Quick Navigation

Report Overview

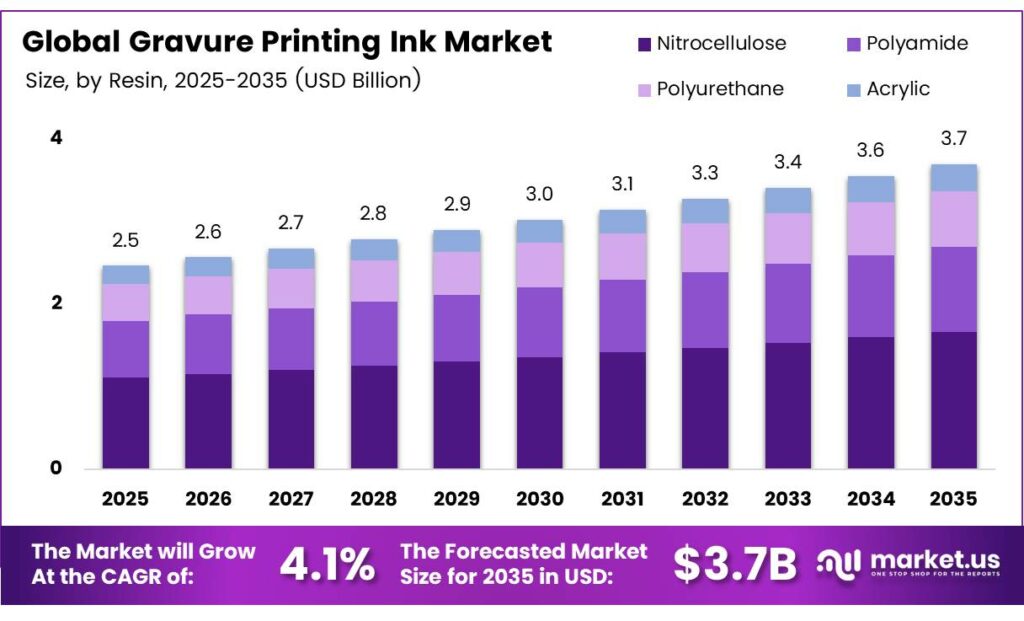

The Global Gravure Printing Ink Market size is expected to be worth around USD 3.7 billion by 2035 from USD 2.5 billion in 2025, growing at a CAGR of 4.1% during the forecast period 2026 to 2035.

Gravure printing inks are precision-formulated liquid colorants designed for the intaglio printing process, where ink transfers directly from engraved cylinders to the substrate. This mechanism delivers consistent, high-resolution output across high-speed runs. The technology serves packaging, publication, furniture, and specialty printing segments at an industrial scale.

Sustainability is reshaping ink chemistry. Water-based gravure ink reduced ink consumption per unit area by 20%–30%. This efficiency gain is not merely environmental — it translates directly into lower material costs per printed unit, creating a commercial case for adoption that runs parallel to regulatory pressure.

Solvent emission control is accelerating formulation shifts. Switching to water-based gravure inks cut workshop VOC concentration from 800 mg/m³ to below 100 mg/m³ — an 87.5% reduction. For ink manufacturers, this performance data reshapes buyer conversations from compliance cost to operational advantage.

Key Takeaways

- The Gravure Printing Ink Market is valued at USD 2.5 billion in 2025 and is forecast to reach USD 3.7 billion by 2035 at a CAGR of 4.1% over the forecast period 2026 to 2035.

- Nitrocellulose leads with a 45.9% market share in 2025.

- Solvent-Based inks hold a dominant 71.3% share, though Water-Based formulations are gaining ground.

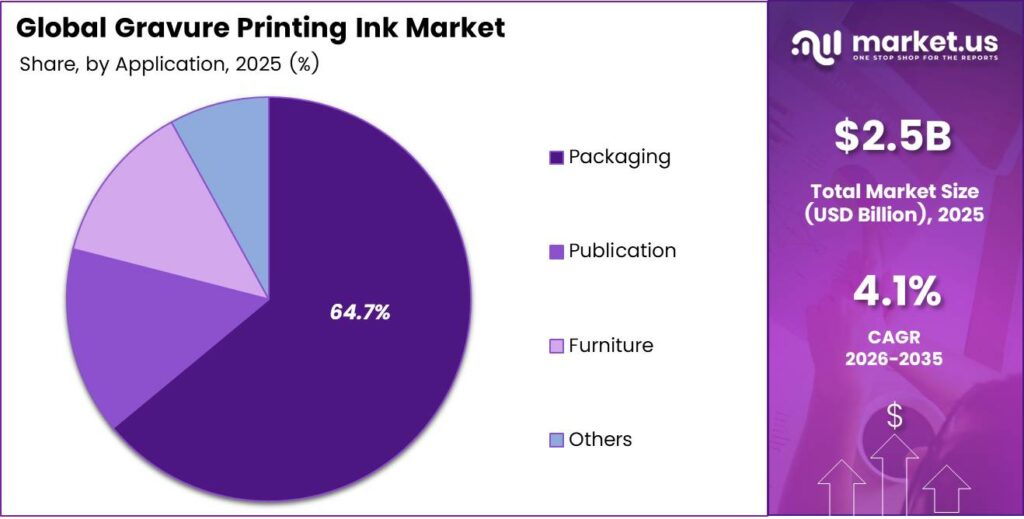

- Packaging commands the largest share at 64.7% of the total market demand.

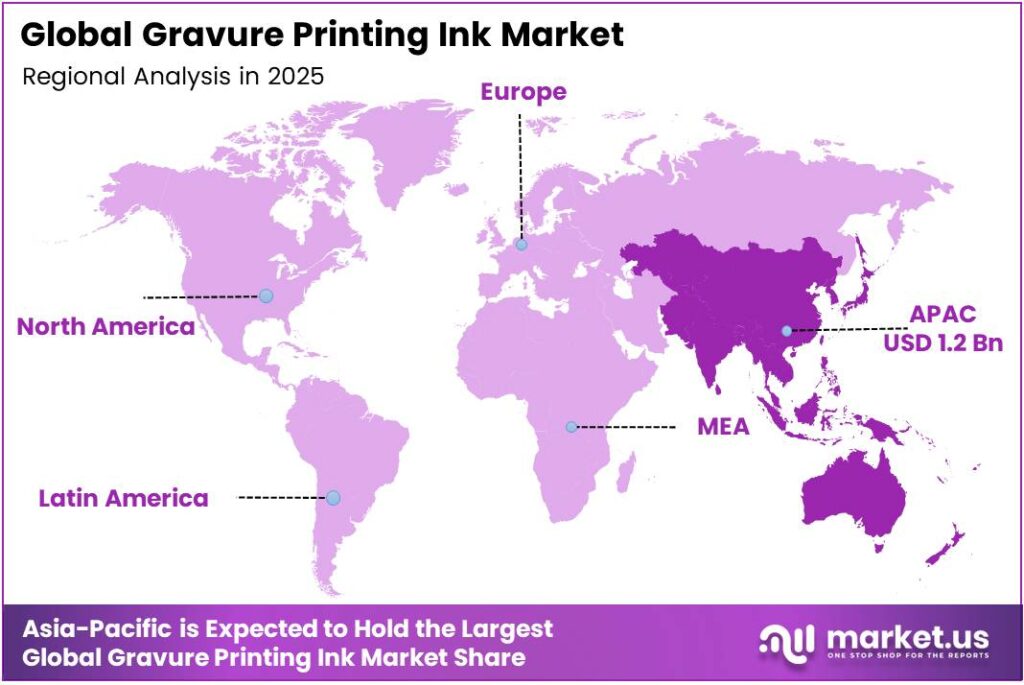

- Asia-Pacific dominates regional demand with a 48.5% share, valued at approximately USD 1.2 billion.

Product Analysis

Nitrocellulose dominates with 45.9% due to fast drying and broad substrate compatibility.

In 2025, Nitrocellulose held a dominant market position in the By Resin segment of the Gravure Printing Ink Market, with a 45.9% share. Its fast-drying characteristics and strong adhesion on flexible substrates make it the default choice for high-speed packaging lines. Converters select it because it minimizes production downtime and delivers consistent color density across long runs.

Polyamide serves as the preferred resin where heat resistance and inter-layer adhesion are non-negotiable. It performs reliably in lamination structures used in food packaging, where seal integrity matters more than cost. Converters running multi-layer flexible films typically specify polyamide to reduce delamination risk, making it structurally important despite its smaller volume share.

Technology Analysis

Solvent-Based dominates with 71.3% due to superior adhesion and high-speed press performance.

In 2025, Solvent-Based inks held a dominant market position in the By Technology segment of the Gravure Printing Ink Market, with a 71.3% share. Their dominance reflects decades of press optimization — solvent systems deliver fast drying, strong adhesion, and reliable color consistency at press speeds. Converters with legacy equipment configurations have limited incentive to switch without compliance pressure.

Water-Based gravure inks represent the fastest-shifting technology sub-segment, driven by VOC regulations in China, the EU, and North America. These formulations now meet previously impossible performance benchmarks — achieving surface drying in ≤2 seconds and full drying in seconds. Recommended VOC collection efficiency for upgraded gravure systems exceeds, making water-based inks a compliance-ready alternative for converters facing regulatory timelines.

Application Analysis

Packaging dominates with 64.7% due to high-volume flexible film printing requirements.

In 2025, Packaging held a dominant market position in the By Application segment of the Gravure Printing Ink Market, with a 64.7% share. Food, beverage, and pharmaceutical manufacturers require consistent, high-resolution print on flexible substrates at volumes that only gravure technology handles economically. This dependency locks the demand for packaged goods into output cycles globally.

Publication printing uses gravure for high-circulation magazines, catalogues, and direct mail formats where color fidelity and throughput justify the cylinder cost. However, digital substitution in publishing reduces long-run print volumes, which constrains this segment’s contribution to overall ink demand. Consequently, the publication’s share faces structural pressure as digital media consumption displaces physical print.

Furniture printing applies gravure technology to decorative paper and foil laminates used in wood-effect panels, flooring, and surface coverings. This segment benefits from residential construction activity and interior design refresh cycles. Moreover, gravure’s ability to replicate wood grain and texture at high resolution gives it a technical advantage over alternative printing methods in this application.

Key Market Segments

By Resin

- Nitrocellulose

- Polyamide

- Polyurethane

- Acrylic

By Technology

- Solvent-Based

- Water-Based

By Application

- Packaging

- Publication

- Furniture

- Others

Emerging Trends

Water-Based and UV-Curable Ink Systems Redefine Gravure Performance Standards

The gravure ink sector is moving away from solvent-heavy systems toward water-based and UV-curable formulations. This shift is not driven by preference — it is driven by tightening VOC regulations in China, the EU, and North America. Water-based gravure ink for BOPP film recorded 16.1% VOC content, well below China’s regulatory ceiling of ≤30%.

Automation and digital press controls now accompany this chemistry shift. Converters adopting automated gravure systems improve dot reproduction consistency — achieving 50% dot enlargement rates of ≤15%. This level of precision reduces press waste and supports the high-definition graphics that brand owners demand on consumer packaging in competitive retail environments.

Recyclable and sustainable packaging materials are reshaping ink specification criteria. Brand owners increasingly require inks that do not compromise substrate recyclability. This forces gravure ink formulators to develop systems compatible with mono-material flexible packaging — a design direction that is accelerating across fast-moving consumer goods categories globally.

Drivers

Flexible Packaging Growth and Superior Print Efficiency Cement Gravure Ink Demand

Flexible packaging demand across the food, beverage, and pharmaceutical sectors directly drives gravure ink consumption. These industries require high-resolution, high-volume printing on barrier films — a combination that gravure delivers more efficiently than any competing print process. E-commerce growth compounds this effect by raising branded packaging volumes across direct-to-consumer supply chains.

Gravure’s press efficiency is a core commercial driver. High-speed production at over 300 m/min reduces per-unit print costs for converters running large orders. Regenerative thermal oxidizers achieved over 90% VOC removal efficiency in printing operations — enabling solvent-based ink users to maintain speed advantages while meeting emission compliance requirements.

The adoption of low-VOC gravure ink formulations further strengthens the market’s structural position. Rather than forcing converters to abandon gravure, compliance pressure is pushing ink innovation — expanding the addressable customer base to include facilities operating under strict environmental permits. This dynamic widens the commercial opportunity for ink suppliers with advanced formulation capabilities.

Restraints

High Equipment Costs and Solvent Emission Regulations Create Entry and Operating Barriers

Gravure printing equipment carries high upfront capital costs and requires continuous maintenance investment. Cylinder engraving alone adds significant pre-press expenditure per job, making gravure economically viable only for long print runs. Shorter-run buyers migrate toward flexographic or digital alternatives, which limits new customer acquisition for gravure ink suppliers.

Solvent-based inks — which hold 71.3% technology share — face tightening regulatory constraints. 68% of printing enterprises relied on granular activated carbon for VOC treatment, achieving only 40%–75% removal efficiency. This performance gap means many facilities still fall short of regulatory thresholds, creating compliance liability and upgrade cost pressure for converters.

The compliance cost burden disproportionately affects small and mid-sized converters who lack the capital to invest in advanced abatement systems or reformulate to water-based inks. This fragmentation slows sector-wide adoption of cleaner gravure processes and keeps a portion of the market in regulatory risk — making large, well-capitalized converters the primary beneficiaries of formulation innovation.

Growth Factors

Bio-Based Ink Development and Smart Packaging Integration Open New Revenue Layers

Bio-based and eco-friendly gravure ink formulations represent a commercially validated growth direction. Formulators who develop plant-derived resin systems can access brand owner sustainability commitments — particularly in food packaging, where consumer-facing claims about packaging materials directly influence procurement decisions. This creates a price premium opportunity for suppliers with certified bio-based ink portfolios.

Improved ink formulations are delivering measurable operational gains. Product rejection rates decreased from 5% to below 2% after converters adopted improved gravure ink formulations. For buyers, this 3-percentage-point quality improvement translates directly into lower material waste costs — a quantifiable ROI that justifies switching from legacy ink systems.

Smart packaging and functional printing applications are creating entirely new demand layers for gravure ink. QR-enabled packaging, conductive inks for RFID integration, and temperature-sensitive inks require gravure’s precision and consistency. Developing economies with expanding middle-class consumer goods sectors add further volume, as packaged goods penetration rises and local converters invest in gravure capacity.

Regional Analysis

Asia-Pacific Dominates the Gravure Printing Ink Market with a Market Share of 48.5%, Valued at USD 1.2 Billion

Asia-Pacific commands 48.5% of the global gravure printing ink market, valued at approximately USD 1.2 billion. China, India, and Southeast Asia house the world’s highest concentration of flexible packaging converters. This manufacturing density, combined with rapid growth in packaged food and pharmaceutical output, makes the region the structural anchor of global gravure ink demand.

North America maintains a mature but stable gravure ink market, supported by large-scale food and beverage packaging operations. Regulatory pressure from EPA VOC standards drives formulation investment toward low-emission and water-based systems. Converters in this region prioritize ink suppliers who can demonstrate both performance compliance and supply chain reliability at scale.

Europe’s gravure ink demand is shaped by the EU’s stringent packaging and chemical regulations, including REACH and the Packaging and Packaging Waste Regulation. These frameworks accelerate converter adoption of water-based and UV-curable inks. Germany, Italy, and France lead regional consumption, driven by their established printing and packaging manufacturing sectors.

Latin America represents an underpenetrated but commercially active gravure ink market. Brazil and Mexico anchor regional demand through their food and personal care packaging industries. Local converter capacity is expanding as multinational consumer goods brands increase production presence, creating consistent volume demand for gravure-quality flexible packaging print.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

CHEMICOAT positions itself as a specialty gravure ink supplier with formulations tailored for flexible packaging substrates. Its competitive advantage lies in customized ink chemistry for specific film types, allowing converters to reduce press adjustments and improve run efficiency. This specialization strategy targets mid-sized converters who require application-specific solutions rather than commodity ink supply.

Flint Group Italia s.r.l operates within the broader Flint Group global network, giving it access to R&D investment and supply chain scale that independent competitors cannot match. Its Italian base positions it to serve European converters navigating strict REACH and VOC compliance requirements. This regulatory expertise translates into a consultative sales advantage over purely product-led competitors.

Mac-Mixu Coating and Chemicals addresses the price-sensitive converter segment with cost-competitive gravure ink formulations. Its market positioning captures converters operating on thin margins where ink cost per unit area directly affects profitability. However, this positioning creates exposure to margin pressure as water-based ink adoption raises formulation complexity and production costs across the industry.

MITSU Inks Pvt. Ltd. leverages its India base to serve the rapidly expanding domestic flexible packaging sector. India’s packaged food and pharmaceutical industries are expanding converter capacity at a pace, and MITSU’s local manufacturing gives it a logistics and turnaround advantage over multinational suppliers. This geographic positioning makes it a key beneficiary of the Asia-Pacific’s structural role in global gravure ink demand.

Key Players

- CHEMICOAT

- Flint Group Italia s.r.l

- Mac-Mixu Coating and Chemicals

- MITSU Inks Pvt. Ltd.

- Siegwerk Druckfarben AG

- Skata Inks Ltd.

- Sun Chemical

- Technocrafts India Pvt. Ltd.

- VirBandhu Industries

- Worldtex Specialty Chemicals

Recent Developments

- In 2025, Flint Group Italia s.r.l expanded resin production at Caronno, Italy, increasing capacity for NC-free PU/acrylic ink intermediates, supporting MatrixCode gravure and VertixCode flexo inks for recyclable flexible packaging. Price increase across packaging inks/coatings due to cost pressures from the Middle East conflict.

- In 2025, Siegwerk Druckfarben AG signed a definitive agreement to acquire Hi-Tech Inks, an Indian producer of flexographic and gravure printing inks; the combined Indian flexible-packaging business was expected to exceed 20% share and add Vapi/Bhiwadi capacity and showcase newer ink/coating developments for labels/packaging and sustainable coatings at Labelexpo Europe and Paperex.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.5 Billion |

| Forecast Revenue (2035) | USD 3.7 Billion |

| CAGR (2026-2035) | 4.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Resin (Nitrocellulose, Polyamide, Polyurethane, Acrylic), By Technology (Solvent-Based, Water-Based), By Application (Packaging, Publication, Furniture, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | CHEMICOAT, Flint Group Italia s.r.l, Mac-Mixu Coating and Chemicals, MITSU Inks Pvt. Ltd., Siegwerk Druckfarben AG, Skata Inks Ltd., Sun Chemical, Technocrafts India Pvt. Ltd., VirBandhu Industries, Worldtex Speciality Chemicals |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |