Quick Navigation

Report Overview

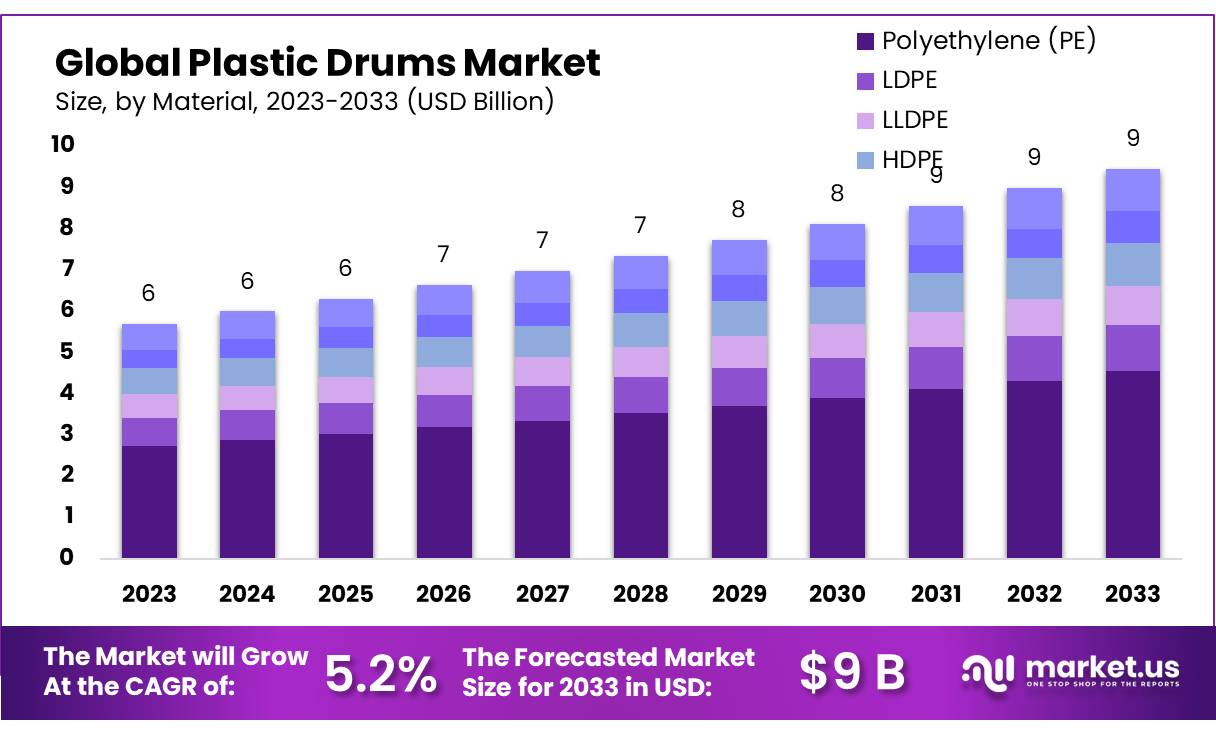

The Global Plastic Drums Market is expected to be worth around USD 9.5 Billion by 2033, up from USD 5.7 Billion in 2023, and grow at a CAGR of 5.2% from 2024 to 2033.

Plastic Drums are cylindrical containers made from durable plastic, typically used for storing and transporting liquids, chemicals, food products, and other bulk materials. They are widely preferred due to their resistance to corrosion, lightweight nature, and cost-effectiveness compared to metal drums.

Plastic Drums Market refers to the industry involved in the production and sale of plastic drums for various applications across industries such as chemicals, pharmaceuticals, food and beverages, and logistics. This market has seen steady growth due to increasing demand for durable, cost-efficient packaging solutions.

Growing industries like chemicals and food processing drive demand for plastic drums due to their durability and ability to preserve product integrity. As e-commerce and industrial logistics expand, the need for efficient, reusable packaging solutions increases. Innovations in recycling technologies and eco-friendly materials present significant growth prospects for manufacturers to cater to sustainability-conscious consumers.

The global Plastic Drums Market is experiencing notable growth, driven by the increasing demand for cost-effective and versatile packaging solutions across various industries such as chemicals, pharmaceuticals, and food and beverages.

Plastic drums are preferred for their resistance to corrosion, lightweight structure, and ability to store both liquids and solids securely, which makes them highly suitable for hazardous materials.

For instance, according to ITP Packaging, the company offers a range of UN-approved plastic open-top and tight-head drums, with capacities ranging from 20 liters to 220 liters, ensuring safe storage and transportation of chemicals, food, and liquids.

A key growth driver is the expanding need for sustainable, durable, and eco-friendly packaging alternatives in the wake of environmental concerns. The adoption of plastic drums over traditional metal variants is becoming more prevalent due to their relatively lower cost and ease of handling. The growing demand for efficient logistics in industries such as e-commerce, along with regulatory changes favoring recyclable materials, supports this trend.

In terms of market segmentation, steel-combi drums, as described by CLSmith, combine the advantages of both tight-head and open-top drums, offering capacity options ranging from 25 liters to 210 liters. While over drums are pricier, they are used for storing large drums, further underscoring the importance of versatile packaging solutions.

Opportunities lie in technological advancements for manufacturing eco-friendly plastic drums, as well as in the development of innovative designs that cater to the needs of both small and large-scale industries. Companies that focus on recycling initiatives and sustainable material sourcing will likely hold a competitive advantage in the coming years.

Key Takeaways

- The Global Plastic Drums Market is expected to be worth around USD 9.5 Billion by 2033, up from USD 5.7 Billion in 2023, and grow at a CAGR of 5.2% from 2024 to 2033.

- Polyethylene (PE) dominates the market with a share of 48.5% due to its durability.

- Open-head plastic drums account for 58.5%, offering flexibility in liquid and solid storage.

- The 30-55 gallon capacity segment holds a 39.3% share, preferred for bulk storage solutions.

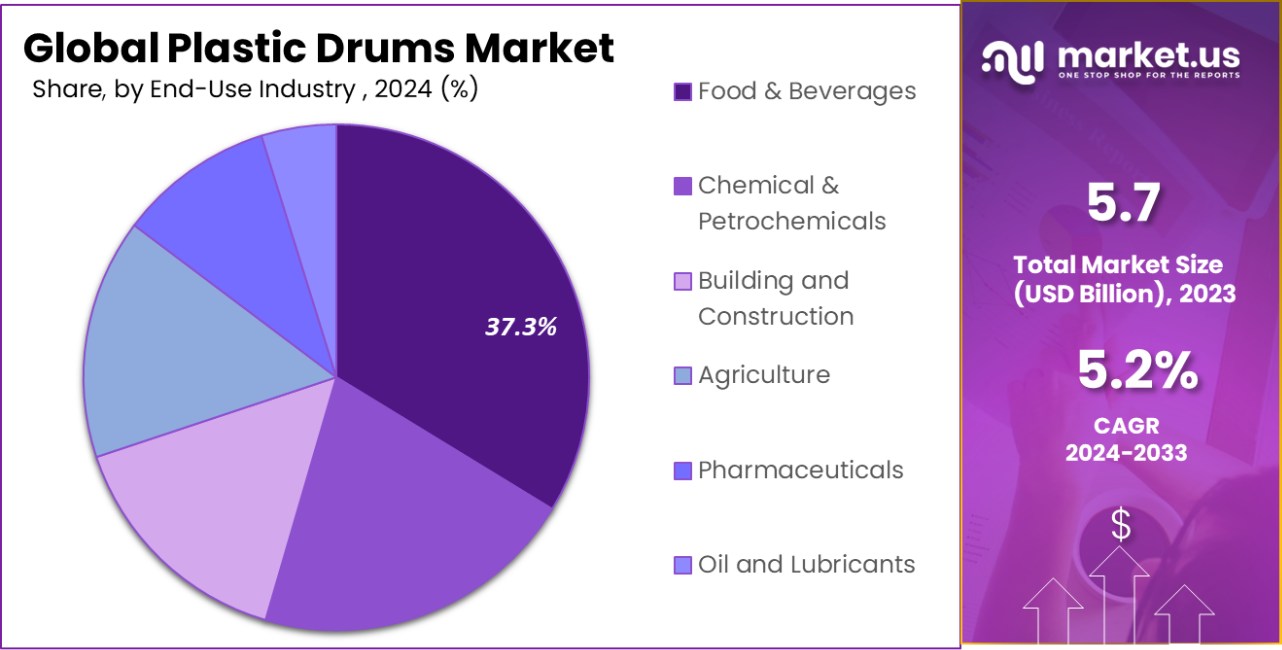

- The food and beverage sector leads with a 37.3% share, requiring safe storage solutions.

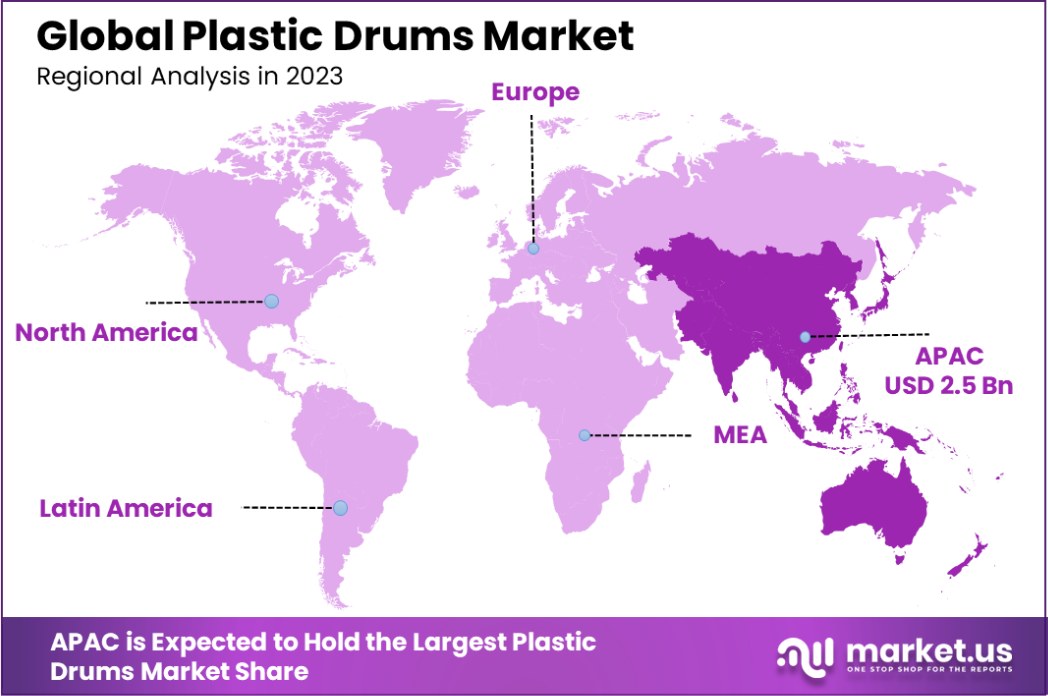

- The Asia-Pacific region holds 45.8% of the Plastic Drums Market, valued at USD 2.5 billion.

By Material Type Analysis

Polyethylene (PE) dominates the Plastic Drums Market, accounting for 48.5% of the total market share.

In 2023, Polyethylene (PE) held a dominant market position in the By Material Type segment of the Plastic Drums Market, with a 48.5% share. This widespread adoption of PE, particularly in low-density polyethylene (LDPE), linear low-density polyethylene (LLDPE), and high-density polyethylene (HDPE), is attributed to its robust properties such as resistance to chemicals, durability, and cost-effectiveness.

Among these, HDPE is the most commonly used, owing to its superior strength and rigidity, making it ideal for heavy-duty applications like chemicals, oils, and food storage.

Following PE, Polypropylene (PP) accounted for a significant share in the market, driven by its high chemical resistance, making it a preferred choice for storage of solvents and hazardous materials. PP’s versatility and higher temperature resistance further contribute to its growing market demand.

The market’s composition in 2023 showed a clear preference for PE-based products, with its low-cost manufacturing process and reliable performance in a variety of industries like chemicals, food, and pharmaceuticals.

As sustainability continues to influence product choices, innovations in biodegradable and recycled polyethylene formulations are expected to shape the future trends in this segment, promoting further growth for PE within the plastic drums market.

By Head Type Analysis

Open-head plastic drums lead the market, with a significant share of 58.5% in demand.

In 2023, Open Head held a dominant market position in the By Head Type segment of the Plastic Drums Market, with a 58.5% share. Open Head drums are preferred for their versatility, offering easy access for filling, cleaning, and maintenance.

This makes them the ideal choice for industries requiring frequent product handling, such as food processing, chemicals, and pharmaceuticals. The design of Open Head drums, which typically feature a removable lid, allows for a more flexible approach to storage and smart transportation, contributing to their widespread use.

In contrast, Tight Head drums accounted for the remaining market share, driven by their superior ability to securely store and transport liquids and hazardous materials. With a fixed top and a tightly sealed structure, Tight Head drums are commonly used in industries that require a high level of security against leakage and contamination, such as petrochemicals and industrial chemicals. Their durable design ensures a high level of integrity during transportation and storage, particularly for volatile substances.

The dominance of Open Head drums in 2023 can be attributed to their adaptability across a broad range of applications. However, Tight Head drums are expected to see growth in sectors where safety and leak-proof properties are critical, reflecting the evolving needs of end-users in the market.

By Capacity Analysis

Plastic drums in the 30-55 gallon range represent 39.3% of the market’s total demand.

In 2023, 30-55 gallons held a dominant market position in the By Capacity segment of the Plastic Drums Market, with a 39.3% share. This capacity range is particularly favored due to its balance between portability and storage efficiency, making it suitable for a wide array of industrial applications.

Industries such as chemicals, food processing, and pharmaceuticals commonly utilize 30-55 gallon drums for transporting and storing liquids, powders, and hazardous materials, as this size accommodates bulk storage needs while maintaining ease of handling.

In comparison, the Less than 10 gallons and 10-30 gallons categories accounted for smaller market shares, driven by specific applications requiring smaller volumes, such as laboratory storage, small-scale manufacturing, and retail packaging. These smaller capacities are ideal for niche markets where limited quantities of materials are handled, and there is a demand for compact, easy-to-store solutions.

The 55 gallons and above category, while accounting for a smaller share than the 30-55 gallon segment, is expected to grow as industries like oil and gas and large-scale manufacturing increase their need for high-volume storage. However, the dominant share of the 30-55 gallon range highlights its versatility across multiple industries, positioning it as the key segment in the global plastic drums market.

By End-Use Industry Analysis

The food and beverages sector is the largest consumer, holding a 37.3% market share

In 2023, Food & Beverages held a dominant market position in the By End-Use Industry segment of the Plastic Drums Market, with a 37.3% share. The food and beverage industry’s preference for plastic drums is driven by the need for secure, hygienic, and cost-effective packaging for bulk ingredients, liquids, and finished products.

Plastic drums are widely used for the storage and transportation of items such as oils, syrups, juices, and sauces, owing to their durable, leak-proof design and ability to meet stringent safety standards.

Chemical & Petrochemicals followed closely, with a significant market share, as plastic drums are essential for the safe containment and transport of chemicals, solvents, and other hazardous materials. Their resistance to corrosion and ability to withstand various chemicals make them a preferred choice in this sector.

Other industries, including Building and Construction, Agriculture, Pharmaceuticals, and Oil and Lubricants, also contributed to the market share. Plastic drums in these sectors are utilized for storing and transporting raw materials, agricultural chemicals, pharmaceutical compounds, and lubricants. Each industry benefits from the durability, portability, and cost-effectiveness of plastic drums.

The continued demand from Food & Beverages, combined with growth in the chemical and petrochemical sectors, solidifies the position of these industries as the primary drivers of the plastic drums market in 2023.

Key Market Segments

By Material Type

- Polyethylene (PE)

- LDPE

- LLDPE

- HDPE

- Polypropylene (PP)

- Others

By Head Type

- Open Head

- Tight Head

By Capacity

- Less than 10 gallons

- 10-30 gallons

- 30-55 gallons

- 55 gallons and above

By End-Use Industry

- Food & Beverages

- Chemical & Petrochemicals

- Building and Construction

- Agriculture

- Pharmaceuticals

- Oil and Lubricants

- Others

Driving Factors

Increasing Demand for Safe, Durable Packaging Solutions

The rising need for secure and durable packaging solutions is a key driving factor in the Plastic Drums Market. Industries such as food and beverages, chemicals, and pharmaceuticals require packaging that can withstand transport, prevent contamination, and protect contents from external factors.

Plastic drums are favored due to their resistance to chemicals, ability to endure harsh conditions, and cost-effectiveness. With growing global trade and transportation of bulk materials, the demand for robust and reliable storage solutions continues to rise, further fueling market growth.

Growth of End-Use Industries Like Chemicals and Food

The expansion of key end-use industries like chemicals, food and beverages, and pharmaceuticals significantly drives the Plastic Drums Market. As these industries scale up production and distribution, they require efficient and secure storage for raw materials, ingredients, and finished goods.

In the food sector, plastic drums are essential for bulk ingredient storage, while in chemicals and pharmaceuticals, they are used to safely handle hazardous materials. The growth in demand from these industries is expected to continue, further boosting the adoption of plastic drums globally.

Cost-Effectiveness and Reusability of Plastic Drums

One of the main advantages driving the adoption of plastic drums is their cost-effectiveness and reusability. Plastic drums offer a lower upfront cost compared to alternatives like steel or fiber drums, making them an attractive option for businesses looking to reduce packaging expenses.

Moreover, plastic drums are often reusable, which helps businesses cut costs further and contribute to sustainability efforts. The durability and long lifecycle of plastic drums make them a preferred choice for businesses seeking affordable, long-term storage and transportation solutions.

According to Corex Recycling, in Dandenong South, they received $253,470 to install new equipment that will enable recovery of highly contaminated soft plastic waste and maintain the highest level of end product purity. According to royalchemical, each year there are over 15 million plastic drums made in North America by four major producers.

Restraining Factors

Environmental Concerns Over Plastic Waste

Environmental concerns regarding plastic waste are a significant restraining factor for the Plastic Drums Market. As the global focus on sustainability increases, industries are under pressure to reduce plastic usage and switch to more eco-friendly packaging alternatives. The accumulation of plastic waste, particularly from single-use drums, contributes to pollution and harms ecosystems.

Governments and consumers are demanding better recycling solutions, and businesses are seeking ways to minimize their environmental footprint. These pressures may slow the adoption of plastic drums or lead to increased costs for sustainable alternatives.

High Costs of Advanced Recycling Technologies

The costs associated with advanced recycling technologies present a challenge to the growth of the Plastic Drums Market. While recycling can help address environmental concerns, the infrastructure for recycling plastic drums remains expensive and complex.

Technologies required for processing used plastic drums into reusable materials are costly and not widely available in some regions. As a result, the recycling rates for plastic drums are lower than desired, leading to concerns about waste management. The high cost of these technologies could limit market growth and hinder adoption in certain sectors.

Competition from Alternative Packaging Solutions

Plastic drums face stiff competition from alternative packaging solutions such as metal, fiber, and composite drums. These alternatives often offer advantages in terms of strength, barrier properties, and suitability for certain materials, which makes them attractive to industries with specific needs, such as hazardous chemicals or pharmaceuticals.

Additionally, some businesses are turning to sustainable packaging options like biodegradable or recyclable materials, further challenging the growth of plastic drums. As these alternatives continue to improve in cost-effectiveness and functionality, plastic drums may lose market share in certain segments.

Growth Opportunity

Increasing Demand for Sustainable and Recyclable Solutions

The growing emphasis on sustainability presents a significant growth opportunity for the Plastic Drums Market. As industries and consumers push for eco-friendly packaging, there is a rising demand for recyclable and reusable plastic drums.

Manufacturers are investing in developing biodegradable and recyclable plastic formulations, which can meet environmental standards while maintaining the durability and cost-effectiveness of traditional plastic drums.

This shift towards more sustainable products aligns with global sustainability goals, creating a strong opportunity for businesses to innovate and capture market share in the eco-conscious consumer segment.

Expansion in Emerging Markets Driving Demand

Emerging markets, particularly in Asia Pacific, Latin America, and the Middle East, are creating new growth opportunities for the Plastic Drums Market. As industrialization accelerates in these regions, the demand for packaging solutions such as plastic drums increases across industries like chemicals, food & beverages, and pharmaceuticals.

Rapid urbanization, improved logistics infrastructure, and expanding manufacturing sectors further contribute to market growth. Companies that establish a strong presence in these emerging markets can tap into the rising need for bulk storage and transportation solutions, helping to boost overall market expansion.

Technological Innovations in Plastic Drum Design

Technological advancements in plastic drum design and production offer significant growth potential in the market. Innovations such as multi-layered plastic drums, improved sealing mechanisms, and enhanced resistance to extreme temperatures and chemicals are driving demand.

Additionally, the development of smart plastic drums equipped with tracking technology can help industries better monitor inventory, enhance logistics operations, and improve safety. These innovations not only enhance the functionality of plastic drums but also provide a competitive edge, encouraging businesses to adopt newer solutions that increase operational efficiency and meet modern storage requirements.

Latest Trends

Shift Towards Eco-Friendly and Recyclable Materials

A key trend in the Plastic Drums Market is the increasing shift towards eco-friendly and recyclable materials. As global regulations on plastic waste tighten and consumer demand for sustainable products rises, manufacturers are focusing on developing plastic drums made from recyclable and biodegradable materials.

This trend is further driven by the growing adoption of circular economy principles, where the reuse and recycling of plastic packaging are prioritized. Companies are also exploring alternatives to traditional plastics, such as plant-based or biodegradable polymers, to reduce environmental impact while meeting regulatory requirements.

Adoption of Smart Plastic Drums for Enhanced Tracking

The integration of smart technology into plastic drums is another emerging trend. Smart plastic drums equipped with RFID tags or GPS tracking systems enable companies to monitor the location, status, and usage of their products in real-time.

This trend is particularly beneficial for industries like chemicals, pharmaceuticals, and food & beverages, where precise tracking of inventory and safe handling is critical. By offering better visibility and control over the supply chain, smart plastic drums are enhancing operational efficiency and reducing risks associated with storage and transportation.

Increasing Use of Plastic Drums in E-Commerce

The growth of e-commerce is driving new demand for plastic drums, particularly in the packaging of bulk goods and liquids. As online shopping continues to rise, especially in sectors like food and beverage delivery, the need for secure and durable packaging solutions has expanded.

Plastic drums, known for their strength and cost-effectiveness, are increasingly being used for shipping bulk items like oils, syrups, and chemicals. This trend is expected to grow as e-commerce platforms look for efficient, scalable packaging solutions to meet the demands of a globalized online market.

Regional Analysis

In 2023, the Asia-Pacific region held a 45.8% share of the Plastic Drums Market, valued at USD 2.5 billion.

In 2023, the Plastic Drums Market demonstrated significant regional variation, with Asia-Pacific emerging as the dominating region, holding a 45.8% market share, valued at USD 2.5 billion. This growth is driven by rapid industrialization, particularly in countries like China and India, alongside the expansion of key industries such as chemicals, food and beverages, and pharmaceuticals.

The region’s increasing demand for bulk packaging solutions, coupled with improving logistics infrastructure, has further fueled market growth.

North America holds a substantial share of the market, accounting for approximately 20.2%. The U.S. remains a key driver in the demand for plastic drums, particularly in industries like chemicals, agriculture, and oil & lubricants. The region benefits from advanced manufacturing capabilities and a high level of demand for secure, reliable packaging for hazardous materials.

Europe follows closely, with a share of 18.5%, supported by stringent regulations around chemical packaging and increasing adoption of eco-friendly packaging alternatives. Germany, the U.K., and France are prominent contributors to the market’s expansion.

The Middle East & Africa and Latin America account for smaller shares, at 8.1% and 7.4%, respectively. These regions are witnessing growing industrial activity and infrastructure development, contributing to the rising demand for durable and cost-effective packaging solutions. Despite the smaller share, both regions are expected to experience steady growth in the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global Plastic Drums Market was shaped by several key players who continue to dominate through their strong market presence, innovation, and extensive product offerings. Greif, Inc., a major player in the packaging industry, holds a significant share of the market due to its broad range of plastic drum products and focus on sustainability initiatives.

Greif’s extensive manufacturing footprint and strong distribution network enable it to cater to diverse industries, including chemicals, food & beverages, and pharmaceuticals.

FDL Packaging Group has carved a niche in the market by offering high-quality, customized plastic drums tailored to specific customer needs, particularly in the food and beverage industry. Its focus on product innovation and customer service has contributed to its increasing market share.

Industrial Container Services, Inc. and its subsidiary Industrial Container Services, LLC, stand out for their expertise in reconditioning and recycling plastic drums, aligning with the growing demand for sustainable solutions in the market. The company’s ability to offer cost-effective and environmentally friendly options positions it as a strong competitor in the industry.

Sonoco Products Company and Mauser Group B.V. are also prominent, leveraging their extensive global operations and strong brand recognition to drive growth. Mauser’s strategic acquisitions and focus on expanding its product portfolio further solidify its position.

Companies like SCHÜTZ GmbH & Co. KGaA, TPL Plastech Ltd., and Delta Containers Direct Limited continue to innovate, providing reliable, durable, and eco-friendly plastic drums, thus ensuring their market leadership.

Overall, the competitive landscape in the Plastic Drums Market is marked by innovation, sustainability efforts, and an increasing focus on expanding into emerging markets, particularly in Asia-Pacific and Latin America.

Top Key Players in the Market

- Greif, Inc.

- FDL Packaging Group

- Industrial Container Services, Inc.

- Sonoco Products Company

- SCHÜTZ GmbH & Co. KGaA

- Mauser Group B.V.

- E-Con Packaging Pvt Ltd

- Delta Containers Direct Limited

- Greif Inc.

- C.L. Smith Company

- Mauser Group B.V.

- Schutz Container Systems, Inc.

- TPL Plastech Ltd.

- Great Western Containers Inc.

- Industrial Container Services, LLC

- Orlando Drum & Container Corporation

- Cospak Pty Ltd.

- Pioneer Plastics (Pty) Ltd.

- U.S. Coexcell Inc.

- Kodama Plastics Co., Ltd.

- Vallero International S.r.l

- Interplastica Pvt. Ltd.

- REMCON Plastics Inc.

Recent Developments

- In 2024, Sonoco acquired Eviosys for approximately $3.9 billion, aiming to enhance its metal packaging division. This move is part of Sonoco’s broader strategy to streamline its portfolio, improve operational efficiencies, and boost market leadership in sustainable packaging solutions.

- In 2023, FDL Packaging Group will offer HDPE plastic drums in various designs like tighthead, open top, and wide neck, suitable for diverse industries, ensuring safe transport and storage of sensitive materials like food and chemicals. These UN-approved, food-grade containers range from 20 to 220 liters.

- In 2023, TPL Plastech Ltd. achieved a 23% volume growth and a 15% rise in total income due to high demand in the industrial packaging sector, particularly from the chemical and pharmaceutical industries in Dahej.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 5.7 Billion |

| Forecast Revenue (2033) | USD 9.5 Billion |

| CAGR (2024-2033) | 5.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Polyethylene (PE), LDPE, LLDPE, HDPE, Polypropylene (PP), Others), By Head Type (Open Head, Tight Head), By Capacity (Less than 10 gallons, 10-30 gallons, 30-55 gallons, 55 gallons and above), By End-Use Industry (Food & Beverages, Chemical and Petrochemicals, Building and Construction, Agriculture, Pharmaceuticals, Oil and Lubricants, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Greif, Inc., FDL Packaging Group, Industrial Container Services, Inc., Sonoco Products Company, SCHÜTZ GmbH & Co. KGaA, Mauser Group B.V., E-Con Packaging Pvt Ltd, Delta Containers Direct Limited, Greif Inc., C.L. Smith Company, Mauser Group B.V., Schutz Container Systems, Inc., TPL Plastech Ltd., Great Western Containers Inc., Industrial Container Services, LLC, Orlando Drum & Container Corporation, Cospak Pty Ltd., Pioneer Plastics (Pty) Ltd., U.S. Coexcell Inc., Kodama Plastics Co., Ltd., Vallero International S.r.l, Interplastica Pvt. Ltd., REMCON Plastics Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |