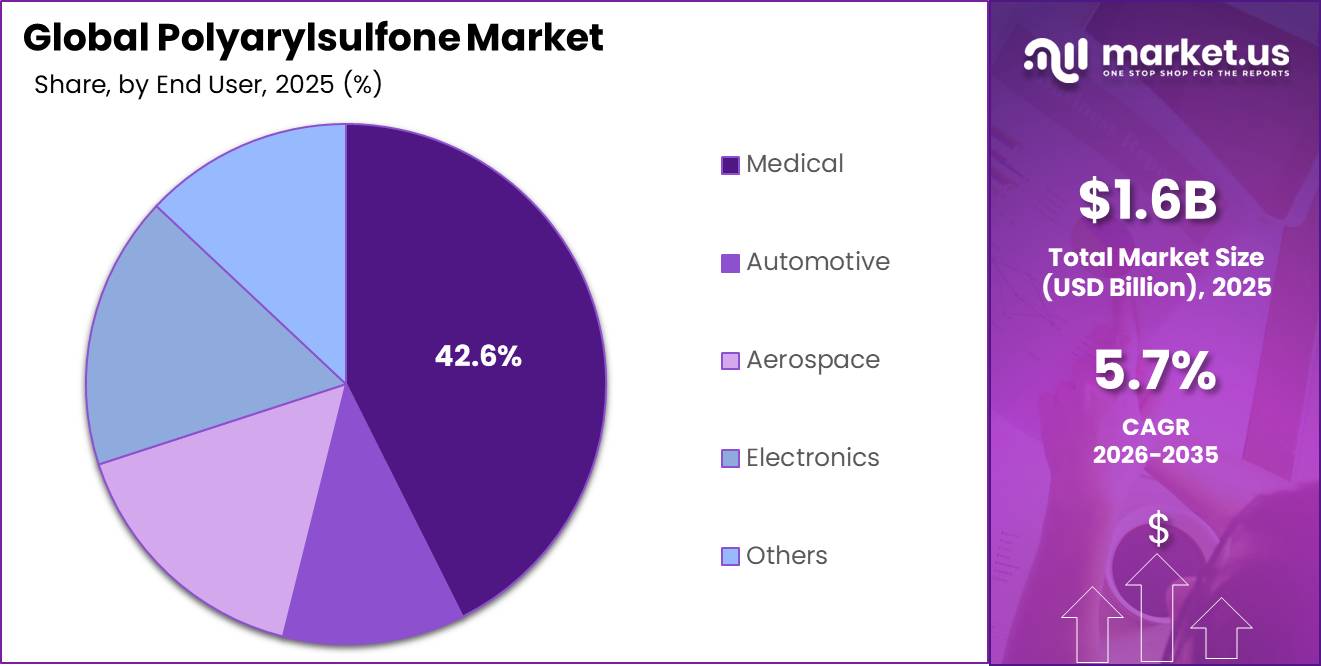

- Based on the end-user industry, the medical segment dominated the global polyarylsulfone market, capturing 42.6% of the total market share in 2025.

- In 2025, Asia Pacific emerged as the leading regional market, accounting for 42.5% of the total global polyarylsulfone market.

By Type Analysis

Polysulfone (PSU) Leads the Market While Polyetherimide (PEI) Emerges as the Fastest-Growing Segment

Polysulfone (PSU) is the dominant segment in the global Polyarylsulfone market, holding the largest share of 38.3%. PSU has earned its leading position for good reason. It strikes the right balance between high thermal stability, strong mechanical performance, and cost-effectiveness, making it a practical and reliable choice for a wide range of applications.

From filtration systems and medical devices to food processing equipment and industrial components, PSU is trusted across industries precisely because it delivers consistent, high-quality performance without the premium price tag associated with more specialized polymers. Its long-established track record and broad regulatory acceptance in medical and food-contact applications further cement its position as the most widely adopted material in the polyarylsulfone family.

Polyetherimide (PEI) is the fastest-growing segment in the global Polyarylsulfone market. What is driving PEI’s rise is its ability to perform exceptionally well in conditions where most materials simply cannot keep up: extreme heat, aggressive chemicals, and high mechanical stress. Industries such as aerospace, electronics, automotive, and medical devices are increasingly turning to PEI as their material of choice because it combines outstanding heat resistance with remarkable dimensional precision, even under the most demanding operating conditions.

End Use Analysis

Medical Sector Leads the Market While Electronics Emerges as the Fastest-Growing Segment

The Medical sector is the dominant end-user segment in the global Polyarylsulfone market, accounting for the largest share of 42.6%. The medical industry’s reliance on polyarylsulfone materials comes down to one simple but critical requirement: the need for materials that are safe, durable, and capable of withstanding repeated sterilization without breaking down or losing performance.

Polyarylsulfone materials, particularly PSU and PPSU, tick all of these boxes, making them a natural fit for medical devices, surgical instruments, sterilization trays, dialysis equipment, and hospital-grade filtration systems. Their proven biocompatibility and regulatory acceptance across major healthcare markets further strengthen their position as the material of choice in an industry where safety and reliability are absolutely non-negotiable.

The Electronics sector is emerging as the fastest-growing end-user segment. As electronic devices become smaller, more powerful, and more complex, the materials used to build them need to keep up, and polyarylsulfone materials are increasingly rising to meet that challenge. Their excellent electrical insulation properties, high heat resistance, and dimensional stability under thermal stress make them particularly well-suited for printed circuit boards, semiconductor components, connectors, and other precision electronic parts where performance under demanding conditions is essential.

Key Market Segments

By Type Analysis

- Polysulfone (PSU)

- Polyethersulfone (PESU)

- Polyphenylsulfone (PPSU)

- Polyetherimide (PEI)

By End User Industry

- Automotive

- Aerospace

- Electronics

- Medical

- Others

Market Dynamics

Challenges

Sulfone polymer production, including PAS, is more energy- and emissions-intensive than many engineering plastics due to high-temperature polymerization and solvent-intensive processing. Compared with some engineering plastics, cradle-to-gate carbon footprints can be 30–60% higher, while many OEMs are targeting 20–40% reductions in product-level emissions by 2030, increasing pressure to adopt lower-carbon materials.

PAS manufacturing is highly dependent on electricity and steam, and energy price increases of 20–30% can raise conversion costs by mid-single digits. In addition, carbon pricing mechanisms may add €50–100 per ton of embedded CO₂, increasing delivered PAS prices by 2–4% in regulated markets and reducing competitiveness in cost-sensitive applications.

Manufacturers are responding by investing in energy-efficiency upgrades capable of reducing specific energy consumption by 10–20%, alongside renewable power sourcing and lower-carbon raw materials. However, these improvements typically require 4–8 years to achieve full-scale impact, while energy costs and emissions concerns are estimated to reduce achievable market CAGR by around 0.5 percentage points.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| BPA-linked feedstock volatility | -1.0% | North America, EU, East Asia | Medium term (2–4 years) |

| Limited sulfone processing expertise | -0.8% | North America core, EU industrial, APAC emerging | Long term (≥ 4 years) |

| High-spec medical & membrane qualification cycles | -0.7% | EU regulatory hubs, North America, APAC medtech clusters | Medium term (2–4 years) |

| Concentrated supplier & capacity clustering | -0.6% | North America, Europe, China, Japan | Long term (≥ 4 years) |

| Energy & emissions intensity of sulfone polymers | -0.5% | EU regulatory hubs, North America, East Asia | Long term (≥ 4 years) |

| Competing advanced polymers in key niches | -0.4% | Global OEM platforms | Medium term (2–4 years) |

Opportunity

High-flux bioprocessing membrane platforms represent a significant growth opportunity for polyarylsulfone (PAS), as suppliers currently focus mainly on resin and membrane materials rather than higher-value integrated systems. PAS membranes offer high-temperature sterilization, pH 1–13 chemical stability, and low protein adsorption, making them well suited for advanced biopharmaceutical filtration.

Expanding into pre-sterilized filter assemblies, cassette modules, and single-use bioprocessing platforms for cell and gene therapy, continuous bioprocessing, and vaccine production could add 1.5–2.0% points to market CAGR. System-level products can achieve 40–45% gross margins, compared with 20–25% for conventional membrane materials.

An estimated US$1.0–1.5 billion bioprocessing-grade PAS market remains underpenetrated due to the industry’s traditional B2B supply model. Suppliers that secure 7–10-year qualified-vendor agreements with leading biopharma manufacturers can increase average selling prices by 15–25% while expanding revenue beyond raw material sales.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| High-flux bioprocessing membrane platforms | +2.0% | North America, EU, APAC emerging | Medium term (2–4 years) |

| Metal-replacement in e-mobility and aviation | +1.5% | North America core, EU, China | Medium term (2–4 years) |

| Next-gen reusable medical devices | +1.8% | North America, EU, India, ASEAN | Short term (≤ 2 years) |

| Hydrogen and battery thermal management | +1.3% | EU, China, Middle East, North America | Long term (≥ 4 years) |

| Water reuse and industrial ZLD membranes | +1.6% | APAC emerging, Middle East, Latin America | Medium term (2–4 years) |

| Specialty compounding and tolling platforms | +1.0% | Global OEM hubs | Short-medium term (≤ 4 years) |

Drivers

Electrical, electronics, and EV thermal management are key growth areas for PAS, supporting applications such as circuit-breaker housings, connectors, busbars, and high-voltage EV components. Its high heat-deflection temperature, dielectric strength, and hydrolysis resistance make it suitable for demanding power electronics.

The high-performance thermoplastics market for electrical and electronics applications is projected to grow at around 5–6% annually through 2035, driven by expanding demand from data centers, 5G infrastructure, industrial automation, and electric vehicles. PAS compounds also improve thermal management and reliability in battery-adjacent EV components.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulated healthcare & sterilizable medical devices | +2.0% | North America core, EU, APAC corridors | Medium term (2–4 years) |

| Water & wastewater treatment membranes expansion | +1.5% | APAC corridors, Middle East, EU | Long term (≥ 4 years) |

| Lightweighting in automotive & aerospace | +1.2% | North America core, EU, APAC corridors | Medium term (2–4 years) |

| Electrical, electronics & EV thermal management | +1.0% | APAC corridors, North America, EU | Short to medium term (≤ 4 years) |

| APAC industrialization & local PAS capacity | +0.8% | APAC corridors, South America spill-over | Long term (≥ 4 years) |

| Petrochemical feedstock & geopolitical volatility | +0.5% (pricing-led) | Global, especially EU & Middle East routes | Short to long term (≤ 2 years and beyond) |

Restraints

Stricter environmental regulations on VOC emissions, hazardous waste, and worker exposure are increasing PAS production costs across the EU, North America, Japan, and South Korea. New EU emissions rules can raise plant operating costs by 5–7%, while U.S. state regulations may require US$20–40 million in additional capital investment per mid-scale facility over 3–5 years.

These requirements increase overall PAS production costs by 6–10% in regulated regions and extend permitting timelines from 12–18 months to 24–30 months for new plants and major expansions. As a result, 15–20% of planned global capacity additions may be delayed beyond 2028, reducing achievable market CAGR by around 0.7%.

For aerospace, medical, and water treatment OEMs, slower availability of certified low-emission PAS grades increases qualification complexity and supply constraints. This can reduce supplier margins by 100–150 basis points on long-term contracts, limiting PAS adoption in highly regulated applications.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High raw material and energy cost volatility | -1.0% | EU, North America core, China | Short-Medium term |

| Environmental and process regulatory tightening | -0.7% | EU, North America, Japan, South Korea | Medium-Long term |

| Supply concentration and capacity bottlenecks | -0.9% | China, EU, North America | Short-Medium term |

| End-use qualification and substitution risk | -0.6% | Global aerospace, medical, filtration corridors | Medium term |

| Capital-intensive scale-up and ROIC drag | -0.5% | Global, with focus on APAC growth hubs | Long term |

| Currency, trade and tariff friction | -0.4% | EU-China, US-China, emerging APAC | Short-Medium term |

Geopolitical Impact Analysis

The international market of polyarylsulfone depends greatly on the political climate in different nations, foreign policies of trading partners, and the availability of raw materials needed in the production process. This is because polyarylsulfone is a highly specialized engineering plastic that requires access to specialty chemicals and expensive energy for production purposes. Any changes in the price of raw materials and energy sources could affect the manufacturing cost of this product significantly.

Trade policies and rules regulating imports and exports are equally important factors that influence market trends. More nations have been making efforts to boost local production and become less dependent on imported polymers. The gradual restructuring of the global supply chains is favoring regional production in areas like Asia-Pacific, Europe, and North America.

Geopolitical instability, transport bottlenecks, and high freight rates may cause short-term supply challenges for producers and downstream industries. Nevertheless, the sustained demand from vital sectors like medicine, electronics, wastewater treatment, and automotive ensures that the international market remains steady. The demand for high-performance polymers persists under all circumstances.

Regional Analysis

Asia Pacific Dominates the Global Polyarylsulfone Market

Asia Pacific is the clear leader in the global Polyarylsulfone market, holding the largest regional share of 42.5%. And when you look at what is happening across the region, it is easy to see why. Countries like China, India, Japan, and South Korea are growing fast, building out their manufacturing capabilities, and investing heavily in healthcare, electronics, and automotive industries that all have a strong and growing appetite for high-performance materials like polyarylsulfone.

Hospitals and medical device manufacturers across the region are turning to polyarylsulfone for equipment that needs to handle repeated sterilization without breaking down, while electronics and automotive manufacturers value it for its ability to perform reliably under heat and mechanical stress. On top of all this, growing concerns about clean water access across parts of Asia are driving increased use of polyarylsulfone membranes in water purification projects, making this region a broad, diverse, and deeply rooted market for the material.

North America, while currently smaller in overall share, is shaping up to be the most exciting growth story in the global Polyarylsulfone market right now. The region has all the right ingredients for accelerated growth: a world-class healthcare system that demands the best materials for medical devices, a thriving aerospace industry that is always looking for lighter and more durable components, and a technology sector that keeps pushing the boundaries of what electronic systems need to do.

Key Regions and Countries Covered in this Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global Polyarylsulfone market is characterized by high competition, with businesses emphasizing quality products, efficient material performance, and cost management. Major firms constantly strive to enhance the heat resistance, durability, and chemical stability of Polyarylsulfone through continuous R&D activities. As Polyarylsulfone is utilized by key industries including healthcare, automobile, electronics, and aerospace, firms need to ensure that the quality standards and supply levels are maintained at all times.

Firms operating in this industry are making efforts towards enhancing their portfolio of offerings and building effective international supply chain networks. Numerous firms are engaging in long-term business collaboration with end-users from industries such as medical devices manufacturing, filtration systems manufacturing, and industrial machinery. Moreover, strategic acquisition and merger activity is also seen among players for achieving a dominant market position.

The cost containment process and manufacturing technology advancement are equally significant when talking about competition. Companies today are resorting to sophisticated processes for the manufacturing of polymers in order to save on costs. There is increasing demand for polymers from the Asia Pacific region as well.

The Following are some of the Major Players in the Industry

- Arkema

- BASF SE

- Celanese Corporation

- Ensinger

- Evonik Industries AG

- Mitsubishi Chemical Corporation

- Polymer Dynamix

- Polymer Industries

- Quadrant Plastics Composites AG

- RTP Company

- SABIC

- Solvay

Key Development

- In February 2025, Evonik Industries AG signed a supply contract with a major aerospace manufacturer to provide polyarylsulfone materials for next-generation aircraft interiors. This agreement highlighted the growing adoption of lightweight, flame-resistant polymers in the aerospace sector as manufacturers seek alternatives to traditional metal components.

- In August 2023, Solvay expanded its medical-grade PSU portfolio with a new product specifically designed for implantable devices. This move was aimed at addressing the increasing demand for biocompatible and sterilization-resistant materials in the global healthcare industry

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 1.6 Bn |

| Forecast Revenue (2035) | US$ 3.0 Bn |

| CAGR (2026-2035) | 5.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Polyetherimide (PEI), Polyethersulfone (PESU), Polysulfone (PSU), and Polyphenylsulfone (PPSU)), By End-Uses (Food and Beverages, Electrical And Electronics, Automotive, Healthcare, Water Treatment, Aerospace, and Other End-Uses) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Arkema, BASF SE, Celanese Corporation, Ensinger, Evonik Industries AG, Mitsubishi Chemical Corporation, Polymer Dynamix, Polymer Industries, Quadrant Plastics Composites AG, RTP Company, SABIC, Solvay |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |