Quick Navigation

Report Overview

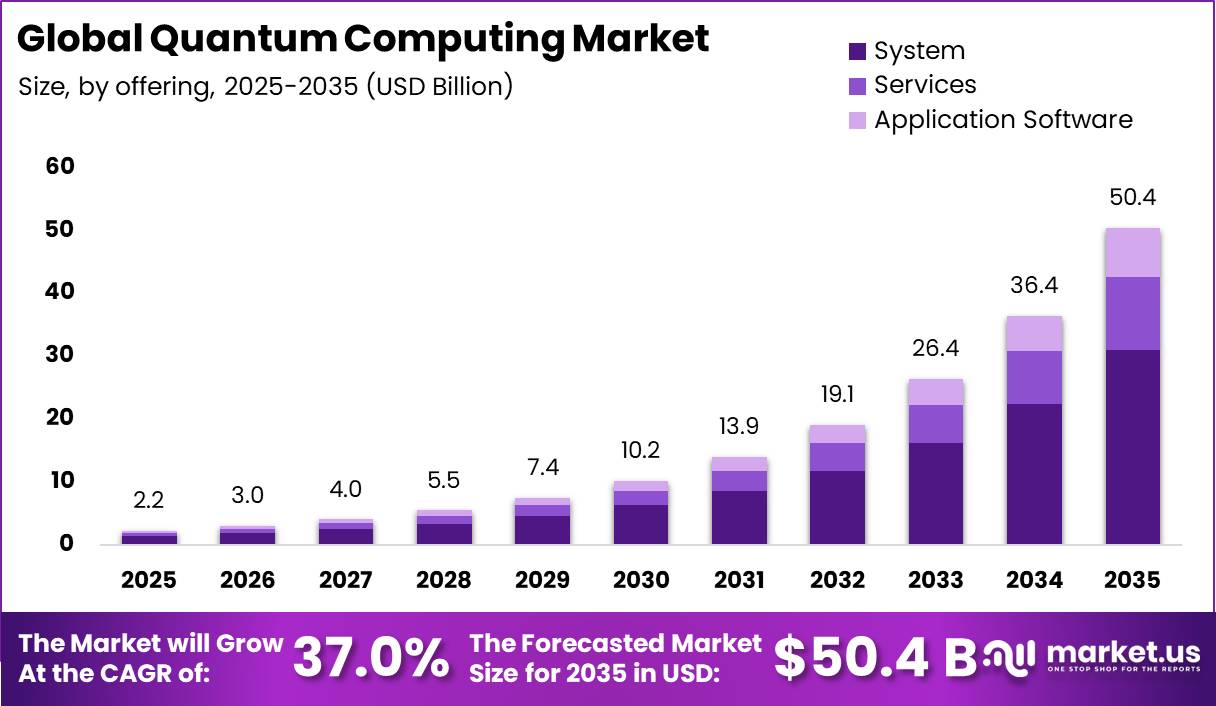

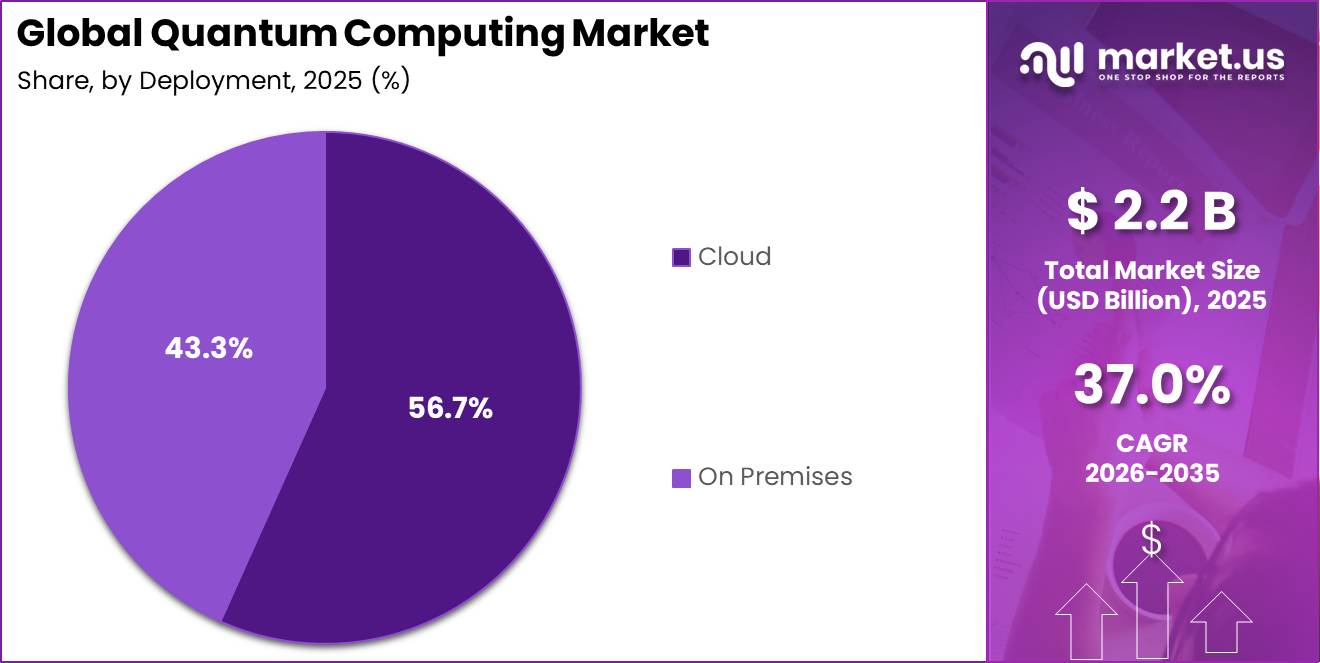

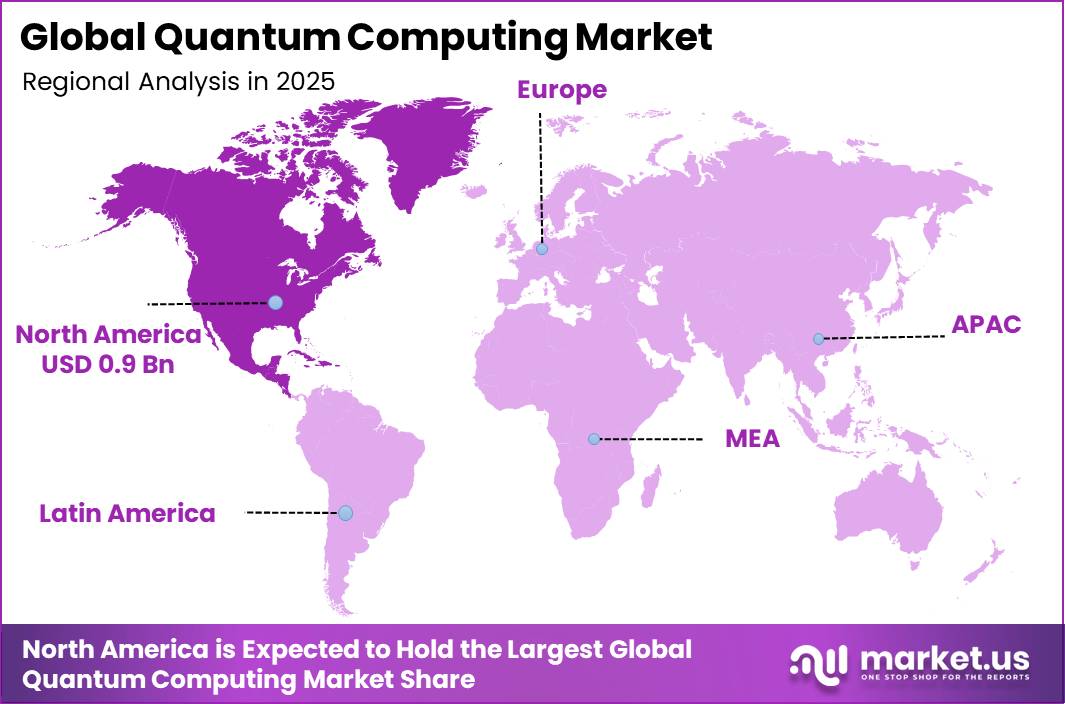

In 2025, the Quantum Computing Market was valued at USD 2.2 billion and is projected to expand at a CAGR of 37.0% from 2026 to 2035, reaching approximately USD 50.4 billion by 2035. North America held the dominant position in the global market in 2025, accounting for more than 38.4% of the total market share and generating around USD 0.9 billion in revenue.

Global R&D expenditure reached approximately USD 3.8 trillion in 2024, with OECD economies contributing nearly two-thirds of global R&D spending, creating a strong funding foundation for emerging technologies such as quantum computing. In addition, the U.S. CHIPS and Science Act has allocated around USD 280 billion toward strengthening semiconductor innovation, high-performance computing, and related deep-tech research, including quantum technologies.

Globally, the quantum technology industry reached approximately USD 1.9 billion in 2025, with quantum computing representing the largest revenue contributor. Furthermore, the global ICT market, valued at over USD 5–6 trillion, continues to expand as enterprises increase spending on cloud computing, AI, cyber security, and high-performance computing. These broader technology investments are creating a strong pathway for quantum adoption, supporting the market’s projected growth toward USD 50.4 billion by 2035.

Key Takeaway

- The Global Quantum Computing Market was valued at USD 2.2 billion in 2025 and is projected to reach approximately USD 50.4 billion by 2035, expanding at a CAGR of 37.0% during the forecast period from 2026 to 2035.

- By Offering, System dominated the global Quantum Computing Market in 2025, accounting for 61.6% of the market share.

- By Deployment, Cloud emerged as the leading segment in 2025, holding a 56.7% market share.

- By Application, Optimization accounted for the dominant market share of 32.7% in 2025.

- By Technology, Superconducting Qubits held the largest market share of 38.9% in 2025.

- By End User Industry, Financial Services and Insurance (BFSI) dominated the market with a 16.8% share in 2025.

- North America dominated the global Quantum Computing Market in 2025, accounting for more than 38.4% of the total market share and generating approximately USD 0.9 billion in revenue.

By Offering

The System offering segment holds the largest share of the quantum computing market, accounting for 61.6% of total revenue, as most quantum computing applications depend on access to advanced hardware infrastructure. This includes quantum processors, cryogenic systems, control electronics, and supporting data-center integration. Government initiatives are also prioritizing investments in quantum hardware development.

For example, India’s National Quantum Mission has allocated INR 6,003.65 crore (approximately USD 720–750 million) through 2030–31 to develop quantum computing capabilities, including 50–1000 qubit-scale systems and research testbeds. Since hardware performance, including qubit capacity, accuracy, and operational stability, directly impacts the success of quantum applications such as optimization, simulation, and cybersecurity, organizations continue to prioritize system-level investments.

By Deployment

The Cloud deployment segment dominates the quantum computing market, accounting for an estimated 56.7% of total revenue, as cloud platforms provide the most practical and cost-effective way for organizations to access advanced quantum computing resources. Quantum hardware requires significant investment, specialized infrastructure, and technical expertise, making on-premises deployment challenging for most enterprises.

Cloud-based quantum platforms enable global access to powerful quantum processors, allowing businesses and researchers to run experiments and develop algorithms without owning dedicated systems. Leading quantum providers have expanded cloud accessibility, with IBM’s cloud-based IBM Quantum Platform reporting more than 400,000 registered users, highlighting the growing preference for remote quantum access.

By Application

The Optimization application segment holds the largest share of the quantum computing market, accounting for 32.7% of total revenue, due to its strong applicability across industries that require complex decision-making and resource management. Sectors such as logistics, transportation, energy, and finance increasingly depend on optimization solutions for route planning and supply chain management.

Global trade reached USD 33 trillion in 2024, increasing the need for efficient logistics networks and advanced optimization capabilities. Additionally, global energy investment is projected to reach USD 3.3 trillion in 2025, with rising complexity in renewable energy integration, grid balancing, and energy distribution creating demand for advanced computational methods.

The Machine Learning application segment is expected to experience the fastest growth in the quantum computing market, supported by increasing artificial intelligence adoption and the need for more powerful computing solutions. Enterprise AI adoption increased from 8.7% in 2023 to 20.2% in 2025, driving demand for advanced capabilities in data processing, model training, and pattern recognition.

By Technology

The Superconducting Qubits technology segment dominates the quantum computing market, accounting for approximately 38.9% of total revenue, supported by its strong commercial maturity and extensive deployment across quantum computing platforms. This technology remains the leading approach for commercially available quantum systems, with major providers operating superconducting quantum processors exceeding 100 qubits and offering access to thousands of aggregate qubits through cloud-based platforms.

The Topological technology segment is expected to witness the fastest growth in the quantum computing market, expanding from a limited installed base at a high double-digit CAGR, typically ranging between 40–50%+, as research advances toward pilot-scale systems. The growth of this segment is driven by the potential of topological qubits to provide greater stability and improved resistance to environmental noise compared with existing approaches.

By End User Industry

The Banking, Financial Services and Insurance (BFSI) segment dominates the quantum computing market by end-use industry, accounting for 16.8% of total revenue, due to the sector’s high dependence on complex data analysis, risk management, and optimization processes. Financial institutions handle large-scale computational challenges, including portfolio optimization, derivative pricing, fraud detection, and risk assessment, where quantum computing can provide potential performance improvements.

The global financial ecosystem continues to expand in complexity, with BIS data reporting global OTC derivatives notional amounts reaching USD 846 trillion by June 2025, creating significant demand for advanced computational capabilities.

Key Market Segments

By Offering

- System

- Services

- Application Software

By Deployment

- Cloud

- On Premises

By Application

- Machine Learning

- Optimization

- Simulation

- Others

By Technology

- Photonic Networks

- Quantum Annealing

- Superconducting Qubits

- Trapped Ions

- Topological

- Others

By End User Industry

- Academic

- Banking

- Chemicals

- Energy and Power

- Financial Services and Insurance (BFSI)

- Government

- Healthcare and pharmaceuticals

- Logistics and Transportation

- Space and Defense

- Others

Market Dynamics

Challenge

The quantum computing industry faces a persistent talent shortage, with global demand for quantum professionals exceeding supply by an estimated 40–50%. Around 35,000–40,000 roles require expertise in quantum computing, low-temperature physics, or quantum error correction, while only 18,000–22,000 qualified specialists are currently available worldwide.

This shortage raises senior quantum engineering compensation to 1.4–1.7× that of comparable AI or cloud engineers and extends hiring timelines to 7–10 months in the US and Europe and 10–14 months in emerging APAC markets. As a result, organizations often operate with 10–20% staffing gaps, slowing product development and reducing the pace of quantum hardware and software advancement.

Limited access to skilled talent also delays roadmap execution, extends commercialization timelines, and restricts enterprise adoption, contributing an estimated 1.5–2.0 percentage point drag on market CAGR. To address this, vendors are investing in internal training programs, retraining HPC and AI engineers, and expanding partnerships with universities, although meaningful workforce expansion is expected to take 4–7 years.

| Challenge | (~) % CAGR | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Deep tech talent deficit | -1.8% | North America, EU, East Asia hubs | Long term (≥ 4 years) |

| Fragile quantum supply chain | -1.5% | North America, EU, Japan, South Korea | Long term (≥ 4 years) |

| Algorithm-to-ROI translation gap | -1.3% | Global Tier-1 enterprises | Medium term (2-4 years) |

| Cloud access and TCO opacity | -0.9% | Global, esp. emerging APAC & LATAM | Medium term (2-4 years) |

| Standards, benchmarks, and trust | -0.8% | US, EU regulatory hubs, global FSIs | Medium term (2-4 years) |

| Funding cyclicality and project churn | -1.0% | US, UK, EU, Israel start-up clusters | Short term (≤ 2 years) |

Opportunity

Quantum-enabled drug discovery platforms represent a major growth opportunity because current quantum computing forecasts assign only a limited share of future revenue to life sciences, despite the significant potential for quantum-enhanced molecular modeling, drug design, and healthcare optimization.

With global biopharmaceutical R&D spending expected to exceed USD 300–350 billion annually by the early 2030s, capturing just 1–2% of this expenditure through quantum-enabled platforms could create an additional USD 3–7 billion annual revenue opportunity.

If quantum-enabled simulation reduces late-stage clinical trial failures by 5–10% and shortens early-stage drug screening by 15–25%, providers could achieve 65–80% gross margins through software and licensing models. Because current quantum hardware is still insufficient for large-scale commercial molecular simulation, these revenues are not included in most baseline market forecasts.

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Verticalized quantum SaaS stacks | +2.0% | North America, Western Europe, Japan | Medium term (2–4 years) |

| Quantum-secure infrastructure & compliance services | +1.8% | North America, EU, APAC developed | Short–medium term (≤ 4 years) |

| Industrial quantum co-creation hubs | +1.5% | EU, North America, East Asia | Medium term (2–4 years) |

| Quantum-enabled drug discovery platforms | +2.3% | North America, EU, APAC biotech clusters | Medium–long term (3–6+ years) |

| National and regional quantum sovereign stacks | +1.7% | US, EU, China, India, Middle East | Long term (≥ 4 years) |

| Quantum–AI hybrid optimization engines | +2.1% | Global digital-native enterprises | Medium–long term (3–6+ years) |

Driver

Migration toward quantum-safe security is emerging as a key demand driver because organizations are beginning to prepare for future cryptographic threats posed by quantum computing. Readiness remains at an early stage, creating significant demand for cryptographic discovery, risk assessment, key management, and post-quantum migration services.

In 2025, the average quantum-safe readiness score improved to 25 out of 100, up from 21 in 2023, indicating growing awareness but limited operational implementation. This gap is especially important for industries managing long-lived sensitive data, including finance, healthcare, defense, and critical infrastructure.

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public R&D & National Quantum Programs | +3.0% | North America core, EU, APAC corridors | Medium term (2–4 years) |

| Large-scale VC & Strategic Corporate Investment | +2.2% | North America core, APAC corridors | Short–Medium (≤2 to 4 years) |

| QPU Performance Improvements (Qubit counts & error correction) | +4.0% | North America core, EU, APAC corridors | Short–Medium (≤2 to 4 years) |

| Diversification of QPU Platforms (photonic, trapped-ion, neutral-atom) | +1.5% | APAC corridors, EU spill-over, North America | Medium–Long (2–≥4 years) |

| Commercialization of Cloud-access & SaaS quantum offerings | +2.0% | North America core, EU, APAC corridors | Short term (≤2 years) |

| Quantum-safe cryptography & regulatory/compliance drivers | +1.3% | EU core, North America, APAC (financial hubs) | Medium–Long (2–≥4 years) |

Restraint

Critical semiconductor and cryo-electronics shortages remain a significant restraint on quantum hardware development because production depends on specialized components such as control ASICs, cryo-CMOS chips, cryogenic wiring, connectors, and advanced packaging technologies that face increasing competition from AI-driven semiconductor demand.

In 2026, fulfillment rates for quantum-grade control chips are estimated at only 60–75% of demand, resulting in procurement and shipping delays of 3–9 months. At the same time, shortages in advanced packaging and specialized components increase bill-of-material (BOM) costs by approximately 15–30%, raising manufacturing expenses for quantum hardware vendors.

These supply constraints delay product launches, slow production scaling, and postpone customer deployments, creating an estimated ~2.5 percentage point drag on quantum computing market CAGR during 2026–2028 until specialized semiconductor and packaging capacity expands.

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export controls & dual-use regulation | -3.0% | North America core, EU, Switzerland | Medium term (2-4 years) |

| Critical semiconductor / cryo-electronics shortages | -2.5% | Global (APAC supply nodes, North America demand) | Short–Medium (≤2 to 4 years) |

| High capex & slow commercialization cadence | -2.0% | Global (research hubs: US, EU, China) | Medium term (2-4 years) |

| Skilled talent bottleneck | -1.2% | North America core, EU, APAC research corridors | Medium–Long (2–≥4 years) |

| Supply chain concentrated single-points (cryostats, lasers) | -1.0% | APAC corridors, North America | Short term (≤2 years) |

| Investor risk aversion & funding cyclicity | -1.3% | Global (venture hubs: US, EU, China, Israel) | Short–Medium (≤2 to 4 years) |

Geopolitical Impact Analysis

Geopolitical tensions are increasing supply chain costs and influencing the global structure of the quantum computing industry, which relies on advanced semiconductors, cryogenic systems, photonics, and specialized materials. U.S. tariffs on Chinese exports have increased to 47.5%, while China’s average tariff on U.S. exports stands at 31.9%, raising costs for quantum-related components such as chips, precision electronics, and control systems.

The U.S. has also planned a phased increase in tariffs on Chinese semiconductors from 25% to 50% by 2025, adding further pressure on quantum hardware manufacturing costs. Shanghai–Europe shipping rates increased by 256%, while Shanghai–U.S. West Coast rates rose by 162%, extending delivery timelines and increasing inventory requirements for quantum equipment providers.

More than 80% of global trade by volume moves through vulnerable maritime routes, increasing risks for the supply of helium, high-purity materials, and photonics components. Industry surveys indicate that nearly 60% of commercial quantum companies expect a materials- or equipment-related supply disruption within three years, making supply chain localization, dual sourcing, and regional manufacturing strategies increasingly important for the quantum computing market.

Regional Analysis

North America accounts for an estimated 38.4% of the global quantum computing market, underpinned by a market value of around USD 0.9 billion, reflecting the region’s early-mover advantage and dense ecosystem of hardware manufacturers, software platforms, cloud hyperscalers, and specialized start-ups.

This leadership is reinforced by strong federal and state-level funding for quantum research, mature venture capital networks, and deep integration of quantum pilot projects across banking, defense, automotive, and advanced manufacturing use cases.

Asia Pacific, by contrast, is recognized as the fastest-growing region in the quantum computing market, driven by aggressive national strategies in China, Japan, South Korea, India, and Australia. Governments across the region are deploying substantial capital into quantum communication networks, sovereign quantum infrastructure, and talent development.

Key Players Analysis

The quantum computing market is highly concentrated among a small group of Tier-1 technology companies, including IBM, Google (Alphabet), Microsoft, and IonQ, which are leading advancements in quantum hardware, software platforms, and commercial applications.

IBM has established a strong market position, reporting more than USD 1 billion in cumulative quantum technology revenue by early 2025 and allocating USD 8.3 billion toward R&D in 2025, including investments in advanced technologies such as quantum computing.

Among pure-play quantum companies, IonQ has emerged as a leading commercial player, reporting USD 130.0 million in GAAP revenue in 2025, representing 202% year-on-year growth. The company became the first publicly traded quantum computing firm to exceed USD 100 million in annual GAAP revenue and ended 2025 with USD 3.3 billion in cash and investments. IonQ also projected USD 225–245 million in revenue for 2026, indicating continued strong expansion in quantum hardware and related services.

Top Key Players in the Market

- Accenture Plc.

- D-Wave Systems Inc.

- Google LLC

- IBM Corporation

- Intel Corporation

- IonQ

- Microsoft Corporation

- QC Ware

- Quantinuum Ltd.

- Rigetti & Co, Inc.

- Riverlane

- Zapata Computing

Recent Developments

- In July 2025, IonQ completed its acquisition of Capella Space, expanding its quantum networking push into a space-based QKD network by integrating Capella’s satellite infrastructure with IonQ’s quantum networking capabilities.

- In January 2026, IonQ announced a definitive agreement to acquire Seed Innovations, a software and technology R&D specialist, in a transaction expected to close on January 30, 2026, strengthening its software and cloud-architecture capabilities.

- In May 2026, Rigetti signed a letter of intent with the U.S. Department of Commerce for up to $100 million in funding over three years to accelerate superconducting quantum computing R&D.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.2 Billion |

| Forecast Revenue (2035) | USD 50.4 Billion |

| CAGR (2026-2035) | 37.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Offering (System, Services, Application Software), By Deployment (Cloud, On-Premises), By Application (Machine Learning, Optimization, Simulation, Others), By Technology (Photonic Networks, Quantum Annealing, Superconducting Qubits, Trapped Ions, Topological, Others), By End-user Industry (Academic, Banking, Chemicals, Energy and Power, Financial Services and Insurance (BFSI), Government, Healthcare and Pharmaceuticals, Logistics and Transportation, Space and Defense, Others), |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Accenture Plc., D-Wave Systems Inc., Google LLC, IBM Corporation, Intel Corporation, IonQ, Microsoft Corporation, QC Ware, Quantinuum Ltd., Rigetti & Co, Inc., Riverlane, Zapata Computing |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |