Quick Navigation

Report Overview

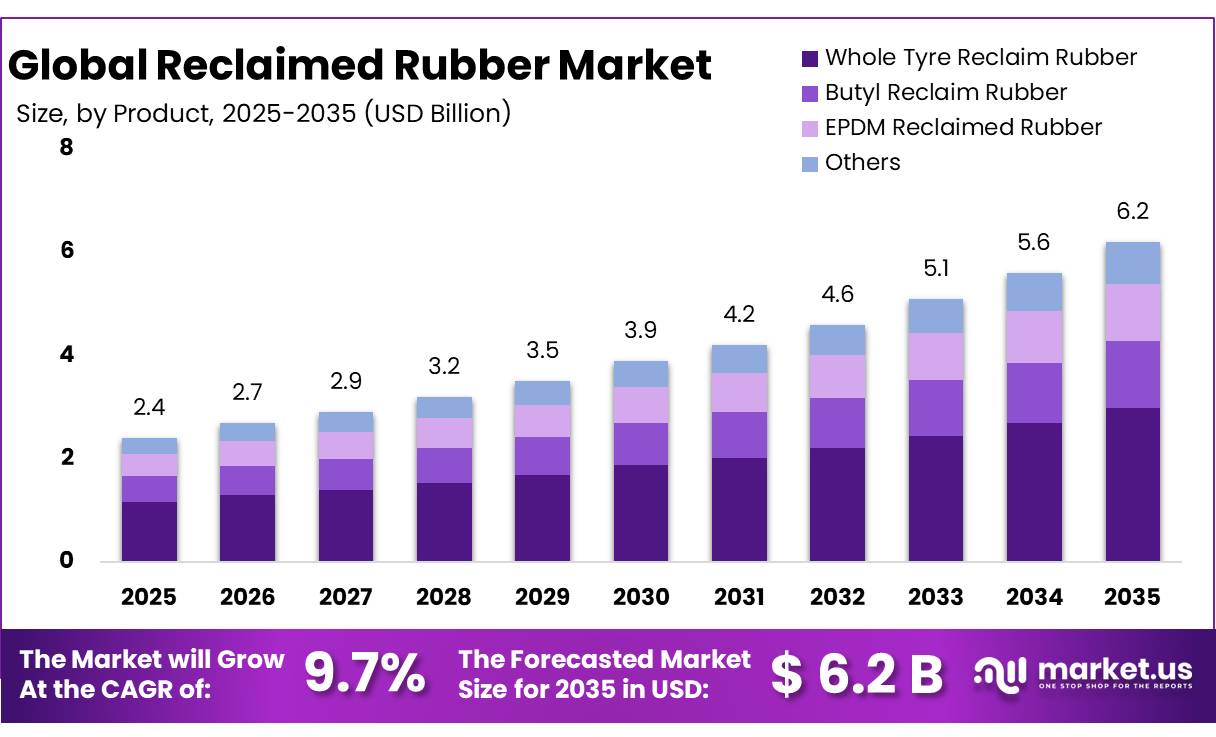

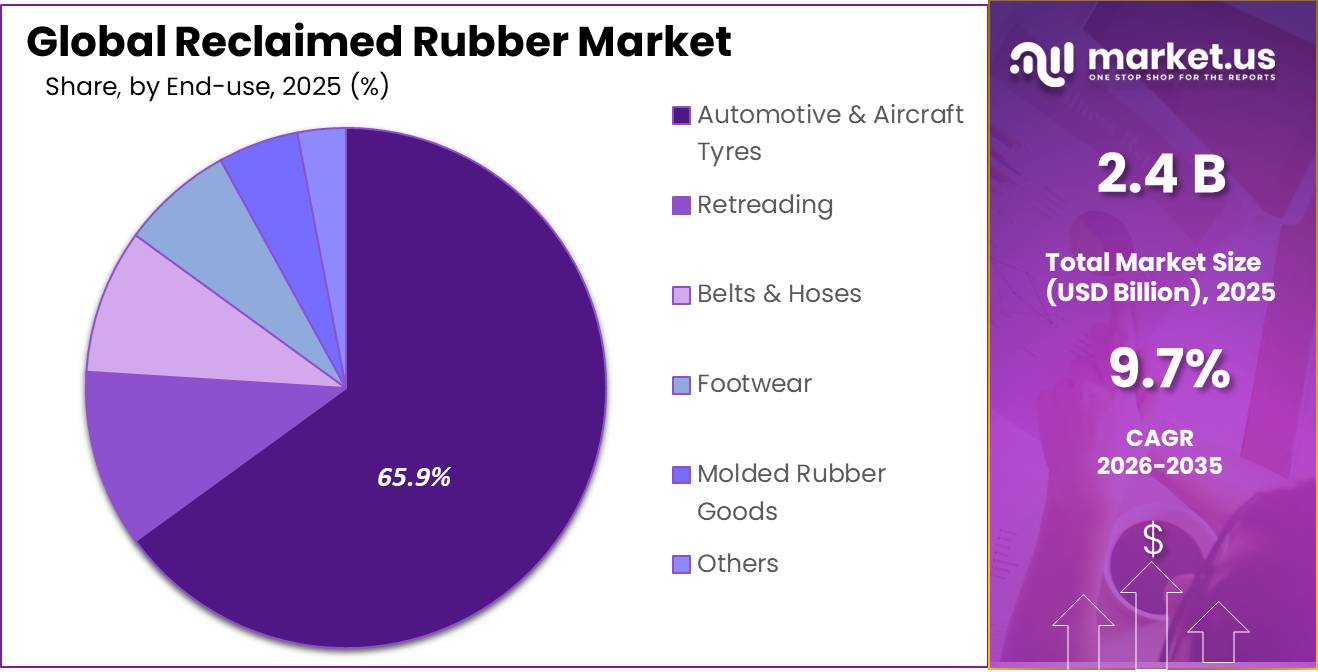

The Global Reclaimed Rubber Market size is expected to be worth around USD 6.2 Billion by 2035, from USD 2.4 Billion in 2025, growing at a CAGR of 9.7% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 54.8% share, holding USD 1.2 Billion revenue.

The reclaimed rubber coating industry is growing as manufacturers look for lower-cost and more sustainable rubber materials for coatings, mats, flooring, automotive parts, construction surfaces, and industrial layers. Reclaimed rubber is produced mainly from end-of-life tyres and rubber scrap, then processed into reusable material.

In Europe, tyres contain around 75% rubber, 15% steel, and 10% textile fibres, giving recyclers a strong material base for recovery. Around 50% of EU end-of-life tyres are mechanically recycled, and recycled rubber is used in sectors such as construction, agriculture, sports, and automotive applications.

The industrial scenario is supported by rising tyre waste treatment and stronger circular economy rules. In 2024, Europe generated about 3.9 million tonnes of end-of-life tyres, while the region achieved a 97% treatment rate. Material recovery from end-of-life tyres in Europe increased from 10% to 60% over the last 25 years, showing that recycling has moved from a waste-control activity to a serious raw-material supply chain.

A major driving factor is the need to reduce landfill use and create higher-value outlets for recycled rubber. In the U.S., 79% of end-of-life tyres were consumed by end-use markets in 2023, while ground rubber demand rose 29% since 2019. Rubber Modified Asphalt used 165,000 tons of end-of-life tyres since 2021, rising 17%, which shows growing acceptance of recycled rubber in infrastructure and coating-type applications.

Government and industry support is also creating future opportunities. In 2025, EuRIC and ETRMA called for EU-wide End-of-Waste rules for tyre-derived rubber, while the EU Circular Economy Act planned for 2026 aims to boost demand for recycled materials. These rules can improve trust, quality control, and cross-border trade for reclaimed rubber materials.

GRP Ltd positions itself as a circular materials company with five decades of recycling expertise across rubber, plastics and advanced recycling platforms. J. Allcock & Sons Ltd states that it recycles over 2,000 MT of rubber and has recycled over 1,000 MT of FKM to date, strengthening its relevance in specialist reclaimed and devulcanized rubber supply.

Key Takeaways

- Reclaimed Rubber Market size is expected to be worth around USD 6.2 Billion by 2035, from USD 2.4 Billion in 2025, growing at a CAGR of 9.7%.

- Whole Tyre Reclaim Rubber held a dominant market position, capturing more than a 48.3% share.

- Automotive & Aircraft Tyres held a dominant market position, capturing more than a 65.9% share.

- Asia-Pacific continues to lead the reclaimed rubber market, accounting for a dominant 54.8% share with an estimated value of USD 1.2 billion.

By Product Analysis

Whole Tyre Reclaim Rubber dominates with 48.3% driven by strong raw material availability and cost efficiency

In 2025, Whole Tyre Reclaim Rubber held a dominant market position, capturing more than a 48.3% share. This segment led the market mainly because whole tyres are widely available as scrap, making them an easy and economical source for reclaiming rubber. Manufacturers prefer this type as it offers a balanced mix of durability and processing flexibility, which suits a wide range of applications like footwear, automotive components, and industrial products.

By End-use Analysis

Automotive & Aircraft Tyres lead with 65.9% backed by strong replacement demand and continuous usage

In 2025, Automotive & Aircraft Tyres held a dominant market position, capturing more than a 65.9% share. This segment stayed ahead mainly because tyres are one of the largest users of rubber, and the need for replacement remains constant across both automotive and aviation sectors. Reclaimed rubber is widely used here to reduce production costs while still maintaining acceptable performance levels.

Key Market Segments

By Product

- Whole Tyre Reclaim Rubber

- Butyl Reclaim Rubber

- EPDM Reclaimed Rubber

- Others

By End-use

- Automotive & Aircraft Tyres

- Retreading

- Belts & Hoses

- Footwear

- Molded Rubber Goods

- Others

Emerging Trends

Circular tyre recycling is becoming the main trend

A major latest trend in reclaimed rubber is the shift from simple waste handling to circular tyre recycling. This means used tyres are being turned into useful rubber material for coatings, flooring, adhesives, moulded goods and industrial parts.

In Europe, the tyre industry has reached a 95% collection and treatment rate for end-of-life tyres, which gives manufacturers a strong recycled raw-material base. This trend is also supported by EU policy. In April 2025, the European Commission adopted its 2025–2030 Ecodesign for Sustainable Products Regulation working plan, which focuses on more circular and energy-efficient products.

Higher-value reclaimed rubber uses are gaining attention

The second strong trend is the movement toward higher-value applications instead of only low-grade recycling. Reclaimed rubber is now being used where flexibility, durability and lower raw-material cost matter, such as conveyor belts, adhesives, footwear, moulded components and coatings.

GRP Ltd lists non-tyre applications including conveyor belts, moulded components, adhesives and footwear, showing that reclaimed rubber is becoming more useful across industrial products. J. Allcock & Sons Ltd also remains connected with recycled and reclaimed rubber, and states that it has recycled over 2,000 MT of rubber and over 1,000 MT of FKM.

Drivers

Rising global tyre waste is pushing demand for reclaimed rubber

One of the biggest reasons behind the growth of reclaimed rubber is the huge amount of tyre waste being generated every year. Across the world, more than 1.5 to 1.8 billion waste tyres are produced annually, and this number keeps increasing with growing vehicle use. At the same time, around 13.5 million tonnes of waste tyres are generated globally each year, which creates serious pressure on landfills and the environment.

In countries like India, the situation is becoming more intense. Waste tyre generation has jumped from about 1.5 million tonnes in 2020 to over 2.8 million tonnes by 2026, showing how fast the problem is growing. Governments and environmental bodies are now actively promoting recycling to control pollution and reduce landfill waste. For example, policies linked to extended producer responsibility (EPR) are encouraging companies to reuse tyre materials instead of dumping them.

Strong recycling momentum and government push supporting market growth

Another major driving factor is the steady improvement in recycling systems and government-backed initiatives. Globally, the recycling rate of tyres has improved a lot, with over 1.8 billion tyres being recycled every year, which is about 85% of total tyre production. This shows that recycling is no longer a small activity—it has become a large-scale industrial process.

In developed regions, recycling rates are even stronger. For example, North America is able to recycle or reuse about 81% of its waste tyres annually, thanks to strict environmental rules and better infrastructure. Governments are also encouraging the use of recycled materials in roads, construction, and industrial products, which directly increases the use of reclaimed rubber.

Restraints

Quality inconsistency limits wider industrial acceptance

One of the key challenges holding back the reclaimed rubber market is the issue of inconsistent quality. Unlike virgin rubber, reclaimed rubber depends heavily on the type of waste material used, which can vary a lot. For example, tyres from trucks, passenger cars, and aircraft all have different compositions, and when mixed, they can affect the final product’s performance. According to industry estimates, nearly 20–25% variation in material properties can occur in reclaimed rubber batches, making it difficult for manufacturers to maintain uniform standards.

Government bodies like the Bureau of Indian Standards (BIS) have set guidelines to improve product quality, but implementation across small and medium recyclers is still uneven. Many smaller units lack advanced processing technology, which further adds to inconsistency. Because of this, large manufacturers often limit the percentage of reclaimed rubber in their products, especially in critical components.

Limited advanced recycling infrastructure in developing regions

Another major restraining factor is the lack of modern recycling infrastructure, especially in developing countries. While global tyre recycling rates are improving, not all regions have access to advanced reclaiming technology. For instance, although over 85% of tyres are recycled in developed markets, many developing regions still rely on informal or outdated recycling methods.

In countries like India, despite generating more than 2.8 million tonnes of waste tyres by 2026, a significant portion is still processed through unorganized sectors. The government has introduced initiatives such as Extended Producer Responsibility (EPR) to improve the situation, but the transition takes time. Setting up modern recycling plants requires high investment, skilled labor, and strict compliance with environmental norms, which many small players find difficult to manage.

Opportunity

Expanding use of recycled rubber in construction and infrastructure

One strong growth opportunity for reclaimed rubber is its rising use in construction and road development projects. Governments across the world are increasingly promoting sustainable materials, and recycled rubber is becoming a practical option. Today, the global tyre recycling system already processes around 15.2 million tonnes of tyre material every year, which is being converted into products like rubberized asphalt, flooring, and insulation materials.

Road construction is one of the biggest areas where this material is being used. Rubber mixed with asphalt improves road life, reduces noise, and handles temperature changes better than traditional materials. Because of these benefits, many governments are encouraging its use in public infrastructure projects. In Europe, strict landfill restrictions and circular economy policies are pushing industries to reuse tyre waste instead of dumping it.

Rising environmental pressure and circular economy goals creating new demand

Another major opportunity comes from the growing global focus on sustainability and waste reduction. Every year, more than 1.5 to 1.8 billion tyres reach end-of-life, creating a massive environmental challenge. At the same time, tyre waste contributes significantly to pollution, including microplastics, with about 6 million tonnes of tyre wear particles released globally each year.

Governments and environmental agencies are pushing industries to move toward a circular economy, where waste is reused instead of discarded. Policies like Extended Producer Responsibility (EPR) are making manufacturers responsible for managing tyre waste, which is directly increasing the demand for reclaimed rubber. In regions like Europe, recycling rates have already crossed 90% in some areas, showing how strong policy support can drive change.

Regional Insights

Asia-Pacific dominates with 54.8% share driven by strong industrial base and high tyre recycling volumes

Asia-Pacific continues to lead the reclaimed rubber market, accounting for a dominant 54.8% share with an estimated value of USD 1.2 billion, making it the most influential regional segment. The region’s leadership is largely supported by its strong automotive manufacturing ecosystem, large-scale tyre consumption, and growing recycling infrastructure. Globally, reclaimed rubber production reached around 3.2 million tons in 2024, with Asia-Pacific contributing a significant portion due to its high volume of end-of-life tyres and industrial demand.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

GRP Ltd, established in 1974, is one of the leading reclaimed rubber manufacturers with around 7 manufacturing units and an installed capacity of nearly 81,200 MT per year. The company’s reclaim rubber segment contributes close to 89% of its total revenue, showing strong business focus. It supplies products to 8 out of the top 10 global tyre manufacturers, highlighting its global reach. GRP has also helped recycle over 3.5 million end-of-life tyres, supporting sustainability and reducing landfill pressure significantly.

Fishfa Rubbers Ltd is a growing reclaimed rubber manufacturer with an estimated production capacity of around 24,000–30,000 MT per year. The company serves both domestic and export markets, supplying to tyre, footwear, and industrial rubber sectors. It has developed a stable distribution network across 25+ countries, supporting its international footprint. Fishfa focuses on improving processing efficiency and product consistency, which helps it compete with larger players while maintaining cost advantages in emerging markets.

Rolex Reclaim Pvt. Ltd is a key Indian player with a production capacity exceeding 36,000 MT annually, focusing on whole tyre and butyl reclaim rubber. The company exports to over 30+ countries, including major markets in Europe and North America. It operates with multiple production lines and maintains strong quality control systems to meet international standards. Rolex has built a solid presence in cost-effective reclaimed rubber solutions, especially for automotive and industrial applications, helping reduce dependency on virgin rubber materials.x

Top Key Players Outlook

- GRP Ltd

- J. Allcock & Sons Ltd

- Rolex Reclaim Pvt. Ltd.

- Fishfa Rubbers Ltd.

- HUXAR

- Tianyu (Shandong) Rubber & Plastic Products Co., Ltd.

- Swani Rubber Industries

- Minar Reclaimation Private Limited

- SRI Impex Pvt. Ltd.

- SNR Reclamations Pvt. Ltd.

- High Tech Reclaim Pvt. Ltd.

- Balaji Rubber Industries (P) Ltd.

- Star Polymers Inc.

Recent Industry Developments

In 2026, GRP Ltd is expanding its recycling capabilities by adding around 3,600 MT of reclaim capacity and investing in pyrolysis technology, which is expected to increase tyre recycling capacity by nearly 1.5–1.8 times.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.4 Bn |

| Forecast Revenue (2035) | USD 6.2 Bn |

| CAGR (2026-2035) | 9.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Whole Tyre Reclaim Rubber, Butyl Reclaim Rubber, EPDM Reclaimed Rubber, Others), By End-use (Automotive And Aircraft Tyres, Retreading, Belts And Hoses, Footwear, Molded Rubber Goods, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | GRP Ltd, J. Allcock & Sons Ltd, Rolex Reclaim Pvt. Ltd., Fishfa Rubbers Ltd., HUXAR, Tianyu (Shandong) Rubber & Plastic Products Co., Ltd., Swani Rubber Industries, Minar Reclaimation Private Limited, SRI Impex Pvt. Ltd., SNR Reclamations Pvt. Ltd., High Tech Reclaim Pvt. Ltd., Balaji Rubber Industries (P) Ltd., Star Polymers Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |