Quick Navigation

Report Overview

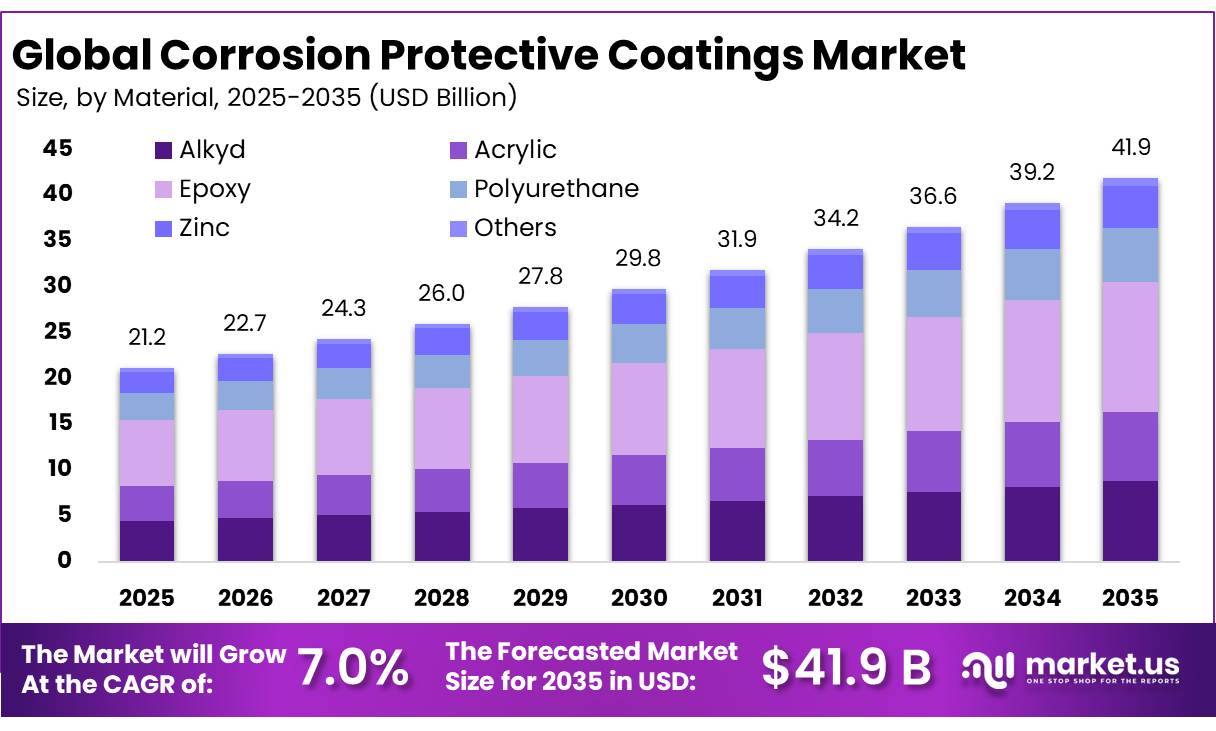

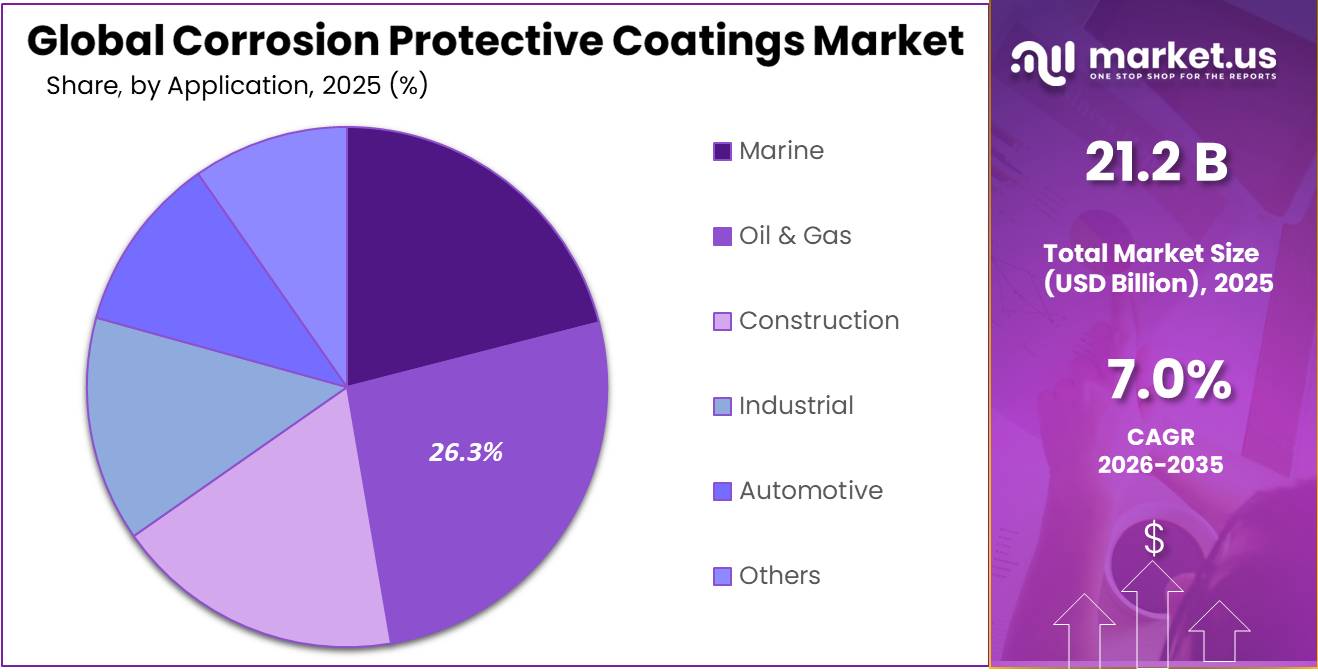

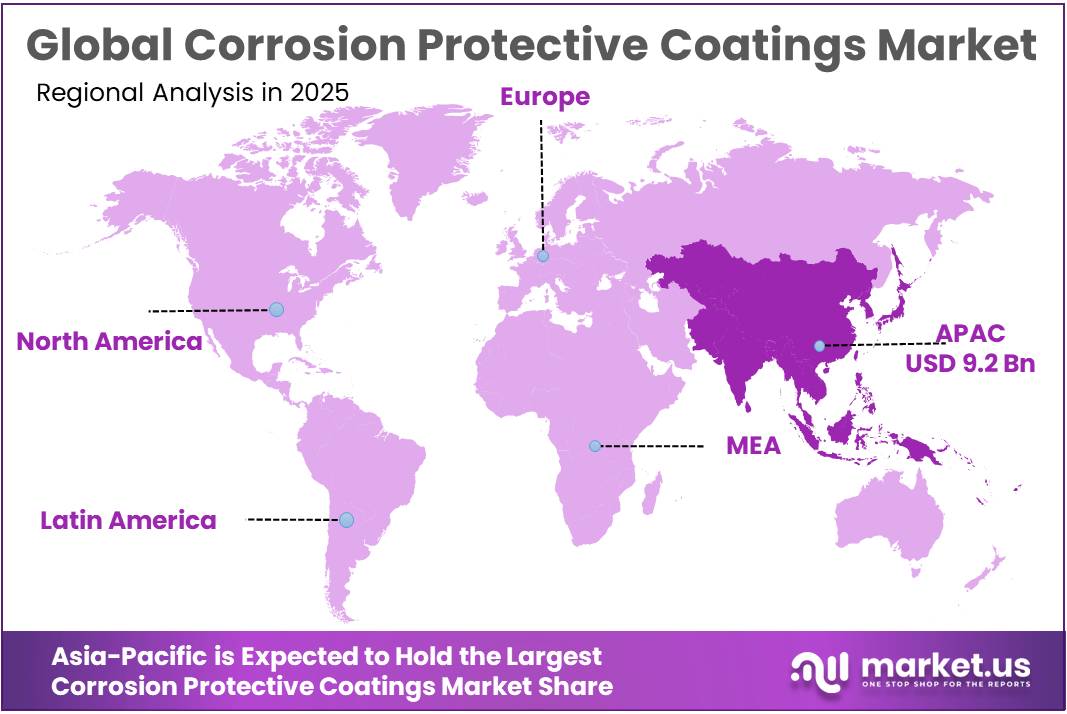

The Global Corrosion Protective Coatings Market size is expected to be worth around USD 41.9 Billion by 2035, from USD 21.2 Billion in 2025, growing at a CAGR of 7.0% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 43.4% share, holding USD 9.2 Billion revenue.

Corrosion protective coatings are specialized barrier, sacrificial, and inhibitive systems used to protect steel, concrete, pipelines, bridges, marine assets, ports, industrial plants, wind structures, and transportation equipment from degradation. The industrial relevance is high because AMPP/NACE estimates the global cost of corrosion at US$2.5 trillion, equal to 3.4% of global GDP, while better corrosion-control practices can save up to 35% of these costs.

The industry scenario is being shaped by infrastructure renewal, marine trade, energy transition, and stricter environmental regulation. In the U.S., the Bipartisan Infrastructure Law had announced US$591 billion for more than 72,000 projects by January 2025, while EPA water programs include more than US$50 billion, including US$20+ billion for drinking water and US$12+ billion for clean water—areas where corrosion-resistant coatings are essential for pipes, tanks and treatment assets.

The market scenario is being shaped by infrastructure renewal, stricter asset-integrity rules and demand for lower-VOC, longer-life coating systems. In the U.S., the Bipartisan Infrastructure Law supports roads, bridges, rail, ports and airports, including US$17 billion for ports and waterways and US$25 billion for airports, creating durable demand for protective coatings on exposed metal structures.

Demand is also supported by renewable-energy construction. The IEA expects 5,500 GW of new renewable capacity to become operational by 2030, with annual additions reaching almost 940 GW by 2030; solar and wind represent 95% of expected growth, increasing the need for corrosion-resistant coatings in towers, offshore foundations, substations, and industrial components.

Europe also supports long-term opportunities through clean-technology manufacturing policy. The EU Net-Zero Industry Act targets 40% domestic production of key clean technologies by 2030 and 15% global production share by 2040, supporting wind, electrolyzers, carbon capture and other assets that need corrosion protection in harsh operating environments.

Akzo Nobel N.V. remains a major participant through marine, protective, powder, and performance coatings. Its 2025 annual report states revenue of €10,158 million, while another credit-source summary notes around 60% of 2025 revenue came from performance coatings.

Key Takeaways

- Corrosion Protective Coatings Market size is expected to be worth around USD 41.9 Billion by 2035, from USD 21.2 Billion in 2025, growing at a CAGR of 7.0%.

- Solvent-borne held a dominant market position, capturing more than a 54.8% share.

- Epoxy held a dominant market position, capturing more than a 34.5% share.

- Oil & Gas held a dominant market position, capturing more than a 26.3% share.

- Asia-Pacific region stands out as the leading contributor, accounting for a dominant 43.4% share with a market value of around USD 9.2 Bn.

By Product Analysis

Solvent-borne dominates with 54.8% driven by strong industrial demand and proven performance

In 2025, Solvent-borne held a dominant market position, capturing more than a 54.8% share. This strong presence is mainly supported by its long-standing use across heavy industries such as oil & gas, marine, and infrastructure, where durability and high-performance protection are critical. Solvent-borne coatings are widely preferred because they offer excellent adhesion, corrosion resistance, and faster drying even in challenging environmental conditions. Many industrial operators continue to rely on these coatings due to their consistent results and compatibility with existing application systems.

By Material Analysis

Epoxy dominates with 34.5% due to its strong durability and wide industrial use

In 2025, Epoxy held a dominant market position, capturing more than a 34.5% share. This leadership is mainly due to its excellent resistance to corrosion, chemicals, and moisture, making it a preferred choice across industries like marine, oil & gas, and construction. Epoxy coatings are known for their strong bonding ability and long service life, which reduces the need for frequent maintenance. Many industries continue to rely on epoxy systems for protecting metal surfaces, pipelines, and structural assets exposed to harsh environments.

By Application Analysis

Oil & Gas dominates with 26.3% driven by constant need for asset protection in harsh environments

In 2025, Oil & Gas held a dominant market position, capturing more than a 26.3% share. This is largely because the sector operates in extremely corrosive environments, including offshore platforms, pipelines, and refineries, where protection against rust and chemical damage is essential. Corrosion protective coatings are widely used to extend the life of equipment and reduce costly shutdowns. The industry’s focus on safety, reliability, and long-term performance continues to support steady demand for high-quality coatings.

Key Market Segments

By Product

- Solvent-borne

- Water-borne

- Powder Coatings

By Material

- Alkyd

- Acrylic

- Epoxy

- Polyurethane

- Zinc

- Others

By Application

- Marine

- Oil & Gas

- Construction

- Industrial

- Automotive

- Others

Emerging Trends

Shift toward eco-friendly coatings gaining strong momentum

One of the most noticeable trends in corrosion protective coatings is the clear move toward environmentally friendly solutions. Industries, including food processing, are under growing pressure to reduce harmful emissions and use safer materials. Traditional coatings often release volatile organic compounds (VOCs), which are now being restricted under global regulations. For example, European policies like REACH have already phased out hazardous materials such as hexavalent chromium by 2024, pushing industries toward safer alternatives.

In 2025, this shift is becoming more practical, with many companies adopting water-based and low-VOC coatings that are safer for both workers and food environments. These coatings are especially important in food industries where hygiene and contamination risks must be controlled. By 2026, the trend is expected to grow stronger as governments tighten emission standards and industries align with sustainability goals.

Rapid growth of water-based coatings driven by food industry needs

Another important trend is the rising use of water-based corrosion protective coatings, especially in industries that require high cleanliness standards like food processing. These coatings are gaining attention because they reduce toxic emissions while still offering good protection against corrosion. In fact, the global water-based anti-corrosion coatings segment reached around $10.74 billion in 2025, showing how quickly industries are shifting toward these safer solutions.

In 2025, food manufacturers are increasingly choosing these coatings for equipment, storage systems, and processing lines, as they help maintain hygiene while meeting environmental guidelines. The presence of acids, cleaning chemicals, and moisture in food plants creates harsh conditions, making protective coatings essential. By 2026, adoption is expected to rise further as industries look for coatings that balance safety, performance, and sustainability.

Drivers

Rising food industry corrosion costs pushing demand for protective coatings

One of the strongest drivers for corrosion protective coatings is the growing need to control damage and cost in the global food processing industry. Equipment used in food factories is constantly exposed to water, acids, cleaning chemicals, and high-pressure washdowns, all of which create a highly corrosive environment. Because of this, industries are increasingly relying on coatings to protect surfaces and maintain hygiene standards. According to NACE International, the food processing sector spends nearly $2.1 billion annually on corrosion-related costs, which clearly shows how serious the issue has become.

In 2025, this cost pressure continues to push manufacturers to invest in long-lasting protective coatings to reduce maintenance and avoid frequent equipment replacement. Corrosion not only damages machinery but also affects production efficiency and increases downtime. By 2026, industries are expected to focus even more on preventive solutions rather than reactive repairs. This shift naturally increases the adoption of corrosion-resistant coatings, as companies try to control operational expenses and improve equipment lifespan in a cost-sensitive environment.

Strict food safety regulations and hygiene standards boosting coating demand

Another major driver comes from the need to meet strict food safety and hygiene regulations. In food processing plants, even minor corrosion can lead to contamination risks, which directly affects product quality and consumer health. Regulatory bodies and food safety standards require equipment surfaces to be corrosion-resistant, smooth, and easy to clean to avoid bacterial growth. Studies show that food processing environments require materials that resist corrosion caused by moisture and low pH conditions to maintain product safety.

In 2025, industries are under increasing pressure to maintain compliance with safety norms, especially as global food demand rises. Corroded surfaces can harbor bacteria and lead to contamination, making coatings essential for safe operations. By 2026, this trend becomes even stronger as companies invest more in protective coatings to ensure hygiene and avoid recalls or safety issues. The use of coatings is no longer optional but a necessary step to meet both regulatory requirements and consumer expectations for safe food production.

Restraints

High cost of compliance and maintenance limiting coating adoption

One of the biggest challenges for corrosion protective coatings is the high cost involved in meeting strict food industry standards. In food processing environments, coatings must not only prevent corrosion but also meet hygiene and safety rules, which increases material and application costs. This becomes a concern especially for small and mid-sized food manufacturers who operate on tight budgets. At the same time, the global food system already faces heavy losses, with nearly 931 million tonnes of food wasted every year, according to the United Nations Environment Programme.

In 2025, many companies are trying to balance between investing in high-quality coatings and managing operational costs. When margins are already affected by food losses and supply chain inefficiencies, spending more on premium coatings becomes a difficult decision.

Environmental regulations and safety concerns slowing product usage

Another important restraint comes from increasing environmental and safety regulations around coating materials. Many traditional coatings contain chemicals that can release harmful emissions or residues, which is a serious concern in food-related industries. Governments and regulatory bodies are tightening rules to ensure safer materials are used, especially in areas where coatings come in contact with food processing equipment.

In 2025, industries are under pressure to shift toward eco-friendly and low-emission coatings, but these alternatives are often more expensive and may not always match the performance of traditional solutions. This creates hesitation among manufacturers who rely on proven systems. By 2026, the situation becomes more complex as sustainability goals push companies to reduce environmental impact while still maintaining durability and protection.

Opportunity

Expansion of food processing infrastructure creating new coating demand

One of the strongest growth opportunities for corrosion protective coatings comes from the rapid expansion of food processing infrastructure, especially supported by government initiatives. In India, the Ministry of Food Processing Industries has been actively promoting large-scale development through schemes like Mega Food Parks. Under this plan, the government provides grants of up to ₹50 crore for each food park, with an expectation of attracting at least ₹250 crore in private investment and setting up 30–35 processing units per park.

In 2025, this kind of infrastructure growth is directly increasing the demand for corrosion-resistant coatings, as food processing plants require clean, durable, and long-lasting surfaces. Equipment, storage tanks, pipelines, and flooring in these facilities are constantly exposed to moisture, chemicals, and cleaning agents. By 2026, as more food parks and processing units become operational, the need for protective coatings is expected to rise further. This creates a clear opportunity for coating manufacturers to supply solutions tailored for hygiene and durability.

Rising global food demand increasing need for safe and durable coatings

Another major opportunity comes from the steady increase in global food demand, which is pushing industries to scale up production while maintaining safety standards. As food production grows, so does the need for reliable infrastructure that can operate without contamination risks. Corrosion can damage equipment surfaces, leading to hygiene concerns, which is why coatings are becoming essential rather than optional.

In 2025, food processing industries are focusing more on efficiency and long-term reliability, especially in large-scale facilities. Government-backed policies and structured industry growth are encouraging companies to invest in better materials and protective systems. By 2026, this trend strengthens as producers aim to reduce losses, improve shelf life, and maintain quality during processing and storage. Protective coatings play a key role here by ensuring that machinery and surfaces remain intact and safe over time.

Regional Insights

Asia-Pacific dominates with 43.4% share valued at USD 9.2 Bn driven by rapid industrialization and infrastructure growth

In the corrosion protective coatings market, the Asia-Pacific region stands out as the leading contributor, accounting for a dominant 43.4% share with a market value of around USD 9.2 Bn. This strong position is mainly supported by the region’s large industrial base, expanding construction activities, and growing investments in infrastructure.

Countries like China, India, Japan, and Southeast Asian nations continue to invest heavily in sectors such as oil & gas, marine, power generation, and transportation, all of which require advanced corrosion protection solutions. The region also benefits from its massive population base, with Asia alone housing nearly 60% of the world’s population, which directly supports industrial expansion and urban development.

In 2025, the demand for corrosion protective coatings in Asia-Pacific is driven by continuous infrastructure upgrades, including bridges, highways, ports, and industrial plants. Governments across the region are actively supporting manufacturing and construction through initiatives aimed at boosting economic growth and industrial output.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Akzo Nobel N.V. is a leading global coatings player with a strong focus on protective and marine coatings. In 2025, the company reported revenue of around $11.49 billion, reflecting its wide industrial presence across more than 150 countries. Its performance coatings segment continues to support corrosion protection demand, especially in infrastructure and marine sectors. The company also reported adjusted EBITDA of nearly €1.44 billion in 2025, showing stable operational strength despite market fluctuations.

PPG Industries, Inc. is one of the largest coatings manufacturers globally, operating in over 70 countries with around 46,000 employees. In 2025, the company generated net sales of approximately $15.9 billion, supported by strong demand in aerospace, marine, and protective coatings. Its performance coatings segment alone reported quarterly sales of about $1.33 billion in 2026, showing steady growth in corrosion-resistant applications.

Jotun is a well-established coatings company specializing in marine and protective coatings. In 2025, the company reported revenue of about 34,333 million NOK with a workforce of nearly 10,933 employees globally. It operates across more than 100 countries, with strong demand from shipping, offshore, and infrastructure sectors. Jotun’s protective coatings segment plays a key role in corrosion prevention, especially in harsh marine environments.

Top Key Players Outlook

- Akzo Nobel N.V.

- PPG Industries, Inc.

- Jotun

- Sherwin Williams Co.

- Kansai Paint Co., Ltd.

- 3M

- Sika AG

- Axalta Coating Systems Ltd.

- BASF SE

- Nippon Paint Holdings Co., Ltd.

- NYCOTE

- Hempel A/S

Recent Industry Developments

PPG Industries plays a major role in the corrosion protective coatings market through its strong Performance Coatings segment, which includes protective, marine, and infrastructure solutions. In 2025, the company reported total net sales of around $15.9 billion, showing stable performance even in a mixed global environment.

Kansai Paint Co., Ltd. has built a steady presence in the corrosion protective coatings market through its industrial and protective coatings portfolio, supporting sectors like infrastructure, marine, and heavy industries. In 2025, the company reported consolidated net sales of about ¥588,825 million, showing stable performance across global regions despite currency and demand fluctuations.

Sherwin Williams Co. plays a very strong role in the corrosion protective coatings market through its Performance Coatings segment, which supplies solutions for infrastructure, marine, and industrial protection. In 2025, the company reported total net sales of about $23.57 billion, showing steady growth despite mixed demand across regions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 21.2 Bn |

| Forecast Revenue (2035) | USD 41.9 Bn |

| CAGR (2026-2035) | 7.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Solvent-borne, Water-borne, Powder Coatings), By Material (Alkyd, Acrylic, Epoxy, Polyurethane, Zinc, Others), By Application (Marine, Oil And Gas, Construction, Industrial, Automotive, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Akzo Nobel N.V., PPG Industries, Inc., Jotun, Sherwin Williams Co., Kansai Paint Co., Ltd., 3M, Sika AG, Axalta Coating Systems Ltd., BASF SE, Nippon Paint Holdings Co., Ltd., NYCOTE, Hempel A/S |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |