Quick Navigation

Report Overview

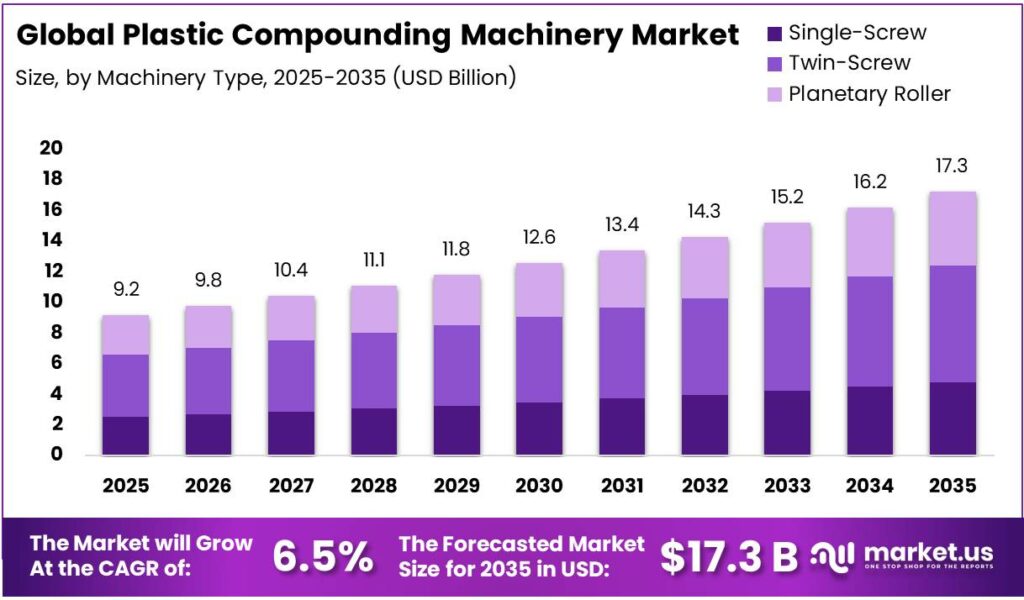

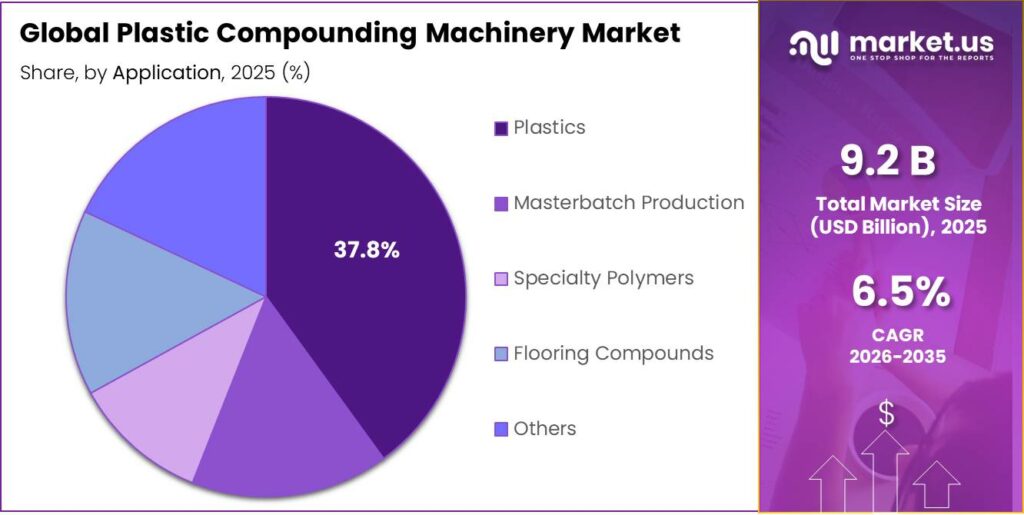

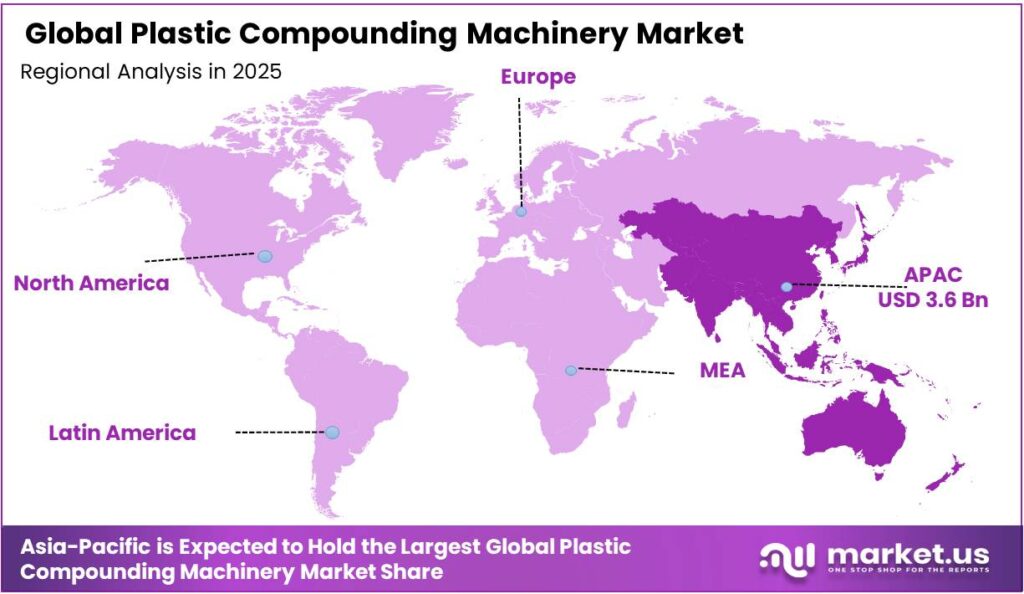

The Global Plastic Compounding Machinery Market size is expected to be worth around USD 16.2 Billion by 2035, from USD 9.2 Billion in 2025, growing at a CAGR of 6.5% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 38.9% share, holding USD 3.6 Billion revenue.

The plastic compounding machinery market is primarily driven by high-volume polymer processing across diverse industrial applications, with Asia Pacific emerging as the largest regional hub due to concentrated polymer production, integrated manufacturing ecosystems, and supportive industrial policies.

Machinery demand is concentrated in general plastics, particularly for packaging, reflecting the sector’s high material throughput, continuous processing requirements, and standardized formulations. Twin-screw extruders dominate due to their superior dispersive and distributive mixing, modular design, high filler-handling capability, and adaptability to recycled or multi-material systems, whereas single-screw and planetary roller machines serve more specialized or low-volume applications.

Strategically, manufacturers focus on technological differentiation, digitalization, and lifecycle services—such as predictive maintenance, process automation, and retrofits—to enhance competitiveness. Trends such as Industry 4.0 adoption, circular economy integration, and electrification-linked material complexity increase demand for sophisticated compounding solutions. Conversely, environmental regulations, supply chain disruptions from geopolitical tensions, and raw material volatility impose operational constraints, influencing production flexibility, sourcing strategies, and machinery design priorities across the market.

Key Takeaways

- The global plastic compounding machinery market was valued at USD 9.2 billion in 2025.

- The global plastic compounding machinery market is projected to grow at a CAGR of 6.5% and is estimated to reach USD 16.2 billion by 2035.

- On the basis of machinery type, twin-screw compounding machinery dominated the market, constituting 44.3% of the total market share.

- Based on the applications of the plastic compounding machinery, plastics led the market, comprising 37.8% of the total market.

- Among the end-uses, the packaging sector held a major share of the market, accounting for around 32.9% of the revenue.

- In 2025, the Asia pacific was the most dominant region in the plastic compounding machinery market, accounting for 38.9% of the total global consumption.

Machinery Type Analysis

Twin-Screw Compounding Machinery is a Prominent Segment in the Market.

The market is segmented based on the machinery type into single-screw, twin-screw, and planetary roller. The twin-screw compounding machinery led the market, comprising 44.3% of the market share, as it provides superior mixing, process control, and material flexibility compared with single-screw and planetary roller systems. Co-rotating twin-screw extruders enable intensive distributive and dispersive mixing, ensuring uniform incorporation of fillers, additives, and reinforcements—critical for engineering plastics and recycled materials. Their segmented screw design allows modular configuration, enabling operators to tailor shear, temperature profile, and residence time for different formulations.

In contrast, single-screw machines are primarily suited for melting and conveying, with limited mixing capability, while planetary roller extruders, though effective for specific temperature-sensitive applications, lack comparable flexibility. Twin-screw systems also support higher filler loadings (often >50%) and efficient devolatilization, improving compound quality. Additionally, their continuous, stable processing and adaptability to multi-material systems make them suitable for diverse applications, including automotive, electrical, and recycling streams, reinforcing their broader industrial adoption.

Application Analysis

Plastics Dominated the Plastic Compounding Machinery Market.

On the basis of applications, the plastic compounding machinery market is segmented into plastics, masterbatch production, specialty polymers, flooring compounds, and others. The plastics dominated the plastic compounding machinery market, comprising 37.8% of the market share, as base polymer processing constitutes the largest and most continuous material flow across industries such as packaging, automotive, construction, and consumer goods. High-volume resins (e.g., polyethylene, polypropylene) require consistent compounding for stabilization, coloring, and property enhancement, resulting in continuous, large-scale utilization of machinery.

In contrast, applications such as masterbatch, specialty polymers, or flooring compounds are comparatively lower-volume and formulation-specific, often produced in shorter runs with tighter tolerances but less frequent throughput. These segments may use similar equipment, but their demand is episodic rather than continuous.

Additionally, general plastics processing typically involves simpler formulations and standardized inputs, enabling higher operating rates and broader applicability of machinery. This combination of scale, repeatability, and cross-industry demand leads to a higher concentration of compounding equipment in conventional plastics rather than niche or specialty applications.

End-Use Analysis

Plastic Compounding Machinery is Mostly Used in the Packaging Industry.

Among the end-uses, 32.9% of the total global consumption of plastic compounding machinery is in the packaging industry, outperforming construction and infrastructure, medical and healthcare, automotive, electronics, chemicals, and other industries, as packaging represents the highest-volume, fastest-turnover application for polymers. Public data from the United Nations Environment Programme indicate that ~36% of global plastics are used in packaging, with a large share designed for single or short-duration use. This creates continuous, high-frequency demand for compounded resins (e.g., for films, containers, and flexible packaging).

Packaging formulations typically require additives for barrier properties, flexibility, clarity, and processability, driving repetitive, large-scale compounding operations. In contrast, sectors such as automotive or electronics use plastics in lower volumes but higher specification applications, often with longer product life cycles and less frequent production cycles.

Additionally, packaging production operates on high-speed conversion lines, requiring steady, standardized material supply, which aligns with continuous compounding processes. This combination of scale, repeatability, and rapid consumption results in a higher concentration of compounding machinery in packaging relative to other industries.

Key Market Segments

By Machinery Type

- Single-Screw

- Twin-Screw

- Co-Rotating Twin-Screw

- Counter-Rotating Twin-Screw

- Planetary Roller

By Application

- Plastics

- Masterbatch Production

- Specialty Polymers

- Flooring Compounds

- Others

By End-Use

- Packaging

- Construction and Infrastructure

- Medical and Healthcare

- Automotive

- Electronics

- Chemicals

- Others

Drivers

Automotive Lightweighting & Electrification Drives the Plastic Compounding Machinery Market.

Automotive lightweighting and electrification jointly intensify demand for engineered polymers, thereby driving requirements for plastic compounding machinery with higher precision and material versatility. Evidence from the American Chemistry Council shows plastics accounted for ~411 lb per vehicle in 2021 (~10% of weight but ~50% of volume), up ~16% from 2012, reflecting substitution toward polymers in structural and functional parts.

Electrification amplifies this shift. Battery systems add substantial mass (1,800 lb in a pickup-class EV), necessitating compensatory lightweighting through plastics and composites. Plastics enable 35% lighter battery enclosures versus metal and facilitate part consolidation, increasing demand for compounded thermoplastics with tailored thermal and mechanical properties. From a performance standpoint, a 10% vehicle weight reduction can improve fuel efficiency by 6–8% and extend EV range by 5–7%, reinforcing regulatory alignment.

Consequently, electrification-linked material complexity (multi-resin systems, high-temperature polymers, electrically functional plastics) raises processing requirements—directly expanding the technical scope and throughput demands of plastic compounding machinery.

Restraints

Stringent Environmental Regulations Against Plastic Might Hamper the Demand for the Plastic Compounding Machinery.

Stringent environmental regulations on plastics impose structural constraints on the plastic compounding machinery market by restricting end-use demand, altering material specifications, and increasing compliance burdens. Government-led bans and regulatory frameworks directly curtail high-volume polymer applications. For instance, India’s Plastic Waste Management Rules prohibit the manufacture, import, and sale of identified single-use plastic items from July 2022, targeting products with “low utility and high littering potential.”

Quantitatively, regulatory focus is concentrated on dominant waste streams: single-use plastics account for 43% of India’s 9.46 million tons of annual plastic waste. Globally, 36% of plastic production is used in packaging, with 85% of this ending up in landfill or unmanaged waste—driving regulatory prioritization of this segment.

Policy tightening extends beyond bans to lifecycle accountability. Over 40 countries have implemented Extended Producer Responsibility (EPR) regimes, with over 45,000 companies participating in India alone, mandating recovery and recycling obligations. Such measures reduce demand for conventional compounding (e.g., low-cost packaging grades) while requiring reconfiguration toward recyclates and compliant materials, increasing technological complexity and capital requirements for machinery manufacturers.

Opportunity

Circular Economy & Recycling Infrastructure Creates Opportunities in the Plastic Compounding Machinery Market.

The expansion of circular economy policies and recycling infrastructure creates a structural opportunity for plastic compounding machinery by increasing demand for reprocessing, material standardization, and recyclate upgrading. Globally, plastic flows remain highly inefficient: only 15% of plastic waste is collected for recycling and less than 9% is ultimately recycled after process losses, indicating substantial latent feedstock for mechanical reprocessing.

Public policy is explicitly targeting this gap. Under the New Plastics Economy Global Commitment, over 500 signatories representing 20% of global plastic packaging have committed to higher collection and recycling rates, with examples such as France targeting 100% recycling of single-use plastic packaging by 2025. Quantitatively, regional systems are scaling: plastic recycling rates in Europe reache41% in 2021, reflecting infrastructure build-out and regulatory enforcement. However, material degradation, contamination, and polymer heterogeneity necessitate advanced compounding, such as additives and compatibilizers, to restore performance properties.

Consequently, the transition from linear to circular material flows increases demand for machinery capable of handling mixed waste streams, improving recyclate quality, and enabling closed-loop applications—directly expanding the technical scope of compounding systems.

Trends

Adoption of Intelligent & Automated Machinery (Industry 4.0).

The adoption of intelligent and automated machinery under Industry 4.0 is emerging as a defining trend in plastic compounding, driven by requirements for process consistency, labor substitution, and real-time optimization. Industry 4.0—originating from the German federal government—integrates cyber-physical systems, IoT, and data analytics to enable smart factories with autonomous decision-making and interconnected production systems.

In plastics processing, machinery is increasingly embedded with sensors and communication capabilities, enabling self-monitoring and data-driven control of compounding parameters such as temperature, shear, and dispersion. Quantitatively, operational pressures are accelerating this shift: a 2026 industry survey indicates nearly 50% of plastics processors report labor shortages affecting operations, prompting increased investment in automation and robotics.

Automation delivers measurable process benefits, including reduced variability, improved throughput, and lower dependence on skilled operators. Integrated systems—such as collaborative robots and AI-assisted controls—are also being deployed to standardize production and reduce error rates. Consequently, plastic compounding machinery is evolving toward digitally integrated, sensor-enabled platforms capable of predictive maintenance, adaptive processing, and closed-loop quality control, redefining equipment functionality beyond conventional mechanical performance.

Geopolitical Impact Analysis

Geopolitical Tensions Have Led to Severe Disruptions in the Plastics Market.

Current geopolitical tensions are exerting multi-layered impacts on the plastic compounding machinery market through disruptions in feedstock supply, trade flows, and capital investment conditions. Recent conflict-driven supply shocks in petrochemicals are quantitatively significant. In 2025, the Middle East accounted for over 40% of global polyethylene exports, and disruptions around the Strait of Hormuz—through which an estimated US$20–25 billion of petrochemical goods transit annually—have constrained up to 50% of polyethylene supply, driving sharp price volatility. This directly affects compounding economics, as polyethylene and polypropylene are primary input resins.

Sanctions and conflict-related trade fragmentation further strain supply chains. European Commission assessments identify logistics disruptions, commodity price spikes, and forced supplier substitution as key transmission channels, with industries required to reconfigure sourcing under constrained conditions. These shifts increase operational uncertainty for machinery deployment and capacity planning.

Cost pressures are compounded by energy and tariff asymmetries. EU plastics production declined by 7.6% in 2023 amid elevated energy prices and trade barriers, while tariff differentials, such as 15% on EU exports to the U.S., alter global competitiveness. Collectively, geopolitical tensions introduce volatility in raw material availability, input costs, and trade regimes, constraining investment visibility and accelerating regionalization of plastics processing and compounding infrastructure.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Plastic Compounding Machinery Market.

In 2025, the Asia Pacific dominated the global plastic compounding machinery market, holding about 38.9% of the total global consumption. Asia Pacific represents the largest and most structurally dominant region in plastics production and consumption, which directly translates into leadership in demand for plastic compounding machinery. Quantitatively, the region accounts for over 50% of global plastic material production, with China alone contributing 33%, indicating concentrated upstream polymer availability and downstream processing activity.

This scale is reinforced by absolute production volumes: Asia-Pacific produced 52% of global plastics (390.7 million tons) in 2021, reflecting dense integration across petrochemicals, conversion, and end-use manufacturing. Industrial structure further amplifies machinery demand. Governments across major economies (e.g., China, India, Southeast Asia) promote domestic manufacturing through policy support, FDI liberalization, and industrial programs, expanding plastics use in automotive, electronics, and consumer goods.

Additionally, the region’s proximity to feedstock sources, lower production costs, and large-scale processing ecosystems enable high-throughput compounding operations. Simultaneously, Asia is a major hub for plastic waste generation and recycling activity, reinforcing continuous demand for both virgin and recycled polymer processing. Collectively, scale concentration, integrated value chains, and policy-supported manufacturing establish Asia Pacific as the primary center of gravity for plastic compounding machinery deployment.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of plastic compounding machinery focus on technology differentiation, process efficiency, and lifecycle services to strengthen competitiveness. A key priority is R&D in advanced extrusion systems, including twin-screw compounding lines capable of handling recycled, bio-based, and high-performance polymers with precise control over dispersion and thermal stability. Companies such as Coperion and Leistritz highlight modular designs and high-torque systems in product disclosures to improve throughput and flexibility.

Digitalization is another focus area, with integration of IoT-enabled monitoring, predictive maintenance, and closed-loop process control to enhance uptime and reduce variability. Firms also expand after-sales services, including retrofits, spare parts, and technical support, to extend equipment life cycles. Additionally, manufacturers pursue geographic expansion and localization of production, alongside collaborations with polymer producers and recyclers, to align machinery capabilities with evolving material requirements and regulatory standards.

The Major Players in The Industry

- Coperion GmbH

- CPM Extricom Extrusion GmbH

- Farrel Corporation

- ICMA San Giorgio S.p.A.

- Ikegai Corporation

- Kobe Steel, Ltd.

- KraussMaffei Group GmbH

- Nordson Corporation

- Randcastle Extrusion Systems, Inc.

- Technovel Corporation

- The Japan Steel Works, Ltd.

- Theysohn Extrusionstechnik GmbH

- Shibaura Machine Co., Ltd.

- TPV Compound S.r.l.

- Useon Extrusion Machinery Co., Ltd.

- Welset Plast Extrusions Pvt. Ltd.

- Leistritz Extrusionstechnik GmbH

- Bühler AG

- Entek Manufacturing, LLC

- Bausano and Figli S.p.A.

- Other Key Players

Key Development

- In March 2023, ENTEK announced the completion of Phase 1 of its build out of the company’s 100,000 ft2 manufacturing facility in Henderson, Nev.

- In March 2023, ICMA San Giorgio completed five installations of recycling lines dedicated to re-compounding of post-consumer plastic waste.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$9.2 Bn |

| Forecast Revenue (2035) | US$16.2 Bn |

| CAGR (2026-2035) | 6.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Machinery Type (Single-Screw, Twin-Screw, and Planetary Roller), By Application (Plastics, Masterbatch Production, Specialty Polymers, Flooring Compounds, and Others), By End-Use (Packaging, Construction and Infrastructure, Medical and Healthcare, Automotive, Electronics, Chemicals, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Coperion GmbH, CPM Extricom Extrusion GmbH, Farrel Corporation, ICMA San Giorgio S.p.A., Ikegai Corporation, Kobe Steel, Ltd., KraussMaffei Group GmbH, Nordson Corporation, Randcastle Extrusion Systems, Inc., Technovel Corporation, The Japan Steel Works, Ltd., Theysohn Extrusionstechnik GmbH, Shibaura Machine Co., Ltd., TPV Compound S.r.l., Useon Extrusion Machinery Co., Ltd., Welset Plast Extrusions Pvt. Ltd., Leistritz Extrusionstechnik GmbH, Bühler AG, Entek Manufacturing, LLC, Bausano and Figli S.p.A., and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |