Quick Navigation

Report Overview

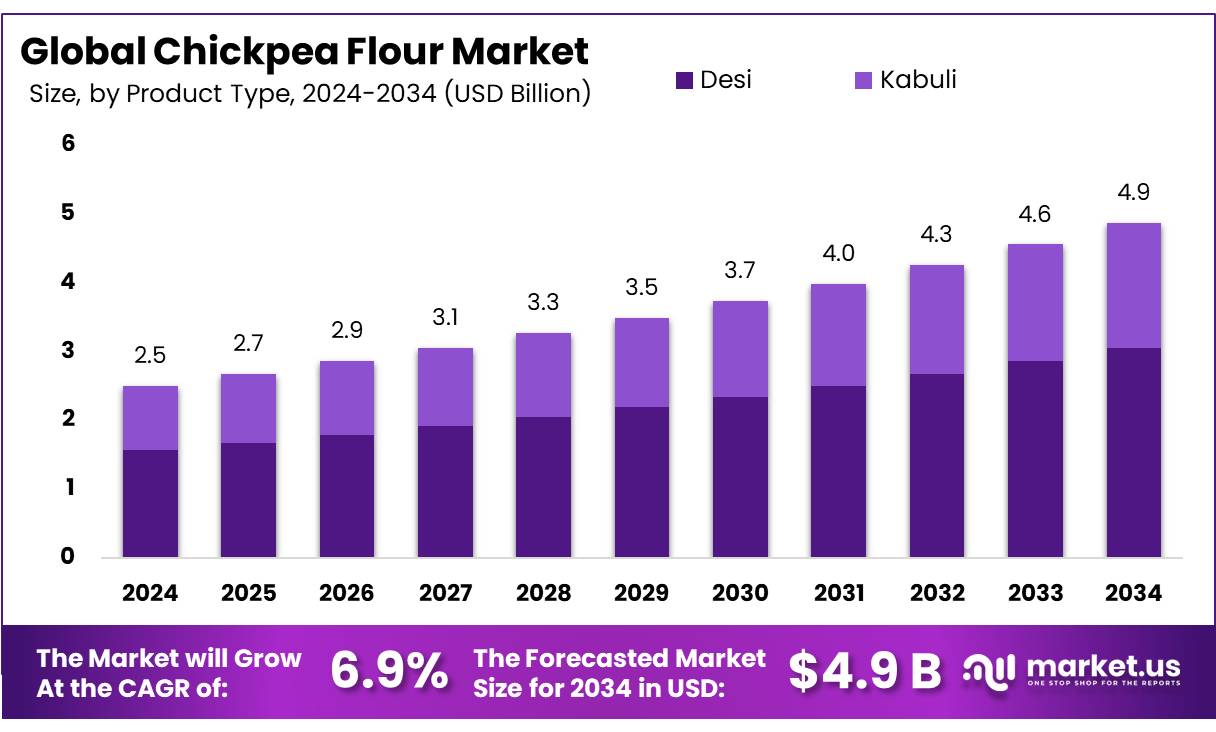

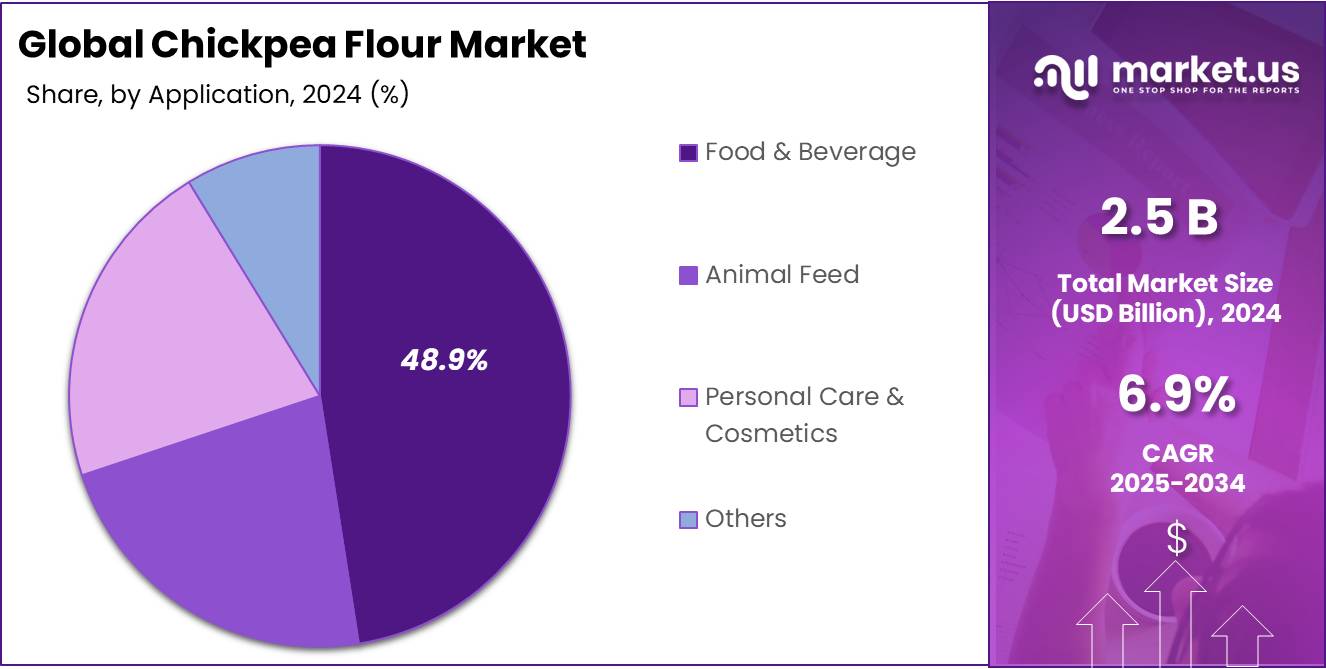

The Global Chickpea Flour Market size is expected to be worth around USD 4.9 billion by 2034, from USD 2.5 billion in 2024, growing at a CAGR of 6.9% during the forecast period from 2025 to 2034.

The Chickpea Flour Market is experiencing robust growth, driven by increasing consumer demand for nutritious, plant-based, and gluten-free food alternatives. Chickpea flour, derived from ground chickpeas (Cicer arietinum), is a versatile ingredient valued for its high protein, fiber, and micronutrient content, making it a staple in South Asian, Middle Eastern, and Mediterranean cuisines and gaining traction globally in diverse culinary applications.

Chickpea flour, derived from garbanzo beans, is a nutrient-dense ingredient that significantly boosts the intake of essential vitamins and minerals. A single cup provides over 4 milligrams of iron (25% of the daily value), 150 milligrams of magnesium (36% of the daily value), 2.6 grams of zinc (24% of the daily value), and 400 micrograms of folate (101% of the daily value). It is a rich source of thiamine, phosphorus, copper, and manganese, making it a valuable addition to a balanced diet.

Nutritionally, one cup of chickpea flour contains approximately 350 calories, primarily from carbohydrates. It includes 10 grams of dietary fiber and 10 grams of sugar, with the remainder being starch. The estimated glycemic index of 44 classifies it as moderately glycemic, suitable for those monitoring blood sugar levels.

The fat content in chickpea flour is predominantly healthy fats, with 2.7 grams of polyunsaturated fat and 1.4 grams of monounsaturated fat per cup, and less than 1 gram of saturated fat. With over 20 grams of protein per cup, chickpea flour is an excellent choice for individuals aiming to increase their protein intake, particularly in plant-based or gluten-free diets.

Chickpea flour contains 24.4%–25.4% protein, double that of wheat flour (9.3%–14.3%), and is rich in lysine but low in sulfur-containing amino acids, enhancing protein quality when mixed with cereal flours. It’s a key protein source in semi-arid tropics for those unable to afford animal proteins. It offers 3.9%–11.2% fiber (vs. wheat’s 0.9%–1.8%) and 3.7%–5.1% fat, primarily linoleic acid, plus B-complex vitamins and minerals (phosphorus, magnesium, potassium), potentially protecting against obesity and metabolic issues.

Key Takeaways

- The Chickpea Flour Market is projected to grow from USD 2.5 billion in 2024 to USD 4.9 billion by 2034, with a CAGR of 6.9%.

- Desi Chickpea Flour holds 62.7% of the market, driven by its use in South Asian and Middle Eastern cuisines.

- Organic and non-GMO chickpea flour commands 87.2% of sales, fueled by demand for clean-label products in North America and Europe.

- The Food and Beverage sector accounts for 48.9% of chickpea flour use, leveraging its gluten-free and protein-rich properties.

- Food chain services dominate distribution with a 54.8% share, driven by gluten-free and plant-based menu innovations.

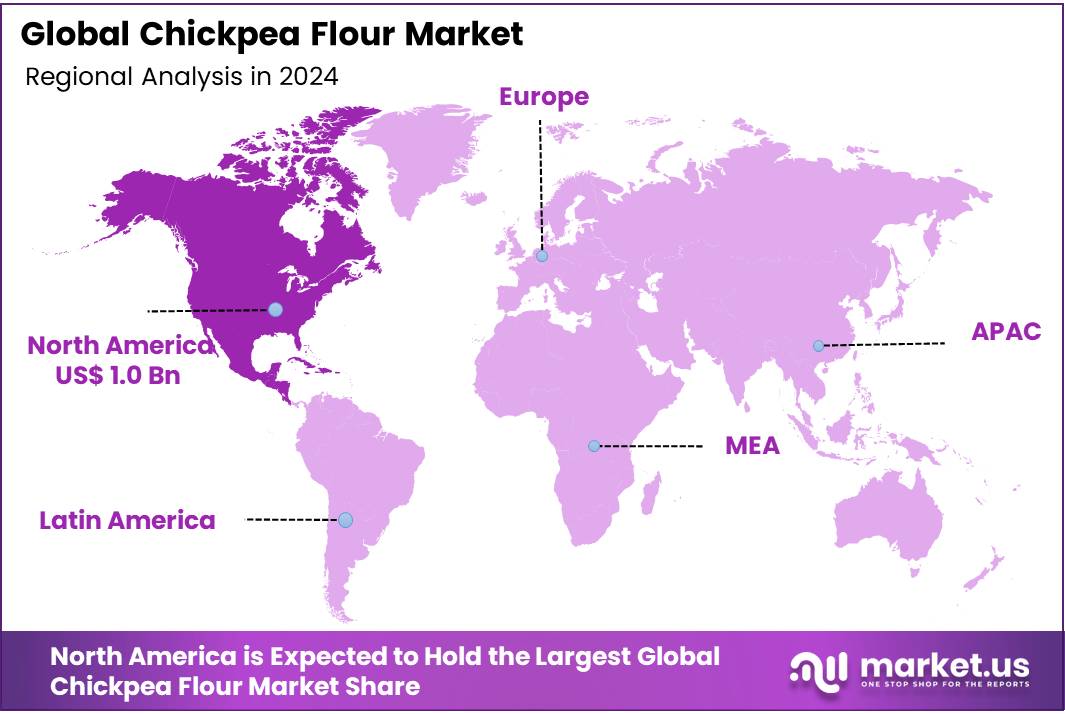

- North America Dominates Chickpea Flour Market with 43.9% Share and USD 1.0 Billion Revenue in 2024.

By Product Type

Desi Segment Dominates with 62.7% Share in 2024

In 2024, the Desi chickpea flour segment held a dominant market position, capturing more than 62.7% of the global market share. This stronghold was driven by its widespread use in traditional cuisines, particularly in South Asia and the Middle East, where it is a staple ingredient in dishes like besan-based curries, snacks, and sweets.

The affordability and easy availability of Desi chickpea flour further reinforced its market leadership. The segment is expected to maintain its lead, though with slight shifts due to growing demand for Kabuli chickpea flour in Western markets.

Desi’s deep-rooted cultural preference and cost-effectiveness will likely keep it as the top choice in key consuming regions. The segment’s growth is also supported by rising health consciousness, as consumers increasingly seek gluten-free and protein-rich alternatives.

By Product Claim

Organic and Non-GMO Chickpea Flour Captures 87.2% Market Share in 2024

In 2024, chickpea flour labeled as Organic or Non-GMO dominated the market, holding a massive 87.2% share of global sales. Consumers increasingly sought clean-label, chemical-free options, pushing demand for certified organic and non-GMO products.

This trend was strongest in North America and Europe, where health-conscious buyers were willing to pay a premium for guaranteed quality. The segment’s growth slowed slightly but remained the clear leader, as conventional chickpea flour saw a minor resurgence in price-sensitive markets.

Organic and non-GMO claims continued to drive premiumization, especially in gluten-free and plant-based food categories. Millennials and Gen Z shoppers, in particular, fueled this demand, prioritizing transparency and sustainability in their purchases.

By Application

Food and Beverage Sector Drives 48.9% of Chickpea Flour Demand in 2024

In 2024, the Food and Beverage industry was the biggest user of chickpea flour, grabbing a 48.9% share of the total market. From snacks and baked goods to soups and sauces, food manufacturers relied heavily on chickpea flour as a gluten-free protein booster.

The rise of plant-based diets and clean-label products pushed restaurants, packaged food brands, and even beverage makers to incorporate them into their recipes. This segment shows only a slight dip as other sectors like pet food and cosmetics began experimenting with chickpea flour.

Still, food and beverage remained the clear leader, thanks to its versatility in everything from vegan pancakes to protein shakes. Fast-food chains and health-focused startups kept demand high, proving that chickpea flour wasn’t just a trend but a staple in modern food production.

By Distribution Channel

Food Chain Services Command 54.8% of Chickpea Flour Market in 2024

In 2024, Food Chain Services – including quick-service restaurants, cafes, and institutional food providers – dominated chickpea flour distribution, capturing a whopping 54.8% share. The surge came as major fast-food brands rolled out gluten-free and plant-based menu items, with chickpea flour becoming a go-to ingredient for everything from crispy coatings to flatbreads.

The segment saw a slight adjustment, as retail and online sales gained traction among home cooks. But food chains still led the pack, thanks to their bulk purchasing power and ability to introduce chickpea flour to mainstream consumers. From falafel wraps in fast-casual spots to chickpea-based pancakes in breakfast chains, food service providers made sure this versatile flour stayed in high demand.

Key Market Segments

By Product Type

- Desi

- Kabuli

By Product Claim

- Organic or Non-GMO

- Conventional

By Application

- Food and Beverage

- Animal Feed

- Personal Care and Cosmetics

- Others

By Distribution Channel

- Food Chain Services

- Modern Trade

- Convenience Store

- Departmental Store

- Online Store

- Others

Drivers

Rising Demand for Plant-Based Protein Alternatives

One of the major driving forces behind the growth of the chickpea flour market is the rising demand for plant-based protein alternatives, especially among health-conscious consumers and those following vegan or vegetarian diets.

Chickpea flour, which is naturally high in protein, fiber, and essential nutrients, is being increasingly adopted as a nutritional substitute for traditional wheat flour in various food applications. This shift is not just a trend but a part of a global dietary movement influenced by health, sustainability, and ethical concerns.

Countries like India, Turkey, and Australia are leading this surge due to the consistent global demand for protein-rich pulses. As a result, chickpeas have become a key ingredient not only in traditional cuisines but also in modern health-focused foods like gluten-free breads, pancakes, snacks, and protein-rich baked goods.

Restraints

Post-Harvest Losses and Supply Chain Challenges in Chickpea Flour Production

A significant challenge facing the chickpea flour industry is the high rate of post-harvest losses during processing and storage. These losses not only reduce the quantity of usable product but also impact the livelihoods of farmers and processors who depend on this crop.

The Food and Agriculture Organization (FAO) highlights that food losses can occur at various stages of the supply chain, including production, post-harvest handling, processing, and distribution. In the case of chickpeas, factors such as inadequate drying, improper storage conditions, and inefficient milling processes contribute to significant losses.

The lack of modern processing facilities in many chickpea-producing regions exacerbates the problem. Traditional milling methods may not effectively remove impurities or achieve the desired flour consistency, leading to lower quality products that are less competitive in the market. This situation is particularly challenging for smallholder farmers and local processors who may lack access to improved technologies and infrastructure.

Opportunity

Government Support and Agricultural Advancements Boost Chickpea Flour Production

The Indian government has implemented various programs to support pulse production, including chickpeas. These initiatives encompass minimum support prices (MSPs), subsidies for quality seeds, and the promotion of improved farming techniques. Such measures have encouraged farmers to cultivate chickpeas, leading to increased availability of raw materials for chickpea flour production.

Agricultural advancements have also played a crucial role. The adoption of high-yielding and disease-resistant chickpea varieties has improved crop productivity. Additionally, better irrigation practices and mechanization have enhanced efficiency in chickpea farming. These developments have collectively contributed to the steady growth of chickpea production in the country.

The rising production of chickpeas has positively impacted the chickpea flour industry. With more raw material available, producers can meet the growing demand for chickpea flour, both domestically and internationally. This growth not only supports the food industry but also benefits farmers and rural communities by providing them with better income opportunities.

Trends

Chickpea Flour’s Expansion into Personal Care Products

Chickpea flour, traditionally a staple in kitchens, is now making its mark in the personal care industry. This shift is driven by a growing consumer preference for natural and sustainable ingredients in skincare and haircare products. In India, the use of chickpea flour, or besan, for skin care is deeply rooted in tradition.

It’s been used for generations as a natural cleanser and exfoliant. This traditional knowledge is now influencing modern personal care formulations. The global personal care industry is recognizing the benefits of chickpea flour, leading to its inclusion in various products.

The Indian government’s initiatives, such as the National Food Security Mission, aim to increase pulse production, including chickpeas. These programs not only enhance food security but also provide raw materials for emerging industries like personal care. Consumers are increasingly seeking products with natural ingredients, and chickpea flour fits this demand.

Regional Analysis

North America Dominates Chickpea Flour Market with 43.9% Share and USD 1.0 Billion in 2024

The North American chickpea flour market is experiencing robust growth, driven by increasing consumer demand for plant-based, gluten-free, and protein-rich food options. Valued at USD 1.0 billion in 2024, the dominating region is due to its strong adoption of health-conscious diets and culinary versatility.

The United States leads the segment, fueled by the popularity of chickpea-based products like hummus, snacks, and gluten-free baked goods. Canada follows, with significant production in Saskatchewan, contributing to both domestic consumption and exports to South Asia and the Middle East.

The food and beverage sector dominates applications, driven by bakery and confectionery products, while the animal feed segment is gaining traction due to chickpea flour’s high protein content. Online distribution channels are expanding rapidly, reflecting the rise of e-commerce and targeted marketing highlighting chickpea flour’s health benefits, such as high fiber and essential minerals.

However, challenges include competition from alternative flours like pea and soy, which offer similar nutritional profiles at potentially lower costs. Innovations in flavor enhancement and sustainable sourcing are expected to further bolster North America’s market leadership.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

- The Scoular Company stands out as a leading player in the chickpea flour market due to its robust global grain sourcing and distribution network. The company emphasizes sustainable sourcing and traceability, catering to growing consumer demand for plant-based and allergen-free ingredients.

- AGT Food and Ingredients, Inc. is a major global processor and supplier of pulse ingredients, including chickpea flour. The company leverages its strong global infrastructure and R&D capabilities to innovate in plant-based food applications, meeting demand in bakery, snacks, and health food segments across North America, Europe, and Asia-Pacific.

- Roland Foods, LLC offers premium global ingredients, including chickpea flour, tailored for chefs, retailers, and food service professionals. Their chickpea flour is known for consistency and culinary versatility. The company continues to strengthen its presence in gourmet and specialty food segments in the U.S. and abroad.

Top Key Players in the Market

- The Scoular Company

- AGT Food and Ingredients, Inc.

- Roland Foods, LLC

- Munchy Seeds

- Hodgson Mill, Inc.

- Ingredion Incorporated

- Hayden Flour Mills, Inc.

- Cargill, Incorporated

- Axiom Foods, Inc.

- Archer Daniels Midland Company

- Blue Ribbon Service Corporation (dba Anthony’s Goods)

- SunOpta

- Anchor Ingredients

- EHL Limited

- Diefenbaker Spice and Pulse

- CanMar Grain Products

Recent Developments

- In 2024, Scoular’s Food Innovation division introduced a functional chickpea flour with gelling, emulsifying, and foaming properties, ideal for egg replacement in bakery applications. This aligns with the rising demand for plant-based alternatives amid doubled egg prices.

- In 2024, AGT Foods strengthened its chickpea flour offerings, utilizing Canada’s robust chickpea production for domestic and export markets. Their high-protein flour is used in gluten-free bakery goods, snacks, and pasta.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.5 Billion |

| Forecast Revenue (2034) | USD 4.9 Billion |

| CAGR (2025-2034) | 6.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Desi, Kabuli), By Product Claim (Organic or Non-GMO, Conventional), By Application (Food and Beverage, Animal Feed, Personal Care and Cosmetics, Others), By Distribution Channel (Food Chain Services, Modern Trade, Convenience Store, Departmental Store, Online Store, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | The Scoular Company, AGT Food and Ingredients, Inc., Roland Foods, LLC, Munchy Seeds, Hodgson Mill, Inc., Ingredion Incorporated, Hayden Flour Mills, Inc., Cargill, Incorporated, Axiom Foods, Inc., Archer Daniels Midland Company, Blue Ribbon Service Corporation (dba Anthony’s Goods), SunOpta, Anchor Ingredients, EHL Limited, Diefenbaker Spice and Pulse, CanMar Grain Products |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |