Quick Navigation

Report Overview

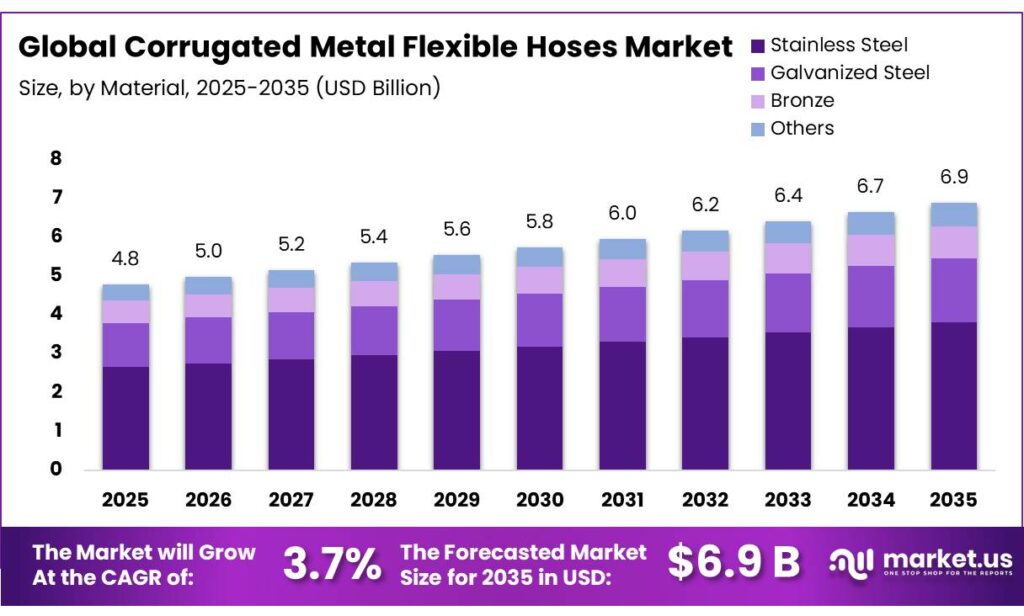

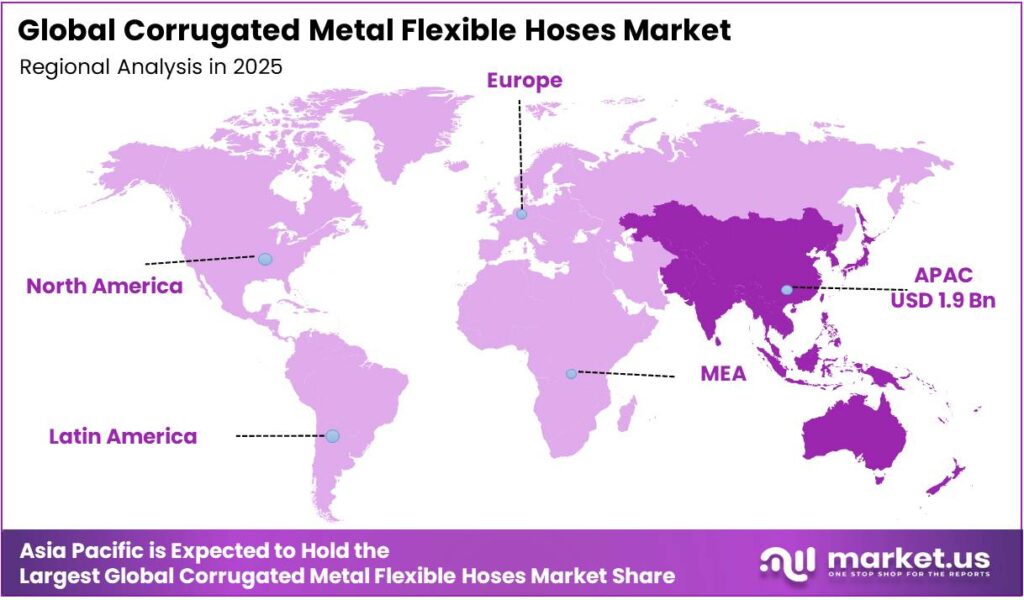

The Global Corrugated Metal Flexible Hoses Market size is expected to be worth around USD 6.9 Billion by 2035, from USD 4.8 Billion in 2025, growing at a CAGR of 3.7% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 44.4% share, holding USD 0.9 Billion revenue.

Corrugated metal flexible hoses are high-performance conduits consisting of a thin-walled metal tube that has been shaped into a series of ridges and valleys (corrugations) to allow for movement while maintaining a leak-tight seal. The market is characterized by structurally driven demand across multiple industrial sectors, with adoption primarily guided by performance, reliability, and operational requirements.

Oil & gas, chemical, and petrochemical sectors constitute the largest users, driven by the need to transport corrosive, high-pressure, and high-temperature fluids while accommodating vibration, thermal expansion, and misalignment. Medium-bore, low-pressure, and unlined stainless steel hoses dominate due to their optimal balance of flow efficiency, mechanical flexibility, corrosion resistance, thermal tolerance, and ease of installation.

Aerospace, HVAC, and power generation applications provide additional opportunities, leveraging hoses for hydraulic, steam, fuel, and cooling systems under stringent safety and fatigue-resistance requirements. Regionally, the Asia Pacific leads due to concentrated industrial output, extensive energy projects, and growing utility infrastructure. Manufacturers emphasize product innovation, certification compliance, customization, and supply chain integration to maintain a competitive advantage.

Key Takeaways

- The global corrugated metal flexible hoses market was valued at USD 4.8 billion in 2025.

- The global corrugated metal flexible hoses market is projected to grow at a CAGR of 3.7% and is estimated to reach USD 6.9 billion by 2035.

- On the basis of material, stainless steel flexible hoses dominated the market, constituting 55.4% of the total market share.

- Based on the diameter, medium bore (1”-6”) flexible hoses dominated the corrugated metal flexible hoses market, with a substantial market share of around 50.4%.

- Based on the pressure rating, low-pressure flexible hoses led the market, comprising 50.7% of the total market.

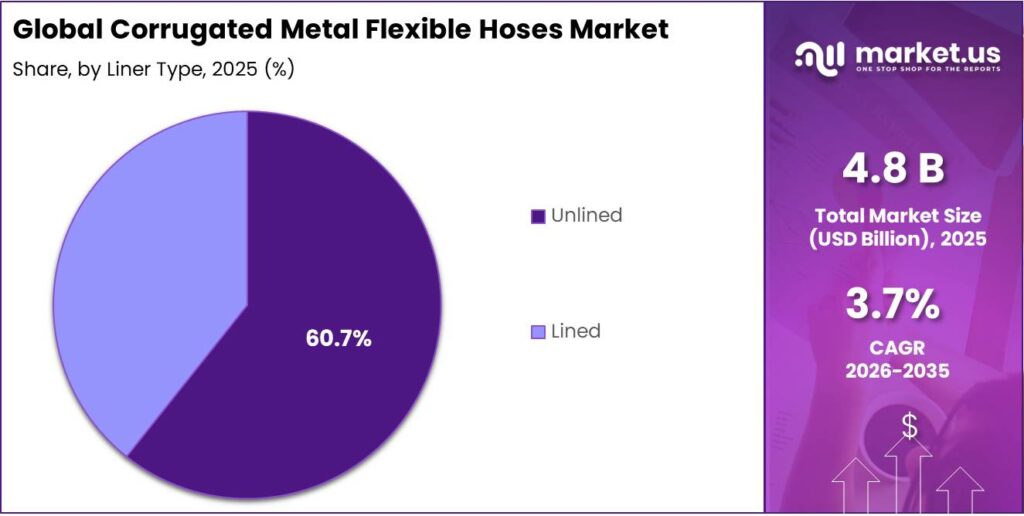

- Among the liner types, unlined hoses held a major share in the corrugated metal flexible hoses market, 60.7% of the market share.

- Among the end-use industries, the chemical & petrochemical sector is the most considerable within the market, accounting for around 30.2% of the revenue.

- In 2025, the Asia Pacific was the most dominant region in the corrugated metal flexible hoses market, accounting for 40.5% of the total global consumption.

Material Analysis

Stainless Steel Hoses are a Prominent Segment in the Market.

The market is segmented based on materials of corrugated metal flexible hoses into stainless steel, galvanized steel, bronze, and others. The stainless steel hoses led the market, comprising 55.4% of the market share, due to their superior balance of corrosion resistance, mechanical strength, and temperature tolerance relative to alternatives. Stainless steels form a stable chromium-oxide passive layer, enabling resistance to moisture, chemicals, and oxidation without coatings.

In contrast, galvanized steel relies on a zinc layer that can degrade under abrasion, high temperature, or aggressive media, exposing the base metal. Additionally, stainless steel maintains strength and ductility across wide temperature ranges and under cyclic loading, supporting long fatigue life in vibration-intensive environments. Bronze offers good corrosion resistance but has lower tensile strength and pressure tolerance.

Diameter Analysis

Medium Bore (1”-6”) Hoses Dominated the Corrugated Metal Flexible Hoses Market.

On the basis of diameter, the corrugated metal flexible hoses market is segmented into small bore (<1”), medium bore (1”-6”), and large bore (>6”). The medium bore (1”-6”) hoses dominated the market, comprising 50.4% of the market share, as they offer an optimal balance between flow capacity, flexibility, and installation. Medium bores accommodate common industrial and utility fluid volumes while maintaining a manageable pressure drop. Small bores restrict flow and are prone to clogging or higher friction losses, limiting their suitability for systems requiring significant throughput.

Medium hoses retain adequate flexibility for bends, vibration absorption, and thermal expansion without excessive stiffness, unlike large bore hoses, which require additional supports and specialized installation techniques. Standard pumps, valves, and flange systems are typically designed for 1”-6” connections, facilitating integration into pipelines and equipment.

Pressure Rating Analysis

Low Pressure Hoses Are the Most Widely Utilized Corrugated Metal Flexible Hoses.

The low-pressure corrugated metal flexible hoses dominated the market, with a notable market share of 50.7%, as they meet the majority of industrial and utility requirements while offering ease of installation, safety, and cost efficiency. Low-pressure hoses require fewer reinforcement layers or braiding, making them lighter and easier to bend, align, and install in tight spaces. Medium and high-pressure hoses need additional layers or thicker walls, reducing flexibility and increasing handling complexity.

Additionally, Low-pressure systems experience lower stress on hose walls and fittings, reducing fatigue and leak risk over time. Many HVAC, water transfer, and light chemical or fuel systems operate well below high-pressure thresholds, making low-pressure hoses sufficient for most installations. Lower mechanical stress translates into longer service life, reduced inspection frequency, and simplified replacement, increasing operational efficiency and practical adoption.

Liner Type Analysis

Unlined Hoses Held a Major Share of the Corrugated Metal Flexible Hoses Market.

Based on liner type, the corrugated metal flexible hoses market is segmented into unlined and lined. 60.7% of the corrugated metal flexible hoses consumed globally are unlined hoses, due to their versatility, mechanical strength, and suitability for high-temperature and high-pressure applications. Without an internal lining, unlined hoses can withstand higher temperatures and pressures, as linings often degrade above certain thresholds or under cyclic pressure.

Unlined stainless steel hoses are compatible with a wide range of fluids, including steam, gases, and water, without risk of lining erosion or contamination. Lined hoses may require frequent inspection and replacement when exposed to abrasive or reactive media. The absence of a lining allows greater flexibility and tighter bending radii, facilitating easier installation in confined or vibration-prone environments. Reduced risk of delamination or lining failure enhances service life, making unlined hoses the preferred choice in most industrial, HVAC, and power applications.

End-Use Industry Analysis

Corrugated Metal Flexible Hoses Are Mostly Utilized in the Chemical & Petrochemical Industry.

Among the end-use industries, 30.2% of the total global consumption of corrugated metal flexible hoses is in the chemical & petrochemical sector, due to the demanding combination of chemical aggressiveness, temperature extremes, and pressure variability in these environments. Corrugated stainless steel hoses can safely convey acids, alkalis, solvents, and corrosive gases without degradation, whereas alternative materials may fail or require frequent replacement.

Chemical processes often involve high temperatures, thermal cycling, and pressurized reactions, conditions well within the operational envelope of metallic hoses. Flexible hoses accommodate vibrations, misalignments, and thermal expansion in complex piping networks typical of chemical plants. These properties make chemical and petrochemical facilities the largest practical users, as other sectors often operate under less corrosive or lower-pressure conditions where alternative hoses suffice.

Key Market Segments

By Material

- Stainless Steel

- Galvanized Steel

- Bronze

- Others

By Diameter

- Small Bore (<1”)

- Medium Bore (1”-6”)

- Large Bore (>6”)

By Pressure Rating

- Low Pressure

- Medium Pressure

- High Pressure

By Liner Type

- Unlined

- Lined

By End-Use Industry

- Oil & Gas

- Chemical & Petrochemical

- Power Generation

- Automotive

- Aerospace

- HVAC

- Food & Beverage

- Others

Drivers

Oil & Gas Industry Demand Drives the Corrugated Metal Flexible Hoses Market.

Demand from the oil & gas industry constitutes a primary driver of corrugated metal flexible hoses due to operational, environmental, and reliability requirements across upstream-midstream systems for high-integrity fluid and gas transfer in extreme operating environments.

Corrugated hoses provide zero-permeation seals for volatile hydrocarbons where rubber alternatives are unsuitable. The hose and pipe systems are integral to hydrocarbon transport, including subsea flowlines, risers, and refinery transfer systems, where they handle high-pressure fluids and dynamic loading conditions. Offshore and deepwater developments, characterized by vessel motion, thermal expansion, and complex seabed geometries, necessitate flexible connections rather than rigid piping.

Around 70% of oil pipeline failures are attributed to corrosion, with 58% occurring internally. Flexible metallic hoses, designed for corrosion resistance and fatigue absorption, address these dominant failure modes. Their primary applications include blowout preventer (BOP) systems, kill and choke lines for well pressure management, and ship-to-shore hydrocarbon transfer.

Oil & gas demand drives adoption through high-pressure and dynamic operating conditions, corrosion-dominated failure risks, and capital-intensive offshore infrastructure requiring flexible, fatigue-resistant fluid transfer systems.

Restraints

Competition from Effective Substitutes Poses a Significant Hurdle to the Corrugated Metal Flexible Hoses Market.

The corrugated metal flexible hose market faces substitution challenges from advanced polymers and composite materials, primarily Polymeric Flexible Pipes (PFP) and Thermoplastic Composite Pipes (TCP). These substitutes target specific performance gaps in traditional metal assemblies.

The flexible pipe systems increasingly integrate polymer inner layers, such as HDPE, PA, and PVDF, for sealing and corrosion mitigation, reducing reliance on fully metallic constructions. Polymer hoses exhibit inherent resistance to acids, salts, and moisture without electrochemical degradation, unlike metals. This enables substitution in chemically aggressive but lower-pressure environments.

Unlike stainless steel grades (304/316L), susceptible to chloride-induced stress corrosion cracking (CSCC), TCP utilizing carbon fiber and PEEK or PVDF liners is chemically inert. According to subsea technology developers, TCP can reduce the total cost of ownership by up to 30% in offshore environments by eliminating corrosion-related maintenance.

The shift is regulated under frameworks such as API 17J (unbonded flexible pipe) and API 15S (spoolable reinforced plastic line pipe). These standards provide the institutional basis for operators to transition from metal to non-metallic flexible solutions in high-stakes energy infrastructure.

Opportunity

Application in HVAC and Power Generation Sectors Creates Opportunities in the Corrugated Metal Flexible Hoses Market.

Applications in HVAC and power generation constitute a structurally grounded opportunity for corrugated metal flexible hoses, supported by operational requirements for thermal management, vibration control, and high-temperature fluid transfer.

Corrugated metal hoses are used for steam, hot water, and high-temperature air, where elastomeric materials degrade, while also enabling leak-tight performance in dynamic HVAC assemblies. According to ASHRAE guidelines, metal hoses are used as vibration eliminators to prevent the transmission of self-excited vibration, often exceeding 5mm/s RMS, from compressors and pumps to rigid building structures. Industrial installations further use such hoses for refrigeration and air-conditioning lines, including non-permeable assemblies for vibration isolation.

In power plants, flexible metal hoses operate across steam lines, fuel delivery systems, cooling water circuits, and high-pressure lubrication lines. In thermoelectric plants, these hoses facilitate the transfer of steam and fuel gases at temperatures reaching thousands of degrees Fahrenheit. They are essential in cooling water systems, connecting cooling towers to generation equipment to manage high-volume flows and absorb pump-induced stress.

Trends

Increased Demand from the Aerospace Industry.

The aerospace industry is a primary driver for the corrugated metal flexible hose market, dictated by the transition toward high-performance fluid management in extreme flight and space environments. The demand is anchored in the requirement for components that maintain structural integrity under high-frequency vibration and cryogenic temperatures.

Aircraft and spacecraft incorporate extensive fluid transfer networks, including fuel, hydraulic, lubrication, and cooling, where flexible hoses are essential to connect moving and stationary components under vibration and motion. A single aircraft integrates multiple hose systems across fuel, oil, brake, and hydraulic circuits, indicating high component multiplicity per unit.

Aerospace hose systems routinely operate at pressures up to 3,000 psi in hydraulic applications and across wide temperature ranges, -65°F to 450°F for PTFE-lined assemblies. In space launch vehicles, corrugated hoses facilitate the transfer of liquid oxygen and liquid hydrogen at temperatures as low as -253°C, where polymer alternatives undergo embrittlement.

Geopolitical Impact Analysis

Geopolitical Tensions Have Led to Fluctuating Market Dynamics for the Corrugated Metal Flexible Hoses.

The geopolitical tensions exert a measurable, multi-channel impact on the corrugated metal flexible hoses market through supply disruption, infrastructure damage, and heightened operational risk in oil & gas systems.

The Strait of Hormuz carries around 20% of global oil and LNG flows, and disruption scenarios indicate potential losses of 13-14 million barrels/day. Simultaneously, attacks on Russian infrastructure have halted about 40% of export capacity, nearly 2 million barrels/day. Such disruptions force rerouting via alternative pipelines and terminals, increasing reliance on flexible, vibration-tolerant connectors in transport and loading systems.

Additionally, in June 2025, the U.S. government increased Section 232 tariffs on steel and aluminum to 50% for nearly all countries. This regulatory shift has led several organizations to pause or delay stainless steel orders, with 30% of industrial consumers switching suppliers to mitigate cost spikes. Furthermore, logistics managers rank geopolitical instability as the single greatest threat to supply chains, forcing a shift from cost-optimized to resilience-focused sourcing strategies.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Corrugated Metal Flexible Hoses Market.

In 2025, the Asia Pacific dominated the global corrugated metal flexible hoses market, holding about 40.5% of the total global consumption, supported by scale effects across energy, industrial, and infrastructure systems. A study by the International Energy Agency indicates that the Asia Pacific accounts for a substantial share of global oil consumption and imports, with hydrocarbons underpinning transport, petrochemicals, and industrial activity. The region’s energy systems rely heavily on pipelines, refineries, and LNG infrastructure, all of which require flexible, high-integrity fluid transfer components.

Additionally, the market is characterized by the localized dominance of stainless steel production. In 2025, global stainless steel production reached 64.2 million metric tons, with Asia accounting for 86.2% of this volume. China alone produced 40.8 million metric tons, representing 64% of total global output. Additionally, widespread use of natural gas in power generation and heating systems further expands pipeline and connector requirements.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of corrugated metal flexible hoses focus on a set of operational and product-centric strategies. Emphasis is placed on high-performance alloys and advanced corrugation designs to improve fatigue life, pressure tolerance, and corrosion resistance. Compliance with standards issued by organizations such as the American Society of Mechanical Engineers and the International Organization for Standardization is used to access regulated sectors.

Firms develop tailored assemblies for industries such as oil & gas, aerospace, and power, where operating conditions vary significantly. Automation, precision welding, and non-destructive testing enhance reliability and reduce failure rates in critical applications. Companies expand regional manufacturing footprints and provide value-added services such as on-site installation, inspection, and lifecycle maintenance. Collaboration with OEMs and EPC contractors supports integration into large infrastructure and industrial projects.

The Major Players in The Industry

- Parker Hannifin Corporation

- Swagelok Company

- Eaton Corporation

- OmegaFlex Inc.

- United Flexible

- Titeflex Corporation

- Hose Master LLC

- Penflex Corporation

- Senior Flexonics

- Kuri Tec Corporation

- Metalflex GmbH

- Flex-Hose Co.

- Ayvaz

- BOA Group

- Witzenmann GmbH

- Polyhose India Pvt. Ltd.

- TIPCO Technologies

- Other Key Players

Key Development

- In March 2024, Swagelok announced the release of new Swagelok FV series vacuum jacketed hoses in sizes 8, 12, and 16, with custom lengths available to meet specific needs.

- In April 2026, TIPCO Technologies announced the opening of its Danfoss Hose Center in Houston, representing continued efforts for the expansion.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$4.8 Bn |

| Forecast Revenue (2035) | US$6.9 Bn |

| CAGR (2026-2035) | 3.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (Stainless Steel, Galvanized Steel, Bronze, and Others), By Diameter (Small Bore (<1”), Medium Bore (1”-6”), and Large Bore (>6”)), By Pressure Rating (Low Pressure, Medium Pressure, and High Pressure), By Liner Type (Unlined and Lined), By End-Use Industry (Oil & Gas, Chemical & Petrochemical, Power Generation, Automotive, Aerospace, HVAC, Food & Beverage, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Parker Hannifin Corporation, Swagelok Company, Eaton Corporation, OmegaFlex Inc., United Flexible, Titeflex Corporation, Hose Master LLC, Penflex Corporation, Senior Flexonics, Kuri Tec Corporation, Metalflex GmbH, Flex-Hose Co., Ayvaz, BOA Group, Witzenmann GmbH, Polyhose India Pvt. Ltd., TIPCO Technologies, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |