Quick Navigation

Report Overview

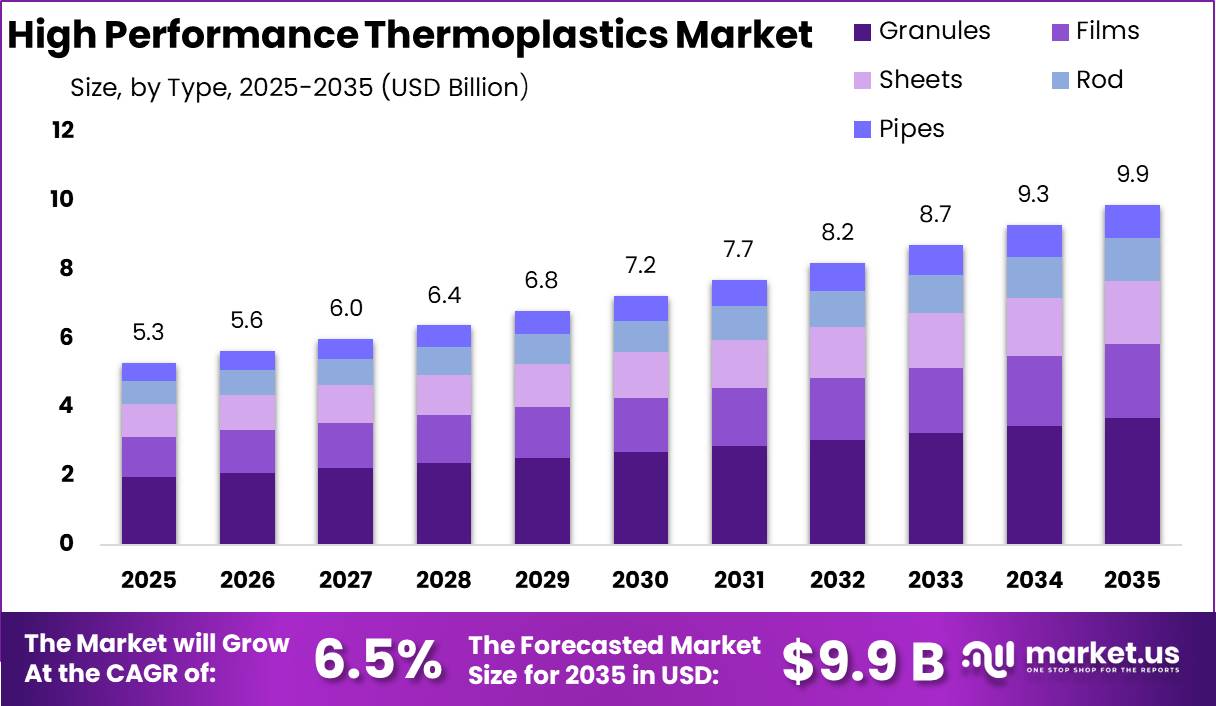

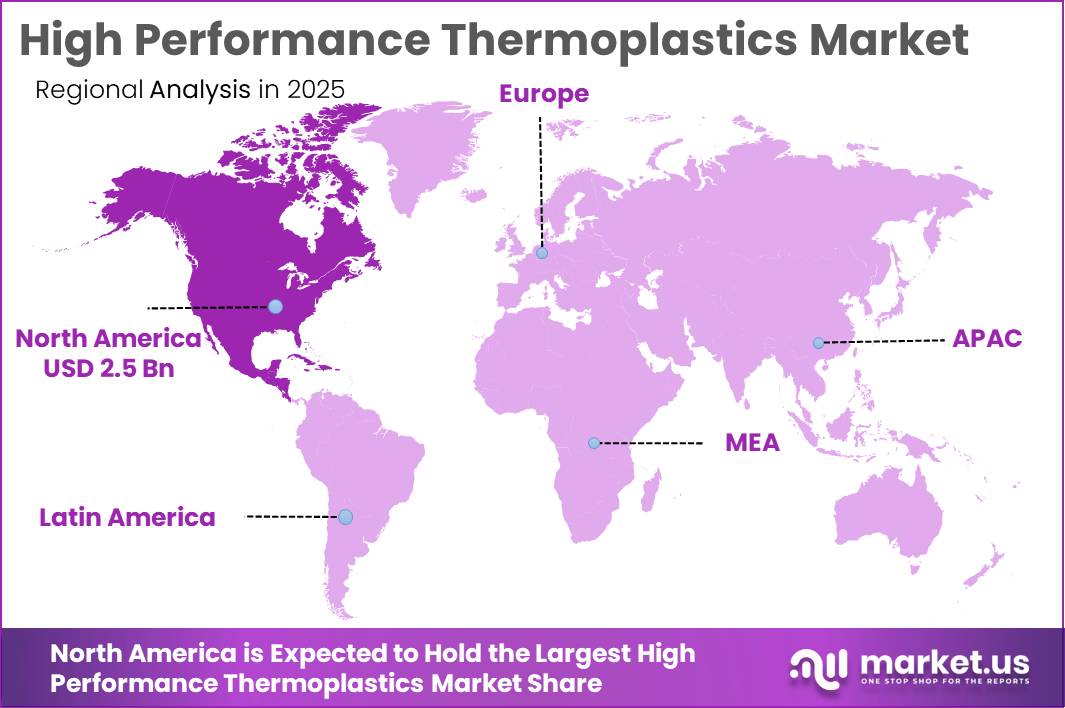

The Global High Performance Thermoplastics Market size is expected to be worth around USD 8.7 Billion by 2035, from USD 5.3 Billion in 2025, growing at a CAGR of 6.3% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 48.40% share, holding USD 2.5 Billion revenue.

High-performance thermoplastics are positioned as advanced engineering materials used where conventional plastics cannot meet heat, chemical, weight, flame, wear, and dimensional-stability requirements. Industrial demand is being shaped by aerospace, electric mobility, electronics, healthcare, energy, and industrial equipment, as these sectors require polymers such as PEEK, PPS, PEI, PVDF, PSU/PPSU, and high-performance polyamides to replace metals, improve part life, and support miniaturization.

- The wider plastics base remains large, with OECD reporting global plastics production and use at 435 million tonnes in 2020, up from 234 million tonnes in 2000, while Europe’s plastics sector generated €398 billion turnover in 2024, despite a 13% decline from 2022.

The industrial scenario is increasingly application-led rather than volume-led. In aerospace, Airbus forecasts demand for 43,420 new passenger and freighter aircraft during 2025–2044, supporting use of lightweight thermoplastic composites, clips, brackets, interiors, insulation, and high-temperature structural parts. In automotive, the U.S. Department of Energy states that a 10% vehicle-weight reduction can improve fuel economy by 6%–8%, strengthening the case for high-performance polymers in under-hood, battery, e-motor, connector, and thermal-management applications.

Driving factors include electrification, fuel efficiency, chemical resistance, metal replacement, regulatory pressure, and circular-design requirements. The International Energy Agency reported global electric car sales above 17 million in 2024, representing more than 20% of new car sales, creating demand for PVDF binders, PEEK insulation films, flame-retardant polyamides, and high-temperature connectors.

Government and institutional initiatives are also supporting growth. The European Commission’s 2024 Advanced Materials for Industrial Leadership strategy aims to accelerate safe, sustainable, and circular advanced materials, while its implementation plan lists 14 actions for coordinated industrial uptake. IEA stated that global installed water-electrolysis capacity reached 2 GW in 2024, with more than 1 GW added through July 2025, supporting demand for chemically resistant polymers in electrolyzer stacks. IATA also expected passenger traffic growth of 5.8% year-on-year in 2025, supporting lightweight aerospace material demand.

BASF strengthened its high-performance thermoplastics position in 2025 through product and partnership-led developments. In March 2025, BASF launched Ultrason E 2010 BMB, described as the world’s first biomass-balanced PESU, using ISCC PLUS mass balance and 100% green electricity at Ludwigshafen. In September 2025, Stargate Hydrogen began using BASF Ultrason S in alkaline water-electrolyzer stack frames, replacing nickel-based metals with lighter, chemically resistant thermoplastic components.

Key Takeaways

- High Performance Thermoplastics Market size is expected to be worth around USD 8.7 Billion by 2035, from USD 5.3 Billion in 2025, growing at a CAGR of 6.3%.

- Polyether held a dominant market position, capturing more than a 36.90% share in the High Performance Thermoplastics market.

- Granules held a dominant market position, capturing more than a 37.20% share in the High Performance Thermoplastics market.

- Injection Molding held a dominant market position, capturing more than a 41.70% share in the High Performance Thermoplastics market.

- Electronics held a dominant market position, capturing more than a 41.80% share in the High Performance Thermoplastics market.

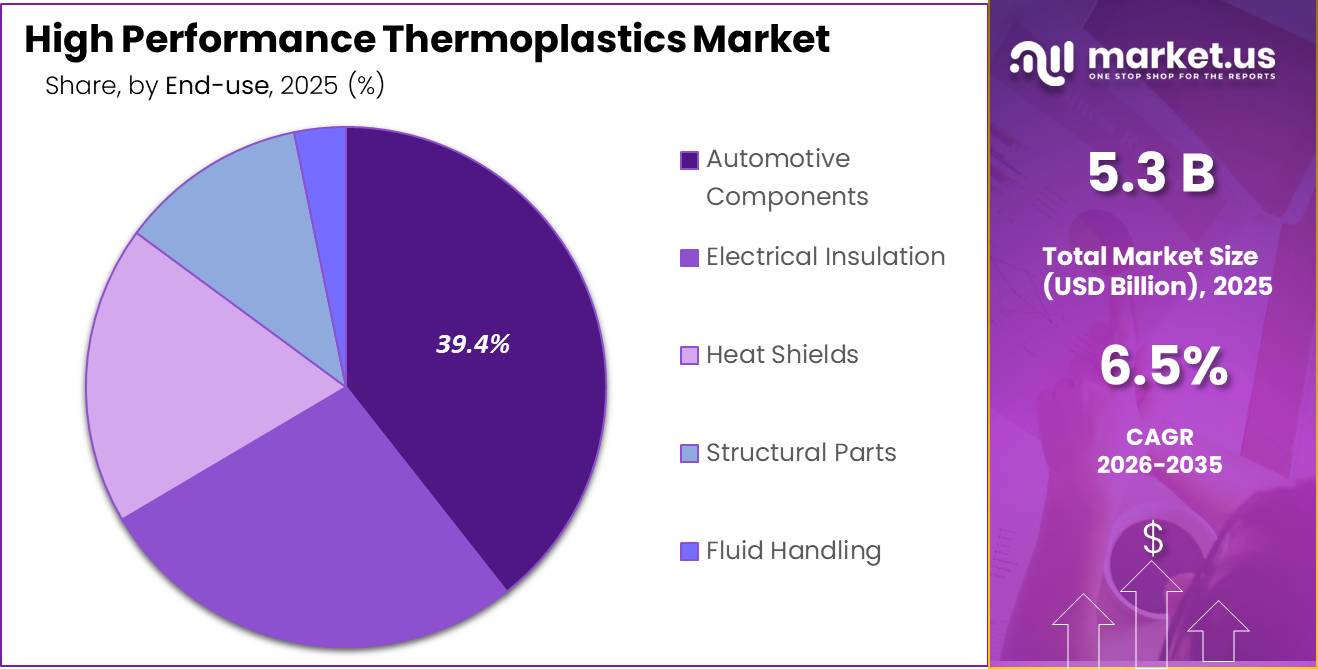

- Automotive Components held a dominant market position, capturing more than a 39.40% share in the High Performance Thermoplastics market.

- North America held a dominant position in the High Performance Thermoplastics market, accounting for 48.40% of the global market and reaching a value of USD 2.5 Billion.

By Type Analysis

Polyether dominates with 36.90% share due to its strong thermal stability and performance in demanding industrial applications

In 2025, Polyether held a dominant market position, capturing more than a 36.90% share in the High Performance Thermoplastics market by type. This leadership was supported by its ability to maintain mechanical strength, chemical resistance, and dimensional stability under high-temperature conditions. Industries that require reliable material performance in demanding environments continued to prefer polyether-based thermoplastics because they offer long service life while reducing maintenance and replacement cycles.

By Form Analysis

Granules dominate with 37.20% share due to their easy processing and broad industrial usability

In 2025, Granules held a dominant market position, capturing more than a 37.20% share in the High Performance Thermoplastics market by form. The segment maintained its leading position mainly because granules are easier to handle, transport, store, and process across different manufacturing environments. Their uniform size and flow properties make them suitable for high-volume production methods, supporting consistent output and reducing material waste during processing.

By Processing Method Analysis

Injection Molding dominates with 41.70% share due to its efficiency in producing complex and high-volume components

In 2025, Injection Molding held a dominant market position, capturing more than a 41.70% share in the High Performance Thermoplastics market by processing method. The segment’s strong position was supported by its ability to manufacture complex shapes with high precision while maintaining consistent product quality. Injection molding remained the preferred processing method because it enables faster production cycles and efficient use of high-performance thermoplastic materials across large manufacturing operations.

By Application Analysis

Electronics dominates with 41.80% share driven by rising demand for durable and heat-resistant components

In 2025, Electronics held a dominant market position, capturing more than a 41.80% share in the High Performance Thermoplastics market by application. The segment maintained its leadership due to the growing need for materials that offer high heat resistance, electrical insulation, dimensional stability, and long-term reliability. High performance thermoplastics continued to gain preference in electronic applications because they support the production of compact, lightweight, and durable components used in modern devices and systems.

By End Use Analysis

Automotive Components dominate with 39.40% share supported by growing demand for lightweight and durable vehicle materials

In 2025, Automotive Components held a dominant market position, capturing more than a 39.40% share in the High Performance Thermoplastics market by end-use industry. The segment remained in the leading position as vehicle manufacturers continued to focus on reducing component weight while maintaining strength, durability, and thermal performance. High performance thermoplastics became an important material choice because they support improved efficiency and help meet evolving design and performance requirements across modern vehicle production.

Key Market Segments

By Type

- Polyether

- Polyphenylene Sulfide (PPS)

- Polyetherimide (PEI)

- Polyphthalamide (PPA)

- Liquid Crystal Polymer (LCP)

- Others

By Form

- Films

- Sheets

- Rod

- Pipes

- Granules

By Processing Method

- Injection Molding

- Extrusion

- Compression Molding

- 3D Printing

- Blow Molding

By Application

- Aerospace

- Automotive

- Electronics

- Industrial

- Medical

By End Use

- Automotive Components

- Electrical Insulation

- Heat Shields

- Structural Parts

- Fluid Handling

Emerging Trends

Lightweight Electrification and Material Replacement are Emerging as the Latest Trend in High Performance Thermoplastics

One of the latest trends shaping the High Performance Thermoplastics market is the increasing replacement of traditional metal components with lightweight, heat-resistant thermoplastic materials across electric mobility and advanced electronics. Industries are moving toward designs that improve energy efficiency while reducing product weight, and this shift is creating stronger demand for materials that deliver performance without adding mass.

High performance thermoplastics are increasingly being selected for battery systems, electrical housings, connectors, insulation components, and compact structural parts. These materials help manufacturers improve thermal management and support product miniaturization.

- According to the International Energy Agency (IEA), global electric car sales crossed 17 million units in 2024, increasing by more than 25% compared with the previous year. The growth momentum remained strong, with electric vehicle adoption continuing to accelerate across major markets.

Advanced Battery and Thermal Management Applications are Expanding Thermoplastic Use

Another noticeable trend is the growing use of high performance thermoplastics in battery-related applications and thermal control systems. As electrified products become more advanced, manufacturers are focusing on materials that improve safety, reduce component weight, and maintain stable performance under higher operating temperatures.

Drivers

Growing Shift Toward Lightweight and Energy-Efficient Materials is Driving High Performance Thermoplastics Demand

One of the strongest factors supporting the growth of the High Performance Thermoplastics market is the rising focus on lightweight and energy-efficient products, especially across transportation and advanced manufacturing industries. Manufacturers are increasingly replacing traditional metal components with high performance thermoplastics because these materials provide strength, heat resistance, and lower overall component weight.

The agency further indicates that more than 20 million electric cars are expected to be sold in 2025, meaning approximately one out of every four new vehicles globally could be electric. This continued increase in electric mobility creates stronger demand for advanced materials capable of supporting lightweight vehicle design and thermal management requirements.

Government Support and Industrial Modernization are Expanding Advanced Material Adoption

Government-led industrial programs and cleaner manufacturing policies are also creating favorable conditions for the High Performance Thermoplastics market. Many countries are promoting energy-efficient technologies, domestic manufacturing expansion, and reduced environmental impact, which is increasing the use of advanced polymer materials across industrial supply chains.

India provides a clear example of this shift. According to a government-backed report published through national policy institutions, electric vehicle sales in India increased from 50,000 units in 2016 to 2.08 million units in 2024. The report also states that India aims to achieve 30% electric vehicle penetration by 2030, showing continued policy focus on cleaner transportation and industrial transformation.

Restraints

High Material and Processing Costs Continue to Limit Wider Adoption of High Performance Thermoplastics

One of the major factors restricting the growth of the High Performance Thermoplastics market is the high overall cost associated with raw materials, manufacturing, and processing. These materials are designed to perform under extreme temperatures and demanding operating conditions, but achieving those properties requires complex production methods and specialized equipment. As a result, production costs remain significantly higher than conventional plastics and many standard engineering materials.

The challenge becomes more visible in industries that operate with tight production budgets and large output volumes. Many small and mid-sized manufacturers continue to delay adoption because switching to high performance thermoplastics often requires equipment upgrades, process changes, and additional investment in quality control systems.

- According to industrial energy studies, plastics manufacturing remains energy intensive, and the U.S. plastics sector recorded approximately 1,884 trillion Btu of total energy use, with 1,547 trillion Btu consumed in plastics materials and resin production alone. This reflects the substantial energy demand involved before finished products even reach end users.

Energy Dependence and Raw Material Volatility Create Long-Term Cost Pressure

Another important restraint is the dependence of thermoplastic production on energy and petrochemical feedstocks. High performance thermoplastics require advanced polymer processing stages, and fluctuations in energy prices can directly affect manufacturing economics. When production costs rise, manufacturers often postpone material substitution projects and continue using lower-cost alternatives.

According to trusted industry and energy assessments, the chemicals industry accounts for approximately 11% of total final global energy consumption, including 14% of oil consumption and 8% of natural gas consumption worldwide. In addition, production activities connected to chemical outputs generate around 1.5 gigatonnes of direct CO₂ emissions annually, of which 1.3 gigatonnes are energy-related emissions. These figures show how closely advanced material production remains tied to energy markets and operating costs.

Opportunity

Safer food processing equipment can drive demand

A major growth opportunity for high performance thermoplastics is food processing equipment. Food companies need materials that can handle heat, steam cleaning, oils, acids, and repeated washing without rusting or breaking.

This is where materials like PEEK, PPS, PEI, and high-grade fluoropolymers can grow. The need is clear: globally, 13.2% of food is lost between harvest and retail, and another 19% is wasted at retail, food service, and home levels, according to FAO/UNEP. Better, longer-lasting conveyor parts, seals, bearings, valves, and processing components can help reduce downtime, contamination risk, and product loss.

Government food-safety rules support better materials

Government rules also support this opportunity. The U.S. FDA says food contact substances include packaging, processing equipment, preparation surfaces, and cookware, so food-grade plastics must be safe for contact use. In the EU, all food-contact packaging materials, including plastics, must follow strict safety rules so they do not harm health or change food taste or smell.

This gives high performance thermoplastics a strong opening, because food makers want trusted, compliant, cleanable materials. In the U.S., food waste is still estimated at 30–40% of the food supply, showing how big the efficiency problem is.

Regional Insights

North America dominated the High Performance Thermoplastics market with a 48.40% share, valued at USD 2.5 Billion, supported by strong industrial and advanced manufacturing demand

In 2025, North America held a dominant position in the High Performance Thermoplastics market, accounting for 48.40% of the global market and reaching a value of USD 2.5 Billion. The region maintained its leadership due to its well-established industrial base, continuous investment in advanced materials, and strong presence across automotive, aerospace, electronics, and industrial manufacturing sectors.

Electronics manufacturing also contributed to regional growth as demand increased for compact and reliable components capable of operating under elevated temperatures. North America benefited from established supply chains, strong research capabilities, and greater integration of high-performance materials into industrial production systems.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF maintains a strong position in high-performance thermoplastics through engineering plastics and high-temperature polymer families including Ultrason®. The company generated €65.3 billion revenue in 2025 and employed around 112,000 employees globally. BASF operates production sites in more than 90 countries and serves customers across industrial sectors including automotive, electronics, energy, and infrastructure.

DuPont remains a major supplier of advanced materials and high-performance thermoplastics for transportation, electronics, medical, water, and industrial markets. The company reported approximately US$12.4 billion revenue in 2025 and operates manufacturing and innovation facilities globally. DuPont’s engineering-material portfolio supports applications requiring thermal resistance, dimensional stability, and reduced component weight.

Evonik Industries participates in the high-performance thermoplastics market through specialty polymer technologies supporting healthcare, additive manufacturing, mobility, and industrial applications. The company reported approximately €15.2 billion revenue in 2025 with operations in more than 100 countries and around 32,000 employees.

Top Key Players Outlook

- Solvay (BE)

- BASF (DE)

- DuPont (US)

- Victrex (GB)

- Evonik Industries (DE)

- PolyOne (US)

- Mitsubishi Chemical (JP)

- SABIC (SA)

- Toray Industries (JP)

- Asahi Kasei Corporation

- Honeywell International Inc.

Recent Industry Developments

In 2026, SABIC moved strongly on merger and acquisition activity by agreeing to divest its Engineering Thermoplastics business in the Americas and Europe to Mutares for about USD 450 million, while its wider asset sale package was valued at USD 950 million. The sold ETP business covered operations in the U.S., Canada, Brazil, and Spain. SABIC also reported a broad global scale, with operations across 44 countries, more than 26,000 employees, 60 production sites, and over 140 markets served, supporting its continued role in advanced thermoplastic materials.

In partnership, Mitsubishi Chemical joined Asahi Kasei and Mitsui Chemicals to form Setouchi Ethylene LLP on August 19, 2025, with ¥1.5 million paid-in capital and a 1:1:1 capital ratio. In investment and expansion, Mitsubishi Chemical added new flame-retardant compound lines in China from April 2025 and France from January 2026 to support cable, mobility, telecom, construction, and gas applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 5.3 Bn |

| Forecast Revenue (2035) | USD 8.7 Bn |

| CAGR (2026-2035) | 6.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Polyether, Polyphenylene Sulfide (PPS), Polyetherimide (PEI), Polyphthalamide (PPA), Liquid Crystal Polymer (LCP), Others), By Form (Films, Sheets, Rod, Pipes, Granules), By Processing Method (Injection Molding, Extrusion, Compression Molding, 3D Printing, Blow Molding), By Application ( Aerospace, Automotive, Electronics, Industrial, Medical), By End Use (Automotive Components, Electrical Insulation, Heat Shields, Structural Parts, Fluid Handling) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Solvay (BE), BASF (DE), DuPont (US), Victrex (GB), Evonik Industries (DE), PolyOne (US), Mitsubishi Chemical (JP), SABIC (SA), Toray Industries (JP), Asahi Kasei Corporation, Honeywell International Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |