Quick Navigation

Report Overview

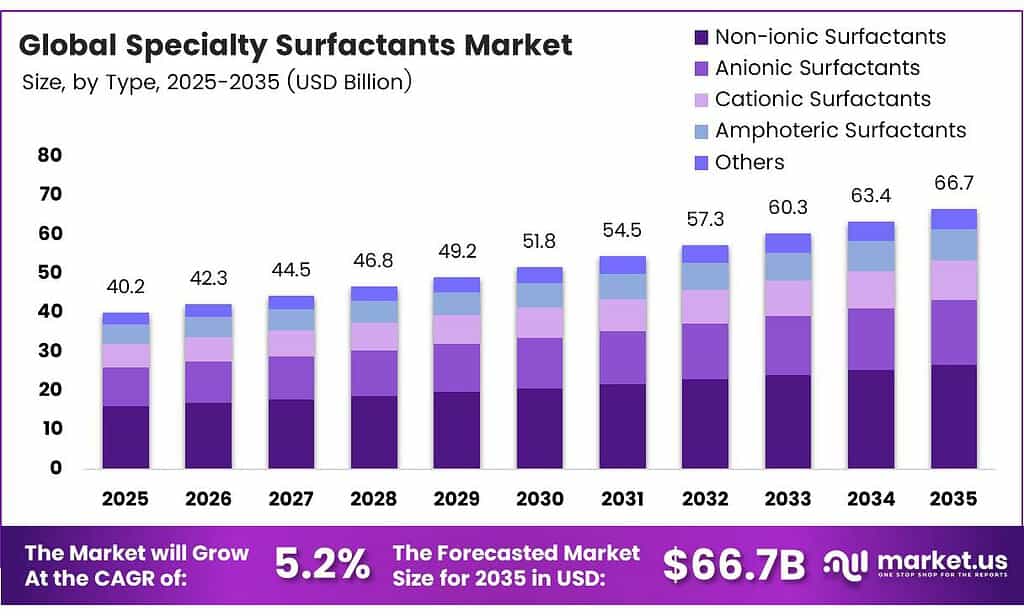

The Global Specialty Surfactants Market size is expected to be worth around USD 66.7 billion by 2035 from USD 40.2 billion in 2025, growing at a CAGR of 5.2% during the forecast period 2026 to 2035.

Specialty surfactants are surface-active compounds engineered for targeted performance across personal care, agriculture, oilfield operations, and industrial cleaning. Unlike commodity surfactants, specialty variants deliver precise functional outcomes — controlled foaming, stable emulsification, or enhanced wetting — that justify their price premium in formulation-sensitive applications.

BASF reported approximately €65 million in cumulative savings in 2025 through continuous improvement in its ethylene oxide value chain, which feeds ethoxylated specialty surfactants. This signals that leading producers are wringing efficiency from existing infrastructure — compressing margins for mid-tier players who cannot match that scale and cost discipline.

Colonial Chemical announced the addition of two new specialty surfactant reactors at its South Pittsburg, U.S., facility. The expansion increases overall surfactant production capacity by 15%, targeting amphoteric and imidazoline-based chemistries to meet tightening demand from personal care and industrial formulators.

The oilfield chemicals segment reinforces this diversified demand base. Enhanced oil recovery operations rely on specialty surfactants to mobilize residual crude in depleted reservoirs. With oil producers focusing on field productivity rather than new exploration, consumption of specialty surfactants in EOR applications has become a consistent procurement category.

Key Takeaways

- The Global Specialty Surfactants Market is valued at USD 40.2 billion in 2025 and is forecast to reach USD 66.7 billion by 2035 at a CAGR of 5.2% during the forecast period 2026 to 2035.

- Non-ionic Surfactants lead with a 36.8% share in 2025.

- Emulsifiers hold the largest share at 26.7% in 2025.

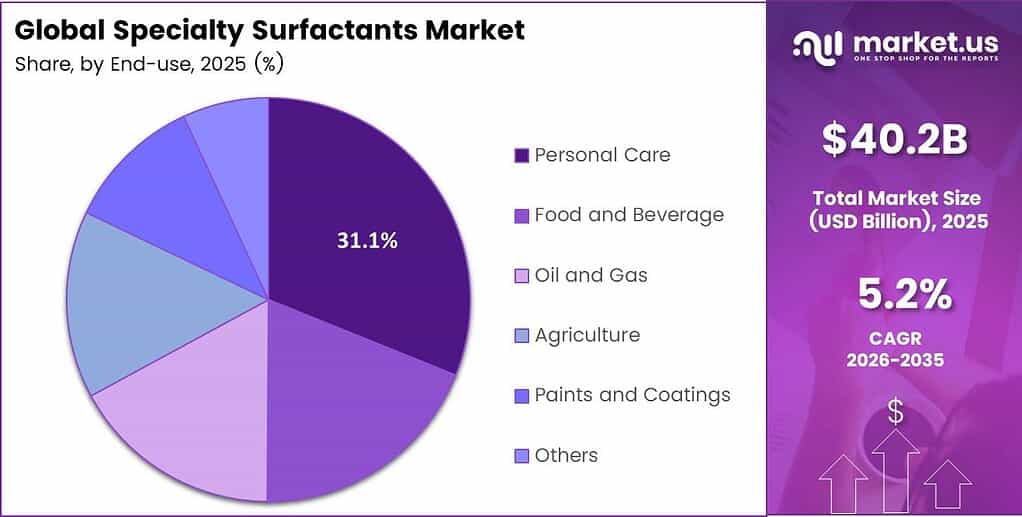

- Personal Care dominates with a 31.1% share in 2025.

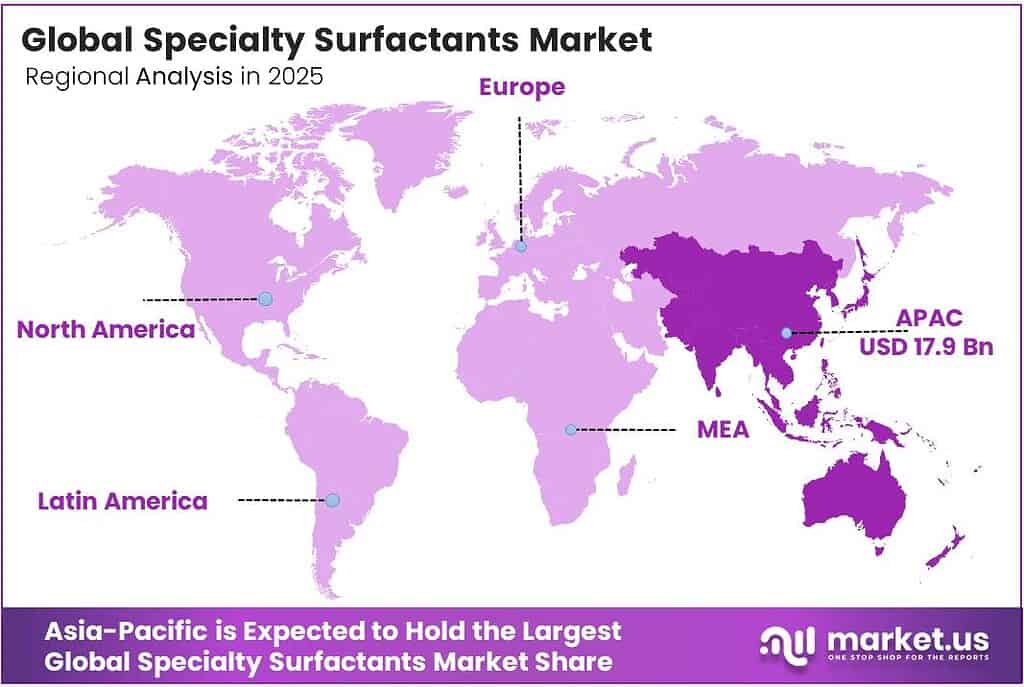

- Asia-Pacific leads regional demand with a 44.6% share, valued at USD 17.9 billion.

Type Analysis

Non-ionic Surfactants dominate with 36.8% due to broad compatibility and low irritation profile.

In 2025, Non-ionic Surfactants held a dominant market position in the By Type segment of the Specialty Surfactants Market, with a 36.8% share. Their charge-neutral structure allows stable formulation alongside both anionic and cationic ingredients — a critical advantage in personal care and industrial cleaning where multi-component compatibility determines product performance.

Anionic Surfactants carry the highest volume per formulation across detergent and shampoo categories, but face reformulation pressure. Consumer sensitivity to sulfates and rising regulatory scrutiny of certain anionic chemistries are pushing formulators toward milder alternatives, compressing anionic surfactant growth in premium product lines while sustaining volume in industrial and institutional applications.

Application Analysis

Emulsifiers dominate with 26.7% due to their indispensable role in formulation stability.

In 2025, Emulsifiers held a dominant market position in the By Application segment of the Specialty Surfactants Market, with a 26.7% share. Personal care, food processing, and pharmaceutical formulations all require stable oil-water interfaces — a function only surfactant-based emulsifiers can reliably deliver. This functional indispensability insulates emulsifier demand from commodity price cycles.

Wetting Agents reduce surface tension to accelerate liquid penetration into solid substrates. In agrochemical applications, wetting agents directly improve pesticide coverage efficiency — reducing active ingredient waste and improving regulatory compliance ratios. Textile and paper industries also depend on wetting agents to control coating uniformity and process speed.

End-User Analysis

Personal Care dominates with 31.1% due to formulation complexity and premium ingredient demand.

In 2025, Personal Care held a dominant market position in the By End-User segment of the Specialty Surfactants Market, with a 31.1% share. Skincare, haircare, and color cosmetics formulators select surfactants on performance criteria — mildness, foam quality, emulsion stability — rather than cost alone. This premium selection behavior makes personal care the highest-value end-user channel for specialty surfactant producers.

Food and Beverage applications depend on emulsifiers, stabilizers, and foaming agents approved under strict food-contact regulations. Specialty surfactants in this segment must meet both functional and regulatory specifications simultaneously — a dual barrier that limits competitive entry and supports stable long-term supply relationships between food manufacturers and approved surfactant producers.

Oil and Gas consumption centers on enhanced oil recovery and drilling fluid formulations. Oilfield specialty surfactants must perform under extreme temperature, pressure, and salinity conditions — requirements that eliminate most standard chemistries. EOR applications in mature fields represent a structurally consistent demand stream as producers optimize production from existing reservoirs rather than developing new ones.

Key Market Segments

By Type

- Non-ionic Surfactants

- Anionic Surfactants

- Cationic Surfactants

- Amphoteric Surfactants

- Others

By Application

- Emulsifiers

- Wetting Agents

- Dispersants

- Foaming Agents

- Stabilizers

- Others

By End-User

- Personal Care

- Food and Beverage

- Oil and Gas

- Agriculture

- Paints and Coatings

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Emerging Trends

Mild Formulations, Nanotechnology Integration, and Strategic Consolidation Reshape Specialty Surfactant Development

Consumer products across haircare and skincare are shifting toward sulfate-free, mild surfactant systems. This is not aesthetic preference — it reflects regulatory restrictions and dermatological evidence linking certain sulfonates to irritation and barrier disruption. Brands reformulating with gentler alternatives are creating sustained, specification-driven procurement demand that favors producers with proprietary mild surfactant chemistries.

Nanotechnology integration in surfactant design enables functional performance unachievable with conventional molecular structures. An Elchemy technical analysis notes that ethoxylated surfactants require ethylene oxide with greater than 99.5% purity and fewer than 10 ppm residuals to maintain consistent functional performance, illustrating that precision input specifications are becoming a baseline competitive requirement in advanced surfactant production.

Strategic consolidations among specialty surfactant producers are simultaneously accelerating portfolio breadth and geographic reach. Producers acquiring complementary chemistry capabilities can offer customers single-source multifunctional surfactant solutions — reducing the number of suppliers a formulator must qualify. For buyers, this simplifies procurement and regulatory documentation.

Drivers

Multisector Demand for High-Performance Specialty Surfactants Accelerates Market Consumption

Personal care formulators are replacing standard surfactants with milder, high-performance alternatives at scale. Haircare and skincare brands now specify surfactant performance attributes — foam texture, irritation index, biodegradability — as primary procurement criteria. Colonial Chemical’s scheduled 15% capacity expansion from late Q4 2025 at its South Pittsburg plant directly reflects this tightening supply-demand balance.

Institutional hygiene standards across emerging economies are creating durable, regulation-driven demand. Food processing facilities, hospitals, and commercial kitchens in Southeast Asia and Latin America now procure surfactants against performance specifications tied to local sanitation mandates.

Agrochemical adjuvants represent a technically demanding and margin-accretive application. Specialty surfactants that improve pesticide coverage efficiency reduce active ingredient waste — a priority for agrochemical producers facing tighter efficacy-per-hectare regulations.

Restraints

Feedstock Price Volatility and Biodegradability Regulations Constrain Specialty Surfactant Margins

Specialty surfactant production depends heavily on petrochemical feedstocks — ethylene oxide, fatty alcohols, and propylene oxide — whose prices move with crude oil markets. When feedstock costs spike, producers face a structural delay between input cost increases and the ability to pass them through contractual customer pricing.

Environmental regulations targeting non-biodegradable surfactants are eliminating entire chemistry classes from approved formulation lists. European REACH and U.S. EPA restrictions on certain anionic and ethoxylated chemistries force reformulation timelines on both surfactant producers and their customers.

The combined pressure of feedstock volatility and regulatory reformulation creates a dual cost burden that disproportionately affects producers without integrated raw material supply or large R&D budgets. Smaller specialty surfactant manufacturers face margin compression from both directions simultaneously — rising input costs and mandatory chemistry reformulation — which is accelerating industry consolidation toward larger, more vertically integrated players.

Growth Factors

Bio-Based Chemistries and Pharmaceutical Applications Open High-Margin Growth Pathways

Bio-based surfactants derived from renewable feedstocks — plant oils, sugars, and fermentation byproducts — address both regulatory and consumer sustainability requirements. A 2025 Royal Society of Chemistry review confirms that process-efficiency projects in specialty surfactant manufacturing can reduce scope-1 energy use by 10–20% in ethoxylation units. This cost reduction makes bio-based production more economically competitive, narrowing the price gap with petrochemical-derived alternatives.

Pharmaceutical drug delivery is emerging as a structurally high-margin application for specialty surfactants. API solubilization, liposomal formulation, and transdermal delivery systems all require surfactants with pharmaceutical-grade purity and biocompatibility — specifications that command significant price premiums.

Water treatment and food processing represent two additional application vectors with structural growth logic. Municipalities and industrial operators facing tighter effluent standards are procuring specialty surfactants for wastewater management. Food manufacturers expanding processed food output in emerging markets simultaneously increase demand for food-grade emulsifiers and stabilizers.

Regional Analysis

Asia-Pacific Dominates the Specialty Surfactants Market with a Market Share of 44.6%, Valued at USD 17.9 Billion

Asia-Pacific commands 44.6% of the global specialty surfactants market, valued at USD 17.9 billion. This position reflects the region’s dense concentration of personal care manufacturing, agrochemical production, and textile processing — all high-consumption end-user sectors. China, India, Japan, and South Korea each operate large domestic surfactant formulation industries, making the Asia-Pacific both the largest production and consumption hub simultaneously.

North America maintains a strong market position built on mature personal care, oilfield chemicals, and institutional cleaning sectors. The U.S. drives volume through a well-established procurement infrastructure in consumer goods manufacturing and EOR operations. Regulatory pressure from the EPA on non-biodegradable chemistries is accelerating reformulation timelines, which structurally favors producers with advanced bio-based and amphoteric surfactant portfolios.

Europe’s specialty surfactant market operates under some of the world’s most stringent chemical regulations, including REACH and the EU Green Deal framework. These constraints paradoxically create commercial opportunity — they force reformulation cycles that generate demand for compliant specialty alternatives. German and French chemical clusters house several globally significant specialty surfactant producers with direct access to major formulation customers across the continent.

Latin America’s market development centers on Brazil and Mexico, where expanding food processing, agrochemical, and personal care manufacturing sectors are converting historically commodity-focused surfactant procurement toward specialty variants. Rising domestic consumer goods production and tightening hygiene standards in institutional sectors are creating structured demand for higher-performance surfactant products beyond standard detergent-grade chemistries.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

BASF holds a structural advantage through its integrated ethylene oxide value chain, which directly feeds its ethoxylated specialty surfactant portfolio. The company’s continuous improvement program in cumulative savings in 2025. This cost efficiency allows BASF to compete on price in volume segments while maintaining margin in high-specification specialty applications.

Evonik differentiates through application-specific surfactant development across personal care, agricultural adjuvants, and oilfield chemicals. Its R&D investment in bio-based surfactant chemistries positions the company to address REACH-driven reformulation requirements in European markets before competitors. Evonik’s direct engagement with formulators at the development stage creates early-stage customer lock-in that is difficult for lower-cost competitors to break post-specification.

Clariant has built a defensible specialty position through its focus on functional surfactants for agrochemical and oilfield applications — segments where technical complexity limits competitive entry. Clariant’s sustainable chemistry agenda, particularly its portfolio of natural and biodegradable surfactants, aligns directly with regulatory trends that are eliminating non-compliant competitors from European and North American markets.

Arkema International AG leverages its specialty chemistry capabilities in high-performance surfactant systems for industrial and technical applications. Arkema’s strategic focus on differentiated chemistries — rather than commodity surfactant volumes — positions it to serve technically demanding end-users in pharmaceutical, electronics, and advanced materials sectors where standard surfactant types cannot meet performance requirements.

Key Players

- BASF

- Evonik

- Clariant

- Arkema International AG

- Stepan Company

- Nouryon

- Syensqo

- Kao Corporation

- Croda International Plc

Recent Developments

- In 2025, BASF and Hannong Chemicals inaugurated a new ethylene oxide and derivatives plant in Daesan, Korea. This is relevant because BASF’s Care Chemicals business uses these intermediates across personal care, home care, industrial & institutional cleaning, and technical applications—all closely tied to surfactant production and formulation.

- In 2025, Evonik said it became the first company worldwide to produce industrial-scale rhamnolipid biosurfactants at its Slovakia site. This remains one of the most important recent developments in biosurfactants among major specialty chemical players.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 40.2 Billion |

| Forecast Revenue (2035) | USD 66.7 Billion |

| CAGR (2026-2035) | 5.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Non-ionic Surfactants, Anionic Surfactants, Cationic Surfactants, Amphoteric Surfactants, Others), By Application (Emulsifiers, Wetting Agents, Dispersants, Foaming Agents, Stabilizers, Others), By End-User (Personal Care, Food and Beverage, Oil and Gas, Agriculture, Paints and Coatings, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | BASF, Evonik, Clariant, Arkema International AG, Stepan Company, Nouryon, Syensqo, Kao Corporation, Croda International Plc |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |