Quick Navigation

Report Overview

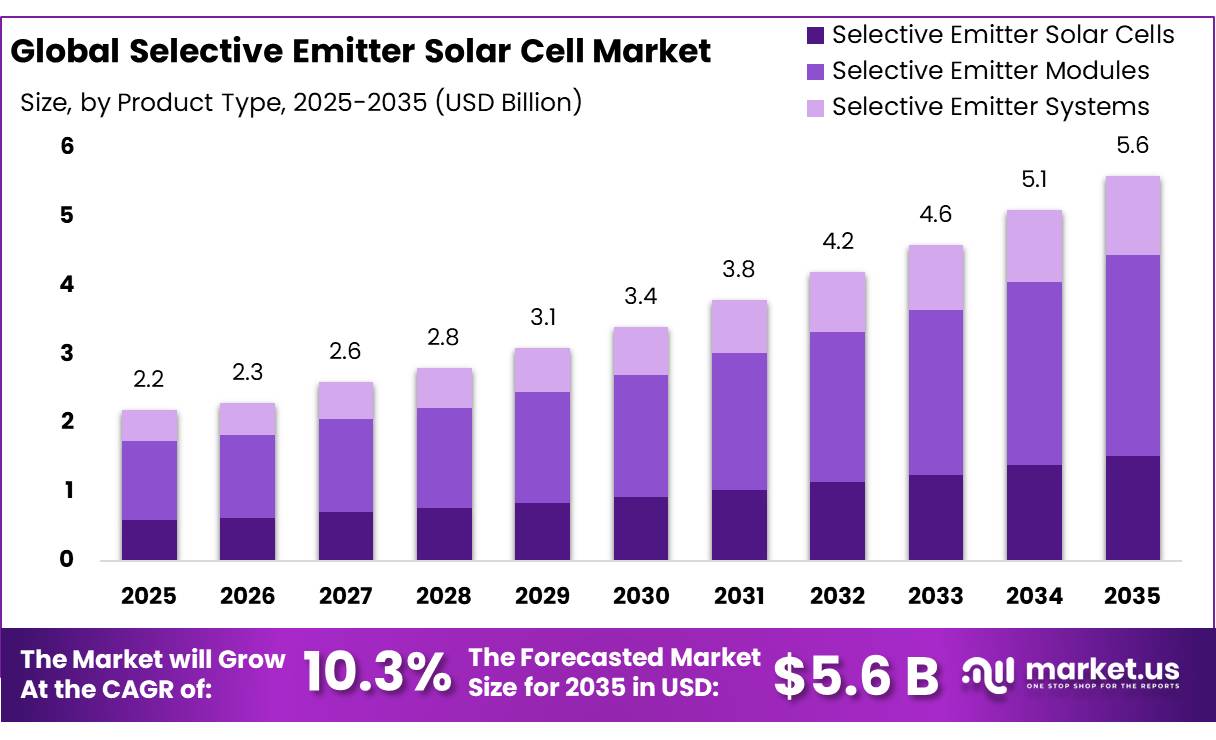

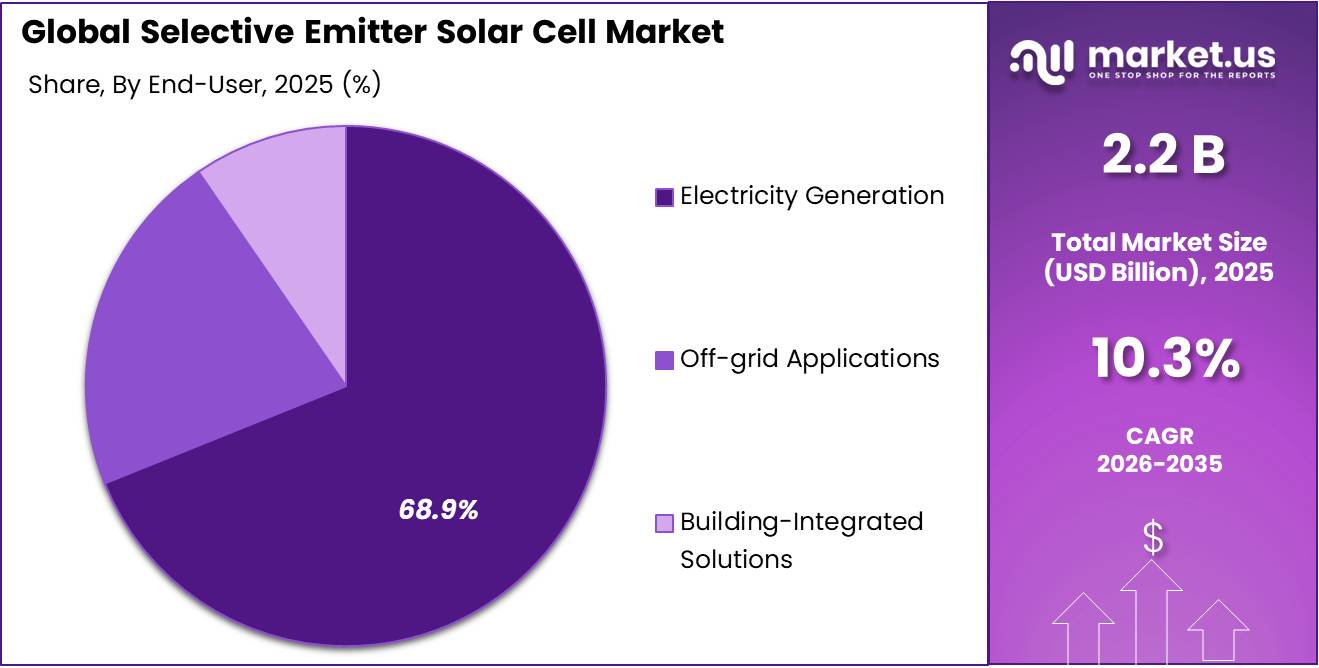

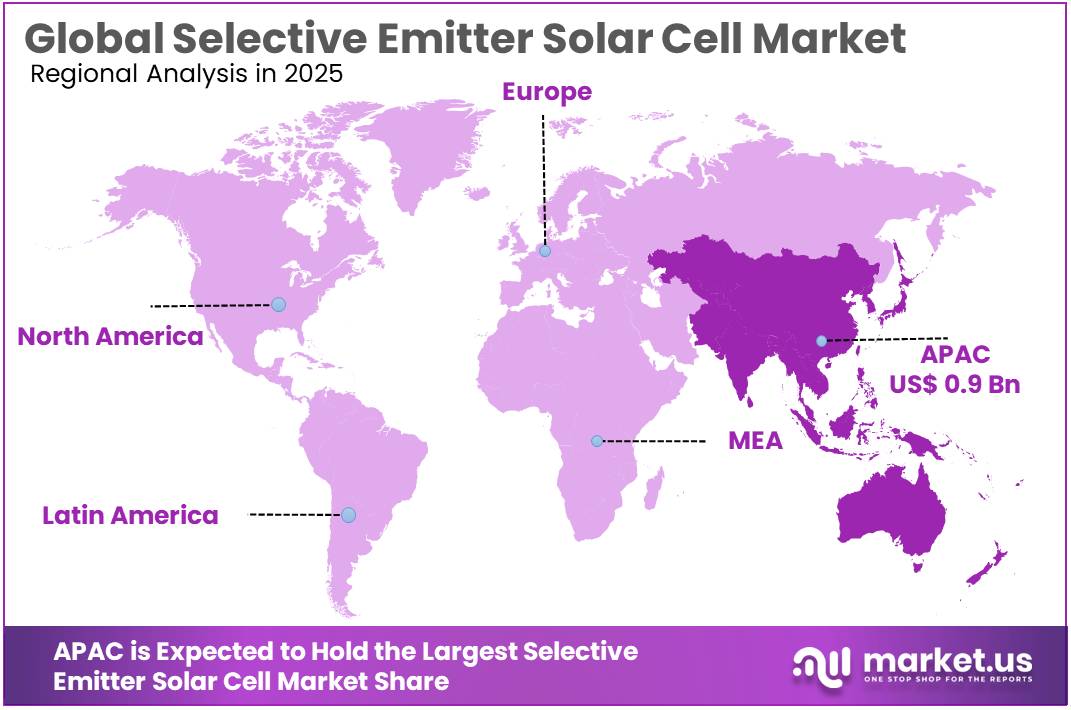

The Global Selective Emitter Solar Cell Market size is expected to be worth around USD 5.6 Billion by 2035, from USD 2.2 Billion in 2025, growing at a CAGR of 10.3% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 43.90% share, holding USD 0.9 Billion revenue.

Selective emitter solar cells are positioned as an industrial efficiency-upgrade technology because they use heavier doping under metal contacts and lighter doping across the active surface to reduce recombination losses and improve current collection. The technology remains relevant as manufacturers move from standard p-type architectures toward higher-efficiency n-type TOPCon, HJT and advanced passivated-contact platforms. Globally, IRENA reported 510.3 GW of solar PV capacity additions in 2025, while renewables reached 49% of global installed power capacity, creating a strong demand base for cell-efficiency improvements.

Key Takeaways

- Selective Emitter Solar Cell Market size is expected to be worth around USD 5.6 Billion by 2035, from USD 2.2 Billion in 2025, growing at a CAGR of 10.3%.

- Selective Emitter Modules held a dominant market position, capturing more than a 52.20% share of the selective emitter solar cell market.

- Monocrystalline Silicon Solar Cells held a dominant market position, capturing more than a 61.40% share of the selective emitter solar cell market.

- Utility-Scale Power Plants held a dominant market position, capturing more than a 41.60% share of the selective emitter solar cell market.

- Electricity Generation held a dominant market position, capturing more than a 68.90% share of the selective emitter solar cell market.

- Asia-Pacific emerged as the dominant region in the Selective Emitter Solar Cell market, holding a leading 43.90% share and reaching a market value of USD 0.9 Billion.

The industrial scenario is shaped by scale, cost pressure and technology migration. IEA expects global renewable power capacity to rise by almost 4,600 GW during 2025–2030, with solar PV representing nearly 80% of renewable capacity expansion. This favors selective-emitter-related process know-how because every fractional efficiency gain can reduce module area, balance-of-system cost and land use. IEA PVPS also noted that PV represented more than 75% of new renewable capacity installed in 2024, confirming PV’s central role in power-sector expansion.

The industrial scenario is shaped by scale, cost pressure and technology migration. IEA expects global renewable power capacity to rise by almost 4,600 GW during 2025–2030, with solar PV representing nearly 80% of renewable capacity expansion. This favors selective-emitter-related process know-how because every fractional efficiency gain can reduce module area, balance-of-system cost and land use. IEA PVPS also noted that PV represented more than 75% of new renewable capacity installed in 2024, confirming PV’s central role in power-sector expansion.

Key driving factors include rising utility-scale installations, pressure to lower levelized cost of electricity, and government-backed manufacturing localization. The European Union’s Net-Zero Industry Act sets a benchmark for EU clean-tech manufacturing capacity to meet at least 40% of annual deployment needs by 2030, supporting advanced cell and module production. In the United States, the DOE/NREL Solar Futures Study states that solar could supply 40% of U.S. electricity by 2035 and 45% by 2050, reinforcing long-term demand for higher-efficiency PV technologies.

Trina Solar remains a major technology participant. In January 2025, Trina reported a world-record 25.44% efficiency for large-area n-type fully passivated HJT modules, certified by Fraunhofer CalLab, demonstrating the industry’s shift toward premium-efficiency cell structures. In 2025, Trina also signed strategic cooperation with HoloSolis for TOPCon technology support and a 5 GW French module manufacturing project, strengthening Europe-focused industrial collaboration.

By Product Type Analysis

Selective Emitter Modules dominates with 52.20% share driven by higher conversion efficiency and better power output

In 2025, Selective Emitter Modules held a dominant market position, capturing more than a 52.20% share of the selective emitter solar cell market. This leadership was mainly supported by the growing focus on improving solar module efficiency while maintaining cost balance in large-scale production. Selective emitter technology became widely preferred because it allows better current collection and reduces recombination losses, helping manufacturers achieve stronger energy output without major changes to existing production lines. The segment also benefited from increasing demand for high-performance photovoltaic installations across utility, commercial, and residential applications where long-term energy yield remained a key purchasing factor.

By Cell Type Analysis

Monocrystalline Silicon Solar Cells leads with 61.40% share supported by strong efficiency and long-term energy performance

In 2025, Monocrystalline Silicon Solar Cells held a dominant market position, capturing more than a 61.40% share of the selective emitter solar cell market. The segment remained ahead due to its ability to deliver higher energy conversion efficiency and stable performance over long operating periods. Manufacturers and project developers increasingly selected monocrystalline cells because they offer better output from limited installation space, making them suitable for residential rooftops as well as large commercial and utility-scale solar projects. Their uniform crystal structure also contributed to improved electrical performance and reduced energy loss during operation.

By Application Analysis

Utility-Scale Power Plants dominates with 41.60% share driven by large project capacity and growing clean energy demand

In 2025, Utility-Scale Power Plants held a dominant market position, capturing more than a 41.60% share of the selective emitter solar cell market. This segment maintained its leading position due to increasing investments in large solar generation projects designed to meet rising electricity demand and support energy transition goals. Utility operators continued to favor selective emitter solar cells because of their improved efficiency and stronger power output, which helped maximize energy generation across large installation areas. Their ability to improve overall plant performance while supporting long-term operational stability made them a practical choice for grid-connected solar developments.

By End Use Analysis

Electricity Generation dominates with 68.90% share supported by rising solar power deployment and growing energy demand

In 2025, Electricity Generation held a dominant market position, capturing more than a 68.90% share of the selective emitter solar cell market. The segment led the market as solar technologies continued to play a larger role in meeting increasing global electricity requirements. Selective emitter solar cells gained wider acceptance in power generation applications because of their ability to improve energy conversion efficiency and deliver reliable output over long operating periods. Their use supported higher electricity production while helping operators improve overall system performance and reduce energy losses across installations of different scales.

Key Market Segments

By Product Type

- Selective Emitter Solar Cells

- Selective Emitter Modules

- Selective Emitter Systems

By Cell Type

- Monocrystalline Silicon Solar Cells

- Polycrystalline Silicon Solar Cells

- Thin Film Solar Cells

By Application

- Residential

- Commercial

- Utility-Scale Power Plants

- Industrial

By End Use

- Electricity Generation

- Off-grid Applications

- Building-Integrated Solutions

Emerging Trends

Shift Toward High-Efficiency Solar Cell Architectures is Emerging as a Key Trend

One of the latest trends shaping the Selective Emitter Solar Cell market is the increasing move toward high-efficiency solar cell architectures that improve power generation without significantly increasing installation area. Energy developers and manufacturers are focusing more on technologies that can deliver greater output and stronger long-term performance as renewable energy targets become more ambitious.

This trend is closely connected with the rapid expansion of solar deployment worldwide. According to the International Energy Agency (IEA), global renewable electricity generation is expected to rise by more than 17,000 terawatt-hours (TWh) between 2023 and 2030, representing an increase of nearly 90%. Solar photovoltaic remains the fastest-growing renewable source and is expected to contribute almost half of this additional generation.

Government-Led Solar Manufacturing Expansion is Encouraging Advanced Cell Adoption

Another major trend is the growing government support for advanced solar manufacturing and local supply chain development. Countries are introducing industrial policies, investment incentives, and clean energy programs to strengthen domestic solar production and improve technology competitiveness. These efforts are creating favorable conditions for advanced cell structures, including selective emitter designs.

According to the International Energy Agency, global solar PV manufacturing investment reached around US$80 billion in 2023 as companies expanded production facilities and upgraded manufacturing capabilities. Government initiatives supporting renewable infrastructure and domestic production continue encouraging adoption of higher-efficiency solar technologies. Manufacturers are increasingly investing in production methods that allow better energy performance while maintaining commercial scalability.

Drivers

Rising Global Solar Capacity Expansion is Accelerating Demand for Selective Emitter Solar Cells

One of the major driving factors for the Selective Emitter Solar Cell market is the rapid expansion of solar power capacity across the world. As governments, utilities, and energy producers continue investing in cleaner electricity systems, there is increasing pressure to improve solar panel efficiency and maximize energy output from every installation. Selective emitter solar cells have gained attention because they help improve electrical performance and reduce energy losses, making them suitable for both utility-scale and distributed solar projects.

The growth in solar deployment clearly reflects this shift. According to the International Energy Agency (IEA), global renewable capacity additions reached around 666 GW in 2024 and are expected to continue rising strongly toward 2030, with solar PV and wind accounting for almost 95% of total additions. The IEA also stated that solar PV is expected to contribute nearly 80% of the global renewable capacity increase over the coming years.

Government Support and Clean Energy Investments are Strengthening Technology Adoption

Another key factor supporting the Selective Emitter Solar Cell market is the growing level of government-backed clean energy programs and investment commitments. Across many regions, energy policies are encouraging faster renewable deployment through incentives, manufacturing support, and long-term renewable targets. These initiatives are pushing developers and manufacturers toward technologies that can improve generation efficiency and project economics.

According to the International Energy Agency, global investment in clean energy technology and infrastructure was expected to reach US$2 trillion in 2024, while investment in solar photovoltaic technology alone was projected to grow to approximately US$500 billion. In addition, global renewable power capacity is projected to increase by nearly 4,600 GW between 2025 and 2030, supported largely by lower solar costs and continued policy support.

Restraints

High Manufacturing Complexity and Production Costs Continue to Limit Wider Adoption

One of the major restraining factors for the Selective Emitter Solar Cell market is the higher manufacturing complexity compared with conventional solar cell technologies. Selective emitter cells require additional processing steps, precise doping methods, and tighter production control to achieve higher conversion efficiency. While the technology improves energy output, it also raises equipment requirements and production expenses, creating challenges for manufacturers operating in cost-sensitive markets.

Industry investment figures reflect the scale of this challenge. According to the International Energy Agency (IEA), global investment in solar photovoltaic manufacturing reached around US$80 billion in 2023, with significant spending directed toward expanding advanced production capabilities and improving manufacturing efficiency. Despite these investments, higher capital requirements remain a barrier for companies trying to move from standard solar cell production to more advanced technologies such as selective emitter designs.

Supply Chain Pressure and Manufacturing Concentration Create Growth Challenges

Another factor limiting the Selective Emitter Solar Cell market is the concentration of solar manufacturing and dependence on specialized supply chains. Advanced solar cell production relies on stable access to refined silicon materials, processing equipment, and high-quality manufacturing infrastructure. Any disruption in these areas can affect production timelines and project economics.

According to the International Energy Agency, more than 80% of global solar PV manufacturing capacity is concentrated in a limited number of production regions, increasing exposure to supply chain risks and market imbalances. Governments across several countries have introduced manufacturing support programs and local production incentives to reduce dependency and improve energy security, but building domestic capacity requires time and substantial capital.

Opportunity

Expansion of Utility-Scale Solar Projects Creates Strong Growth Opportunity for Selective Emitter Solar Cells

One of the strongest growth opportunities for the Selective Emitter Solar Cell market is the rapid expansion of utility-scale solar installations supported by national clean energy targets and large renewable investments. As electricity demand continues to rise, governments and power developers are focusing on technologies that can generate more power from the same installation area. Selective emitter solar cells are well positioned to benefit because they improve energy conversion efficiency and support better output over the life of the solar project.

According to the International Energy Agency (IEA), global renewable power capacity is expected to expand by nearly 5,500 GW between 2024 and 2030, with solar photovoltaic accounting for approximately 80% of the total growth. This large-scale solar expansion creates direct opportunities for advanced cell technologies that can improve project returns and lower generation losses.

Government Manufacturing Programs and Clean Energy Investment Support Long-Term Market Expansion

Another major opportunity comes from rising government support for solar manufacturing and domestic clean energy production. Countries are increasingly investing in local solar supply chains to reduce import dependency and strengthen energy security. This trend supports technologies that deliver higher efficiency and stronger long-term performance.

The International Energy Agency reported that global investment in clean energy technologies reached approximately US$2 trillion in 2024, with solar attracting around US$500 billion in investment. At the same time, multiple government initiatives continue encouraging production expansion through incentives, infrastructure funding, and renewable energy commitments. Selective emitter solar cells stand to benefit from this transition because manufacturers are looking for advanced solutions that can improve module competitiveness while meeting stricter efficiency expectations.

Regional Insights

Asia-Pacific dominated the Selective Emitter Solar Cell market with a 43.90% share, accounting for USD 0.9 Billion due to strong solar manufacturing capacity and renewable energy expansion.

In 2025, Asia-Pacific emerged as the dominant region in the Selective Emitter Solar Cell market, holding a leading 43.90% share and reaching a market value of USD 0.9 Billion. The region’s leadership was supported by its large-scale solar manufacturing ecosystem, expanding renewable energy infrastructure, and continued investments in advanced photovoltaic technologies. Countries across the region continued to prioritize high-efficiency solar deployment to meet rising electricity demand while reducing dependence on conventional energy sources.

The region maintained a strong position because of its established solar supply chain and broad installation base across utility-scale and distributed energy projects. Asia-Pacific has remained a global center for solar production and module deployment, creating favorable conditions for selective emitter technologies that improve conversion efficiency and increase energy output. Manufacturers in the region have also focused on upgrading production capabilities to support next-generation solar cell designs and improve competitiveness in export markets.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Trina Solar is one of the leading industrial participants in advanced crystalline-silicon and selective-emitter-related cell technologies through its focus on passivation, TOPCon and heterojunction integration. The company reported cumulative module shipments exceeding 292 GW by June 2025, demonstrating large-scale industrial deployment capability. Trina also achieved a certified 25.44% conversion efficiency for large-area n-type HJT modules in 2025, reinforcing efficiency-led manufacturing strategy. The company operates across 180+ countries and recorded 37 world records in PV efficiency and module output between 2011–2025.

JinkoSolar maintains strong positioning in selective-emitter-compatible and TOPCon manufacturing through large-scale n-type cell production. The company’s high-efficiency monocrystalline silicon cell reached 26.1% conversion efficiency, supported by technologies including laser-doped selective emitter structures, advanced passivation and ultra-thin metallization. By the end of 2024, Jinko’s manufacturing roadmap indicated capacities of 120 GW wafers, 110 GW cells and 130 GW modules, including more than 100 GW of n-type capacity, making it one of the largest global solar manufacturers.

Top Key Players Outlook

- Trina Solar

- SolarWorld

- JinkoSolar

- Pionis Energy

- Alps Technology

- Itek Energy

- Longi Green Energy

- Canadian Solar Inc.

- SunPower Corporation

- REC Group

Recent Industry Developments

In 2026, Alps Technology Inc. remained a small U.S.-based solar module and solar cell supplier in the Selective Emitter Solar Cell value chain, mainly serving commercial, industrial, and telecommunication applications. The company lists solar panels, solar cells, flexible panels, and solar power generators in its product portfolio, with its address shown in Walnut, California. Its available product data includes AP-BP85W at 85 W, 17.6 V, and 34.8 A, along with ATI-140/150/170 W panels offering a 140–170 Wp power range, 36 cells, 10-year product warranty, 600 V maximum system voltage, and 20–230 Wp crystalline product range.

In 2025, Pionus Energy, often searched as Pionis Energy, appeared to be a small India-based solar service company rather than a large selective emitter solar cell manufacturer. Public records show the company was incorporated on 24 December 2020, with authorized capital of ₹10,00,000 and paid-up capital of ₹1,20,000.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.2 Bn |

| Forecast Revenue (2035) | USD 5.6 Bn |

| CAGR (2026-2035) | 10.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Selective Emitter Solar Cells, Selective Emitter Modules, Selective Emitter Systems), By Cell Type (Monocrystalline Silicon Solar Cells, Polycrystalline Silicon Solar Cells, Thin Film Solar Cells), By Application (Residential, Commercial, Utility-Scale Power Plants, Industrial), By End Use (Electricity Generation, Off-grid Applications, Building-Integrated Solutions) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Trina Solar, SolarWorld, JinkoSolar, Pionis Energy, Alps Technology, Itek Energy, Longi Green Energy, Canadian Solar Inc., SunPower Corporation, REC Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |