Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of Phosphorus Trichloride

- By Grade Analysis

- By Application Analysis

- By End-Use Industry Analysis

- By Sales Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

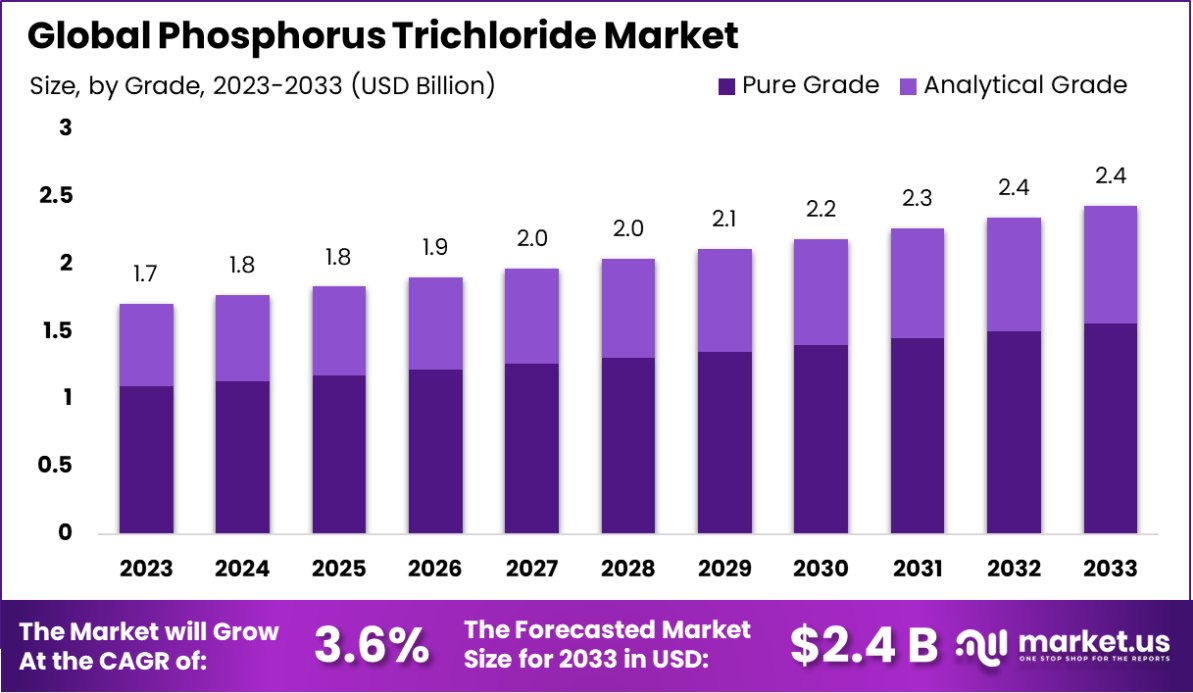

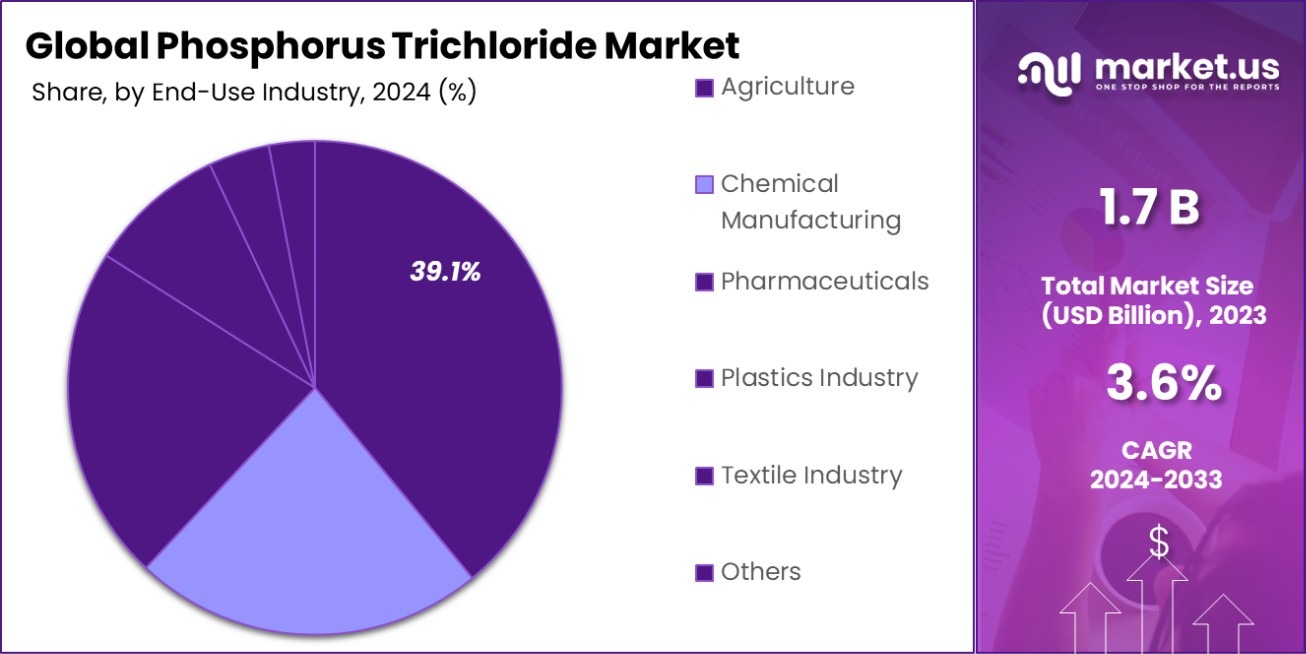

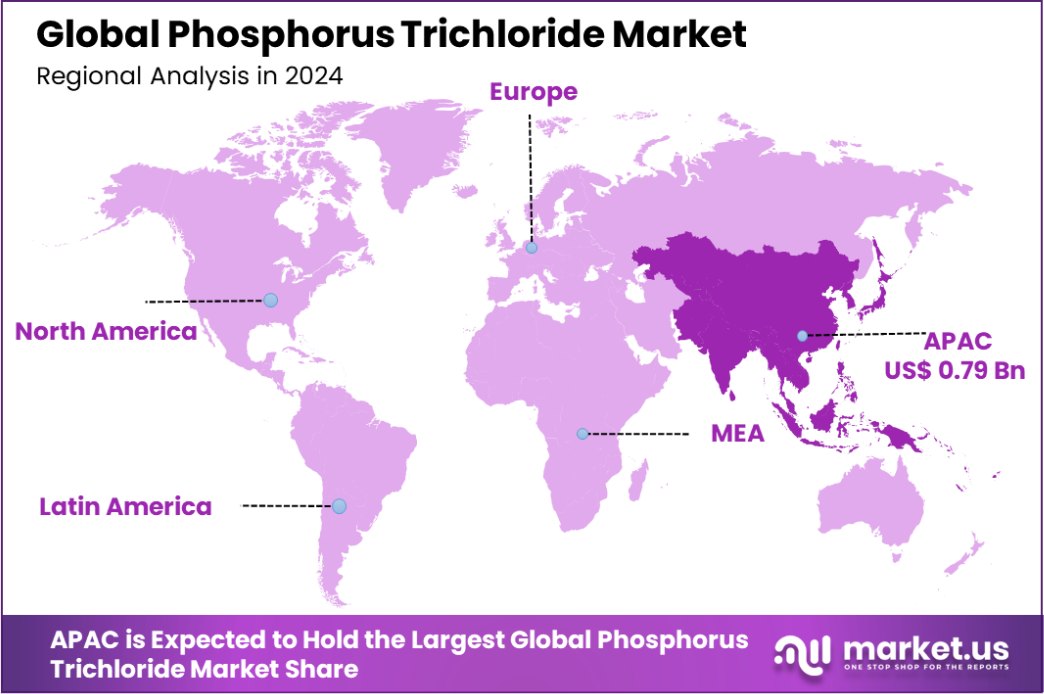

The Global Phosphorus Trichloride Market is expected to be worth around USD 2.4 Billion by 2033, up from USD 1.7 Billion in 2023, and grow at a CAGR of 3.6% from 2024 to 2033. Asia-Pacific holds 46.2% of the Phosphorus Trichloride Market, USD 0.79 Bn.

Phosphorus trichloride (PCl3) is a volatile, colorless liquid with a pungent odor, primarily utilized as an intermediate in the production of organophosphorus compounds, including pesticides, plasticizers, and flame retardants. Its reactivity with water, releasing hydrochloric acid, necessitates careful handling and storage.

The industrial landscape for phosphorus trichloride is closely tied to the global phosphorus industry, which has experienced notable fluctuations in recent years. In 2022, the phosphate fertilizer market faced supply disruptions and elevated prices, leading to decreased consumption in certain regions.

By 2023, global production of phosphate rock, the primary source of phosphorus, was estimated to have declined compared to 2022. However, consumption of phosphorus pentoxide (P2O5) in fertilizers was projected to rise from 43.8 million tons in 2022 to 45.7 million tons in 2023, with an anticipated increase to 50 million tons by 2027, driven by agricultural demands in Asia and South America.

Several factors are propelling the phosphorus trichloride market. The expansion of the agricultural sector, particularly in developing economies, has heightened the demand for phosphorus-based fertilizers, thereby increasing the need for intermediates like PCl3.

Additionally, the chemical industry’s growth, encompassing the production of flame retardants and plasticizers, has further stimulated PCl3 demand. Nonetheless, geopolitical tensions, such as the Russia-Ukraine conflict, have exacerbated supply constraints, influencing global fertilizer availability and pricing.

Emerging trends in the phosphorus trichloride market include a shift towards sustainable agricultural practices and the adoption of precision agriculture technologies. Precision farming agriculture, which involves the use of technologies to optimize field-level management regarding crop farming, has been gaining traction.

As of 2023, only 27% of U.S. farms or ranches reported using precision agriculture practices to manage crops or livestock. This growing emphasis on efficiency and sustainability is expected to influence the demand for phosphorus-based fertilizers and, consequently, PCl3.

Looking ahead, the phosphorus trichloride market is poised for growth, underpinned by increasing agricultural activities and the expanding chemical industry. The global phosphate production capacity, in terms of P2O5 content, is projected to rise from 63.6 million tons in 2023 to 69.1 million tons by 2027, with capacity expansions underway in countries like Brazil, Kazakhstan, Mexico, Morocco, and Russia.

However, challenges such as supply chain disruptions, environmental concerns, and regulatory policies may impact market dynamics. Stakeholders should monitor these developments to navigate the evolving landscape effectively.

Key Takeaways

- The Global Phosphorus Trichloride Market is expected to be worth around USD 2.4 Billion by 2033, up from USD 1.7 Billion in 2023, and grow at a CAGR of 3.6% from 2024 to 2033.

- The pure-grade segment dominates the phosphorus trichloride market, capturing a 64.1% market share.

- Chemical intermediates lead in application, contributing to 53.4% of the global phosphorus trichloride market.

- Agriculture remains a prominent end-use sector, accounting for 39.1% of phosphorus trichloride market demand.

- Distribution channels dominate sales, representing 70% of the total market share for phosphorus trichloride globally.

- In 2023, Asia-Pacific held 46.2% of the Phosphorus Trichloride Market, valued at USD 0.79 billion.

Business Benefits of Phosphorus Trichloride

Phosphorus trichloride (PCl3) is a vital chemical in various industrial applications, significantly contributing to business operations. It serves as a key intermediate in producing organophosphorus compounds, which are essential in manufacturing pesticides and flame retardants. This role supports the agricultural and safety sectors by ensuring crop protection and enhancing fire safety measures.

In the pharmaceutical industry, PCl3 is utilized in synthesizing active pharmaceutical ingredients (APIs), facilitating the development of medications that improve public health. Its application in producing plasticizers and additives enhances the quality and durability of plastic products, benefiting the plastics industry.

The Bureau of Indian Standards (BIS) has established specifications for phosphorus trichloride under IS 4581:2021, ensuring its quality and safe usage in industrial processes. Adherence to these standards promotes consistency and reliability in manufacturing operations.

Furthermore, the Department of Chemicals and Petrochemicals has initiated measures to make BIS standards mandatory for major chemicals, including phosphorus trichloride. This initiative aims to ensure that both domestic manufacturers and overseas suppliers meet the BIS parameters, thereby ensuring adequate safety for human and animal health and protecting the environment.

By integrating phosphorus trichloride into their production processes, businesses can enhance product quality, comply with regulatory standards, and contribute to sectors such as agriculture, pharmaceuticals, and manufacturing. This integration supports economic growth and development across various industries.

By Grade Analysis

The pure grade of phosphorus trichloride dominates, capturing 64.1% market share due to its high demand.

In 2023, Pure Grade held a dominant market position in the By Grade segment of the Phosphorus Trichloride Market, capturing a significant 64.1% share. This segment’s dominance is primarily attributed to the extensive use of Pure Grade phosphorus trichloride in various industrial applications, including the production of organophosphorus compounds and plasticizers, which are crucial in manufacturing plastics and other polymer materials.

The high purity level of this grade ensures optimal performance in chemical syntheses, making it indispensable in sectors such as pharmaceuticals, agrochemicals, and other chemical industries.

Conversely, Analytical Grade, used primarily in scientific research and precise analytical applications, held a smaller share of the market. Its utilization is essential in environments that require high accuracy and control, such as analytical labs and quality control departments in chemical manufacturing units.

Despite its critical role in precision-based processes, the demand for Analytical Grade is relatively lower compared to Pure Grade, as its applications are more niche and specialized.

Overall, the segmentation by grade in the Phosphorus Trichloride Market underscores the diverse applications of these chemical grades and their impact on market dynamics.

Pure Grade’s predominant share is driven by its broad utility and essential role in key industrial processes, while Analytical Grade remains vital for its specific applications in research and analysis.

By Application Analysis

Chemical intermediates lead applications, accounting for 53.4% market share, driving growth through widespread industrial usage globally.

In 2023, Chemical Intermediate held a dominant market position in the By Application segment of the Phosphorus Trichloride Market, with a substantial 53.4% share. This leading position can be attributed to the extensive application of phosphorus trichloride as a key component in the synthesis of organophosphorus compounds, which are fundamental to various manufacturing processes.

The chemical intermediate application is critical in producing flame retardants, herbicides, pesticides, and other industrial chemicals, showcasing its versatility and indispensability across multiple sectors.

Following Chemical Intermediate, the Agrochemicals segment also leverages phosphorus trichloride, primarily in the production of pesticides and herbicides, crucial for enhancing agricultural productivity. Although significant, its market share is less compared to chemical intermediates due to more targeted applications.

The market for Phosphorus Trichloride in Gasoline Additives and Plasticizers remains smaller yet essential. These applications exploit the chemical’s properties to improve gasoline combustion and to produce flexible polymers in plastic manufacturing, respectively.

The diverse applications of Phosphorus Trichloride underline its critical role in modern industrial applications, with Chemical Intermediate leading due to its broad utility and foundational role in numerous chemical synthesis processes.

By End-Use Industry Analysis

Agriculture contributes 39.1% to the phosphorus trichloride market, fueled by its essential role in agrochemical production.

In 2023, Agriculture held a dominant market position in the By End-Use Industry segment of the Phosphorus Trichloride Market, capturing a 39.1% share. This significant market share is driven by the critical role phosphorus trichloride plays in the production of agrochemicals, particularly pesticides and herbicides, which are essential for crop protection and yield enhancement.

The demand in the agricultural sector is bolstered by the global need to increase agricultural output to support growing populations.

Following closely, Chemical Manufacturing utilizes phosphorus trichloride extensively in synthesizing various organic derivatives and chemical reagents, contributing to its strong market presence. Pharmaceuticals also form a crucial segment, where phosphorus trichloride is used in manufacturing key intermediates for drugs, reflecting its importance in healthcare and medicine.

The Plastics and Textile Industries represent smaller segments of the market. In plastics, phosphorus trichloride is used to produce flame retardants and plasticizers, enhancing polymer properties. Meanwhile, in the textile industry, it finds applications in the production of fireproof and flame-retardant fabrics, underscoring its utility across diverse industrial applications.

Overall, Agriculture’s leadership in the market highlights the indispensable nature of phosphorus trichloride in supporting essential global industries, from food production to advanced manufacturing and healthcare.

By Sales Channel Analysis

Distribution channels dominate with a 70% share, underscoring their critical role in meeting diverse industry demands.

In 2023, Distribution Channel held a dominant market position in the By Sales Channel segment of the Phosphorus Trichloride Market, with a commanding 70% share. This predominant position is largely due to the effectiveness and efficiency of distribution networks that cater to a wide range of industries utilizing phosphorus trichloride.

The distribution channel’s success is anchored in its ability to provide extensive reach, reliable delivery, and streamlined logistics, which are crucial for handling chemicals that require specific storage and handling conditions.

In contrast, the Direct Channel, while important, accounts for a smaller portion of the market. This channel typically involves direct sales from manufacturers to end-users, preferred by some for its potential cost savings and customization options.

However, the complexity and safety requirements associated with phosphorus trichloride make the broader distribution networks more favorable for most buyers.

The significant lead of the Distribution Channel underscores its critical role in ensuring the availability and accessibility of phosphorus trichloride to a diverse clientele. This includes major industries like agriculture, pharmaceuticals, and chemical manufacturing, where a timely and reliable supply of chemical inputs is vital for uninterrupted operations.

Key Market Segments

By Grade

- Pure Grade

- Analytical Grade

By Application

- Chemical Intermediate

- Agrochemicals

- Gasoline Additive

- Plasticizer

- Others

By End-Use Industry

- Agriculture

- Chemical Manufacturing

- Pharmaceuticals

- Plastics Industry

- Textile Industry

- Others

By Sales Channel

- Distribution Channel

- Direct Channel

Driving Factors

Expanding Agrochemical Use Fuels Phosphorus Trichloride Demand

The increased global need for agricultural yield enhancements has significantly driven the demand for phosphorus trichloride, as it is a key ingredient in manufacturing a variety of agrochemicals.

With rising population numbers and the consequent need for more food production, agrochemicals play a pivotal role in protecting crops and improving productivity, thereby elevating the need for phosphorus trichloride.

Growth in Flame Retardant Usage Propels Market Expansion

Phosphorus trichloride is integral to producing flame retardants, which are increasingly used in industries like construction and electronics for safety measures. As regulatory standards become stricter worldwide to ensure fire safety, the demand for effective flame retardant chemicals has surged, thereby boosting the market for phosphorus trichloride.

Pharmaceutical Sector’s Expansion Supports Phosphorus Trichloride Sales

The expansion of the pharmaceutical industry globally contributes to the rising demand for phosphorus trichloride. This chemical serves as a crucial intermediate in synthesizing various pharmaceutical compounds.

With the healthcare sector’s growth due to an aging population and increased health awareness, the requirement for high-quality pharmaceutical ingredients has bolstered the phosphorus trichloride market.

Restraining Factors

Stringent Environmental Regulations Limit Market Growth

Environmental concerns and stringent regulations around the use of hazardous chemicals have become significant barriers to the Phosphorus Trichloride market. Due to its toxicity and potential environmental impact, many countries have imposed tight controls on the handling, storage, and disposal of phosphorus trichloride.

These regulations increase operational costs and complicate production processes, restraining market expansion as manufacturers must invest in safer, more compliant technologies.

Volatility in Raw Material Prices Challenges Stability

The phosphorus trichloride market is particularly sensitive to fluctuations in raw material costs, primarily phosphorus and chlorine. These raw materials are subject to volatile prices due to geopolitical tensions, trade disputes, and economic instability, which can unpredictably increase production costs. This volatility discourages long-term planning and investment, hindering consistent market growth.

Health Hazards Associated with Phosphorus Trichloride Deter Use

Health risks associated with phosphorus trichloride, including its potential to cause severe burns and respiratory issues, pose significant usage restraints. Industries often seek safer alternatives to avoid health risks to workers and reduce liability.

This shift towards safer, less hazardous chemicals can detract from the demand for phosphorus trichloride, particularly in sectors with stringent health and safety standards.

Growth Opportunity

Emerging Markets Offer New Avenues for Expansion

The growing industrial sectors in emerging economies present significant opportunities for the phosphorus trichloride market. As countries like India, China, and Brazil continue to develop their agricultural, pharmaceutical, and chemical manufacturing capabilities, the demand for phosphorus trichloride is expected to rise.

These markets offer new avenues for expansion due to their increasing industrial activities and less stringent regulatory environments compared to developed countries, making them attractive destinations for market players looking to increase their global footprint.

Innovation in Safer Chemical Processes Boosts Adoption

Innovation aimed at reducing the hazardous impacts of chemical manufacturing could open up new growth opportunities for the phosphorus trichloride market. Developing safer synthesis processes and handling techniques for phosphorus trichloride not only aligns with increasing regulatory demands but also enhances market acceptability.

Companies that invest in cleaner and safer technologies are likely to gain competitive advantages, tapping into markets that prioritize environmental and worker safety.

Expansion of Flame Retardant Applications in New Sectors

The expansion of applications for flame retardants into new sectors such as renewable energy equipment, advanced electronics, and electric vehicles provides a growth opportunity for the phosphorus trichloride market. As these industries continue to grow, the demand for materials with excellent fire safety standards increases.

Phosphorus trichloride, being a key component in many flame retardant formulations, stands to benefit significantly from this trend, especially as global safety regulations become more stringent.

Latest Trends

Increased Focus on Sustainable and Green Chemistry

The trend towards sustainable and green chemistry is shaping the phosphorus trichloride market. Companies are increasingly exploring ways to minimize environmental impact by developing eco-friendly and efficient processes for chemical production, including the use of phosphorus trichloride.

This shift not only helps meet regulatory requirements but also appeals to the growing consumer demand for environmentally responsible products, potentially expanding market reach and improving brand reputation.

Advancements in Agrochemical Formulations Drive Demand

Technological advancements in agrochemical formulations are driving new uses for phosphorus trichloride. As agricultural industries seek more effective solutions for pest and disease control, the role of phosphorus trichloride as a precursor in synthesizing novel pesticides and herbicides is becoming increasingly important.

This trend is likely to continue as the global demand for higher crop yields escalates, making it a significant driver for the phosphorus trichloride market.

Integration of Phosphorus Trichloride in High-Tech Industries

The integration of phosphorus trichloride in high-tech industries, particularly in the production of specialty chemicals used in electronics and pharmaceuticals, represents a growing trend. As these industries expand, they require more specialized chemical compounds that provide precise functionalities.

Phosphorus trichloride is crucial in the synthesis of these specialty chemicals, indicating a potential surge in demand aligned with technological advancements and increased production capacities in these sectors.

Regional Analysis

In 2023, the Asia-Pacific Phosphorus Trichloride market held a 46.2% share, valued at USD 0.79 billion.

The Phosphorus Trichloride Market exhibits distinct regional dynamics, influenced by local industrial activities, regulatory environments, and market demands. Asia-Pacific emerges as the dominant region, commanding a significant 46.2% market share, valued at USD 0.79 billion.

This leadership is propelled by robust manufacturing sectors in China and India, extensive agricultural activities requiring agrochemicals, and the rapid expansion of pharmaceutical industries in the region.

In contrast, North America and Europe show substantial market activity, driven by advanced chemical manufacturing technologies and stringent environmental regulations that govern the use and disposal of phosphorus trichloride.

These regions focus on innovative applications and safety improvements in handling hazardous chemicals, which moderate their market growth but enhance the quality and safety of phosphorus trichloride applications.

The Middle East & Africa and Latin America are emerging markets with growing potential. These regions are experiencing gradual industrial growth, particularly in agriculture and chemical manufacturing, which could increase the demand for phosphorus trichloride.

However, their market share remains smaller due to less developed industrial infrastructure and lower technological adoption compared to Asia-Pacific, North America, and Europe. As these regions develop, they represent important future growth areas for the phosphorus trichloride market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global Phosphorus Trichloride market has been significantly shaped by contributions from key players, with each company playing a vital role in defining industry dynamics and driving innovation.

Among these, Akzo Nobel N.V. and Bayer AG continue to stand out due to their robust commitment to sustainable chemical manufacturing practices and extensive global reach. These companies have been pivotal in advancing the use of phosphorus trichloride in environmentally conscious applications, enhancing both market growth and regulatory compliance.

Another notable contributor, Nutrien Ltd., has capitalized on its integrated supply chain to ensure the stable availability of phosphorus trichloride, particularly in agricultural applications where the demand for agrochemicals remains high. Their strategic positioning in major agricultural markets has allowed them to maximize their impact on the sector.

Emerging players like Anhui Guangxin Agrochemical Co., Ltd. and Jiangsu Tianyuan Chemical Co., Ltd. are also making significant inroads into the market by focusing on the Asia-Pacific region, where the demand for phosphorus trichloride is driven by rapid industrialization and agricultural expansion. Their localized approach to manufacturing and distribution has enabled them to cater effectively to fast-growing markets.

Lanxess and Italmatch Chemicals are influencing the market through specialized applications of phosphorus trichloride in the pharmaceuticals and plastics industries, leveraging advanced technologies to produce high-purity products that meet stringent industry standards.

Overall, the competitive landscape in 2023 is marked by a blend of innovation, strategic market placement, and adaptation to regulatory environments, with each key player contributing uniquely to the expansive growth and technological advancement of the phosphorus trichloride market.

As industries continue to evolve, these companies are well-positioned to respond to the shifting demands of a diverse client base, ensuring long-term sustainability and market leadership.

Top Key Players in the Market

- Akzo Nobel N.V.

- Anhui Guangxin Agrochemical Co., Ltd.

- Bayer AG

- Excel Industries

- Guangzhou Zoron Chemical Technology Co. Ltd

- Henan Qingshuiyuan Technology Co., Ltd.

- Italmatch Chemicals

- Jiangsu Tianyuan Chemical Co., Ltd.

- Lanxess

- LianYunGang Dongjin Chemical Co. Ltd.

- Merck KGaA

- Mosaic Company

- Nutrien Ltd.

- Parchem fine & specialty chemicals

- PCC Rokita Spólka Akcyjna

- Protection AG

- SANDHYA GROUP

- Shandong Futong Chemical Co., Ltd.

- Shanghai Fopol Chem-Tech Industry Co. Ltd.

- Solvay S.A.

- Syngenta Crop

- UPL Limited

- Xuzhou Jianping Chemical Co., Ltd

- Zhejiang Xinan Chemical Industrial Group Co., Ltd,

Recent Developments

- In 2023, Akzo Nobel N.V. saw significant financial growth, increasing its adjusted operating income and EBITDA despite market challenges. The company continued this trend into 2024, focusing on cost management and sustainable innovations to target an EBITDA of approximately €1.5 billion.

- In 2023, Anhui Guangxin Agrochemical Co., Ltd. focused on improving Phosphorus Trichloride properties and sustainability. Their innovations support the growing pharmaceutical sector and other industries requiring high-quality chemical intermediates.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.7 Billion |

| Forecast Revenue (2033) | USD 2.4 Billion |

| CAGR (2024-2033) | 3.6% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Grade (Pure Grade, Analytical Grade), By Application (Chemical Intermediate, Agrochemicals, Gasoline Additive, Plasticizer, Others), By End-Use Industry (Agriculture, Chemical Manufacturing, Pharmaceuticals, Plastics Industry, Textile Industry, Others), By Sales Channel (Distribution Channel, Direct Channel) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Akzo Nobel N.V., Anhui Guangxin Agrochemical Co., Ltd., Bayer AG, Excel Industries, Guangzhou Zoron Chemical Technology Co. Ltd, Henan Qingshuiyuan Technology Co., Ltd., Italmatch Chemicals, Jiangsu Tianyuan Chemical Co., Ltd., Lanxess, LianYunGang Dongjin Chemical Co. Ltd., Merck KGaA, Mosaic Company, Nutrien Ltd., Parchem fine & specialty chemicals, PCC Rokita Spólka Akcyjna, Protection AG, SANDHYA GROUP, Shandong Futong Chemical Co., Ltd., Shanghai Fopol Chem-Tech Industry Co. Ltd., Solvay S.A., Syngenta Crop, UPL Limited, Xuzhou Jianping Chemical Co., Ltd, Zhejiang Xinan Chemical Industrial Group Co., Ltd, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |