Quick Navigation

Report Overview

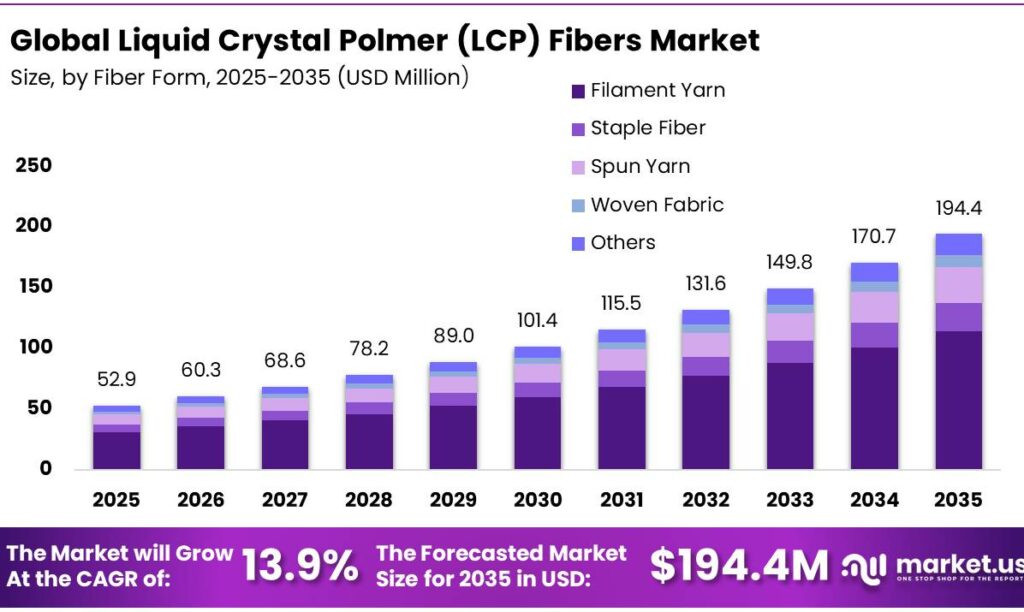

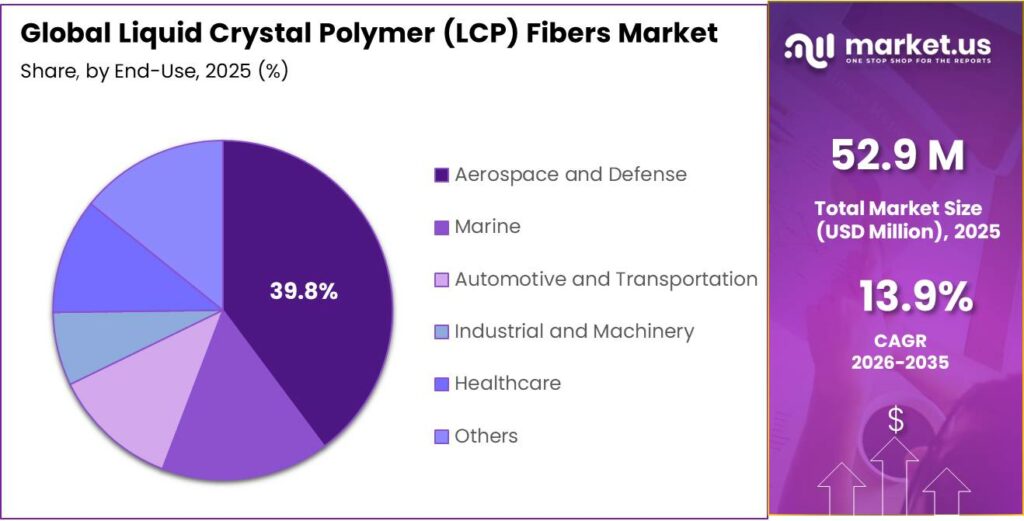

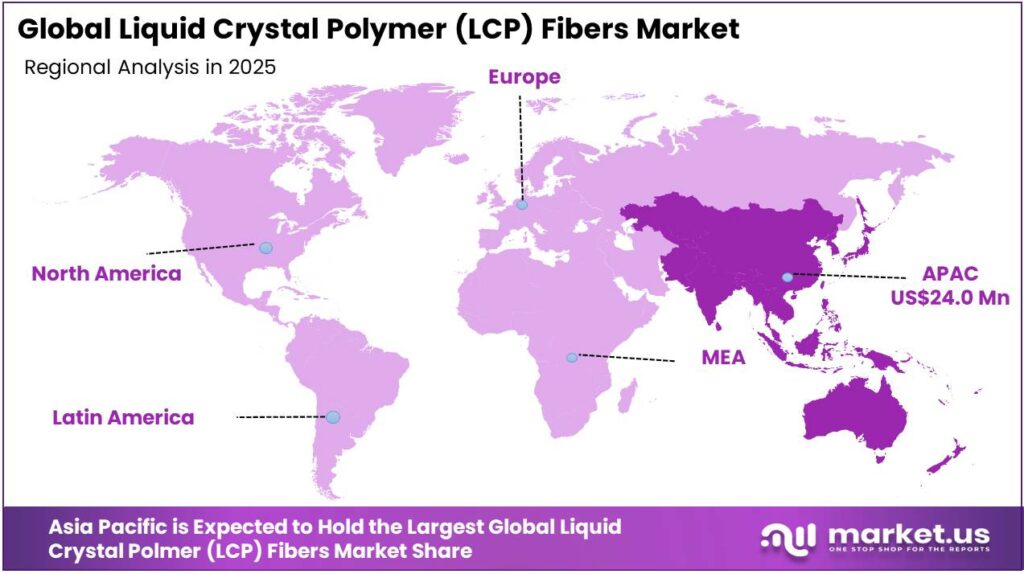

The Global Liquid Crystal Polymer (LCP) Fibers Market size is expected to be worth around USD 194.4 Million by 2035, from USD 52.9 Million in 2025, growing at a CAGR of 13.9% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 45.3% share, holding USD 24.0 Billion revenue.

Liquid crystal polymer (LCP) fibers are high-performance synthetic materials made from a unique class of aromatic polyesters that maintain a highly ordered molecular structure even when melted. This liquid crystal state allows the molecules to align themselves during processing, resulting in a self-reinforcing material with exceptional strength and stability. The market is defined by its focus on high-performance, niche applications where extreme mechanical, thermal, and dielectric properties are required.

LCP fibers exhibit high tensile strength, low creep, flame resistance, and stability at temperatures above 250-300°C, enabling use in aerospace, defense, and advanced electronics. Demand is structurally driven by sectors prioritizing performance over cost, particularly aerospace and defense systems, as well as emerging opportunities in 5G infrastructure and miniaturized electronic components requiring low dielectric loss and dimensional stability. Adoption in medical devices is increasing, supported by low moisture absorption of less than 0.04% and biocompatibility.

However, market expansion is constrained by complex manufacturing processes, high processing temperatures, limited raw material availability, and concentrated supply chains. Regionally, the Asia Pacific dominates due to integrated production ecosystems and strong electronics manufacturing bases. The market remains specialized, innovation-driven, and dependent on high-barrier, performance-critical applications.

Key Takeaways

- The global liquid crystal polymer (LCP) fibers market was valued at US$52.9 million in 2025.

- The global liquid crystal polymer (LCP) fibers market is projected to grow at a CAGR of 13.9% and is estimated to reach US$194.4 million by 2035.

- On the basis of fiber form, filament yarn dominated the market, constituting 58.9% of the total market share.

- Based on the grades, high-tenacity grade liquid crystal polymer led the market, comprising 43.7% of the total market.

- Among the end-uses, the aerospace and defense sector held a major share of the market, accounting for around 39.8% of the revenue.

- In 2025, the Asia Pacific was the most dominant region in the liquid crystal polymer (LCP) fibers market, accounting for 45.3% of the total global consumption.

Fiber Form Analysis

Filament Yarn Fibers are a Prominent Segment in the Market.

The market is segmented based on the fiber form into filament yarn, staple fiber, spun yarn, woven fabric, and others. The filament yarn fibers led the market, comprising 58.9% of the market share, as they provide continuous, high-strength filaments with uniform orientation, maximizing tensile strength, modulus, and dimensional stability, which are key performance attributes in aerospace, defense, and electronics applications. The continuous nature of filament yarn enables efficient load transfer, minimal creep, and consistent mechanical behavior under high-stress or high-temperature conditions, which are critical for structural reinforcements, cables, and high-performance composites.

In contrast, spun yarns consist of short staple fibers with more inter-fiber friction and less uniformity, reducing strength and reliability. Woven LCP fabrics or specialized coated fibers, while suitable for specific applications such as protective layers or flexible substrates, are less versatile and often involve additional processing steps. Filament yarn’s combination of continuous high strength, process efficiency, and adaptability across multiple high-performance applications drives its broader adoption relative to other LCP forms.

Grade Analysis

High-Tenacity Grade Liquid Crystal Polymer (LCP) Fibers Dominated the Market.

On the basis of grades, the liquid crystal polymer (LCP) fibers market is segmented into standard grade, high-tenacity grade, high thermal/chemical-resistance grade, and surface-treated/coated grade. The high-tenacity grade liquid crystal polymer (LCP) fibers dominated the market, comprising 43.7% of the market share, because they deliver the most broadly applicable performance attribute, which is load-bearing capability. Their tensile strength, typically more than 2.5-3 GPa, and high modulus directly address primary functional requirements in cables, ropes, reinforcement fabrics, and aerospace components, where mechanical integrity under stress is critical.

By contrast, high thermal/chemical-resistance grades serve narrower environments where exposure conditions justify specialized properties, while surface-treated or coated variants are application-specific, adding processing steps and cost without universal benefit. Standard grades, although less expensive, often fall short in demanding structural applications requiring minimal creep and high fatigue resistance.

End-Use Analysis

Liquid Crystal Polymer (LCP) Fibers Are Mostly Used in the Aerospace and Defense Sector.

Among the end-uses, 39.8% of the total global consumption of liquid crystal polymer (LCP) fibers is in the aerospace and defense sector, outperforming marine, automotive and transportation, industrial and machinery, healthcare, and other sectors, as their performance characteristics align with mission-critical requirements that outweigh cost and processing constraints. These fibers provide very high tensile strength, low creep, inherent flame resistance, and thermal stability above 250-300 °C, which are essential for aircraft structures, space systems, and military load-bearing applications operating under extreme stress, vibration, and temperature variation.

In contrast, automotive, industrial, and general machinery sectors prioritize cost efficiency and high-volume manufacturability, where lower-cost materials, such as polyamides, polyesters, or aramids, meet performance thresholds. Healthcare applications, while requiring biocompatibility and precision, typically use LCP in films or molded components rather than fibers due to design needs.

Key Market Segments

By Fiber Form

- Filament Yarn

- Staple Fiber

- Spun Yarn

- Woven Fabric

- Others

By Grade

- Standard Grade

- High-Tenacity Grade

- High Thermal/Chemical-Resistance Grade

- Surface-Treated/Coated Grade

By End-Use

- Aerospace and Defense

- Marine

- Automotive and Transportation

- Industrial and Machinery

- Healthcare

- Others

Drivers

Expansion of the Aerospace & Defense Sector Drives the Liquid Crystal Polymer (LCP) Fibers Market.

The expansion of the aerospace & defense sector serves as a primary driver for the liquid crystal polymer (LCP) fiber market, underpinned by requirements for extreme environmental resistance and lightweight structural components. LCP fibers exhibit high tensile strength, thermal stability, and low creep, enabling use in extreme-load and temperature environments typical of aerospace systems. These properties align with documented applications in rocket casings, antenna structures, and aircraft components where dimensional stability and non-flammability are required.

The aerospace-grade LCP fiber adoption has increased in defense applications. The program-level requirements, such as around 20% weight reduction targets in aircraft wiring harnesses, translate into material substitution toward high-modulus fibers, including LCP, in electrification initiatives.

LCP-based components have been deployed in space missions, such as cushioning systems for planetary landings, and in military load-bearing systems such as cargo tie-downs and tow ropes. The aerospace and defense expansion drives LCP fiber uptake through weight-efficiency mandates, extreme-environment tolerance requirements, and validated deployment in mission-critical systems.

Restraints

Production and Cost Barriers Might Hamper the Demand for the Liquid Crystal Polymer (LCP) Fibers.

Production and cost barriers materially constrain the adoption of liquid crystal polymer (LCP) fibers due to process complexity, input concentration, and capital intensity. Manufacturing requires precise melt-spinning under tightly controlled alignment conditions, with processing temperatures often exceeding 300°C and narrow operational windows, increasing defect risk and equipment specialization.

Cost structures are heavily skewed toward inputs and scale limitations. Resin precursors and catalysts account for 25-30% of total fiber cost, while production yields incur up to 5% losses from filament breakage during spinning. Raw material constraints are significant, such as limited availability of specialty monomers and concentrated supply chains, where the top producers control output, creating price volatility and supply risk. The high input costs, process inefficiencies, and concentrated supply collectively limit scalability and broader industrial penetration.

Opportunity

The 5G Infrastructure and the Electronics Industry Create Opportunities in the Liquid Crystal Polymer (LCP) Fibers Market.

Investments in 5G infrastructure and the electronics industry represent significant expansion opportunities for Liquid Crystal Polymer (LCP) fibers and resins, driven by the requirement for materials with specific dielectric properties suitable for high-frequency signal transmission. The transition to 5G millimeter-wave (mmWave) frequencies (24–100 GHz) necessitates materials that minimize signal attenuation. LCP exhibits a stable dielectric constant (Dk) of approximately 3.0 and a low dissipation factor (Df) of 0.004 across a broad range up to 110 GHz.

LCP’s low moisture absorption prevents dielectric degradation in humid environments, ensuring long-term reliability for outdoor 5G base stations. Similarly, with a coefficient of thermal expansion (CTE) comparable to copper, LCP enables the fabrication of high-density, multi-layer flexible printed circuits (FPCs) such as Murata’s MetroCirc.

The rollout of 5G drives demand for LCP in several key electronic sub-sectors. LCP is utilized in antenna-in-package (AiP) modules for smartphones, allowing for complex 3D wiring and a profile reduction compared to traditional glass-epoxy substrates. In 5G base stations, LCP is integrated into filters and housing to reduce weight and facilitate the integration of massive MIMO antenna arrays.

Manufacturers utilize LCP for sub-miniature connectors due to its high flow properties, allowing for wall thicknesses as thin as 0.1 mm while maintaining structural integrity during lead-free soldering processes exceeding 260°C. These technical attributes position LCP as a critical soft infrastructure material for global 5G network expansion.

Trends

Adoption in the Expanding Medical Equipment Sector.

Adoption of liquid crystal polymer (LCP) fibers in the expanding medical equipment sector is driven by material-specific performance requirements, particularly biocompatibility, sterilization tolerance, and miniaturization. LCP exhibits extremely low moisture absorption, significantly lower than polyimide and parylene-C, directly improving the long-term reliability of implantable devices in aqueous physiological environments.

LCP fibers are increasingly specified for neurovascular and cardiovascular catheters where thin-wall construction is critical. LCP fibers, such as Kuraray’s Vectran, provide a tensile strength of 3.2 GPa, approximately five times that of steel, allowing for smaller device profiles without sacrificing torque response or pushability. With moisture regain below 0.1% and a low coefficient of thermal expansion (CTE), LCP ensures consistent mechanical performance during high-precision surgical procedures.

Furthermore, a primary driver for LCP adoption is the demand for MRI-compatible diagnostic and interventional tools. LCP monofilaments, such as those developed by Zeus, serve as non-metallic braiding that eliminates antennas in MRI environments, reducing patient risk from induced currents and radiation exposure common in X-ray guided procedures. Medical-grade LCPs, including Celanese’s Vectra MT, are compliant with USP Class VI and ISO 10993 standards. They maintain structural integrity through repeated autoclaving, Gamma, and Ethylene Oxide (EtO) sterilization cycles.

Geopolitical Impact Analysis

Geopolitical Tensions Have Led to Severe Disruptions of the Supply Chains of Liquid Crystal Polymer (LCP) Fibers.

The geopolitical tensions are exerting measurable constraints on the liquid crystal polymer (LCP) fibers market through supply-chain fragmentation, trade restrictions, and raw material concentration risks. The European Commission Joint Research Centre identifies specialty polymers as dependent on critical raw materials with geographically concentrated production, heightening vulnerability to export controls and political disruptions.

Trade-policy frictions have translated into operational disruptions. The geopolitical realignments and regional sourcing shifts have increased lead times and logistics costs, while reducing consistency in material quality, directly affecting production efficiency for high-performance polymers such as LCP. A study by the Plastics Export Promotion Council noted that global politico-economic conditions have affected polymer exports, indicating the sensitivity of advanced materials to cross-border policy changes.

Moreover, the concentration risks are significant in the market. For instance, engineering plastics production exceeds 22 million tons annually in China, underscoring regional dominance in upstream supply chains relevant to LCP intermediates.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Liquid Crystal Polymer (LCP) Fibers Market.

In 2025, the Asia Pacific dominated the global liquid crystal polymer (LCP) fibers market, holding about 45.3% of the total global consumption, supported by integrated manufacturing ecosystems and dominant downstream industries. The market is anchored by its concentration of high-volume electronics manufacturing and significant capital expansions by regional producers. For instance, adoption is accelerated by China’s build-out of over 2.3 million 5G base stations as of late 2025, which utilizes LCP for low-loss high-frequency antenna substrates.

Similarly, in the region, major producers are actively increasing regional supply to meet recovering demand in the electronics and automotive sectors. In Japan, Sumitomo Chemical expanded its LCP capacity at the Ehime Works plant by 30% to address global supply tightening. Furthermore, in Taiwan, Polyplastics commenced operations at a new greenfield LCP plant in Kaohsiung in February 2025, adding 5,000 tons of annual capacity to establish an integrated production system. In China, Celanese completed the first phase of a greenfield LCP facility in 2024, with an installed capacity of 20,000 tons to serve the domestic electronics market.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of liquid crystal polymer (LCP) fibers focus on process optimization, application-specific innovation, and supply-chain control to strengthen competitive positioning. Companies emphasize refining melt-spinning and molecular alignment techniques to improve tensile strength, thermal stability, and yield consistency under high-temperature processing conditions.

Similarly, manufacturers prioritize miniaturization-compatible formats, such as ultra-fine filaments and flexible substrates, to align with electronics integration trends. Upstream integration and long-term sourcing agreements for specialty monomers are used to mitigate raw material volatility and ensure supply continuity. In parallel, firms invest in qualification and certification processes to secure entry into regulated, high-barrier applications.

The Major Players in The Industry

- Avient Corporation

- Celanese Corporation

- Kingfa Sci. and Tech Co., Ltd.

- Kuraray Co., Ltd.

- Polyplastics Co., Ltd.

- RTP Company

- SABIC

- Shanghai PRET Composites Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Syensqo

- Toray Industries, Inc.

- Ueno Fine Chemicals Industry, Ltd.

- Other Key Players

Key Development

- In May 2024, Celanese launched several new grades derived from former DuPont materials. Vectra/Zenite LCP ECO-B is a liquid crystal polymer produced using a mass-balance method, incorporating up to 60% renewable content. Zenite LCP 16236(N) is an ultra-high-flow, low-warpage LCP designed for miniaturized connector applications. It offers excellent flow for thin-wall designs while maintaining consistent dimensional stability.

- In June 2025, Polyplastics developed bio-based p-hydroxybenzoic acid (PHBA), a crucial raw material used in the production of its LAPEROS liquid crystal polymer (LCP). The company highlighted that this advancement supports its efforts toward more sustainable and environmentally friendly materials in high-performance applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$52.9 Bn |

| Forecast Revenue (2035) | US$104.4 Bn |

| CAGR (2026-2035) | 13.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Fiber Form (Filament Yarn, Staple Fiber, Spun Yarn, Woven Fabric, and Others), By Grade (Standard Grade, High-Tenacity Grade, High Thermal/Chemical-Resistance Grade, and Surface-Treated/Coated Grade), By End-Use (Aerospace and Defense, Marine, Automotive and Transportation, Industrial and Machinery, Healthcare, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Avient Corporation, Celanese Corporation, Kingfa Sci. and Tech Co., Ltd., Kuraray Co., Ltd., Polyplastics Co., Ltd., RTP Company, SABIC, Shanghai PRET Composites Co., Ltd., Sumitomo Chemical Co., Ltd., Syensqo, Toray Industries, Inc., Ueno Fine Chemicals Industry, Ltd., and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Fibers Market")