Quick Navigation

Report Overview

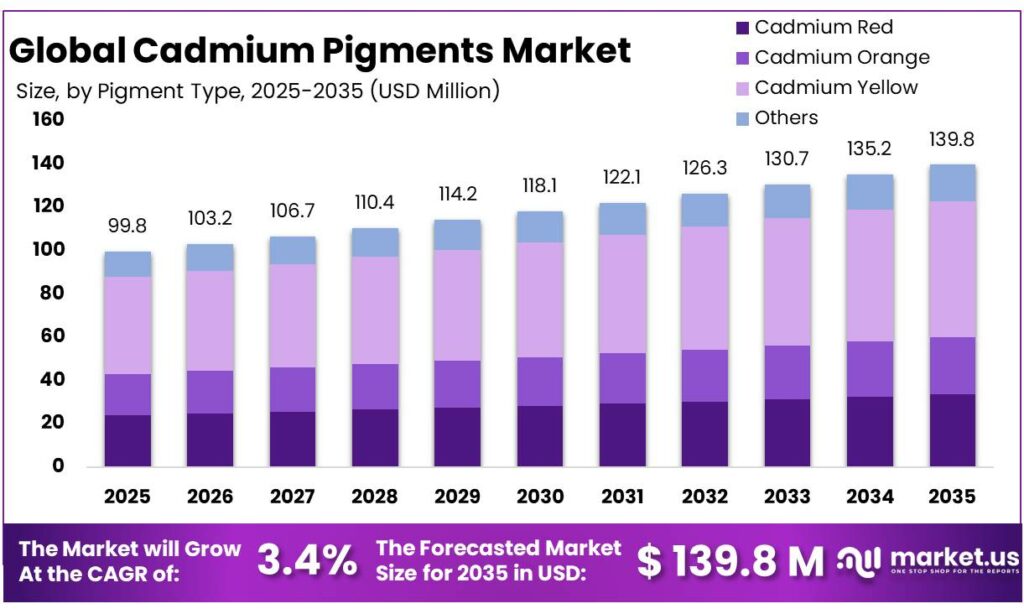

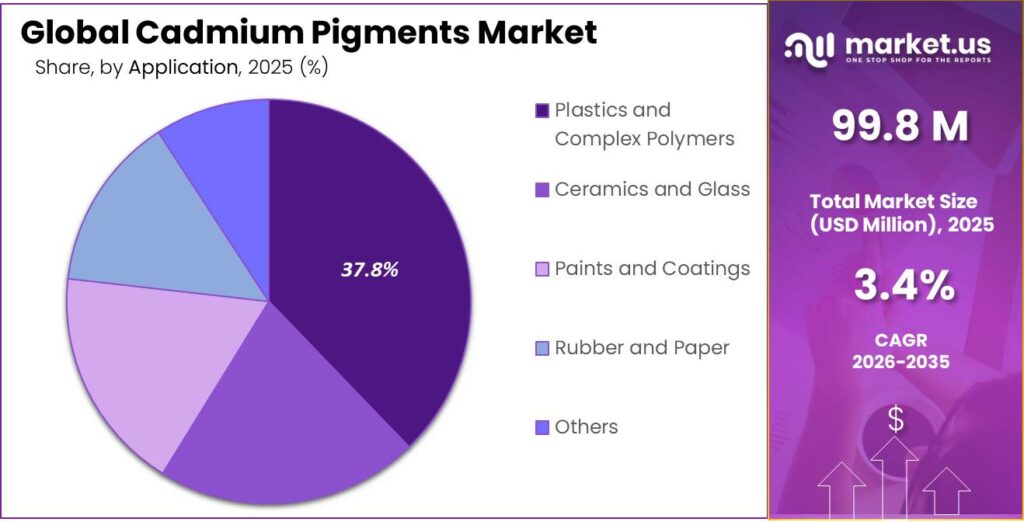

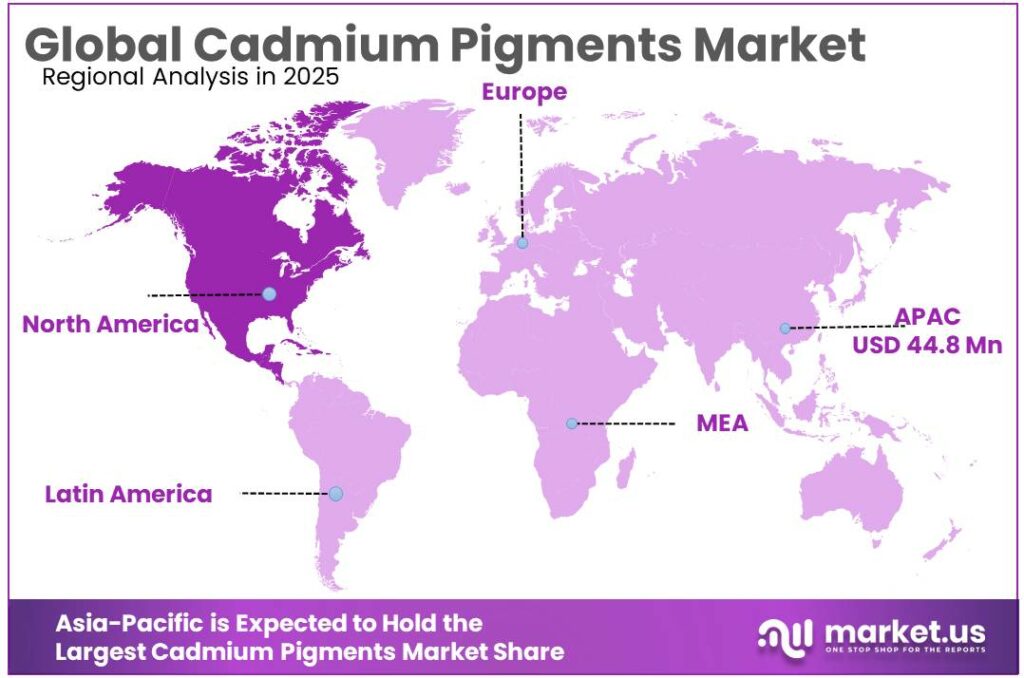

The Global Cadmium Pigments Market size is expected to be worth around USD 139.8 Million by 2035, from USD 99.8 Million in 2025, growing at a CAGR of 3.4% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 44.9% share, holding USD 44.8 Million revenue.

Cadmium pigments remain a specialized inorganic colorant segment, centered on cadmium sulfide and cadmium sulfoselenide chemistries that deliver bright yellow, orange, and red shades. Their industrial relevance is strongest where heat stability, opacity, lightfastness, and chemical resistance outweigh substitution pressure, especially in ceramics, glass enamels, coil coatings, powder coatings, road markings, and engineering plastics processed at or above 300°C; encapsulated systems can extend firing performance to above 900°C.

The industrial scenario is niche and regulation-led rather than mass-market. USGS’ 2025 data release covers 2020–2024 U.S. salient statistics and world production for cadmium, with the 2025 Mineral Commodity Summaries positioned as the earliest government source for 2024 mineral production data. China remained a key cadmium-refining base, with USGS 2026 estimates showing China at 8,900 metric tons in 2024 and 9,500 metric tons in 2025, while Japan was estimated at 1,580 metric tons in 2024 and 1,300 metric tons in 2025.

Demand is driven by technical necessity in applications where organic pigments may degrade under heat or repeated processing. The International Cadmium Association notes that cadmium pigments are used in industrial or professional supply chains, not direct consumer powder-pigment use, and highlights applications in ceramics, glass, enamels, coil coatings, powder coatings, road markings, and plastics. In the EU, cadmium use in several plastics, paint/varnish, jewellery and solder is restricted at 0.01% by weight, while EU RoHS keeps cadmium in electrical/electronic homogeneous materials to 0.01%.

Regulation is the central market-shaping factor. The EU classifies cadmium compounds under REACH restrictions, and ECHA identifies cadmium compounds as substances with restricted uses at EU level. Food-safety agencies reinforce the risk context: EFSA set cadmium’s tolerable weekly intake at 2.5 µg/kg body weight, while FAO/WHO JECFA established a provisional tolerable monthly intake of 25 µg/kg body weight because cadmium has a long biological half-life. OSHA also limits workplace airborne cadmium exposure to 5 µg/m³ as an 8-hour time-weighted average.

The main restraint is compliance. In the EU, finished plastic articles colored with cadmium are restricted where cadmium exceeds 0.01% by mass of plastic material, and RoHS also sets cadmium at 0.01% by weight in homogeneous electrical and electronic materials. This creates opportunity for suppliers that can document REACH compliance, controlled industrial use, encapsulated pigment performance, and safe handling systems.

Key Takeaways

- Cadmium Pigments Market size is expected to be worth around USD 139.8 Million by 2035, from USD 99.8 Million in 2025, growing at a CAGR of 3.4%.

- Cadmium Yellow held a dominant market position, capturing more than a 45.2% share.

- Plastics and Complex Polymers held a dominant market position, capturing more than a 37.8% share.

- Asia-Pacific emerged as the leading region in the cadmium pigments market, accounting for a dominant 44.9% share valued at 44.8 Mn.

By Pigment Type Analysis

Cadmium Yellow dominates with 45.2% due to its strong color performance and consistent demand across industries

In 2025, Cadmium Yellow held a dominant market position, capturing more than a 45.2% share. This leadership was mainly driven by its bright hue, excellent opacity, and long-lasting color stability, making it a preferred choice in applications such as plastics, coatings, and artists’ paints. Its ability to maintain color integrity even under high temperatures and exposure to light supported its steady demand throughout the year.

By Application Analysis

Plastics and Complex Polymers lead with 37.8% driven by strong use in durable and high-performance materials

In 2025, Plastics and Complex Polymers held a dominant market position, capturing more than a 37.8% share. This segment saw steady demand as cadmium pigments, especially for bright and stable coloring, are widely used in engineering plastics and specialty polymers. These materials often require pigments that can handle high processing temperatures without losing color strength, which supported consistent adoption during the year. Industries such as automotive, construction, and consumer goods continued to rely on these pigments for long-lasting color performance.

Key Market Segments

By Pigment Type

- Cadmium Red

- Cadmium Orange

- Cadmium Yellow

- Others

By Application

- Plastics and Complex Polymers

- Ceramics and Glass

- Paints and Coatings

- Rubber and Paper

- Others

Emerging Trends

Shift toward encapsulated and safer cadmium pigment technologies

One of the most noticeable trends in the cadmium pigments market is the shift toward safer and encapsulated pigment technologies. Manufacturers are no longer relying on traditional forms alone; instead, they are developing advanced versions that reduce environmental and health risks. Recent industry data shows that more than 25% of cadmium pigment products have already moved to encapsulated formats, helping to limit direct exposure while maintaining color quality.

This shift is closely linked to global safety concerns. Cadmium is a toxic heavy metal, and food safety bodies like the European Food Safety Authority have set strict intake limits of 2.5 µg per kg body weight per week, reinforcing the need for safer handling. Because of this, industries are investing in technologies that lock the cadmium inside stable structures, reducing the risk of leaching into the environment or food chain.

Growing focus on sustainability and reduced environmental exposure

Another major trend shaping the market is the increasing focus on sustainability and reducing environmental exposure to cadmium. Studies show that over 70% of cadmium intake comes through the food chain, mainly due to environmental contamination. This has made governments and industries more careful about how cadmium is produced, used, and disposed of.

Organizations like FAO and WHO have also set guidance levels for safe intake, suggesting that adults should not exceed around 0.4–0.5 mg per week, which highlights the need to control long-term exposure. Because of this, industries are now adopting cleaner production methods, better waste management systems, and recycling practices to reduce the release of cadmium into soil and water.

Drivers

Strong regulatory pressure shaping demand and application use

One of the biggest driving factors for cadmium pigments is the growing pressure from governments and food safety bodies to control heavy metals in consumer products. Cadmium is known to be toxic even at low levels, which is why strict exposure limits are in place globally. For example, the European Food Safety Authority has set a tolerable weekly intake of 2.5 μg per kg of body weight, highlighting how carefully cadmium exposure is monitored in food systems. At the same time, the Joint FAO/WHO Expert Committee on Food Additives allows a slightly higher provisional limit of 7 μg per kg body weight.

These limits directly influence industries using pigments, especially plastics, coatings, and packaging that may come into contact with food. Governments have also introduced strict packaging regulations—for instance, total heavy metals like cadmium must stay below 100 ppm, with actual measured levels often kept under 2 ppm in compliant materials.

Industrial demand remains strong due to unmatched performance properties

Even with strict regulations, cadmium pigments continue to see demand because of their unique performance, especially in industrial applications. These pigments are known for their brightness, heat resistance, and long-term color stability. In fact, around 2000 tonnes of cadmium per year is still used globally for pigment production, showing that the material remains relevant in specific sectors

Industries such as plastics, engineering polymers, and high-end coatings rely on these pigments because alternatives often cannot match their durability under extreme conditions. For example, cadmium pigments can withstand high processing temperatures and still maintain color strength, which is essential in automotive parts, construction materials, and specialty plastics.

Restraints

Strict health limits and food safety rules restrict cadmium use

One of the biggest restraining factors for cadmium pigments is the strict health limits set by global food and safety authorities. Cadmium is not just another industrial material—it is a toxic heavy metal that builds up in the human body over time. Because of this, organizations like the European Food Safety Authority have set very tight exposure limits. For example, the tolerable weekly intake is just 2.5 micrograms per kg of body weight, which shows how little of this substance is considered safe

In real life, this becomes a serious challenge for industries. Food regulations are getting stricter every year, with cadmium limits in food products ranging from as low as 0.005 mg/kg in baby foods to around 0.5 mg/kg in fruits and vegetables. Governments also keep updating these limits, forcing manufacturers to rethink materials used in packaging, coatings, and plastics.

Rising health concerns and exposure risks limit industrial adoption

Another major restraint comes from growing awareness of how cadmium affects human health. Studies show that food is the main source of cadmium exposure for most people, which makes regulators and industries even more cautious. In some regions, research has found that up to 31.2% of people can exceed the safe intake level based on their diet alone.

Global organizations like World Health Organization and FAO have also highlighted safe intake levels, suggesting adults should not exceed roughly 0.4–0.5 mg per week to avoid long-term health effects. Continuous exposure has been linked to kidney damage, bone problems, and even cancer risks in extreme cases.

Opportunity

Niche industrial demand creates space for controlled and high-value applications

A key growth opportunity for cadmium pigments lies in their continued use in niche industrial applications where performance matters more than volume. Despite restrictions, certain industries still depend on these pigments because of their ability to deliver bright colors, high heat resistance, and long-term stability. For example, global usage of cadmium in pigments is still estimated at around 2000 tonnes annually, showing that demand has not disappeared but shifted toward specialized areas.

Government regulations, especially in regions like Europe, now focus more on controlled use rather than a complete ban. This creates an opportunity for manufacturers to supply cadmium pigments in applications where exposure risk is minimal, such as high-performance plastics, aerospace coatings, and industrial equipment. These sectors value durability and precision, which many alternative pigments struggle to match. Strict food safety limits—like the 2.5 μg/kg body weight weekly intake set by the European Food Safety Authority—push companies to clearly separate food-related and non-food applications.

Technological improvements and safer handling practices support future growth

Another important opportunity comes from improvements in how cadmium pigments are produced and handled. Industries are investing in better encapsulation techniques and safer manufacturing processes to reduce environmental and health risks. This allows cadmium pigments to remain in use while staying within regulatory limits. In packaging and material safety rules, total heavy metal content is often required to stay below 100 ppm, with much lower levels targeted in practice.

Such regulations are pushing innovation rather than stopping production. Companies are now focusing on closed-loop systems, recycling methods, and improved waste management to meet government expectations. This shift is supported by environmental programs from agencies like the European Commission, which encourage safer chemical use without fully eliminating essential materials.

Regional Insights

Asia-Pacific dominates with 44.9% share valued at 44.8 Mn driven by strong industrial growth and manufacturing demand

Asia-Pacific emerged as the leading region in the cadmium pigments market, accounting for a dominant 44.9% share valued at 44.8 Mn. The region’s strong position is mainly supported by rapid industrialization and large-scale manufacturing activities across countries like China, India, and Japan. These countries have a high demand for cadmium pigments in plastics, coatings, and specialty materials, where durability and color stability are essential. The presence of expanding automotive, construction, and consumer goods sectors further supports consistent usage of these pigments in the region.

One of the key factors behind this dominance is the strong production base of plastics and polymers. Asia-Pacific alone contributes more than half of global plastics production, with countries like China leading the output, which directly increases the need for high-performance pigments in these materials. In addition, increasing investments in infrastructure and urban development are boosting demand for paints and coatings, where cadmium pigments are valued for their resistance to heat and fading.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Dalian Great Fortune Chemical Co., Ltd operates as a small-scale but active player in pigment and chemical supply. The company was established in 2013 and reports an annual revenue range of US$2.5 million to US$5 million, with a workforce of around 5–10 employees. It serves multiple regions including Europe, North America, and the Middle East.

Henan Kingway Chemicals, founded in 2001, has grown into a mid-scale exporter with a strong international presence across 30+ countries. The company employs around 101–200 people and records an annual export value between US$50 million and US$100 million

Huntsman Corporation stands out as a global leader with strong financial scale and global operations. Founded in 1970, the company generated approximately US$6 billion in revenue in 2023 and employs around 7,000 people across more than 25 countries. It operates over 60 manufacturing and R&D facilities worldwide. Through its pigments and additives business, Huntsman plays a major role in supplying high-performance materials for coatings, plastics, and industrial applications.

Top Key Players Outlook

- Dalian Great Fortune Chemical Co., Ltd

- Henan Kingway Chemicals

- Hunan Jufa Technology Co. Ltd

- Huntsman Corporation

- HUPC Chemical Co., Ltd

- James M. Brown Ltd

- Johnson Matthey

- Proquimac

- Rockwood Pigments NA Inc

- Sudarshan Chemical Industries Limited

Recent Industry Developments

In 2025/2026, Johnson Matthey is not mainly a cadmium pigment maker, but it is relevant to the wider pigment and specialty-chemical chain through its Catalyst Technologies business, which serves sectors including paints and chemical catalysts; this unit was first agreed for sale to Honeywell for £1.8 billion in 2025, later cut to £1.33 billion in 2026 after weaker unit profit performance. Company data in numbers: founded 1817, headquarters London, UK, 2025 revenue £11.67 billion, operating income £538 million, net income £373 million, and about 10,644 employees.

Proquimac operates as a specialty pigment solution provider, not a volume-driven global leader, but it holds a steady position by offering customized products and regulatory-compliant formulations aligned with EU standards. Company data in numbers: founded 1974/1975, headquarters Vacarisses, Barcelona, plant size ~2,500 sq. m + 700 sq. m offices, 4 business divisions, and 35+ pigment product listings including cadmium variants.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 99.8 Mn |

| Forecast Revenue (2035) | USD 139.8 Mn |

| CAGR (2026-2035) | 3.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Pigment Type (Cadmium Red, Cadmium Orange, Cadmium Yellow, Others), By Application (Plastics and Complex Polymers, Ceramics and Glass, Paints and Coatings, Rubber and Paper, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Dalian Great Fortune Chemical Co., Ltd, Henan Kingway Chemicals, Hunan Jufa Technology Co. Ltd, Huntsman Corporation, HUPC Chemical Co., Ltd, James M. Brown Ltd, Johnson Matthey, Proquimac, Rockwood Pigments NA Inc, Sudarshan Chemical Industries Limited |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |