Quick Navigation

Report Overview

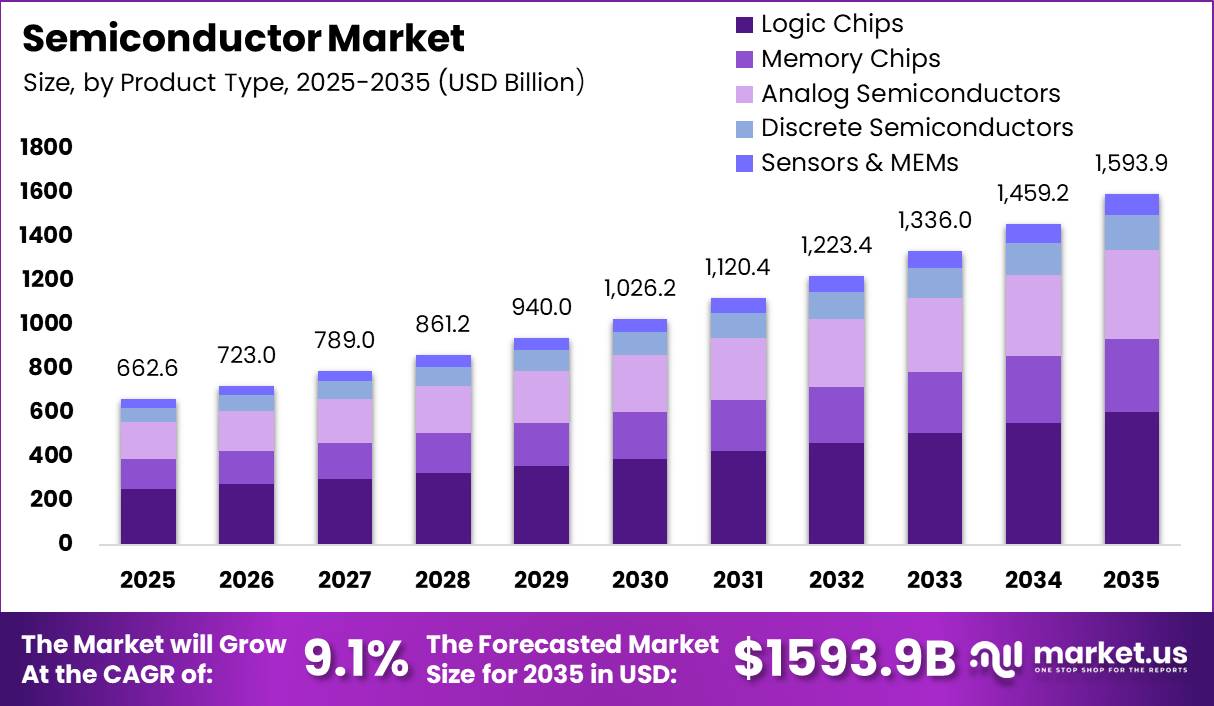

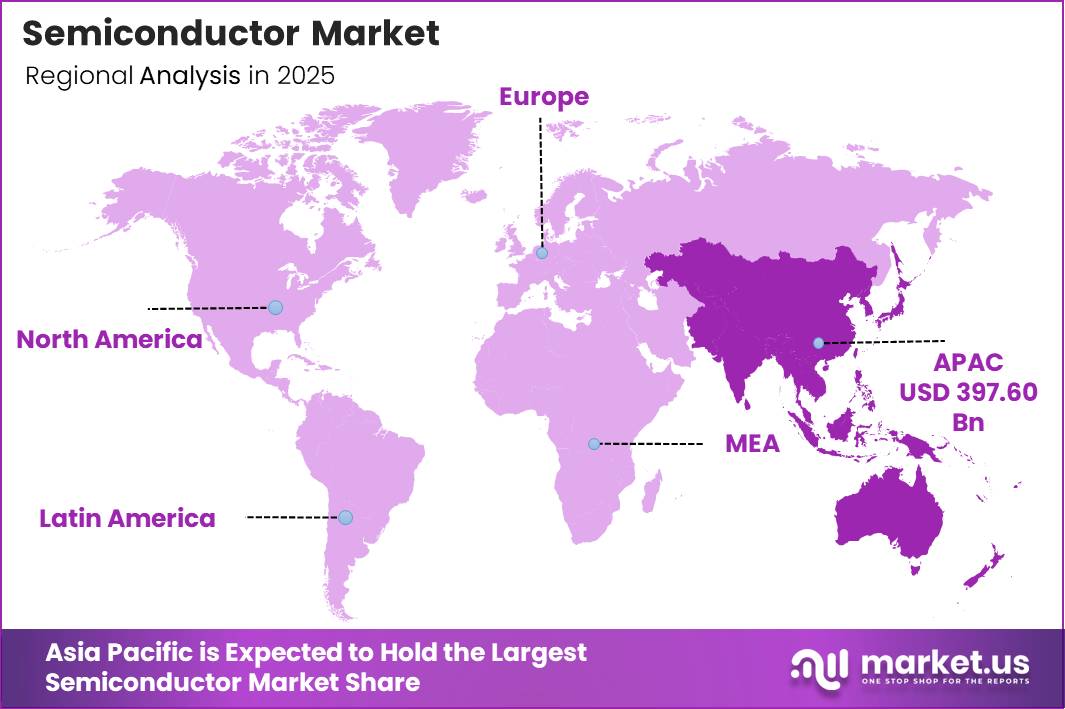

In 2025, the Global Semiconductor Market was valued at USD 662.6 billion. The market is projected to grow at a CAGR of 9.1% during 2026–2035, reaching approximately USD 1593.9 billion by 2035. Asia Pacific dominated the global market in 2025, accounting for more than 60.0% of the total market share and generating approximately USD 397.6 billion in revenue.

This growth is being supported by rising demand for artificial intelligence systems, consumer electronics, electric vehicles, industrial automation, and advanced data centres. According to the World Semiconductor Trade Statistics and the Semiconductor Industry Association, global semiconductor sales approached USD 800 billion in 2025, led mainly by strong demand for logic and memory chips used in AI servers and cloud infrastructure. Industry revenues are also expected to exceed USD 1 trillion by 2026.

Data-centre expansion will remain an important demand driver, as the International Energy Agency expects global data-centre electricity consumption to reach around 945 TWh by 2030, nearly double the current level. This will increase the need for high-performance processors, accelerators, power-management chips, and memory devices. Consumer and automotive demand will also contribute significantly.

Smartphone shipments reached nearly 1.26 billion units in 2025, while global electric car sales were expected to exceed 20 million units, representing more than 25% of total vehicle sales. Asia Pacific is supported by its strong position in chip manufacturing, electronics assembly, foundries, smartphones, electric vehicles, and data-centre equipment production.

Key Takeaway

- The Semiconductor Market was valued at USD 662.6 billion in 2025 and is projected to reach USD 1593.9 billion by 2035, growing at a CAGR of 9.1%.

- Logic chips held the largest product-type share at 38.0%, while analog semiconductors were the fastest-growing device segment.

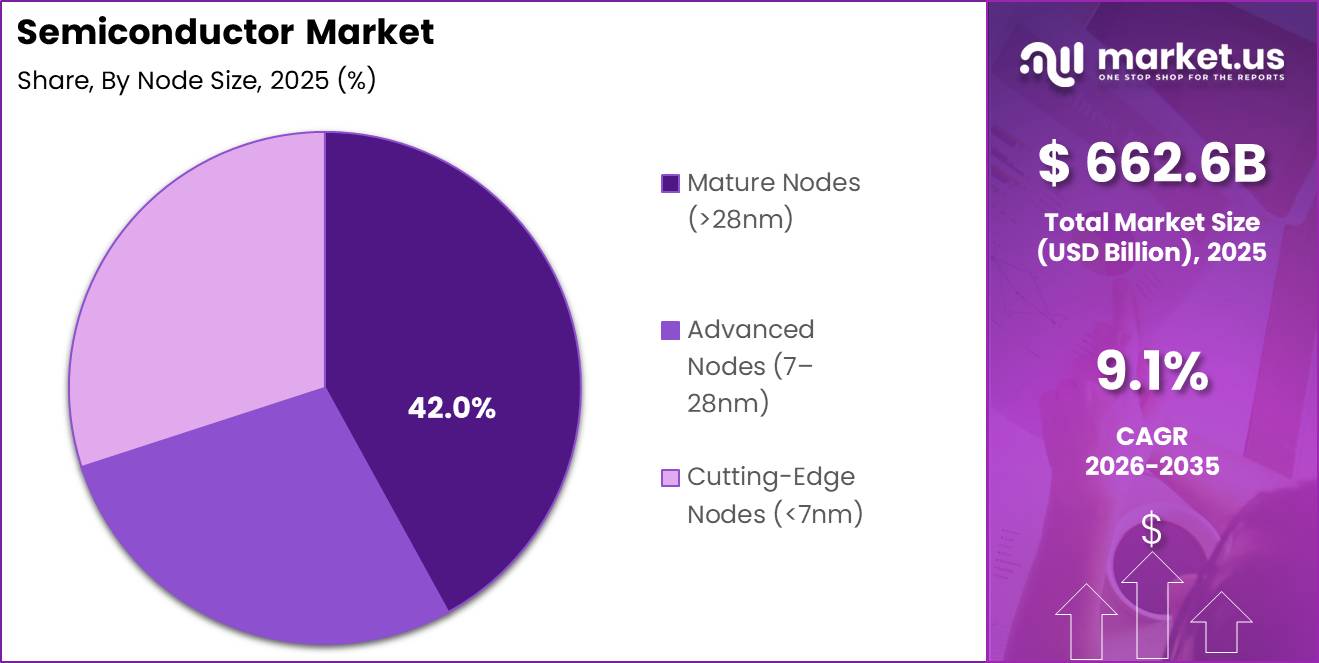

- Mature nodes above 28 nm accounted for around 42.0% of the market, while nodes below 7 nm were the fastest-growing segment.

- Consumer electronics led both applications and end users with a 28.0% share, while data centres and AI represented the fastest-growing segment.

- Asia Pacific led the market with more than 60.0% share, generating approximately USD 397.60 billion in 2025.

By Product Type

Logic chips held a leading 38.0% share of the semiconductor market, supported by their essential role in smartphones, personal computers, servers, networking equipment, vehicles, and industrial systems. These chips process instructions, control data movement, and coordinate communication between memory, sensors, storage, and power components. As AI servers, advanced telecom networks, and autonomous vehicles require several high-value processors and controllers, demand for complex logic devices continues to rise.

Meanwhile, Analog semiconductors represent the fastest-growing device segment because they connect digital systems with real-world signals such as temperature, pressure, sound, motion, and voltage. They are also widely used for power control in batteries, charging systems, inverters, motor drives, and electric vehicles.

According to the International Federation of Robotics, around 542,000 industrial robots were installed worldwide in 2024, while the global operational robot stock reached approximately 4.7 million units. Asia accounted for nearly 75% of new robot installations, highlighting the region’s strong automation activity. Each industrial robot, electric vehicle powertrain, and automated production line requires several analog integrated circuits for sensor processing, voltage regulation, and motor control.

By Node Size

Mature semiconductor nodes above 28 nm held around 42.0% of the market, supported by their lower production cost, proven reliability, and long operating life. These nodes remain widely used in automotive electronics, industrial equipment, household appliances, and consumer devices that do not require the highest computing performance.

China has been expanding its mature-node manufacturing capacity, with industry estimates suggesting that its output for 28 nm and above technologies could account for nearly one-third of global capacity by 2025 and exceed 10 million wafers per month. Much of this production is expected to support vehicles, home appliances, power systems, and industrial control equipment.

In comparison, advanced nodes below 7 nm are emerging as the fastest-growing segment because they are essential for AI accelerators, premium smartphone processors, cloud computing CPUs, and other high-performance applications. Smaller chip geometries improve computing power, energy efficiency, and processing density, making them important for data centres and next-generation electronics.

By Application

Consumer electronics held a leading 28.0% share of the semiconductor market, supported by the high volume of chips used in smartphones, personal computers, televisions, wearable devices, and connected home products. According to IDC, global PC shipments reached approximately 260 million units in 2025, while quarterly shipments were close to 76 million units, driven by device replacement, new operating systems, and hybrid working needs.

Each computer requires multiple CPUs, GPUs, memory chips, controllers, and interface components. Television demand also supports semiconductor consumption, as global TV shipments exceeded 47 million units during a weaker quarter of 2025. Modern televisions use video processors, tuners, Wi-Fi and Bluetooth chipsets, display drivers, and power-management ICs.

Meanwhile, data centres and AI represent the fastest-growing application segment. According to the International Energy Agency, data centres consumed around 240–340 TWh of electricity in 2022, with some scenarios indicating consumption could exceed 1,000 TWh by 2026. This expansion requires large numbers of CPUs, GPUs, AI accelerators, networking chips, and advanced memory devices.

By End User

Consumer electronics OEMs held a leading 28.0% share of the semiconductor end-user market, supported by the large number of chip-based products manufactured and sold worldwide. Major electronics producers ship hundreds of millions of smartphones, personal computers, televisions, wearable devices, and smart home products each year.

Every finished device requires several processors, memory chips, connectivity components, sensors, display controllers, and power-management ICs. Regular product upgrades and replacement cycles therefore create steady and recurring semiconductor demand from consumer electronics manufacturers.

Meanwhile, cloud and data centre companies represent the fastest-growing end-user segment as they expand artificial intelligence and high-performance computing infrastructure. According to the International Energy Agency, data centres consumed around 460 TWh of electricity in 2022, and consumption could exceed 1,000 TWh by 2026. This increase reflects the rapid installation of advanced CPUs, GPUs, AI accelerators, storage systems, networking chips, and high-bandwidth memory.

Industry data also indicated that global data centre capital expenditure reached approximately USD 455 billion in 2024, while worldwide server revenue totalled nearly USD 236 billion. GPU-based accelerated servers contributed a major share of server revenue growth, directly increasing semiconductor purchases by hyperscale cloud operators and AI service providers.

Key Market Segments

By Product Type

- Logic Chips

- AI / ML Processors

- CPUs

- FPGAs

- ASICs

- Memory Chips

- DRAM

- NAND Flash

- Analog Semiconductors

- Power Management ICs

- RF Chips

- Discrete Semiconductors

- Sensors & MEMs

By Node Size

- Mature Nodes (>28nm)

- Advanced Nodes (7–28nm)

- Cutting-Edge Nodes (<7nm)

- 3nm Node

- 5nm Node

- 7nm Node

By Application

- Consumer Electronics

- Smartphones

- PCs / Laptops

- Data Centers & AI

- AI Accelerators

- Cloud Server Chips

- Automotive

- ADAS Chips

- EV Power Chips

- Industrial

- Communications

- Others

By End User

- Consumer Electronics OEMs

- Cloud & Data Center Companies

- Automotive OEMs

- Industrial Companies

- Telecom Companies

- Defense & Aerospace

- Others

Geopolitical Impact Analysis

Geopolitical tensions are increasing semiconductor production costs and weakening supply reliability. US–China trade restrictions have placed several semiconductor materials, manufacturing tools, and equipment under Section 301 tariffs, exposing selected imports to additional duties of up to 25%. These tariffs raise the delivered cost of specialty chemicals, front-end production tools, and capital equipment used by US semiconductor plants.

Supply risks have also increased since China introduced export controls on gallium and germanium in 2023, requiring exporters to obtain licences. China accounts for more than 90% of global gallium production and 83% of germanium production. It also supplies over 70% of EU gallium imports and 45% of EU germanium imports.

These restrictions are encouraging chipmakers to diversify suppliers, maintain larger inventories, and enter long-term purchasing contracts, increasing wafer and device prices. Logistics disruptions are creating additional pressure. According to UNCTAD, Red Sea attacks and lower Suez Canal activity reduced container traffic through the route by around 67%.

Ships rerouted through the Cape of Good Hope face delays of approximately 10–14 days and fuel-cost increases of nearly 40%. In 2024, container freight rates increased by up to 276% on Far East–Northwest Europe routes and 167% on Far East–Mediterranean routes, while average shipping costs from Shanghai more than doubled compared with late 2023.

Regional Analysis

Asia Pacific held a dominant position in the global semiconductor market, accounting for around a 60.0% share and generating approximately USD 397.6 billion in 2025. The region benefits from a strong and connected semiconductor ecosystem that covers wafer fabrication, chip design, packaging, testing, and final electronics assembly.

Taiwan and South Korea remain major foundry and memory production centres, while Japan has a strong presence in semiconductor materials, equipment, and integrated device manufacturing. China, ASEAN countries, and India also support regional growth through large-scale production of smartphones, consumer electronics, electric vehicles, industrial machinery, and other chip-based products.

Strong domestic demand allows a large portion of semiconductor output to be consumed within the region. New capacity for mature and advanced semiconductor nodes is therefore being added across the region. Supported by continued capital investment and rising demand, Asia Pacific is expected to remain both the largest and fastest-growing regional market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Drivers

| Driver | (~) % CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI & Data Center Infrastructure Demand | +3.2% | Global — concentrated in North America, East Asia | Short term (≤ 2 years) |

| Government Subsidy & Industrial Policy Stimulus | +1.8% | USA, EU, Japan, India, South Korea | Medium term (2–4 years) |

| Automotive Electrification & ADAS Adoption | +1.4% | Europe, China, North America | Medium term (2–4 years) |

| 5G Network Densification & Infrastructure Rollout | +1.1% | Asia-Pacific, Middle East, Emerging Markets | Short term (≤ 2 years) |

| Memory Supercycle & HBM Price Appreciation | +0.9% | South Korea, USA, Taiwan | Short term (≤ 2 years) |

| Industrial IoT & Smart Manufacturing Expansion | +0.7% | Germany, China, Japan, USA | Medium term (2–4 years) |

AI & Data Center Infrastructure Demand

Generative AI model training and inference workloads have structurally reorganized semiconductor demand hierarchies, making leading-edge logic and high-bandwidth memory the fastest-growing product categories in the industry, each expanding at CAGRs exceeding 20% through the end of the decade, per McKinsey’s January 2026 analysis, versus a 9.1% baseline for the broader market.

The proximate mechanism is a self-reinforcing CapEx cycle: hyperscale cloud operators and sovereign AI programs collectively committed to infrastructure expenditure at a pace that drove generative AI chip revenues above $125 billion in 2024 and likely above $150 billion in 2025, with AI data centers estimated to absorb approximately 70% of high-end DRAM supply in 2026 alone.

This concentration effect compresses addressable supply for non-AI segments while simultaneously inflating blended ASPs across logic and memory product lines a dual mechanism that lifts nominal revenue growth substantially above unit-volume growth, widening operating margins for leading foundries and IDMs even as wafer starts remain capacity-constrained at advanced nodes below 5nm.

Restraints

| Restraint | (~) % CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| US–China Multilateral Export Control Regime | -2.1% | USA, China, Netherlands, Japan, Taiwan | Short term (≤ 2 years) |

| Prohibitive Leading-Edge Fab Construction Costs | -1.5% | USA, Europe — relative to Asia incumbents | Medium term (2–4 years) |

| Geopolitical Taiwan Strait Supply Concentration Risk | -1.2% | Global — sourcing concentrated in Taiwan | Short term (≤ 2 years) |

| Escalating Semiconductor Tariff Uncertainty | -0.9% | USA, China, EU bilateral corridors | Short term (≤ 2 years) |

| Water & Energy Resource Scarcity for Fab Operations | -0.6% | Taiwan, Arizona (USA), South Korea | Long term (≥ 4 years) |

US–China Multilateral Export Control Regime

The U.S. export-control framework, introduced in October 2022 and expanded in 2023, 2024, and early 2026, has divided the global semiconductor market. The rules restrict Chinese access to logic chips below 14 nm/16 nm FinFET, DRAM at 18 nm half-pitch or finer, NAND with 128 layers or more, and the equipment required to manufacture these technologies.

As of January 2026, TSMC, Samsung, and SK Hynix must apply annually for U.S. export licences to operate their fabrication plants in China, replacing earlier standing approvals. NVIDIA’s H200 sales to China were conditionally permitted under a framework that imposed a 25% Section 232 tariff and limited shipments to approximately 1 million H200 units, below reported Chinese order volumes.

China represents nearly two-thirds of Asia Pacific semiconductor consumption, making these restrictions commercially significant. The controls are keeping much of China’s production focused on mature nodes while encouraging domestic investment in semiconductor self-sufficiency.

Challenges

| Challenge | (~) % CAGR | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Structural Engineering Talent Deficit | -1.4% | USA, Europe, India — greenfield fab regions | Long term (≥ 4 years) |

| Transistor Scaling Physical Limits | -1.1% | Global — leading-edge foundries in Taiwan, South Korea | Long term (≥ 4 years) |

| Supply Chain Single-Region Concentration | -0.9% | Global — sourcing dependency on East Asia | Medium term (2–4 years) |

| Cyclical Memory Oversupply Overhang Risk | -0.8% | South Korea, USA (Micron), China memory fabs | Medium term (2–4 years) |

| Semiconductor IP Cybersecurity Vulnerabilities | -0.5% | Global — particularly USA, Taiwan, EU | Long term (≥ 4 years) |

Structural Engineering Talent Deficit

The semiconductor workforce shortage is a long-term structural issue rather than a temporary cycle. The Semiconductor Industry Association’s 2024 report projected a U.S. shortfall of around 67,000 workers by 2030, including nearly 26,000 technicians, 23,000 bachelor’s-level engineers or computer scientists, and 17,400 postgraduate engineers. The pressure is increasing as more than 53% of existing U.S. semiconductor workers were expected to leave the industry in 2024, compared with an attrition rate of 40% in 2021.

Globally, Deloitte estimates that the semiconductor industry will need more than 1 million additional skilled workers by 2030. The shortage is especially serious in new manufacturing locations such as Arizona, Ohio, and emerging European fab sites, where local education and training systems have limited experience in cleanroom operations and semiconductor engineering.

This talent gap is extending the ramp-up period for new U.S. and European fabs by an estimated 12–18 months compared with projects in established East Asian manufacturing hubs. These delays could slow revenue generation from more than USD 1 trillion in committed global capital expenditure through 2030. New Western fabs may also face operating margins that are 20–30% lower than facilities in Taiwan and South Korea due to higher labour and training costs.

Opportunities

| Opportunity | (~) % CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Advanced Packaging & Chiplet Monetization | +2.4% | Taiwan, South Korea, USA, Japan | Short term (≤ 2 years) |

| Edge AI Silicon for Automotive & Industrial | +1.7% | Global — strongest in Europe, Japan, China | Medium term (2–4 years) |

| Custom Silicon & ASIC Design-as-a-Service | +1.3% | USA, India, UK — fabless design ecosystems | Medium term (2–4 years) |

| Semiconductor Supply Chain Regionalization Plays | +1.1% | USA, India, EU, Japan, Southeast Asia | Long term (≥ 4 years) |

| Quantum & Neuromorphic Chip Commercialization | +0.8% | USA, EU, Canada, Japan | Long term (≥ 4 years) |

| Semiconductor-as-a-Service & IP Licensing Platforms | +0.6% | Global — led by USA & UK | Medium term (2–4 years) |

Advanced Packaging & Chiplet Monetization

Advanced packaging, including 2.5D interposer integration, 3D hybrid bonding, and heterogeneous chiplet architectures, represents one of the strongest growth opportunities above the baseline semiconductor forecast. Many mid-tier foundries and OSATs still depend on monolithic die economics, leaving significant room for new revenue from advanced packaging services.

As traditional transistor scaling approaches its physical limits below 2 nm, performance improvements are increasingly shifting toward chiplets and packaging innovation. The global 2.5D/3D IC packaging segment was valued at around USD 67.9 billion in 2025 and is projected to reach approximately USD 154.9 billion by 2033, expanding at a 10.8% CAGR. TSMC’s CoWoS and SoIC capacity is expected to remain heavily oversubscribed through at least 2027, creating a pricing advantage for new capacity.

Chiplet-based designs can reduce silicon area per function by an estimated 30–50% compared with monolithic chips while allowing integration of IP from multiple suppliers. This shifts value from wafer fabrication, which historically delivers 50–60% gross margins for leading-edge logic, toward assembly, testing, and IP licensing. Advanced system-level packaging can also generate margin premiums of around 15–25 percentage points over standard packaging services.

Key Players Analysis

Tier-1 semiconductor leaders are defined by large production scale, high capital spending, and control over key technologies such as AI processors and advanced foundry capacity. NVIDIA, TSMC, Samsung Electronics, and Intel lead this group. NVIDIA generated more than USD 115 billion in data centre revenue in fiscal 2025, with total revenue exceeding USD 120 billion and growth of over 70%.

TSMC recorded around USD 75–80 billion in revenue in 2024 and captured nearly 70% of pure-play foundry revenue by 2025. Its quarterly sales reached about USD 30 billion, while 5 nm and below technologies contributed almost half of wafer revenue. TSMC also planned USD 52–56 billion in capital expenditure for 2026.

Samsung generated more than USD 70 billion in semiconductor revenue in 2025, while Intel reported around USD 54 billion and invested over USD 25 billion annually. Together, these companies control an estimated 40–45% of global semiconductor revenue.

Tier-2 companies compete through specialized products. Broadcom generated around USD 35–40 billion and spent over USD 5 billion on R&D. Texas Instruments recorded more than USD 18 billion, with 75% from analog and 20% from embedded processing, while annual capital spending reached USD 3.5–4.0 billion.

AMD produced about USD 25–30 billion, Qualcomm exceeded USD 35 billion, and SK hynix and Micron each generated around USD 20–30 billion. Applied Materials reported USD 26–27 billion, while Arm exceeded USD 3 billion and supported more than 30 billion chips annually. Collectively, Tier-2 companies account for about 25–30% of global semiconductor revenue.

Top Key Players in the Market

- NVIDIA Corporation

- Samsung Electronics

- Intel Corporation

- TSMC

- Qualcomm

- AMD

- Broadcom Inc.

- Texas Instruments

- SK Hynix

- Micron Technology

- Applied Materials

- Arm Holdings

Recent Developments

- In February 2026, NVIDIA reported fiscal 2026 revenue of USD 215.9 billion, representing a 65% year-over-year increase. Its Data Center business generated USD 193.7 billion, rising 68%, supported by strong demand for Blackwell GPUs, AI networking products, and accelerated computing systems. The results strengthened NVIDIA’s position as a leading semiconductor supplier for global AI infrastructure.

- In January 2026, TSMC announced planned capital expenditure of approximately USD 52–56 billion for 2026. Nearly 70–80% of this investment was allocated to advanced manufacturing technologies, including 3 nm and 2 nm production capacity. A further 10–20% was directed toward advanced packaging, testing, and related facilities to meet growing demand for high-performance AI and computing chips.

- In February 2026, the Semiconductor Industry Association reported that global semiconductor sales reached USD 791.7 billion in 2025, increasing 25.6% from USD 630.5 billion in 2024. Fourth-quarter sales totaled USD 236.6 billion, supported by rising demand for logic, memory, and AI-related devices. The strong performance indicated that the global semiconductor industry was moving closer to the USD 1 trillion revenue level.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 662.6 Billion |

| Forecast Revenue (2035) | USD 1593.9 Billion |

| CAGR (2026-2035) | 9.18% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Logic Chips, including AI / ML Processors, CPUs, FPGAs, and ASICs; Memory Chips, including DRAM and NAND Flash; Analog Semiconductors, including Power Management ICs and RF Chips; Discrete Semiconductors; and Sensors and MEMs), By Node Size (Mature Nodes (>28nm), Advanced Nodes (7–28nm), and Cutting-Edge Nodes (<7nm), including 3nm Node, 5nm Node, and 7nm Node), By Application (Consumer Electronics, including Smartphones and PCs / Laptops; Data Centers and AI, including AI Accelerators and Cloud Server Chips; Automotive, including ADAS Chips and EV Power Chips; Industrial; Communications; and Others), By End User (Consumer Electronics OEMs, Cloud and Data Center Companies, Automotive OEMs, Industrial Companies, Telecom Companies, Defense and Aerospace, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | NVIDIA Corporation, Samsung Electronics, Intel Corporation, TSMC, Qualcomm, AMD, Broadcom Inc., Texas Instruments, SK Hynix, Micron Technology, Applied Materials, Arm Holdings, and Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |