Quick Navigation

Report Overview

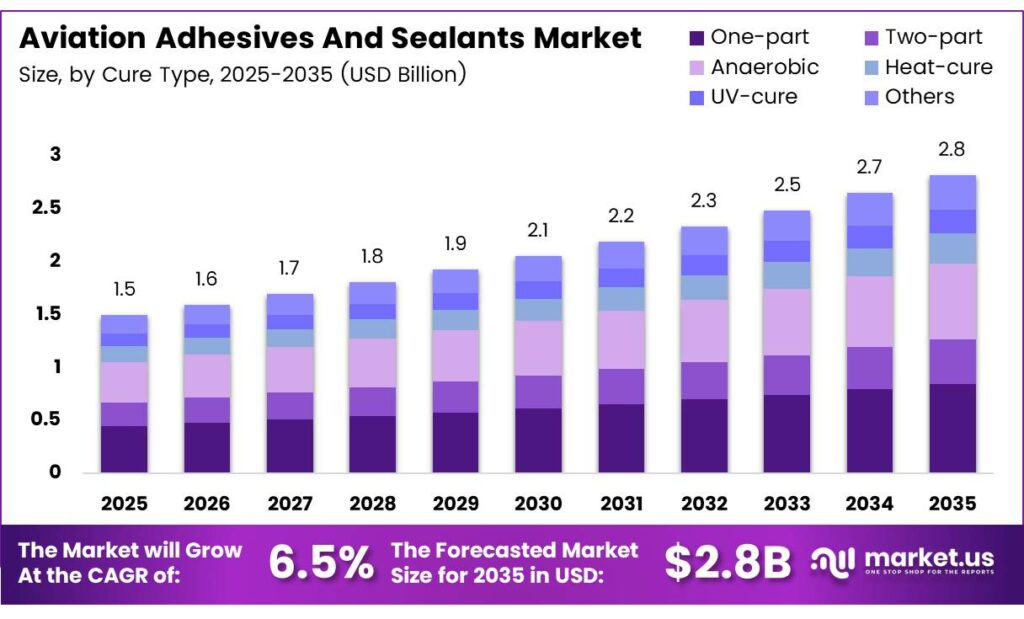

The Global Aviation Adhesives and Sealants Market size is expected to be worth around USD 2.8 billion by 2035 from USD 1.5 billion in 2025, growing at a CAGR of 6.5% during the forecast period 2026 to 2035.

Aviation adhesives and sealants serve as structural and protective bonding materials used across airframe assembly, interior fitouts, electronics protection, and MRO applications. These materials replace or supplement mechanical fasteners, reducing aircraft weight and improving fuel efficiency. Their performance under extreme temperature, pressure, and chemical exposure makes them non-substitutable in modern aerospace manufacturing.

Rising fleet expansion by major OEMs highlights a clear production-driven pull on materials demand. Airbus delivered 793 commercial aircraft in 2025, marking a 4% year-over-year increase. This growth directly boosts the need for adhesives and sealants during assembly, giving suppliers with certified aerospace-grade formulations a durable advantage as output continues to scale.

3M AC-730 aerospace sealant demonstrates strong performance for such applications, achieving 2.76 MPa tensile strength and 378% elongation after curing. Even after fuel immersion, it retains 2.32 MPa tensile strength and 342% elongation, confirming its reliability for dynamic structural sealing under real operating conditions.

Sustainability mandates and low-VOC compliance requirements are reshaping procurement criteria across aerospace supply chains. Regulatory bodies in North America and Europe are tightening chemical emissions thresholds for manufacturing facilities, pushing aerospace buyers to qualify environmentally compliant alternatives. Suppliers who complete this transition ahead of regulatory deadlines reduce buyer risk and strengthen long-term contract renewal prospects.

Key Takeaways

- The Global Aviation Adhesives and Sealants Market was valued at USD 1.5 billion in 2025 and is forecast to reach USD 2.8 billion by 2035 at a CAGR of 6.5% during the forecast period 2026 to 2035.

- Epoxy leads the market with a 36.9% share in 2025.

- Two-part systems hold the dominant position with a 39.1% share.

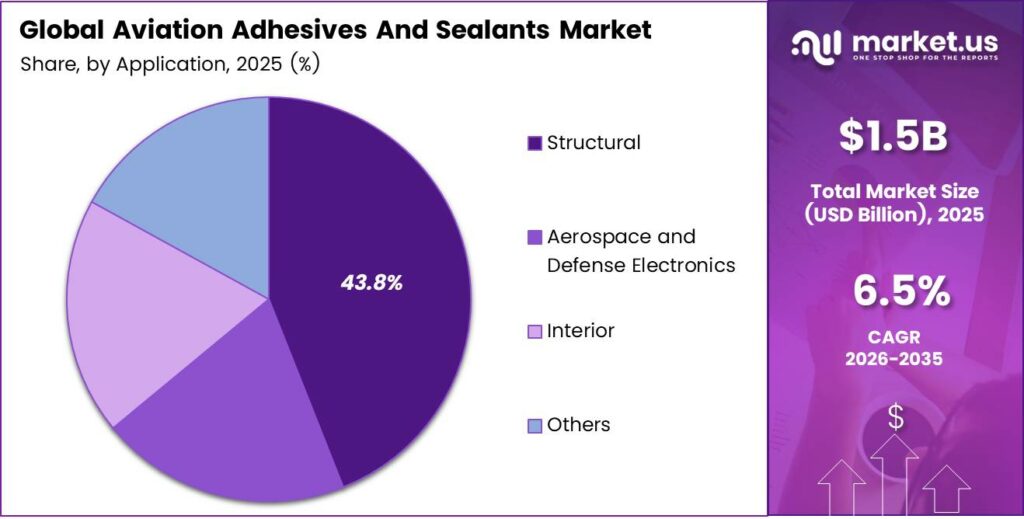

- Structural applications account for the largest share at 43.8%.

- Commercial Aviation commands 51.3% of the total market share.

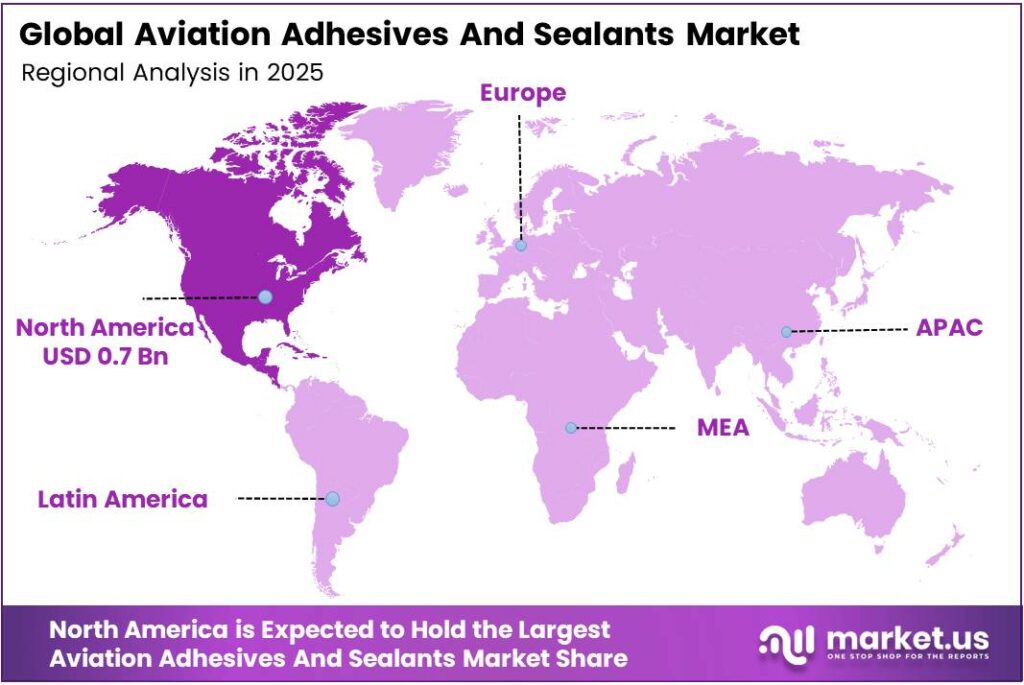

- North America leads all regions with a 44.4% share, valued at USD 0.7 billion.

Product Analysis

Epoxy dominates with 36.9% due to superior structural bonding in composite-heavy airframes.

In 2025, Epoxy held a dominant market position in the By Resin segment of the Aviation Adhesives and Sealants Market, with a 36.9% share. Epoxy systems deliver high tensile strength, chemical resistance, and compatibility with carbon fiber reinforced polymers — the primary structural material in next-generation aircraft. Their dominance reflects the direct relationship between composite airframe adoption and structural adhesive specification.

Acrylic adhesives serve applications requiring fast cure times and strong bonding to dissimilar substrates. Acrylics offer flexibility advantages over rigid epoxy systems, making them suitable for interior panels, secondary structures, and vibration-prone assemblies. Their use has expanded as MRO facilities prioritize faster repair cycles to minimize aircraft ground time.

Cure Type Analysis

Two-part systems dominate with 39.1% due to superior strength-to-weight performance in structural joints.

In 2025, Two-part cure systems held a dominant market position in the by-cure-type segment of the Aviation Adhesives and Sealants Market, with a 39.1% share. Two-part formulations — where resin and hardener mix at application — deliver higher crosslink density and mechanical performance than single-component alternatives.

One-part systems attract MRO and secondary assembly applications where simplified handling outweighs peak performance requirements. Eliminating mix ratios reduces operator error and speeds up workflow — two factors that matter significantly in time-sensitive repair operations. Airbus recorded 1,000 gross aircraft orders in 2025 from 57 customers, indicating sustained fleet expansion that will sustain long-term MRO adhesive demand, including one-part formats.

Application Analysis

Structural applications dominate with 43.8% due to composite airframe mandates requiring certified bonding solutions.

In 2025, Structural applications held a dominant market position in the By Application segment of the Aviation Adhesives and Sealants Market, with a 43.8% share. Structural adhesives bond primary load-bearing assemblies, including fuselage skins, wing panels, and floor structures. As composite content in new aircraft exceeds 50% by weight, structural adhesive consumption per aircraft unit increases proportionally — a direct volume multiplier for suppliers holding OEM approvals.

Aerospace and Defense Electronics bonding covers potting compounds, conformal coatings, and encapsulation adhesives used in avionics boxes, radar systems, and flight control electronics. These applications demand materials with dielectric properties, thermal conductivity, and resistance to moisture ingress.

Interior applications include cabin wall linings, overhead bins, galley structures, and seat track bonding. Interior adhesives must meet fire, smoke, and toxicity standards set by aviation safety authorities. Airline fleet refurbishment cycles create a recurring demand channel for interior adhesive materials that operates independently of new aircraft production volumes.

End-Use Industry Analysis

Commercial Aviation dominates with 51.3% due to high-volume fleet production and structured MRO cycles.

In 2025, Commercial Aviation held a dominant market position in the By End-Use Industry segment of the Aviation Adhesives and Sealants Market, with a 51.3% share. Passenger aircraft production at OEM scale consumes adhesives and sealants across thousands of bonded joints per aircraft. Boeing’s recovery to 600 deliveries in 2025 — its strongest performance since 2018 — confirms that commercial aviation now anchors the consumption baseline for the entire adhesives and sealants market.

Defense Aviation procurement operates under military specification frameworks that require independent qualification of every adhesive and sealant used in combat or surveillance platforms. Defense programs favor long-term supply contracts with pre-qualified material sources, creating a stable but access-restricted revenue channel. Suppliers with dual-use approvals across commercial and military specifications hold the strongest competitive position in this segment.

Key Market Segments

By Resin

- Epoxy

- Acrylic

- Cyanoacrylate

- Polyurethane

- Silicone

- VAE/EVA

- Others

By Cure Type

- One-part

- Two-part

- Anaerobic

- Heat-cure

- UV-cure

- Others

By Application

- Structural

- Aerospace and Defense Electronics

- Interior

- Others

By End-Use Industry

- Commercial Aviation

- Defense Aviation

- General Aviation and Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Emerging Trends

Nano-Enhanced Formulations and Smart Adhesive Technologies Redefine Performance Benchmarks in Aerospace Bonding

Nano-particle reinforcement in adhesive matrices delivers measurable strength and durability improvements without adding structural weight. Carbon nanotube and nano-silica additives increase fracture toughness and fatigue resistance in bonded joints — performance dimensions that standard resin systems cannot match.

Smart adhesives with self-healing and sensing capabilities represent a functional shift from passive bonding to active structural monitoring. The AF 3074 adhesive system operates from -55°C to 135°C and cures between 120°C and 180°C — a performance envelope that illustrates the thermal discipline required even in current-generation aerospace adhesive products, let alone next-generation smart variants.

Fast-curing one-component adhesive formats address OEM and MRO throughput pressures by eliminating mix preparation steps. Digital twin and predictive maintenance platforms now incorporate sealant degradation models that generate proactive replacement schedules — reducing unplanned maintenance events and shifting adhesive procurement from reactive to planned purchasing cycles.

Drivers

Fleet Expansion and MRO Growth Push Sustained Demand for High-Performance Aerospace Bonding Materials

Commercial aircraft fleet expansion creates the most direct pull on aviation adhesive and sealant consumption. Each new aircraft assembly requires thousands of bonded joints across structural, interior, and electronic applications. Airbus ended 2025 with a backlog of 8,754 aircraft — a production pipeline that guarantees multi-year material procurement at scale and removes demand uncertainty for approved adhesive suppliers.

Composite material adoption in modern airframe design raises adhesive consumption per aircraft unit. As OEMs replace aluminum panels with carbon fiber reinforced structures, mechanical fasteners alone cannot deliver the required joint integrity. Epoxy and polyurethane adhesives become load-bearing components — not secondary materials — in these assemblies.

MRO activity creates a parallel and largely cycle-independent demand channel. Airlines operating aging fleets require sealant replacement, structural repair compounds, and interior rebonding materials on fixed maintenance schedules. Stringent airworthiness directives issued by aviation regulators mandate regular sealant inspection and replacement across pressurized fuselage sections and fuel systems — converting regulatory compliance into a predictable, recurring revenue source for qualified material suppliers.

Restraints

Raw Material Price Volatility and Certification Complexity Constrain Margin Stability and Market Entry

Raw material costs for epoxy resins, polyurethane precursors, and specialty silicones fluctuate with petrochemical feedstock pricing. Aerospace adhesive manufacturers cannot easily pass cost increases to OEM customers bound by multi-year fixed-price supply agreements. Boeing increased 737 production to 42 aircraft per month and 787 to 8 aircraft per month in late 2025 — a volume ramp that amplifies raw material cost exposure for suppliers locked into pre-negotiated pricing structures.

Aerospace material certification timelines extend from 18 months to several years, depending on the application category and certifying authority. New adhesive formulations require qualification testing across temperature extremes, fluid immersion, fatigue cycles, and aging protocols before OEM approval. This process consumes significant capital and delays revenue generation — creating a structural entry barrier that protects incumbent suppliers but limits the pace at which the market can adopt next-generation low-VOC or nano-enhanced formulations.

Dual compliance requirements across commercial and defense specifications multiply the certification burden for suppliers seeking full-market access. A material qualified for commercial OEM use may require separate military specification testing for defense program eligibility. This parallel compliance structure increases development costs, extends time-to-market, and concentrates competitive advantage among large, resource-rich suppliers who can absorb multi-track qualification programs simultaneously.

Growth Factors

Electric Aircraft Programs and Emerging Aerospace Hubs Open New Material Specification Channels

Next-generation electric and hybrid aircraft programs introduce bonding requirements that existing adhesive portfolios only partially address. Lightweight battery enclosures, thermal management interfaces, and motor-to-airframe structural joints require adhesives with electrical insulation, heat dissipation, and vibration damping properties — a combination that standard aerospace epoxies do not fully deliver.

Aerospace manufacturing expansion in the Asia Pacific and Middle Eastern economies creates geographically distributed procurement hubs. Boeing, a record $682 billion backlog including 6,100+ aircraft in 2025, confirms sustained conventional production, while electric program development runs in parallel — creating a dual-track demand structure for adhesive suppliers.

Automation and robotics integration in adhesive application processes reduces labor variability and improves bond consistency at scale. Robotic dispensing systems require adhesives with precisely controlled viscosity, pot life, and cure profiles — specifications that differ from manually applied formats.

Regional Analysis

North America Dominates the Aviation Adhesives and Sealants Market with a Market Share of 44.4%, Valued at USD 0.7 Billion

North America commands 44.4% of the global Aviation Adhesives and Sealants Market, valued at USD 0.7 billion in 2025. The United States hosts the primary manufacturing facilities of both major commercial aircraft OEMs and a dense tier-1 aerospace supply chain.

Europe holds the second-largest regional share, anchored by Airbus’s commercial aircraft production footprint across France, Germany, Spain, and the UK. The region’s dense aerospace manufacturing ecosystem generates consistent adhesive demand across OEM assembly and tier-1 component production.

Asia Pacific represents the fastest-expanding geography for aviation adhesive demand, driven by fleet growth in China, India, and Southeast Asia. Government investment in domestic aerospace manufacturing capability — particularly China’s COMAC program and India’s defense production initiatives — creates new OEM-level adhesive procurement channels.

Latin America’s aviation adhesive market centers on Brazil, home to Embraer’s commercial and defense aircraft programs that generate consistent structural adhesive demand. Regional carriers’ fleet modernization programs create MRO adhesive consumption as aging aircraft transition to newer platforms.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

3M holds a strong position in the aviation adhesives and sealants market through a broad portfolio of FAA- and OEM-approved structural and sealing compounds. The company’s dual-chemistry coverage — spanning epoxy, silicone, and polysulfide formats — allows it to address both new aircraft assembly and MRO applications from a single approved supplier relationship. This breadth reduces customer switching risk and strengthens 3M’s contract retention across long-cycle OEM programs.

Henkel AG and Co. KGaA competes through deep integration with aerospace tier-1 manufacturers and a technically differentiated product line covering structural film adhesives, threadlockers, and potting compounds. Henkel’s approach of co-developing application-specific formulations with aircraft assemblers creates high qualification switching costs for buyers. This co-development model translates technical expertise into durable supply agreements that resist displacement even during procurement consolidation cycles.

Dow leverages silicone and polyurethane chemistry leadership to address high-temperature and flexible sealing applications across commercial and defense aircraft platforms. Dow’s global manufacturing footprint supports regional supply chain requirements that large OEM customers increasingly mandate. Its investment in sustainable chemistry — including low-VOC silicone sealants — positions the company to capture share as aerospace buyers face tightening environmental compliance timelines.

Key Players

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- Beacon Adhesives, Inc.

- Chemique Adhesives and Sealants Ltd

- DELO Industrie Klebstoffe GmbH and Co. KGaA

- Dow

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- Master Bond Inc.

- Permabond LLC.

- PPG Industries, Inc.

- Solvay

Recent Developments

- In 2024, 3M highlighted aerospace as part of its Transportation & Electronics Business Group in its Annual Report, reporting that this business group generated $7.4 billion in net sales and serves industries including aerospace and defense.

- In 2025, Beacon published an aerospace-and-aviation industry page saying its products have been used in aerospace and aviation for more than 70 years, including aircraft and aerospace epoxies and sealants for helicopters, drones, commercial aircraft, and aerospace electronics.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.5 Billion |

| Forecast Revenue (2035) | USD 2.8 Billion |

| CAGR (2026-2035) | 6.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Resin (Epoxy, Acrylic, Cyanoacrylate, Polyurethane, Silicone, VAE/EVA, Others), By Cure Type (One-part, Two-part, Anaerobic, Heat-cure, UV-cure, Others), By Application (Structural, Aerospace and Defense Electronics, Interior, Others), By End-Use Industry (Commercial Aviation, Defense Aviation, General Aviation and Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | 3M, Arkema Group, AVERY DENNISON CORPORATION, Beacon Adhesives Inc., Chemique Adhesives and Sealants Ltd, DELO Industrie Klebstoffe GmbH and Co. KGaA, Dow, H.B. Fuller Company, Henkel AG and Co. KGaA, Huntsman International LLC, Illinois Tool Works Inc., Master Bond Inc., Permabond LLC., PPG Industries Inc., Solvay |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |