Global Produced Water Treatment Market By Type (Physical Treatment, Chemical Treatment, and Biological Treatment), By Application (Onshore and Offshore), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 185282

- Number of Pages: 215

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

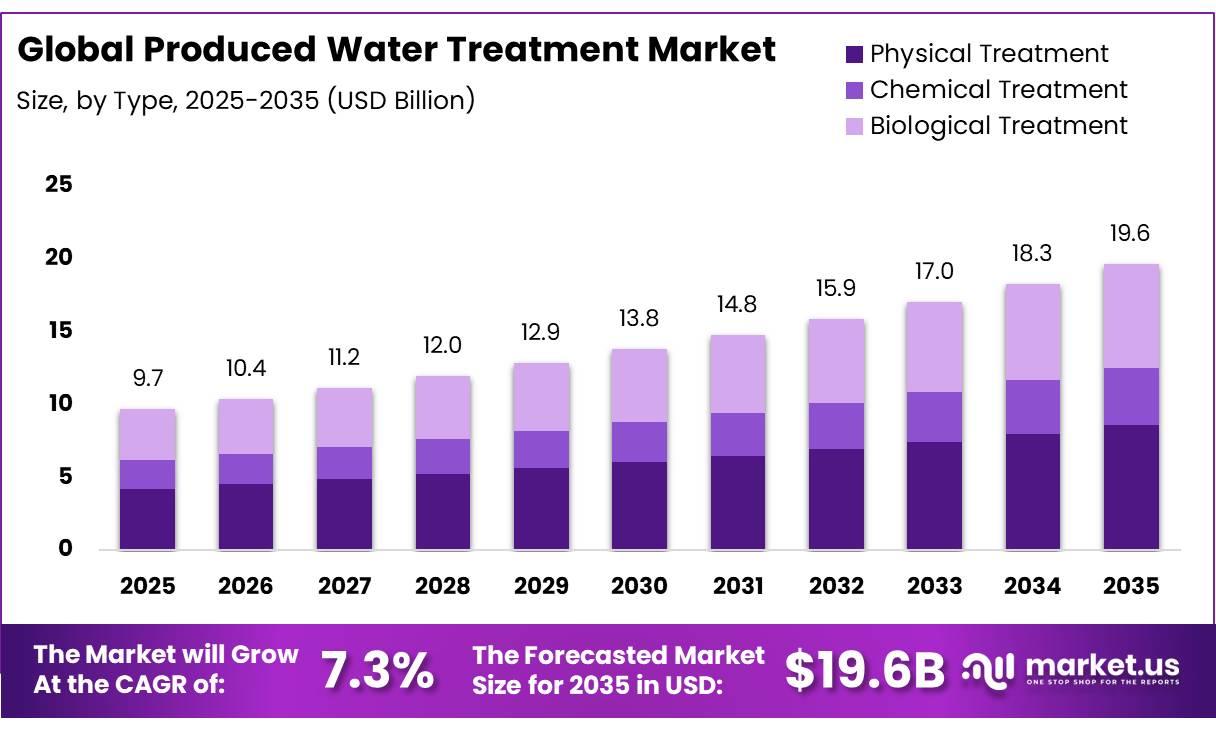

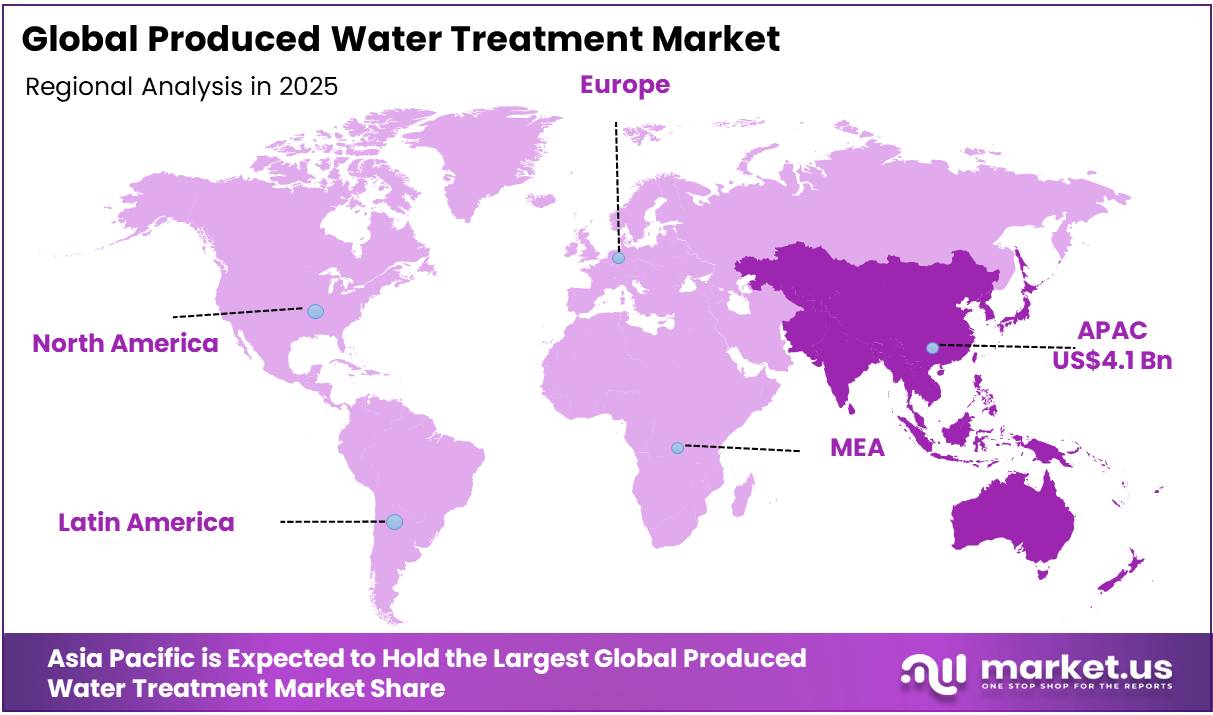

The Global Produced Water Treatment Market size is expected to be worth around USD 19.6 Billion by 2035, from USD 9.7 Billion in 2025, growing at a CAGR of 7.3% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 41.9% share, holding USD 4.1 Billion revenue.

Produced water treatment is the process of removing contaminants from water that is brought to the surface as a byproduct during oil and gas extraction. Produced water, often exceeding oil volumes in mature fields, contains dispersed hydrocarbons, dissolved minerals and heavy metals, high salinity (frequently more than 200,000 mg/L TDS), and complex contaminants, necessitating multi-stage treatment.

The produced water treatment market is structurally driven by regulatory compliance, operational constraints, and evolving technology adoption across oil and gas systems. Regulatory frameworks enforced by bodies such as the U.S. Environmental Protection Agency and the OSPAR Commission impose strict discharge limits, such as 30 mg/L oil-in-water, making treatment a compliance requirement.

Physical treatment methods dominate due to reliability and cost efficiency, while chemical and biological processes are used selectively. Onshore applications account for most treatment activity, supported by infrastructure and stricter disposal constraints, whereas offshore systems prioritize compact, high-efficiency technologies. Key market dynamics include high treatment costs relative to disposal, increasing digitalization and automation, and regional concentration in the Asia Pacific due to mature fields and offshore production.

Key Takeaways

- The global produced water treatment market was valued at USD 9.7 billion in 2025.

- The global produced water treatment market is projected to grow at a CAGR of 7.3% and is estimated to reach USD 19.6 billion by 2035.

- Based on the types of produced water treatment, physical treatment dominated the market, with a market share of around 43.8%.

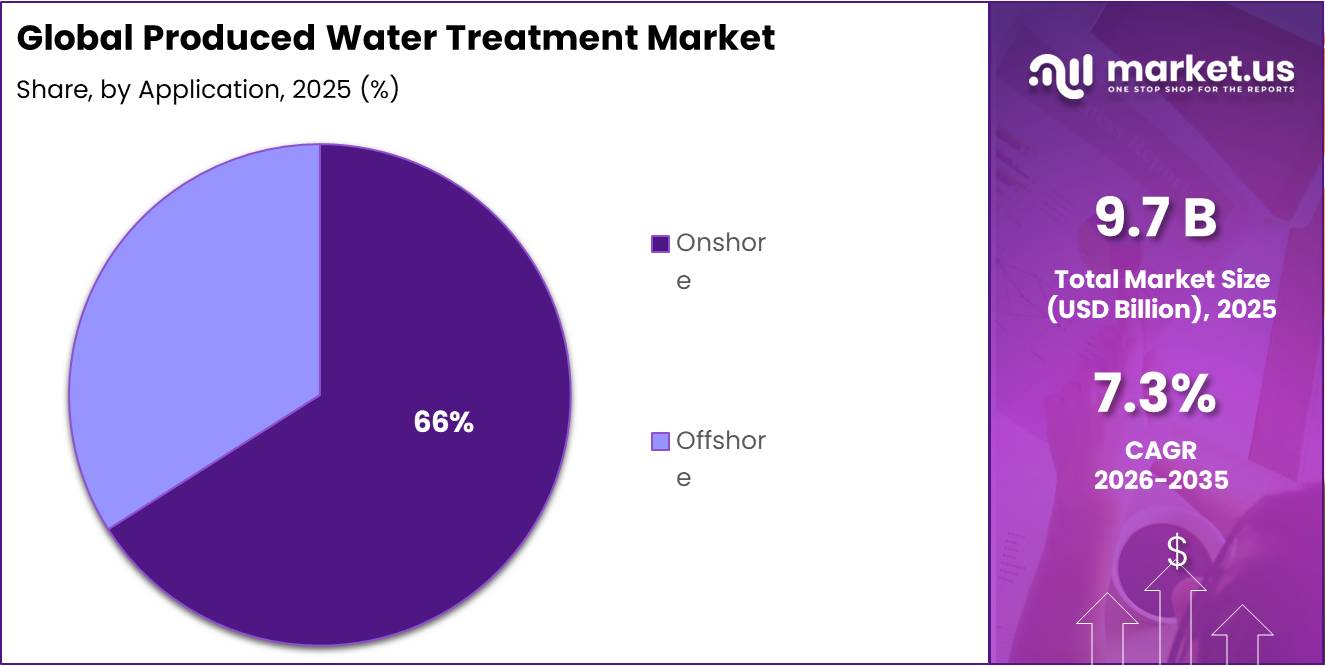

- Among the applications of produced water treatment, onshore applications held a major share in the market, 65.9% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the produced water treatment market, accounting for around 41.9% of the total global consumption.

Type Analysis

Physical Treatment Held the Largest Share in the Produced Water Treatment Market.

The produced water treatment market is segmented based on type into physical treatment, chemical treatment, and biological treatment. The physical treatment dominated the produced water treatment market, comprising around 43.8% of the market share, as it aligns with operational, regulatory, and fluid characteristics typical of oil and gas systems. Produced water often contains dispersed oil droplets and suspended solids, which can be efficiently removed using gravity separation, hydrocyclones, and filtration without altering water chemistry.

Unlike chemical treatment, they avoid reagent handling, sludge generation, and dosing variability. Additionally, space and weight constraints on offshore platforms favor compact mechanical systems over multi-stage biological units. Consequently, physical processes serve as the primary and often indispensable first-stage treatment in most produced water management systems.

Application Analysis

Produced Water Treatment is Mostly Utilized in Onshore Applications.

Based on the applications of produced water treatment, the market is divided into onshore and offshore. The onshore applications dominated the produced water treatment market, with a market share of 65.9%, as disposal pathways, infrastructure availability, and operational flexibility differ materially from offshore settings. Onshore operations generate large volumes of produced water and often face restricted discharge options, requiring treatment prior to reuse or disposal. In the United States, regulations under frameworks such as the U.S. Environmental Protection Agency prohibit the discharge of wastewater from many onshore unconventional operations to surface systems, necessitating treatment or reinjection.

Onshore environments further allow space-intensive, multi-stage treatment systems, which are impractical offshore due to footprint and weight constraints. Additionally, extensive pipeline and trucking networks enable centralized treatment facilities handling high throughputs. In contrast, offshore platforms typically rely on direct discharge after primary treatment within regulated limits or reinjection, reducing the need for complex systems.

Key Market Segments

By Type

- Physical Treatment

- Filtration

- Flotation

- Others

- Chemical Treatment

- Precipitation

- Oxidation

- Others

- Biological Treatment

By Application

- Onshore

- Offshore

Drivers

Stringent Environmental Regulations Drive the Produced Water Treatment Market.

Stringent environmental regulations constitute a primary structural driver of produced water treatment deployment by directly constraining discharge pathways and mandating contaminant removal. Produced water is the largest wastewater stream in oil and gas extraction, with water-to-oil ratios exceeding 10:1 in some formations, amplifying regulatory exposure. Regulatory frameworks impose quantitative discharge limits and, in some cases, outright prohibitions.

For instance, the U.S. effluent guidelines (40 CFR 435) prohibit the discharge of wastewater pollutants from onshore unconventional operations to publicly owned treatment works, forcing on-site treatment or reinjection. For offshore discharges, the oil and grease content is restricted to a daily maximum of 42 mg/l, with a 30-day average not to exceed 29 mg/l for new sources.

Similarly, under Subpart E (Agricultural and Wildlife Water Use), the daily maximum for oil and grease is capped at 35 mg/l. In Texas, the Railroad Commission (RRC) Chapter 4 rules mandate that produced water recycling pits maintain a freeboard of at least two feet plus capacity for a 25-year, 24-hour rainfall event to prevent environmental contamination. The binding discharge limits, prohibition regimes, and contaminant diversity institutionalize treatment as a compliance requirement rather than an operational choice.

Restraints

High Costs & Economic Viability Might Hamper the Demand for Produced Water Treatment.

High capital expenditures (CAPEX) and operational expenses (OPEX) remain the primary structural barriers to the widespread adoption of advanced produced water treatment, particularly for beneficial reuse outside the oilfield. The economic challenge is rooted in the extreme salinity of produced water, often exceeding 100,000 mg/L of total dissolved solids (TDS). Data from the Texas Produced Water Consortium (TXPWC) 2024 pilot studies indicate that achieving high-purity water of less than 500mg/L TDS requires multi-stage treatment trains involving pre-treatment, advanced membrane desalination, and post-treatment.

While low-hanging fruit recycling for hydraulic fracturing is economically feasible as it avoids disposal costs, the infrastructure for broader reuse faces a significant funding gap. The U.S. EPA’s 2024 assessment estimated national wastewater infrastructure needs at US$630 billion, a 45% increase since 2016, driven by inflation and supply chain disruptions.

Consequently, despite regulatory pressure, operators often prioritize lower-cost disposal pathways, indicating that economic thresholds, rather than technical feasibility, remain the binding constraint on broader treatment deployment.

Opportunity

Offshore Technology Demands Create Opportunities in the Market.

Offshore technology requirements create a distinct opportunity for produced water treatment by imposing space, performance, and discharge constraints that necessitate advanced, high-efficiency systems. Offshore production accounts for about 30% of global oil output, with produced water volumes rising per day globally, intensifying treatment demand at sea-based facilities.

The discharge regimes are quantitatively stringent and technology-forcing. For instance, offshore frameworks such as OSPAR require oil-in-water concentrations to be reduced to less than or equal to 30 mg/L, necessitating high-performance separation and polishing technologies beyond conventional hydrocyclones.

The offshore platforms face limited footprint, weight restrictions, and automation requirements, compelling the adoption of compact, modular, and low-maintenance systems. Multi-stage configurations integrating flotation, membranes, and chemical treatment are therefore standard to handle complex mixtures of hydrocarbons, metals, and dissolved organics. Environmental exposure further reinforces demand. The high-volume generation, strict discharge thresholds, and platform constraints institutionalize advanced offshore treatment technologies as a necessary operational capability.

Trends

Adoption of Digitalization and Artificial Intelligence.

The adoption of digitalization and artificial intelligence (AI) is emerging as a structural trend in produced water treatment, driven by the need to manage high data volumes, process variability, and compliance constraints. Oil and gas operations generate continuous real-time data streams from sensors and SCADA systems that exceed manual processing capacity, necessitating algorithmic control and analytics.

AI-enabled systems facilitate real-time process optimization, dynamically adjusting parameters such as chemical dosing, flow rates, and treatment sequencing, improving operational stability under variable water chemistries. Predictive models further enhance system performance by forecasting water quality and equipment behavior, enabling pre-emptive adjustments and reducing unplanned downtime.

The produced water streams can reach water-to-oil ratios of 10:1 or higher in mature basins, reinforcing the scale at which automated control becomes necessary. Field-level implementations demonstrate functional integration, as AI platforms linked to IoT and control systems can forecast volumes, pressures, and routing constraints in real time, and autonomously recommend or execute treatment decisions within defined limits. The digitalization transforms treatment systems from static, rule-based operations to adaptive, data-driven processes, enhancing efficiency, compliance, reliability, and resource utilization.

Geopolitical Impact Analysis

Geopolitical Tensions Are Impacting the Global Oil and Gas Market.

The geopolitical tensions are exerting measurable, multi-channel impacts on the produced water treatment market by altering upstream activity, cost structures, and infrastructure priorities. The supply disruptions directly affect production-linked water volumes. Recent conflicts have removed 8-10 million barrels per day (mb/d) of global oil supply, equivalent to around 8% of global output, through infrastructure damage and shipping constraints, leading to abrupt reductions in produced water generation in affected regions.

Additionally, sanctions and conflict exposure reshape geographic production patterns. Approximately one-third of OPEC output is affected by sanctions or instability, redistributing production toward politically stable regions. This reallocation shifts produced water treatment demand geographically, often toward jurisdictions with stricter environmental compliance, thereby increasing treatment intensity per unit of production.

Similarly, geopolitical volatility elevates cost uncertainty. Oil-import-dependent economies, such as India, face price and supply instability linked to conflicts and sanctions, constraining capital allocation for non-core investments such as advanced water treatment. The geopolitical tensions introduce opposing effects, such as localized contraction of treatment demand in disrupted regions, alongside structurally higher compliance and infrastructure needs in more stable production zones.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Produced Water Treatment Market.

In 2025, the Asia Pacific dominated the global produced water treatment market, holding about 41.9% of the total global consumption, due to the convergence of high energy consumption, mature fields, and offshore-intensive production. The region accounts for about 8% of global oil production despite hosting a majority of the global population, indicating intensive exploitation of aging reservoirs with rising water cuts. Mature field dynamics are structurally significant. The government-backed assessments show declines of over 1.2 mb/d in Southeast Asian production between 2000 and 2023, driven by aging assets and limited discoveries.

As reservoirs age, water-to-oil ratios increase substantially, expanding produced water volumes per unit of hydrocarbon output and elevating treatment requirements. Offshore dependence further reinforces treatment intensity. Countries such as Indonesia and Malaysia rely on deepwater developments and floating production systems, where discharge constraints and space limitations necessitate compact, high-efficiency treatment technologies. Simultaneously, high regional oil demand, driven by industrialization and transport, sustains production activity and associated wastewater generation.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Players in the produced water treatment market pursue a combination of technology, integration, and partnership-led strategies to strengthen competitive positioning. A primary focus is on technology innovation and R&D, with firms developing advanced treatment systems and compact modular units capable of treating and recovering most of the water. Additionally, companies emphasize integrated and customized solutions, combining physical, chemical, and biological processes into end-to-end treatment trains tailored to site-specific water chemistries and regulatory requirements.

Similarly, firms pursue strategic partnerships and long-term contracts with oil and gas operators to secure stable project pipelines and embed technologies within upstream operations. Furthermore, mergers and acquisitions are used to access proprietary technologies and expand geographic presence, reinforcing scale and technical capabilities. These strategies reflect competition centered on technological differentiation, operational efficiency, and solution integration rather than commoditized service provision.

The Major Players in The Industry

- SLB

- Baker Hughes

- Halliburton

- TechnipFMC

- Veolia Environnement

- Siemens Energy

- Aker Solutions

- Aquatech International

- Frames Group

- Weatherford International

- Ovivo

- Mineral Technologies

- Enviro-Tech Systems

- CETCO Energy Services

- Cannon Artes S.P.A.

- Other Key Players

Key Development

- In December 2024, Halliburton Labs announced that it added Espiku to its collaborative ecosystem to accelerate the commercialization of its produced water treatment technology.

- In March 2025, Veolia Water Technologies, a global leader in produced water treatment, announced the launch of ToroJet, a nutshell filtration system designed to meet the toughest produced water polishing needs in the oil and gas industry.

Report Scope

Report Features Description Market Value (2025) US$9.7 Bn Forecast Revenue (2035) US$19.6 Bn CAGR (2025-2035) 7.3% Base Year for Estimation 2025 Historic Period 2021-2024 Forecast Period 2025-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Physical Treatment, Chemical Treatment, and Biological Treatment), By Application (Onshore and Offshore) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape SLB, Baker Hughes, Halliburton, TechnipFMC, Veolia Environnement, Siemens Energy, Aker Solutions, Aquatech International, Frames Group, Weatherford International, Ovivo, Mineral Technologies, Enviro-Tech Systems, CETCO Energy Services, Cannon Artes S.P.A., and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Produced Water Treatment MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample

Produced Water Treatment MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- SLB

- Baker Hughes

- Halliburton

- TechnipFMC

- Veolia Environnement

- Siemens Energy

- Aker Solutions

- Aquatech International

- Frames Group

- Weatherford International

- Ovivo

- Mineral Technologies

- Enviro-Tech Systems

- CETCO Energy Services

- Cannon Artes S.P.A.

- Other Key Players

Our Clients

- 185282

- April 2026