Quick Navigation

Report Overview

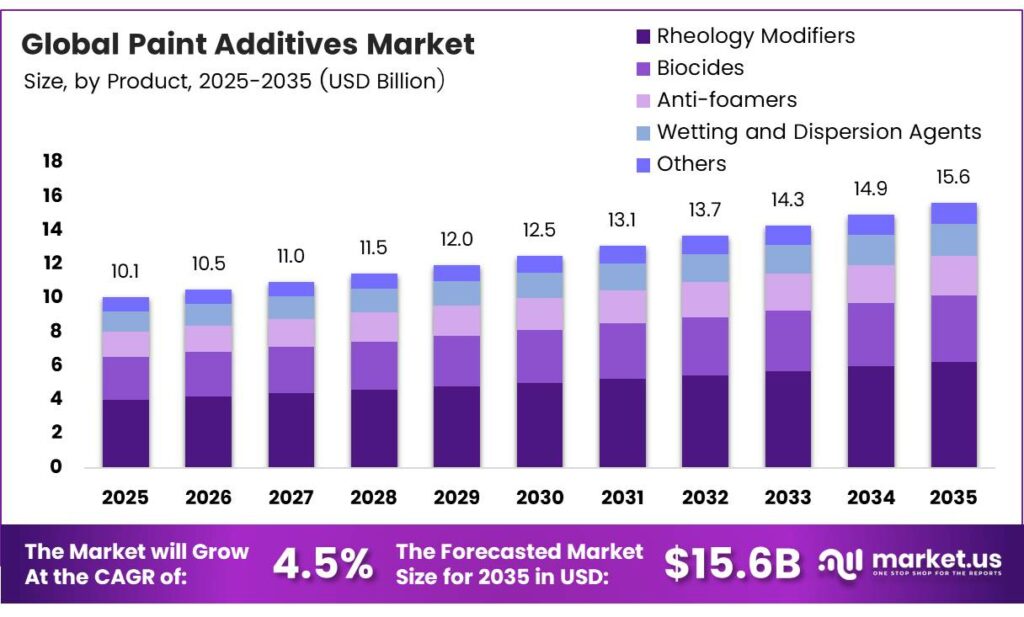

The Global Paint Additives Market size is expected to be worth around USD 15.6 billion by 2035 from USD 10.1 billion in 2025, growing at a CAGR of 4.5% during the forecast period 2026 to 2035.

Paint additives are specialty chemicals added to paint and coating formulations to improve performance, stability, and application properties. These compounds enhance characteristics such as flow, adhesion, durability, and microbial resistance. Manufacturers across industries rely on additives to meet specific performance standards and regulatory requirements.

Powder coating technology using dedicated flow, curing, and charge-control additives reduces 23.40 kg CO2 and 1.47 kg VOCs per vehicle compared with traditional solvent-based processes. This finding highlights the environmental value that advanced paint additives deliver in automotive applications.

Rheological additives in sealing and coating systems significantly improve the plugging performance of fly-ash-based sealing coatings, enhancing functional sealing efficiency. This demonstrates the critical technical role these additives play in infrastructure-grade coating performance.

Key Takeaways

- The Global Paint Additives Market is valued at USD 10.1 billion in 2025 and is projected to reach USD 15.6 billion by 2035 at a CAGR of 4.5% during the forecast period 2026 to 2035.

- Rheology Modifiers hold the dominant share at 32.8% in 2025.

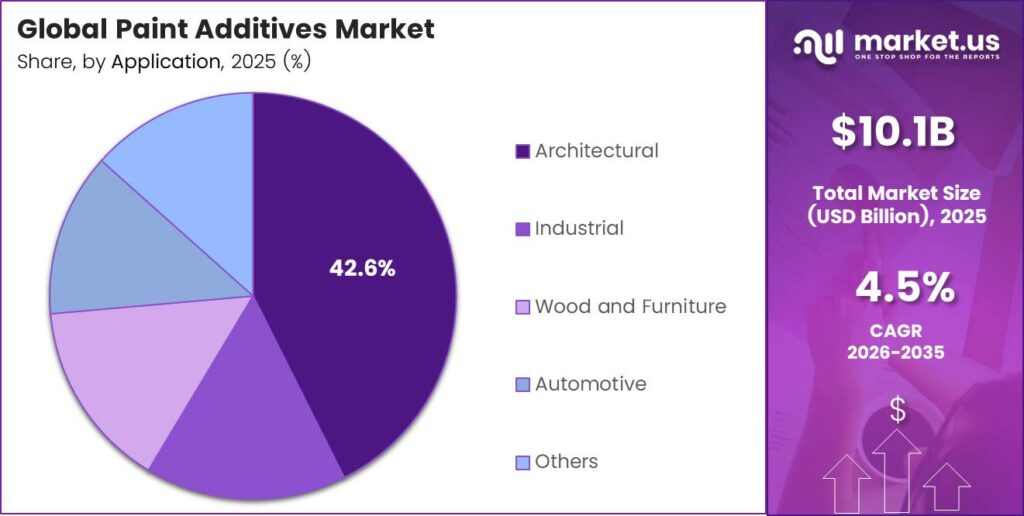

- Architectural leads the market with a 42.6% share in 2025.

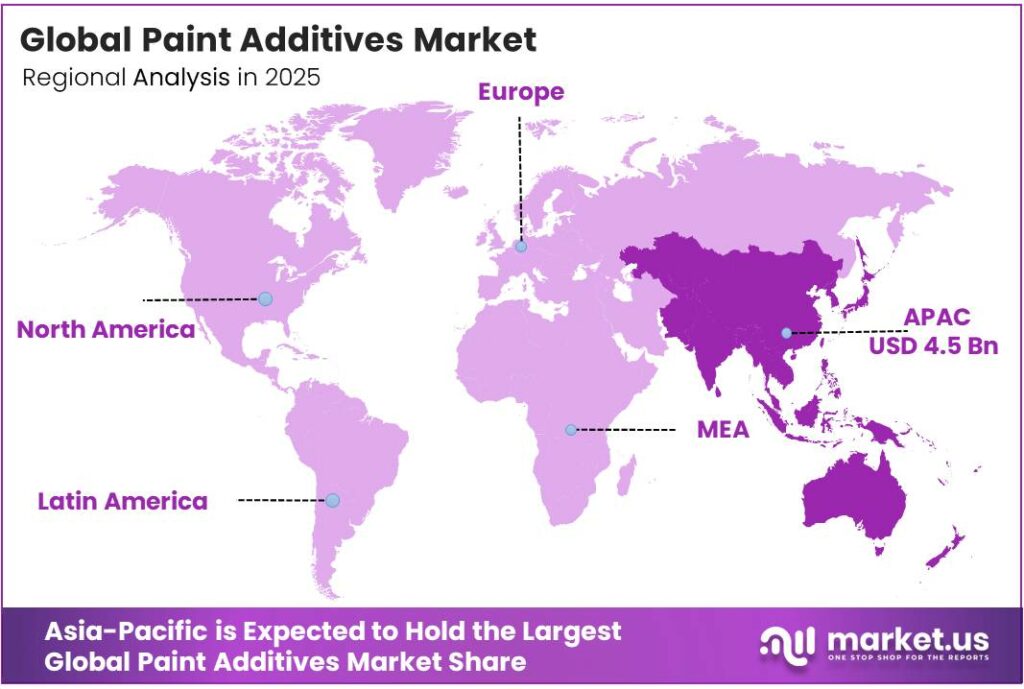

- Asia Pacific dominates the regional landscape, accounting for 44.2% of the global market, valued at approximately USD 4.5 billion.

By Product Analysis

Rheology Modifiers dominate with 32.8% due to their critical role in controlling paint flow, viscosity, and application consistency across industrial and architectural coatings.

In 2025, Rheology Modifiers held a dominant market position in the By Product segment of the Paint Additives Market, with a 32.8% share. These additives regulate viscosity and flow behavior, ensuring smooth and uniform paint application. Their use spans architectural, industrial, and automotive coatings, making them the most broadly applied additive category across global paint formulations.

Biocides serve an essential function by preventing microbial contamination in water-based paint systems. Manufacturers integrate biocides to protect both in-can stability and applied film integrity. Moreover, stricter hygiene standards in residential and commercial construction markets continue to support consistent demand for effective biocide-based preservation solutions.

Anti-foamers prevent foam generation during high-speed mixing and application of paint products. Foam-related defects reduce coating quality and surface finish. Therefore, formulators incorporate anti-foaming agents across water-based systems where air entrainment poses a significant production and performance challenge.

By Application Analysis

Architectural coatings dominate with 42.6% due to massive global construction activity and sustained residential and commercial infrastructure development.

In 2025, Architectural held a dominant market position in the By Application segment of the Paint Additives Market, with a 42.6% share. Urbanization in the Asia Pacific and Latin America drives continuous demand for interior and exterior paints. Moreover, increasing consumer preference for durable, low-VOC finishes in residential buildings further strengthens this segment’s leading position.

Industrial coatings represent a high-value application area requiring performance-grade additive packages. These coatings protect machinery, pipelines, and infrastructure from corrosion and chemical exposure. Consequently, industries such as oil and gas, marine, and heavy manufacturing maintain strong consumption of specialized additive-enhanced industrial coating systems.

Wood and Furniture coatings rely on additives for aesthetic quality and surface protection. Anti-foamers, wetting agents, and UV stabilizers improve the finish and longevity of wood-based products. Additionally, the global growth of premium furniture manufacturing and cabinetry sectors sustains demand for tailored additive solutions in this segment.

Key Market Segments

By Product

- Rheology Modifiers

- Biocides

- Anti-foamers

- Wetting and Dispersion Agents

- Others

By Application

- Architectural

- Industrial

- Wood and Furniture

- Automotive

- Others

Emerging Trends

Multifunctional Additives and Digital Color Technologies Transform Paint Formulation

Paint formulators increasingly adopt multifunctional additives that simultaneously enhance durability, aesthetics, and compatibility. Digital color technologies further improve additive integration accuracy during production. Adding 0.5 wt% modified mica nanosheets achieved an impedance of 3.29 × 10⁹ Ω·cm² after 28 days in saline conditions, demonstrating measurable corrosion protection gains from nano-additive inclusion.

Protective Coatings for Renewable Energy and Custom Formulation Solutions Gain Traction

Renewable energy infrastructure expansion creates growing demand for protective coatings with specialized additive requirements. Wind turbines and solar structures require coatings that resist moisture, UV exposure, and mechanical stress. Additionally, end-user industries increasingly request custom-formulated additive solutions tailored to specific performance criteria, driving innovation in flexible and application-specific coating systems.

Drivers

High-Performance Coating Demand and Urbanization Accelerate Additive Consumption

Automotive and industrial manufacturers drive rising demand for performance coatings that deliver durability, corrosion resistance, and regulatory compliance. A 10% reduction in electrocoat paint consumption through optimized additive packages decreases CO2 emissions by 0.40 kg per vehicle.

This result confirms that advanced additives deliver measurable environmental and efficiency benefits in automotive paint lines. Manufacturers given a 181-day compliance timeline under the 2025 EPA rule, actively reformulate products with new additive packages.

Construction Growth and Low-VOC Preferences Expand Market Reach

Urbanization across South and Southeast Asia fuels sustained construction activity, expanding demand for architectural and protective paint products. Developers and contractors increasingly specify low-VOC formulations to meet green building standards. Moreover, growing environmental awareness among consumers pushes paint brands to incorporate water-based and bio-based additives, broadening the addressable market for sustainable additive technologies.

Restraints

Stringent Environmental Regulations Restrict Certain Additive Chemistries

Regulatory bodies worldwide tighten restrictions on chemical additives in paint formulations. The 2025 aerosol coatings rule added 17 new compounds and reactivity factors to the regulatory framework, with the default reactivity factor for unlisted VOCs reset to 18.50 g O₃/g VOC. These changes require manufacturers to reformulate products within strict timelines, increasing compliance costs and limiting the commercial use of certain high-performance additive chemistries.

Raw Material Price Volatility Pressures Margins Across the Supply Chain

Paint additive manufacturers face ongoing challenges from unstable raw material prices. Petrochemical feedstock costs fluctuate due to geopolitical tensions, supply chain disruptions, and energy price changes. Consequently, producers struggle to maintain consistent profit margins while simultaneously investing in new formulation development. Smaller manufacturers face disproportionate pressure, limiting their capacity to absorb cost increases or compete on pricing.

Growth Factors

Nanotechnology and Smart Coatings Open High-Value Additive Opportunities

Nanotechnology-enabled additives deliver superior corrosion protection, barrier performance, and surface functionality. Its Rheovis coating-additive range now contains up to 35% biogenic content and delivers up to 30% lower product carbon footprint compared with fossil-based versions. This development reflects a broader industry shift toward sustainable, high-performance additive technologies that simultaneously meet environmental and functional performance targets.

Water-Based Additives and Developing Region Construction Drive Expansion

A 2025 polyurethane coating study demonstrated impedance of 1.8 × 10¹⁰ Ω·cm² after 28 days, four orders of magnitude higher than pure coating, confirming performance gains from advanced additive integration. Additionally, developing regions in Africa, Southeast Asia, and Latin America present significant untapped opportunities. Rising construction investment and infrastructure spending in these markets actively expand the customer base for water-based and bio-based additive product lines.

Regional Analysis

Asia Pacific Dominates the Paint Additives Market with a Market Share of 44.2%, Valued at USD 4.5 Billion

Asia Pacific leads the global paint additives market with a 44.2% share, valued at approximately USD 4.5 billion in 2025. Rapid urbanization in China, India, and Southeast Asia drives massive demand for architectural and industrial coatings. Moreover, expanding automotive production and infrastructure investment across the region generates consistent consumption of performance-grade additive formulations.

North America represents a mature and innovation-driven market for paint additives. Strong demand from automotive OEMs, aerospace, and industrial maintenance sectors supports steady additive consumption. Additionally, stringent EPA regulations and consumer preference for low-VOC formulations push manufacturers to invest in advanced bio-based and water-soluble additive chemistries across the region.

Europe maintains a strong demand for environmentally compliant paint additives driven by REACH regulations and green building standards. Germany, France, and the UK lead regional consumption in both architectural and industrial coating segments. Furthermore, European manufacturers actively invest in sustainable additive innovation, including bio-based rheology modifiers and low-emission dispersion agents for the construction sector.

Latin America presents a growing opportunity for paint additive suppliers as construction activity expands in Brazil and Mexico. Infrastructure development programs and rising residential housing demand fuel architectural coating consumption. However, economic volatility and import dependency for specialty chemicals create challenges for consistent additive supply and pricing stability across this region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

AkzoNobel N.V. operates as a global leader in paints, coatings, and specialty chemical solutions. The company maintains a strong portfolio of additive technologies designed for architectural, industrial, and decorative coating applications. Moreover, AkzoNobel actively invests in sustainable additive development, aligning its product strategy with global demand for low-VOC and environmentally compatible paint formulation systems.

Arkema develops a broad range of specialty additive solutions serving the coatings, adhesives, and construction industries. The company focuses on innovative rheology modifiers, surface agents, and polymer-based additives that enhance coating performance. Additionally, Arkema’s investment in bio-sourced and renewable raw materials positions it competitively in the growing market for sustainable and green additive technologies.

BASF SE holds a prominent position in the global paint additives industry through its comprehensive range of functional coating chemicals. The company’s additive product lines cover rheology control, wetting, dispersion, and preservation applications across multiple end-use sectors. BASF continues to drive innovation by integrating bio-based content into its core additive ranges, supporting customer sustainability goals across industrial and architectural coating markets.

The Dow Chemical Company delivers a wide portfolio of performance additives targeting rheology, adhesion, and film-forming properties in paint systems. Dow’s additive technologies serve formulators in the architectural, automotive, and industrial coating segments globally. The company’s expertise in polymer chemistry and surface science enables it to develop next-generation additive solutions for high-performance and environmentally driven coating applications.

Top Key Players in the Market

- AkzoNobel N.V.

- Arkema

- BASF SE

- The Dow Chemical Company

- Evonik Industries

- Ashland Global Holdings Inc.

- ANGUS Chemical Company

- Buckman Laboratories International, Inc.

- Cabot Corporation

- DAIKIN INDUSTRIES, Ltd.

- Eastman Chemical Company

- Elementis Specialties, Inc.

- Dynea Oy

- The Lubrizol Corporation

Recent Developments

- In 2025, AkzoNobel extended its long-term partnership with the McLaren Mastercard Formula 1 Team and expanded the collaboration to include McLaren’s new Hypercar Team in the FIA World Endurance Championship (WEC). The partnership emphasizes shared values in sustainability, technological innovation, and product development for performance coatings.

- In 2025, Arkema achieved a significant sustainability milestone with more than 70% of its global coating facilities now ISCC PLUS certified. This allows the company to offer a wide portfolio of bio-attributed products that demonstrate at least a 20% reduction in Product Carbon Footprint (PCF) compared to conventional fossil-based alternatives.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 10.1 Billion |

| Forecast Revenue (2035) | USD 15.6 Billion |

| CAGR (2026-2035) | 4.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Rheology Modifiers, Biocides, Anti-foamers, Wetting and Dispersion Agents, Others), By Application (Architectural, Industrial, Wood and Furniture, Automotive, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AkzoNobel N.V., Arkema, BASF SE, The Dow Chemical Company, Evonik Industries, Ashland Global Holdings Inc., ANGUS Chemical Company, Buckman Laboratories International, Inc., Cabot Corporation, DAIKIN INDUSTRIES Ltd., Eastman Chemical Company, Elementis Specialties Inc., Dynea Oy, The Lubrizol Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |