Quick Navigation

Report Overview

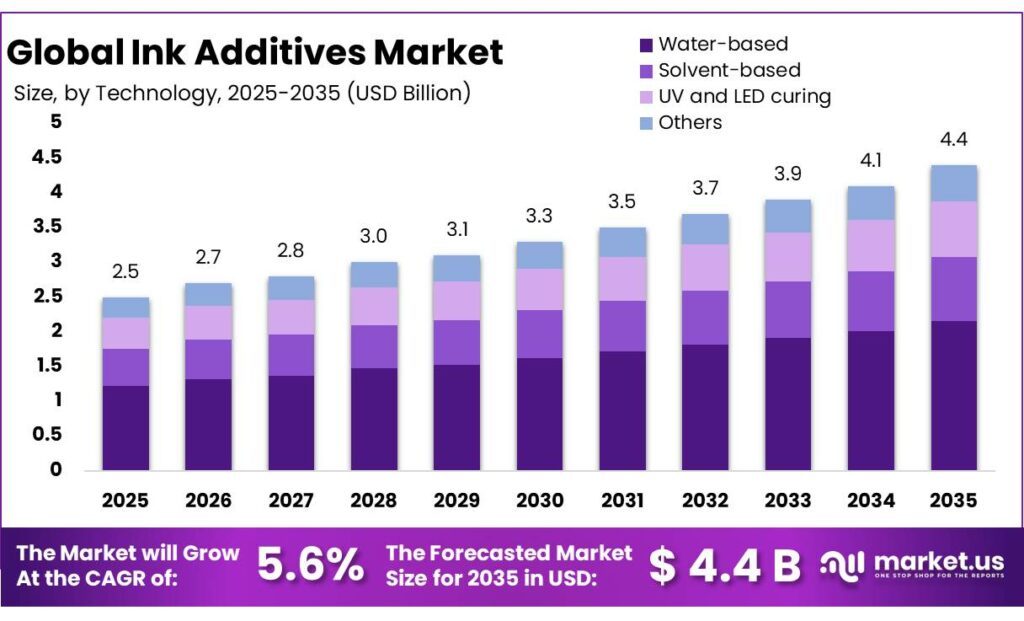

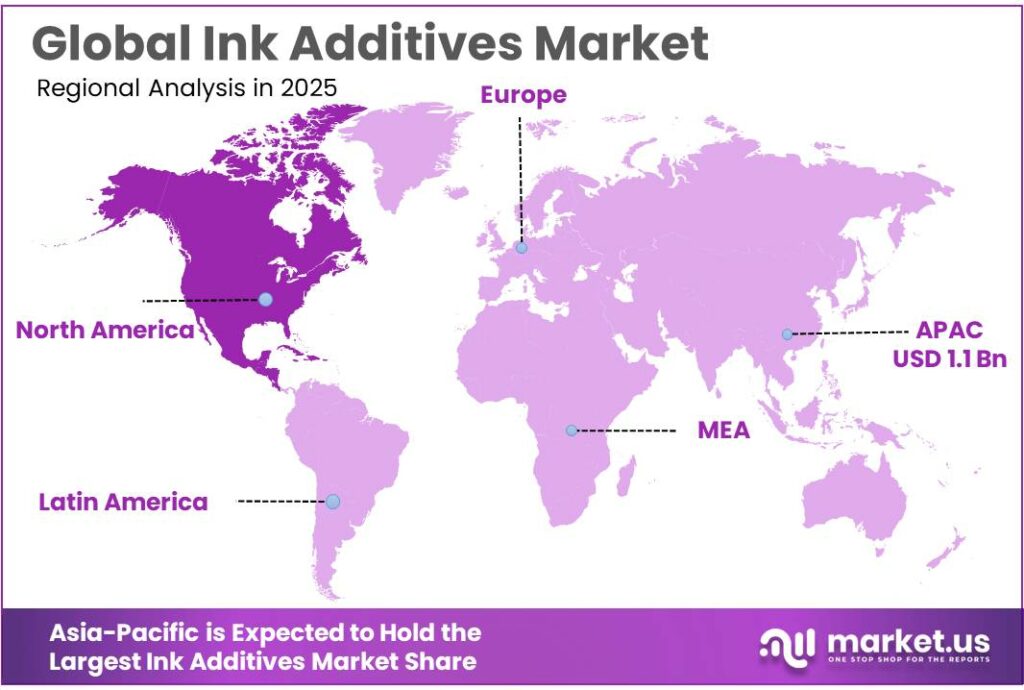

The Global Ink Additives Market size is expected to be worth around USD 4.4 Billion by 2035, from USD 2.5 Billion in 2025, growing at a CAGR of 5.6% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 47.2% share, holding USD 1.1 Billion revenue.

Ink additives are specialty materials used in printing inks to control rheology, pigment dispersion, wetting, adhesion, gloss, slip, foam, drying, curing and durability. The industry’s demand is closely linked to packaging, labels, commercial printing, publication inks and industrial coding, with strongest momentum coming from flexible packaging, corrugated, labels and low-VOC ink systems. In Europe, EuPIA says its members represent more than 90% of European ink sales, equal to 700,000 tonnes and €3 billion in 2024, employing about 12,000 people.

The industrial scenario is shifting from conventional solvent-heavy systems toward waterborne, UV/EB-curable and higher-solids inks, because converters need faster press speeds, better color strength, food-packaging compliance and easier recyclability. Packaging remains a major demand base: the U.S. EPA estimated 14.5 million tons of plastic containers and packaging generated in 2018, equal to 5.0% of U.S. municipal solid waste. OECD-based data also shows packaging accounts for 37% of plastic waste in the U.S., 38% in Europe and 45% in China, reinforcing the pressure for printable, recyclable and lower-migration packaging systems.

Key driving factors include stricter VOC expectations, migration-safe food packaging, waterborne inkjet growth, radiation-curing systems and the shift from decorative printing toward functional packaging performance. In 2025, Elementis reported revenue of US$597.5 million, compared with US$603.8 million in 2024, with the movement partly linked to lower Coatings volumes and mix effects.

Regulation is another major driver. The European Commission’s Packaging and Packaging Waste Regulation requires all packaging to be recyclable by 2030, pushing ink systems toward deinking, recyclability, waterborne technologies and cleaner additive chemistries. The FDA also maintains 21 CFR inventories for authorized food-contact substances, including indirect additives under 21 CFR Parts 175–178.

In 2025, Evonik Industries AG remained highly active in ink additives. In March 2025, it launched TEGO® Wet 270 eCO and TEGO® Foamex 812 eCO, its first mass-balanced coating and ink additives; the products contain over 40% and over 60% bio-carbon respectively. Evonik also introduced TEGO® Res 1100, where 3–10% addition enables deinking of solventborne packaging inks at temperatures as low as 40°C. In April–May 2025, it launched TEGO® Wet 288 for waterborne inkjet and radiation-curing inks, plus four AERODISP® dispersions for inkjet receptive coatings.

Key Takeaways

- Ink Additives Market size is expected to be worth around USD 4.4 Billion by 2035, from USD 2.5 Billion in 2025, growing at a CAGR of 5.6%.

- Rheology Modifiers held a dominant market position, capturing more than a 61.5% share.

- Water-based held a dominant market position, capturing more than a 49.6% share.

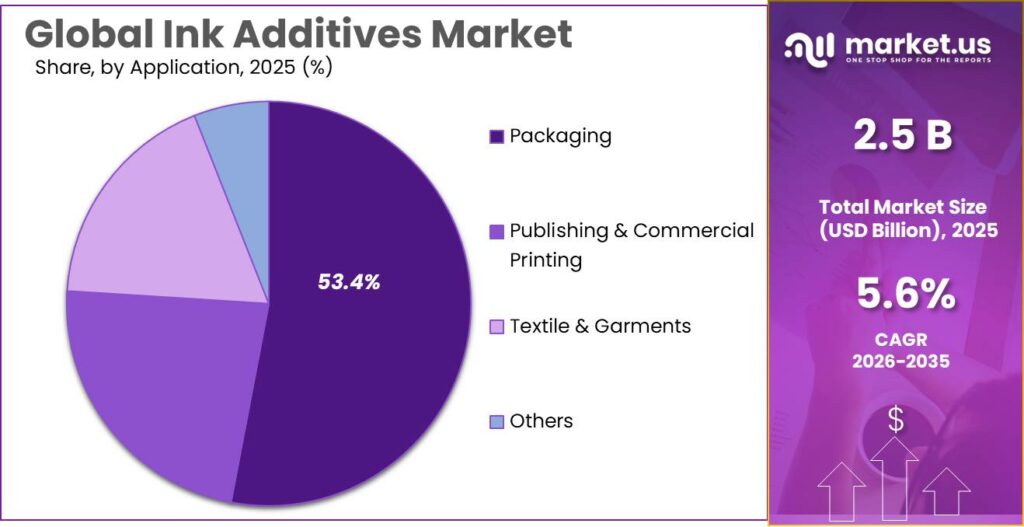

- Packaging held a dominant market position, capturing more than a 53.4% share.

- Asia-Pacific emerged as the dominating region in the ink additives market, accounting for around 47.2% share and reaching a value of nearly USD 1.1 billion.

By Type Analysis

Rheology Modifiers dominate with 61.5% driven by their critical role in ink performance and stability

In 2025, Rheology Modifiers held a dominant market position, capturing more than a 61.5% share. This strong position is mainly because these additives directly control the flow, viscosity, and overall behavior of ink during printing. Manufacturers rely heavily on rheology modifiers to ensure smooth application, proper drying, and consistent print quality across different substrates. Whether it is packaging, publishing, or industrial printing, maintaining the right ink thickness and flow is essential, and this is where rheology modifiers play a key role.

By Technology Analysis

Water-based inks lead with 49.6% as industries shift toward safer and eco-friendly solutions

In 2025, Water-based held a dominant market position, capturing more than a 49.6% share. This growth is largely driven by increasing environmental awareness and stricter regulations around solvent emissions. Water-based inks are widely preferred because they contain fewer harmful chemicals, making them safer for both workers and the environment. They are commonly used in packaging, especially for food and consumer goods, where safety and low odor are important.

By Application Analysis

Packaging leads with 53.4% as demand for printed consumer goods keeps rising

In 2025, Packaging held a dominant market position, capturing more than a 53.4% share. This strong share is mainly due to the growing need for printed packaging across food, beverages, personal care, and e-commerce products. Ink additives play an important role in ensuring that packaging prints are clear, durable, and resistant to smudging or fading during handling and transport. Brands are also focusing more on attractive designs and high-quality finishes to stand out on shelves, which further increases the use of advanced ink formulations.

Key Market Segments

By Type

- Rheology Modifiers

- Synthetic Water-based

- Inorganic

- Cellulosic

- Solvent-based Synthetic

- Defoamers

- Wetting Agents

- Mineral Oil-based

- Surfactant-based

- Polymer-based

- Silicone-based

- Acrylic Polymer-based

- Fluorosurfactants

- Others

By Technology

- Water-based

- Solvent-based

- UV and LED curing

- Others

By Application

- Packaging

- Flexible Packaging

- Rigid Packaging

- Labels & Tags

- Corrugated Packaging

- Publishing & Commercial Printing

- Textile & Garments

- Others

Emerging Trends

Shift toward eco-friendly and low-emission inks is becoming a key market trend

One of the most noticeable trends in the ink additives market is the growing move toward eco-friendly and low-emission ink solutions, especially in food packaging. This shift is not random—it is strongly linked to the environmental pressure created by global food systems. According to the Food and Agriculture Organization, food loss and waste alone contribute 8–10% of global greenhouse gas emissions

Ink manufacturers are now focusing on additives that reduce harmful emissions like VOCs and support safer packaging. In 2025 and 2026, many companies are moving toward water-based, plant-based, and UV-curable inks, which are designed to lower environmental impact while maintaining print quality. These inks are especially important for food packaging, where safety and compliance are critical. At the same time, sustainability guidelines are encouraging inks that do not interfere with recycling processes.

Innovation in sustainable packaging materials is changing additive requirements

Another important trend is the rapid innovation in sustainable packaging materials, which is directly influencing the type of ink additives needed. The FAO reports that around 37.3 million tonnes of plastic are used in food packaging globally. At the same time, plastic pollution has become a serious issue, with 19–23 million tonnes of plastic entering aquatic ecosystems each year.

As these new materials enter the market, traditional ink additives often struggle to perform effectively on them. This has created a need for advanced additives that can deliver strong adhesion, faster drying, and better durability on non-traditional surfaces. In 2026, innovation is clearly moving toward additives that support circular economy goals, meaning they work well with recycling and reuse systems. Packaging is no longer just about protecting food—it is also about reducing waste and environmental impact.

Drivers

Rising food waste is pushing demand for better packaging and ink additives

One of the biggest drivers for the ink additives market is the growing global concern around food loss and waste. According to the Food and Agriculture Organization, about 13.2% of food is lost after harvest, and an additional 19% is wasted at retail and consumer levels. This is a huge issue because food waste not only impacts supply but also increases environmental pressure. Around 8–10% of global greenhouse gas emissions are linked to food loss and waste.

This situation has made packaging more important than ever. Proper packaging helps extend shelf life, protect food during transport, and reduce spoilage. As a result, industries are investing more in high-performance inks that can print on advanced packaging materials without affecting food safety. Ink additives play a key role here, improving adhesion, durability, and resistance to moisture or temperature changes.

Growth in global food packaging is increasing additive demand

Another strong driver comes from the rapid growth of food packaging across the world. Data from the Food and Agriculture Organization shows that food systems used around 37.3 million tonnes of plastic in packaging alone. This highlights how massive the packaging sector has become, especially with rising demand for processed and packaged food products.

As packaging volumes increase, the need for high-quality printing also grows. Labels, branding, safety instructions, and expiry details all depend on reliable ink performance. Ink additives help improve print clarity, drying speed, and resistance to smudging, which is essential for large-scale food distribution.

Restraints

Strict food safety and migration rules are limiting additive usage

One major restraining factor for the ink additives market is the growing pressure from food safety regulations, especially for packaging that comes in direct or indirect contact with food. Governments and global organizations are tightening rules to ensure that chemicals from inks do not migrate into food. This has become a serious concern because food contamination risks are rising along with global waste levels. According to the Food and Agriculture Organization, around 13.2% of food is lost in the supply chain and 19% is wasted at retail and consumer levels

Manufacturers are required to reformulate inks to meet compliance standards, which increases production costs and slows down innovation. In 2025 and 2026, stricter compliance checks, certifications, and testing procedures have made it harder for smaller players to compete. While these rules are important for consumer safety, they act as a barrier for the wider adoption of certain ink additives, particularly in sensitive sectors like food packaging.

Environmental concerns and emission targets are restricting chemical-based additives

Another key challenge comes from rising environmental concerns and global emission targets. Food waste itself already contributes significantly to environmental damage, accounting for 8–10% of global greenhouse gas emissions according to FAO data. This has pushed governments and international bodies to introduce stricter environmental policies, not just in agriculture but across the entire supply chain, including packaging and printing.

Ink additives, especially solvent-based ones, are being closely monitored because they release volatile organic compounds (VOCs) and other pollutants. Many countries are now promoting low-emission or eco-friendly alternatives, which limits the use of conventional additives. In 2026, sustainability targets linked to the UN’s food waste reduction goals are also influencing packaging standards.

Opportunity

Sustainable packaging shift is opening new demand for eco-friendly ink additives

One of the biggest growth opportunities for ink additives is coming from the global push toward sustainable food packaging. The Food and Agriculture Organization highlights that around 37.3 million tonnes of plastic are used in food packaging every year. This massive scale shows how dependent the food industry still is on traditional packaging materials.

This transition is creating a strong need for new types of ink additives that can work with eco-friendly substrates like biodegradable films, paper-based packaging, and recycled plastics. Traditional additives often do not perform well on these materials, so manufacturers are developing safer and more adaptable formulations.

Expanding packaged food consumption is creating long-term growth potential

Another strong opportunity comes from the steady rise in packaged food consumption worldwide. According to FAO-based insights, global packaged food consumption grew by around 8% in 2023, showing a clear increase in demand for processed and ready-to-eat products. As more people rely on packaged foods for convenience, the need for high-quality packaging continues to grow across regions.

Governments are also encouraging better labeling standards and safer food distribution systems, which increases the need for high-performance inks. As packaging volumes increase, even small improvements in ink formulation can have a big impact, making additives an essential part of the value chain. This ongoing expansion of packaged food consumption creates a stable and long-term growth path for the ink additives market.

Regional Insights

Asia-Pacific dominates with 47.2% share valued at USD 1.1 Bn driven by strong packaging and manufacturing demand

In 2025, Asia-Pacific emerged as the dominating region in the ink additives market, accounting for around 47.2% share and reaching a value of nearly USD 1.1 billion. This strong position is mainly supported by the region’s large-scale manufacturing base and rapidly expanding packaging industry. Countries across Asia-Pacific continue to see high demand for packaged food, consumer goods, and e-commerce shipments, all of which require high-quality printing solutions.

The growing use of flexible packaging and labeling has directly increased the consumption of ink additives used to improve print performance, durability, and visual appeal. Market expansion in the region is also supported by the steady growth of printing technologies and increasing adoption of digital and flexographic printing processes.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Elementis showed steady performance in 2025 with total revenue of $597.5 million, slightly down from $603.8 million in 2024, but with improved profitability. The company reported adjusted operating profit of $126.7 million and a 21.2% operating margin, reflecting better cost control and pricing strategies. Personal Care contributed $224.5 million, while Coatings generated $373.0 million, showing strong segment diversification.

Evonik remains one of the largest players in specialty chemicals, reporting €14.1 billion in sales in 2025, despite a 7% decline from the previous year. The company achieved €1.87–1.9 billion adjusted EBITDA, showing strong operational efficiency and cost management. Net income reached €265 million, reflecting improved profitability.

Lubrizol Corporation operates as a major global supplier of specialty chemicals, with reported revenue of around $6.5 billion. The company serves multiple industries including transportation, industrial applications, and personal care, with a workforce of over 7,000 employees globally.

Top Key Players Outlook

- Elementis

- Evonik Industries AG

- Lubrizol Corporation

- Münzing Corporation

- Patcham FZC

- Shamrock Technologies

- BASF SE

- Arkema S.A.

- Ashland

- Clariant AG

- Eastman Chemical Company

Recent Industry Developments

In 2025, Elementis plc continued to strengthen its position in the ink additives sector through its focus on rheology modifiers and performance additives used in coatings and printing inks. The company reported revenue of around $597.5 million in 2025, with adjusted operating profit reaching $126.7 million and operating margins improving to 21.2%, showing solid efficiency despite softer demand in coatings markets.

In 2025, Evonik Industries AG continued to play a strong role in the ink additives sector through its Coating Additives business, which supports printing inks with dispersants, defoamers, and surface modifiers used in packaging and industrial printing. The company reported total sales of €14.1 billion in 2025, with adjusted EBITDA close to €1.9 billion and net income of €265 million, showing stable financial performance despite a challenging demand environment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.5 Bn |

| Forecast Revenue (2035) | USD 4.4 Bn |

| CAGR (2026-2035) | 5.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Rheology Modifiers, Wetting Agents), By Technology (Water-based, Solvent-based, UV and LED curing, Others), By Application (Packaging, Publishing And Commercial Printing, Textile And Garments, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Elementis, Evonik Industries AG, Lubrizol Corporation, Münzing Corporation, Patcham FZC, Shamrock Technologies, BASF SE, Arkema S.A., Ashland, Clariant AG, Eastman Chemical Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |