Quick Navigation

Report Overview

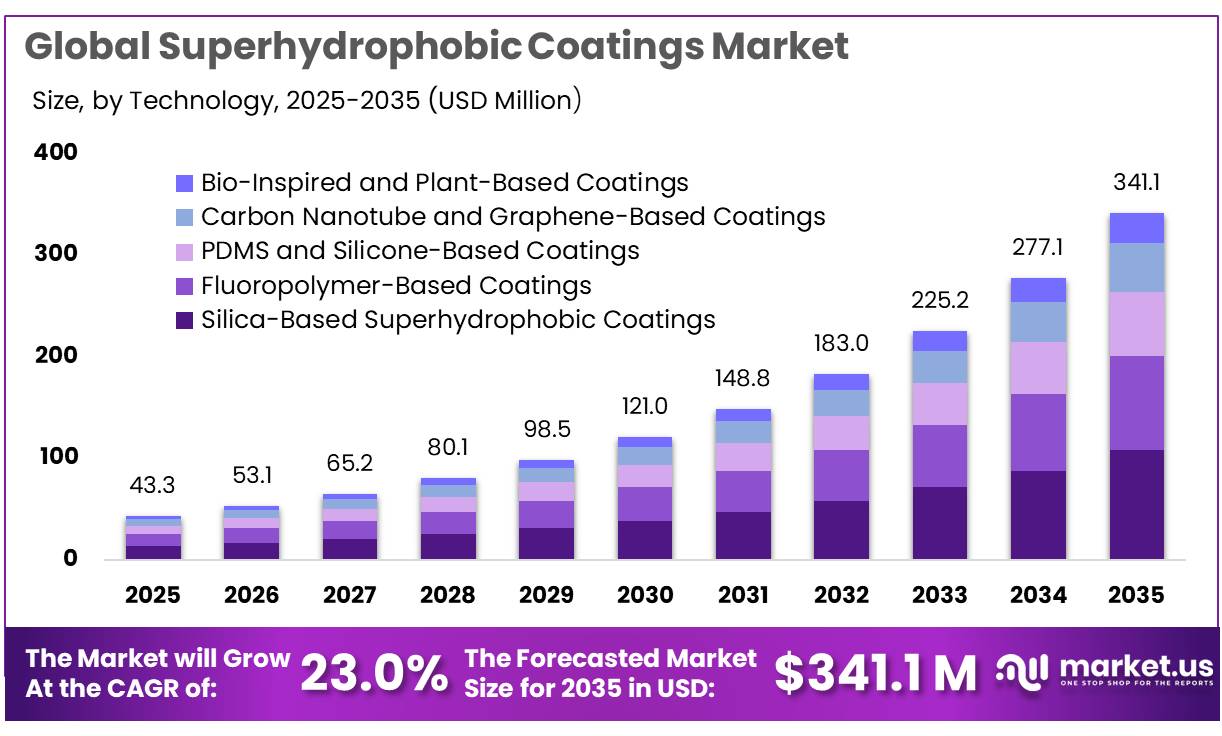

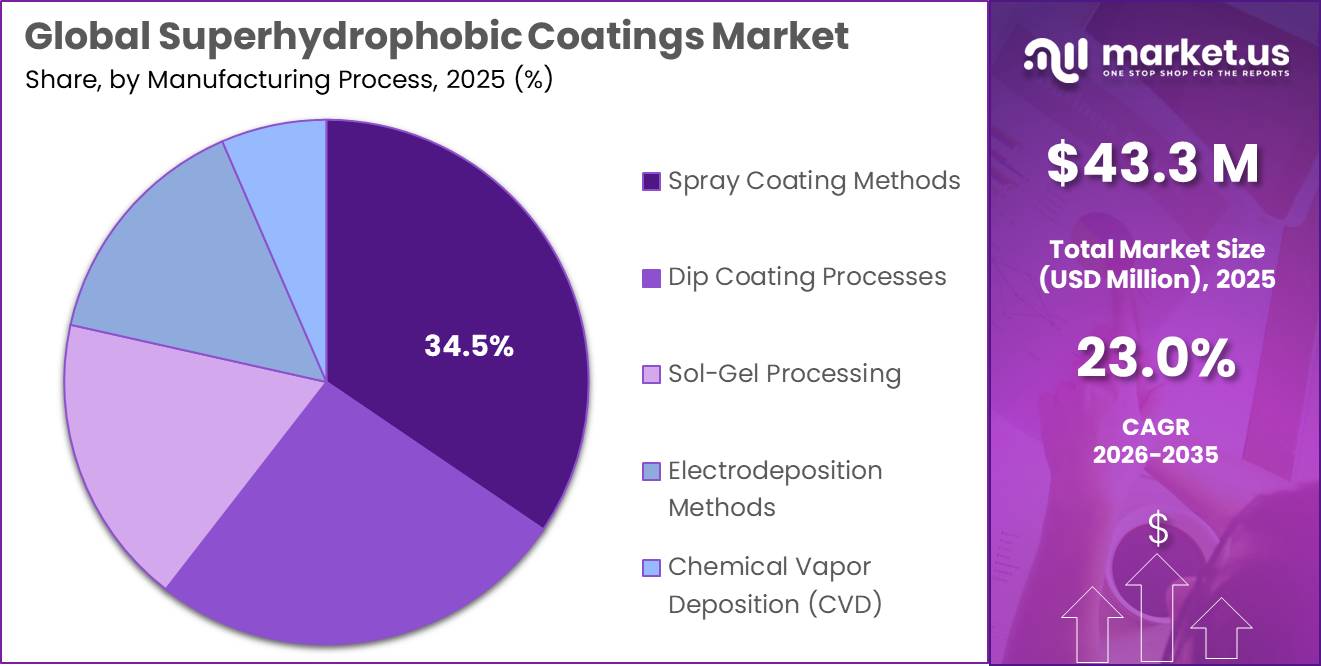

The Global Superhydrophobic Coatings Market size is expected to be worth around USD 341.1 Million by 2035, from USD 43.3 Million in 2025, growing at a CAGR of 23.0% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 43.8% share, holding USD 9.3 Billion revenue.

Superhydrophobic coatings are advanced surface-treatment systems that create extremely high water repellency, typically by combining low-surface-energy chemistry with nano/micro-textured surfaces. Industrially, they are gaining relevance in food processing equipment, packaging, cold-chain assets, electronics, automotive, marine, construction, medical devices, and renewable-energy components because they can reduce wetting, sticking, corrosion, icing, fouling, staining, and cleaning frequency. In the food ecosystem, the value proposition is tied to hygiene, residue reduction, and waste control: WHO estimates 600 million foodborne illness cases and 420,000 deaths annually, while unsafe food costs low- and middle-income economies about US$110 billion each year in productivity and medical expenses.

The industrial scenario is being shaped by hygiene, waste reduction and sustainability. FAO reports 13.2% global food loss between harvest and retail, and another 19% wasted at retail, food service and household levels; USDA/FDA estimate U.S. food waste at 30–40% of supply, equal to 133 billion pounds and US$161 billion in 2010 value. These figures support interest in self-cleaning, anti-fouling and easy-sanitize coatings for equipment, storage, packaging and transport surfaces.

Demand drivers include food-waste reduction, water-saving cleaning, longer asset life, and regulatory pressure for safer coating chemistries. UNEP estimated 1.05 billion tonnes of food waste in 2022, equal to 132 kg per capita, with households contributing 60%, food service 28%, and retail 12%. These figures support industrial opportunities for easy-release packaging, anti-fouling processing equipment, and lower-residue surfaces in food logistics, while non-food demand remains strong in electronics, automotive, aerospace, solar panels, and marine applications.

Government initiatives are also reshaping future opportunities. The EU Packaging and Packaging Waste Regulation entered into force in February 2025 and includes PFAS limits for food-contact packaging that apply from August 12, 2026. EFSA also notes European Commission monitoring of PFAS in food from 2022 to 2025, reinforcing demand for safer water- and grease-repellent alternatives.

Among key companies, 3M Company remains important because of its materials science, films, adhesives, and surface-technology platform. In 2025, 3M’s major development was its PFAS transition: the company had committed to exit all PFAS manufacturing and discontinue PFAS use across its product portfolio by the end of 2025, with manufactured PFAS previously representing about US$1.3 billion in annual net sales and roughly 16% EBITDA margins. 3M also reported US$1.1 billion in 2024 R&D spending, equal to 4.4% of sales, and more than 135,000 patents, supporting continued innovation in advanced materials and coatings.

Key Takeaways

- Superhydrophobic Coatings Market size is expected to be worth around USD 341.1 Million by 2035, from USD 43.3 Million in 2025, growing at a CAGR of 23.0%.

- Silica-Based Superhydrophobic Coatings held a dominant market position, capturing more than a 31.7% share.

- Spray Coating Methods held a dominant market position, capturing more than a 34.5% share.

- Automotive and Transportation held a dominant market position, capturing more than a 21.6% share.

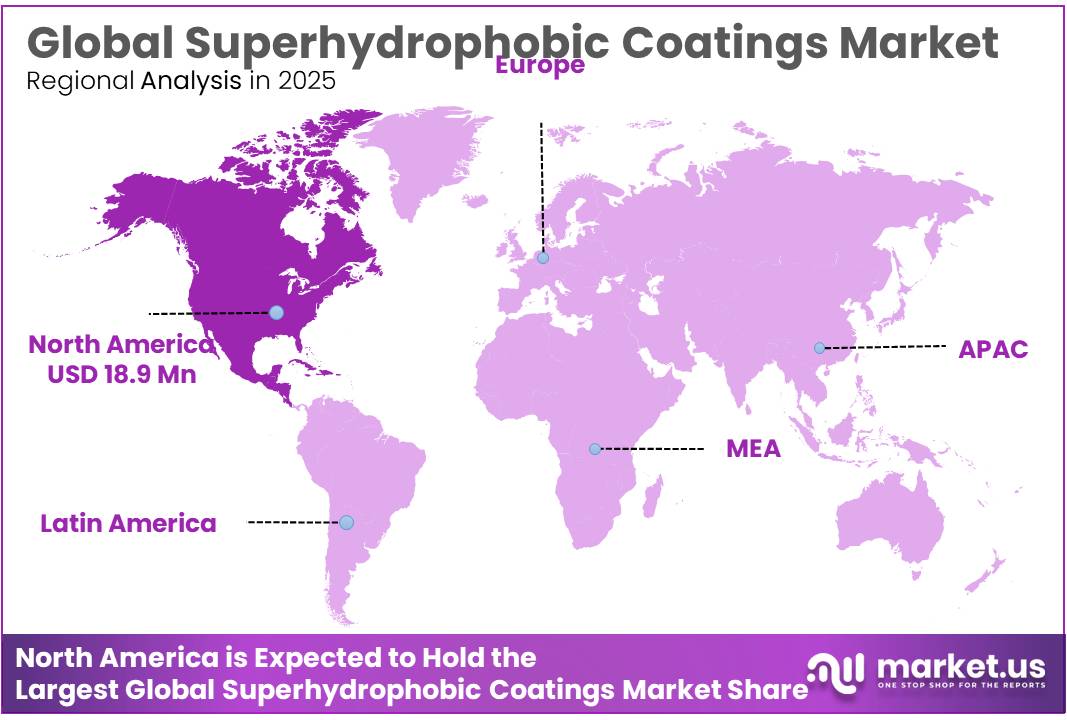

- Asia-Pacific continues to gain momentum. North America accounted for a leading 43.8% share, valued at around USD 18.9 million.

By Technology Analysis

Silica-Based Superhydrophobic Coatings dominate with 31.7% due to strong durability and cost-effective raw materials

In 2025, Silica-Based Superhydrophobic Coatings held a dominant market position, capturing more than a 31.7% share. This leadership came largely from the easy availability of silica and its strong compatibility with different coating surfaces such as glass, metals, and textiles. Manufacturers continued to prefer silica-based formulations because they offer a reliable balance between performance and cost, especially in large-scale industrial applications. These coatings also gained attention for their ability to provide long-lasting water repellency without requiring complex processing methods, which made them attractive for both developed and emerging markets.

By Manufacturing Process Analysis

Spray Coating Methods dominate with 34.5% thanks to easy application and scalability across industries

In 2025, Spray Coating Methods held a dominant market position, capturing more than a 34.5% share. This strong position came from how simple and flexible the process is compared to other coating techniques. Spray coating allows manufacturers to apply superhydrophobic layers quickly over large and uneven surfaces, which makes it widely useful in industries like automotive, construction, and electronics. It also does not require highly complex equipment, which helps reduce setup costs and makes it suitable for both small-scale and large-scale production. Because of this, many companies preferred spray methods to meet rising demand without heavy investment.

By Application Analysis

Automotive and Transportation leads with 21.6% driven by rising demand for protective and self-cleaning surfaces

In 2025, Automotive and Transportation held a dominant market position, capturing more than a 21.6% share. This growth was mainly supported by the increasing use of superhydrophobic coatings to protect vehicle surfaces from water, dust, and corrosion. Automakers started focusing more on improving vehicle durability and reducing maintenance needs, which made these coatings a practical choice. They were widely used on windshields, body panels, and sensor systems, helping improve visibility and performance in different weather conditions. The push for better aesthetics along with functional benefits also added to their demand in this sector.

Key Market Segments

By Technology

- Silica-Based Superhydrophobic Coatings

- Fluoropolymer-Based Coatings

- PDMS and Silicone-Based Coatings

- Carbon Nanotube and Graphene-Based Coatings

- Bio-Inspired and Plant-Based Coatings

By Manufacturing Process

- Spray Coating Methods

- Dip Coating Processes

- Sol-Gel Processing

- Electrodeposition Methods

- Chemical Vapor Deposition (CVD)

By Application

- Automotive and Transportation

- Aerospace and Defense

- Marine and Offshore

- Construction and Architecture

- Textiles and Apparel

- Electronics and Telecommunications

- Medical and Healthcare

- Solar Energy and Renewable

- Others

Emerging Trends

Shift Toward Smart and Sustainable Food Packaging is Emerging as a Key Trend

One of the most noticeable trends in the superhydrophobic coatings market is the move toward smarter and more sustainable food packaging solutions. The reason behind this shift is quite clear—food waste is still at a massive level globally. According to the United Nations Environment Programme, around 1.05 billion tonnes of food were wasted in 2022, which equals nearly 19% of food available to consumers. This has pushed industries to rethink how packaging can do more than just contain food.

Superhydrophobic coatings are now being explored as part of next-generation packaging that can repel moisture, reduce residue sticking, and keep food fresh for longer. Governments are also supporting this trend through initiatives linked to Sustainable Development Goal 12.3, which focuses on cutting global food waste by half by 2030. In 2025–2026, food companies are gradually shifting toward packaging that not only protects but also improves efficiency in storage and transportation. The idea is simple—if packaging can reduce even a small percentage of waste, it can save millions of tonnes of food globally.

Increasing Focus on Cold Chain Efficiency and Moisture Control

Another important trend is the rising focus on improving cold chain systems and moisture control across the food supply chain. A significant portion of food is lost before it even reaches consumers. The Food and Agriculture Organization estimates that about 13% of food—around 1.25 billion tonnes—is lost after harvest and before retail. Much of this loss is linked to poor storage conditions, temperature issues, and moisture exposure during transport.

Governments and organizations like FAO are also encouraging investments in cold chain infrastructure to reduce losses and improve food security. In 2026, this trend is becoming more visible, especially in developing regions where improving storage efficiency can directly impact food availability. As food demand continues to rise and supply chains become more complex, the need for better moisture control is pushing the adoption of these coatings in real-world applications.

Drivers

Rising Need to Reduce Food Waste Driving Demand for Protective Coatings

One of the strongest drivers for superhydrophobic coatings is the growing global focus on reducing food waste and improving storage efficiency. According to the Food and Agriculture Organization (FAO), around 13% of food—about 1.25 billion tonnes—is lost between harvest and retail, while an additional 19% is wasted at retail and consumer levels. This huge loss pushes industries to look for better surface protection technologies that can extend shelf life and reduce spoilage. Superhydrophobic coatings help by creating water-repellent surfaces on packaging, storage units, and processing equipment, preventing moisture buildup that often leads to bacterial growth and food degradation.

Governments and global organizations are actively supporting this shift. Under the United Nations Sustainable Development Goal 12.3, countries are working to cut food waste by half by 2030. This has encouraged investments in better storage infrastructure and advanced coating technologies. In 2026, many food processing companies started adopting these coatings in cold chains and transport systems to reduce losses during transit. The need is simple—less moisture, less spoilage, and more usable food.

Environmental Pressure and Emission Reduction Initiatives Supporting Market Growth

Another key factor driving the market is the environmental impact linked to food waste and inefficient food systems. Data from the United Nations Environment Programme shows that food loss and waste contribute nearly 8–10% of global greenhouse gas emissions. This is a major concern for governments trying to meet climate targets. When food spoils due to moisture or contamination, it wastes not only the product but also water, energy, and land used in production. This is where superhydrophobic coatings play a practical role by improving hygiene and reducing contamination risks in food handling and storage environments.

Several countries began strengthening policies around sustainable packaging and food preservation technologies. For example, initiatives linked to climate action plans and circular economy models are encouraging industries to use coatings that reduce waste and improve efficiency. Studies also show that about 60% of food waste comes from households, which highlights the importance of better packaging solutions.

Restraints

High Production Cost and Limited Scalability Restrains Wider Adoption

One of the biggest challenges for superhydrophobic coatings is their high production cost and difficulty in scaling for large industries like food processing and packaging. While the technology performs well in labs, applying it on a mass scale—especially in food-related environments—remains expensive. Food industries operate on thin margins, and even small cost increases can slow down adoption. This becomes more critical when we look at the scale of food handling globally. According to the Food and Agriculture Organization, about 13.3% of food, equal to nearly 1.31 billion tonnes, is lost before it even reaches retail.

To prevent such losses, industries need affordable solutions that can be applied widely across storage units, transport systems, and packaging materials. However, superhydrophobic coatings often require specialized materials and processes, which increase overall costs. Governments and organizations are pushing for better food preservation under initiatives like SDG 12.3, but industries still hesitate due to budget constraints. In 2025–2026, this gap between technology capability and cost practicality continues to limit adoption, especially in developing regions where infrastructure investment is already a challenge.

Regulatory and Safety Concerns in Food-Contact Applications

Another major restraint comes from strict safety regulations when these coatings are used in food-related environments. Any material that comes in contact with food must pass detailed safety checks, and this slows down the adoption of new coating technologies. Superhydrophobic coatings often involve nano-scale materials, and there is still ongoing discussion about their long-term safety in food packaging or processing surfaces. This makes regulatory approvals longer and more complex.

The need for safe solutions becomes clearer when looking at global food waste patterns. Data from the United Nations Environment Programme shows that around 19% of food available to consumers is wasted, with households alone responsible for nearly 60% of that waste. This highlights the importance of better storage and handling systems—but also the need for materials that are fully safe. Governments are introducing stricter guidelines to ensure food safety, which is necessary but also slows innovation.

Opportunity

Expanding Demand for Advanced Food Packaging Solutions Creating Growth Opportunities

One of the biggest growth opportunities for superhydrophobic coatings is in advanced food packaging, where the focus is shifting toward reducing waste and improving product shelf life. Globally, around 1.05 billion tonnes of food were wasted in 2022, which equals nearly 19% of all food available to consumers. This massive loss clearly shows the need for better packaging systems that can protect food from moisture, contamination, and spoilage. Superhydrophobic coatings help here by creating water-repellent surfaces that prevent liquids from sticking, which keeps food fresher for longer periods.

Governments and international organizations are actively promoting better packaging under initiatives linked to the United Nations Sustainable Development Goal 12.3, which aims to cut global food waste by half by 2030. Many food companies in 2025–2026 are already exploring coated packaging materials that reduce leakage and improve hygiene. This is especially useful for liquid foods, dairy, and ready-to-eat products where residue loss is common. As food demand grows and supply chains become longer, the need for efficient packaging is increasing.

Growth in Cold Chain and Storage Infrastructure Supporting Adoption

Another strong opportunity comes from the rapid expansion of cold chain systems and food storage infrastructure across the world. A large portion of food loss happens during transportation and storage due to poor handling and moisture exposure. In fact, about 13% of food is lost in the supply chain before it even reaches retail. This highlights a major gap where better surface protection can make a difference.

Governments have been investing heavily in improving food logistics, especially in developing countries where storage losses are higher. Programs supported by organizations like the FAO are encouraging better cold storage facilities and efficient transport systems. At the same time, rising urban populations and changing food consumption patterns are increasing pressure on supply chains to deliver fresh food over longer distances.

Regional Insights

North America leads with 43.8% (USD 18.9 Mn) while Asia-Pacific emerges as the fastest-growing regional market

The global superhydrophobic coatings market shows a strong regional divide, with North America maintaining its dominant position while Asia-Pacific continues to gain momentum. North America accounted for a leading 43.8% share, valued at around USD 18.9 million, supported by its advanced industrial base and strong presence of aerospace, automotive, and electronics sectors.

The region benefits from well-established research infrastructure and continuous investment in nanotechnology and material innovation, which has accelerated the commercial use of high-performance coatings. In addition, strict environmental regulations and the push toward PFAS-free and sustainable coatings have encouraged companies to adopt advanced formulations, further strengthening the region’s leadership.

Government-led initiatives such as smart city development, renewable energy projects, and manufacturing expansion programs are further boosting demand for advanced coatings across Asia-Pacific. The increasing use of superhydrophobic coatings in solar panels, consumer electronics, and public infrastructure is also supporting regional growth. While North America continues to dominate in terms of technological advancement and revenue, Asia-Pacific is quickly catching up due to its large-scale production capabilities and rising adoption across multiple industries, making it a key region for future market expansion.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

3M Company holds a strong position in the superhydrophobic coatings market, supported by its wide product portfolio and global reach across more than 70 countries. The company invests nearly 5–6% of its annual revenue in R&D, which helps it continuously innovate surface protection technologies. Its coating solutions like Scotchgard and Novec are widely used in electronics, automotive, and industrial sectors. With over 55,000 products and millions of customers globally, 3M benefits from large-scale adoption and strong distribution networks.

BASF SE is one of the largest chemical companies in the world, operating in more than 90 countries with over 110,000 employees. The company leverages its strong chemical manufacturing base to develop advanced coating materials, including hydrophobic and superhydrophobic solutions. BASF invests billions annually in innovation, allowing it to develop sustainable and high-performance coatings. Its products are widely used in construction, automotive, and industrial sectors, making it a major contributor to the coatings value chain and global supply network.

Top Key Players Outlook

- 3M Company

- Aculon, Inc.

- Advanced NanoTech Lab

- BASF SE

- Cytonix, LLC

- DryWired

- Hydrobead

- Lotus Leaf Coatings, Inc.

- NEI Corporation

- Nanex Company

Recent Industry Developments

By 2026, 3M’s strategy is clearly shifting toward more sustainable coatings, especially with its decision to phase out PFAS-based chemistries by the end of 2025, impacting a business segment valued at roughly USD 1.3 billion in annual sales.

By 2026, Advanced NanoTech Lab is increasingly focusing on high-efficiency applications such as solar panels, where its coatings can help reduce energy loss of up to 30% caused by dust accumulation, improving overall system output.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 43.3 Mn |

| Forecast Revenue (2035) | USD 341.1 Mn |

| CAGR (2026-2035) | 23.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Silica-Based Superhydrophobic Coatings, Fluoropolymer-Based Coatings, PDMS and Silicone-Based Coatings, Carbon Nanotube and Graphene-Based Coatings, Bio-Inspired and Plant-Based Coatings), By Manufacturing Process (Spray Coating Methods, Dip Coating Processes, Sol-Gel Processing, Electrodeposition Methods, Chemical Vapor Deposition (CVD)), By Application (Automotive and Transportation, Aerospace and Defense, Marine and Offshore, Construction and Architecture, Textiles and Apparel, Electronics and Telecommunications, Medical and Healthcare, Solar Energy and Renewable, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | 3M Company, Aculon, Inc., Advanced NanoTech Lab, BASF SE, Cytonix, LLC, DryWired, Hydrobead, Lotus Leaf Coatings, Inc., NEI Corporation, Nanex Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |