Quick Navigation

Report Overview

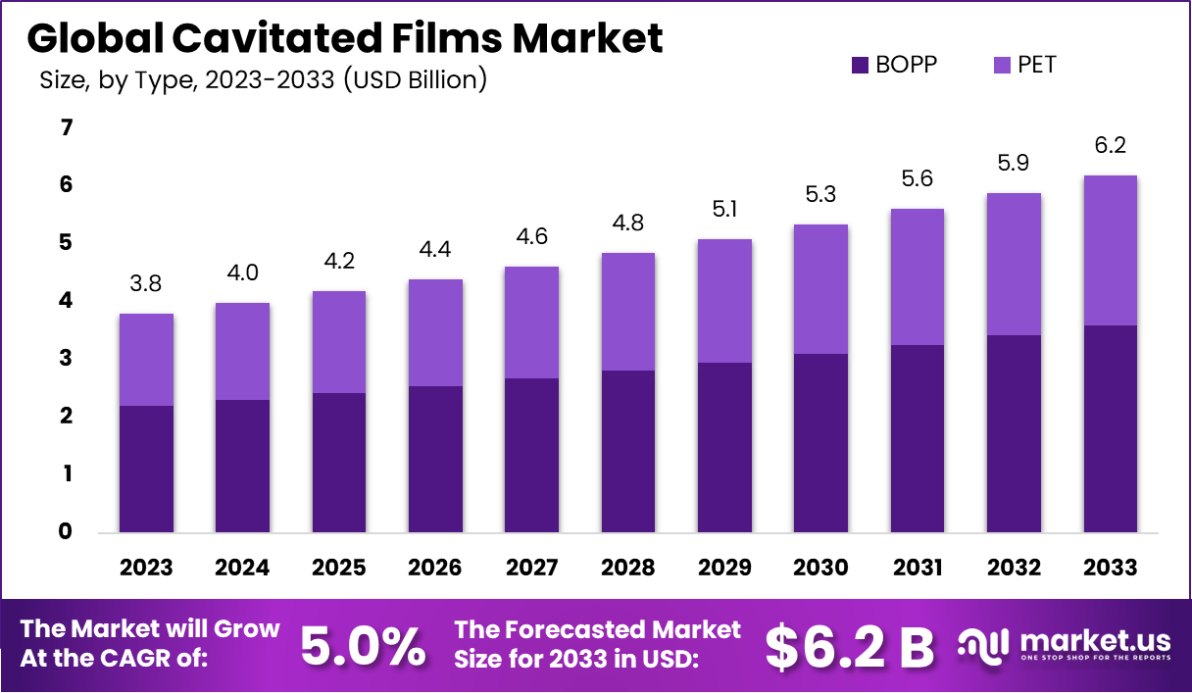

The Global Cavitated Films Market is expected to be worth around USD 6.2 Billion by 2033, up from USD 3.8 Billion in 2023, and grow at a CAGR of 5.0% from 2024 to 2033.

Cavitated Films are packaging materials with micro-sized voids or cavities created within their structure, improving the film’s strength and insulation properties while reducing material usage. They are often used in food packaging, medical applications, and consumer goods. The cavities enhance barrier properties and offer better heat insulation without significantly increasing weight.

Cavitated Films Market refers to the global industry involving the production, distribution, and consumption of these films. It serves various sectors like food packaging, healthcare, and electronics, driven by the demand for lightweight, durable, and cost-effective materials.

Advancements in material science and rising consumer demand for sustainable packaging drive market growth. Increased adoption in food packaging for extended shelf life and consumer preference for lightweight materials boost demand. Innovations in biodegradable cavitated films and expanding applications in eco-friendly packaging offer significant growth opportunities.

The Cavitated Films market is demonstrating innovative growth driven by advancements in film technology, emphasizing efficiency and cost-effectiveness in packaging applications. Cavitated films, particularly the SWPB product range by Manucor, exemplify this progression.

This range offers a significant advantage in terms of material density, recorded at 0.71, compared to traditional options ranging from 0.75 to 0.82. Such reduced density not only ensures a lower material requirement but also posits a cost-effective alternative for manufacturers using VFFS (Vertical Form Fill Seal) and HFFS (Horizontal Form Fill Seal) machines.

Furthermore, understanding the behavior of these materials under different conditions is essential. For instance, the concept of vapor pressure in cavitated films, although different from its meteorological counterpart, plays a critical role in determining the operational efficiency and stability of these films.

Discharge cavitation, another critical aspect, typically manifests at extremely high pump discharge pressures, particularly when a pump operates at less than 10% of its best efficiency point. This phenomenon must be managed to avoid operational inefficiencies and potential damage.

Incorporating these technical nuances into market analysis allows stakeholders to navigate potential challenges effectively while capitalizing on the inherent benefits of advanced cavitated film technologies. As the market continues to evolve, the adoption of these specialized films is expected to increase, driven by their operational and cost efficiencies, aligning with the broader trends toward sustainability and reduced resource usage in the packaging industry.

Key Takeaways

- The Global Cavitated Films Market is expected to be worth around USD 6.2 Billion by 2033, up from USD 3.8 Billion in 2023, and grow at a CAGR of 5.0% from 2024 to 2033.

- BOPP dominates the Cavitated Films market with a substantial 58.1% share by type.

- Polypropylene (PP) is the preferred material, capturing 45.2% of the market by material.

- Films with a thickness between 20-40 microns represent 47.1% of the market by thickness.

- Bags and pouches lead applications, constituting 36.1% of the market by application.

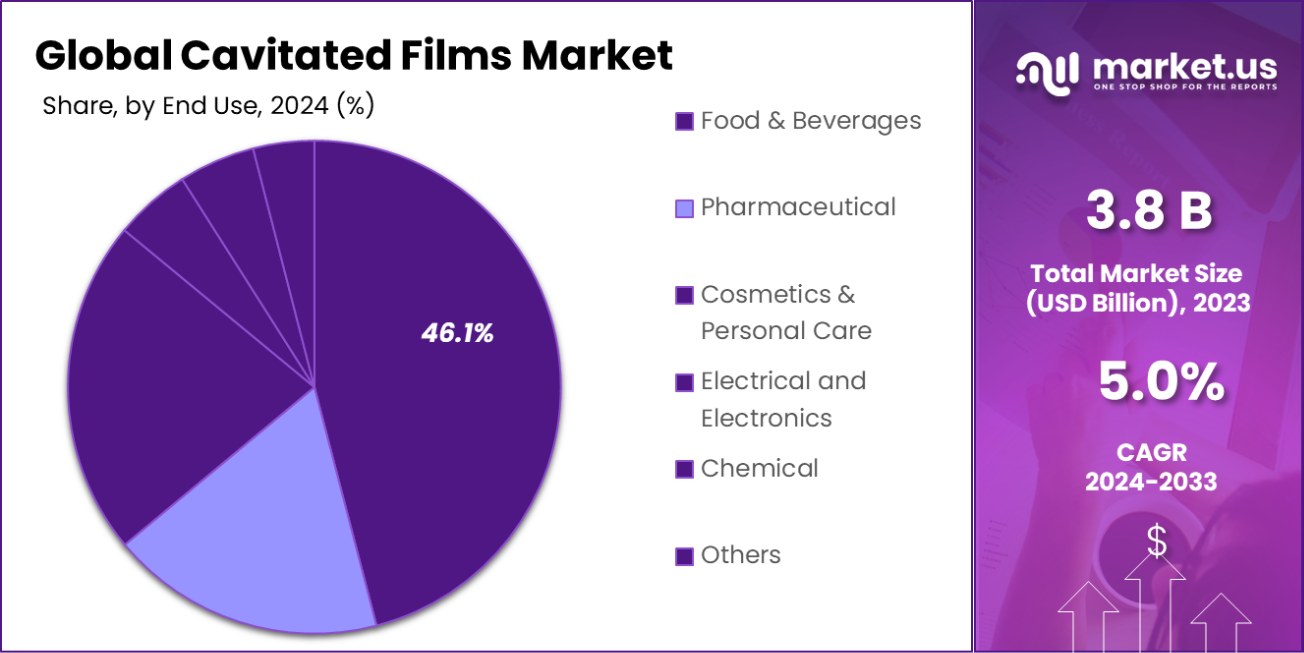

- The food & beverages sector is the largest end-user, holding 46.1% of the market.

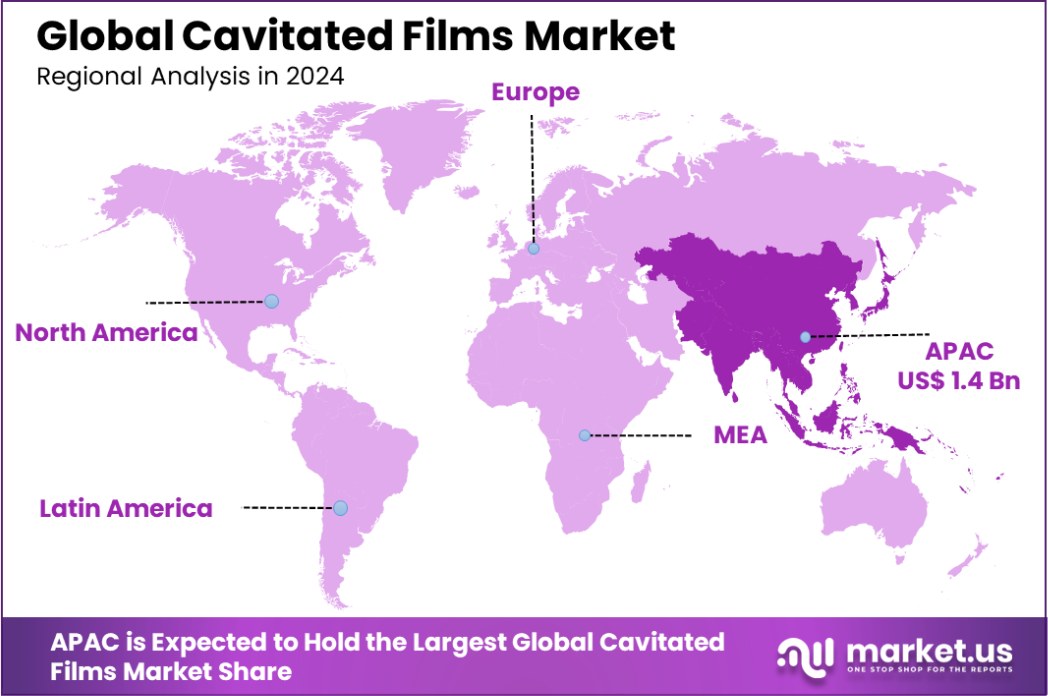

- Asia-Pacific holds 38.3% of the cavitated films market, USD 1.4 billion.

By Type Analysis

In 2023, BOPP dominated the Cavitated Films Market by type, capturing a significant 58.1% market share.

In 2023, BOPP held a dominant market position in the “By Type” segment of the Cavitated Films Market, commanding a 58.1% share. Its counterpart, PET, secured a lesser share, illustrating a clear preference for BOPP in this sector.

The preference for BOPP can be attributed to its superior barrier properties, cost-effectiveness, and higher mechanical strength, which are critical for packaging applications. These attributes have driven its adoption across various industries, notably in food packaging, where extended shelf life and product integrity are paramount.

Furthermore, the market dynamics of the Cavitated Films industry show a trend towards sustainable packaging solutions, which further bolsters the demand for BOPP. This material is not only efficient in performance but also aligns with the increasing regulatory and consumer demands for environmentally friendly packaging options.

On the other hand, PET, while also beneficial for its clarity and recyclability, faces challenges in competing with the economic and functional advantages offered by BOPP. This competitive landscape indicates a robust growth trajectory for BOPP in the coming years, as innovations and improvements in film technology continue to enhance its appeal to manufacturers and end-users alike.

By Material Analysis

Polypropylene (PP) led the material segment in the Cavitated Films Market with a 45.2% share, demonstrating strong demand.

In 2023, Polypropylene (PP) held a dominant market position in the “By Material” segment of the Cavitated Films Market, with a 45.2% share. This was followed by Polyethylene (PE), Biaxially Oriented Polyester (BOPET), Polyamide (PA), Polystyrene (PS), and Polyvinyl Chloride (PVC), each capturing varying shares that collectively shape the competitive landscape of this market.

The dominance of PP can be attributed to its favorable properties such as moisture resistance, flexibility, and excellent chemical resistance, which make it highly suitable for the packaging industry.

Polyethylene (PE) also plays a significant role in the market, valued for its strength, durability, and clarity, making it ideal for both consumer and industrial applications. BOPET, noted for its high tensile strength and transparency, finds extensive use in sophisticated packaging solutions.

Meanwhile, Polyamide (PA) is favored for its barrier properties against oxygen and aroma, essential for food preservation. Polystyrene (PS) and Polyvinyl Chloride (PVC) round out the market, with specific uses in niche applications due to their unique characteristics.

The ongoing development and enhancement of these materials are likely to drive their adoption further, influenced by evolving demands for sustainable and advanced packaging solutions.

By Thickness Analysis

The 20-40 Microns category was most preferred in thickness, holding a 47.1% share in the Cavitated Films Market.

In 2023, the 20-40 Microns category held a dominant market position in the “By Thickness” segment of the Cavitated Films Market, with a 47.1% share. This was followed by Below 20 Microns, 41-70 Microns, and Above 70 Microns, each contributing differently to the market’s configuration.

The prominence of the 20-40 Microns thickness range can be primarily attributed to its optimal balance between strength and flexibility, making it highly desirable for a broad spectrum of packaging applications. This thickness ensures sufficient durability for handling and transportation while maintaining cost-efficiency and material usage effectiveness.

The Below 20 Microns segment caters primarily to applications requiring high clarity and flexibility, such as overwrap and personal care product packaging. Meanwhile, the 41-70 Microns segment is favored in applications demanding enhanced protective properties and structural integrity, including food and industrial goods packaging.

The Above 70 Microns thickness is less common but vital for specialized heavy-duty applications where superior barrier properties and puncture resistance are required. The market trends suggest that the demand for the 20-40 Microns segment will continue to grow, driven by its versatility and adaptability to various consumer needs and environmental regulations.

By Application Analysis

Bags and pouches were the leading application for Cavitated Films, accounting for 36.1% of the market in 2023.

By End Use Analysis

Food & Beverages maintained the highest usage of Cavitated Films, dominating the end-use segment with a 46.1% share.

In 2023, the Food & Beverages sector held a dominant market position in the “By End Use” segment of the Cavitated Films Market, commanding a 46.1% share. This sector outpaced other end-use segments including Pharmaceutical, Cosmetics & Personal Care, Electrical and Electronics, and Chemical.

The predominant use of cavitated films in the Food & Beverages industry is primarily due to their exceptional barrier properties against gases, odors, and moisture, which are crucial for preserving the freshness, flavor, and quality of food products.

The demand within the Food & Beverages sector is propelled by the growing need for extended shelf life of products and the shift towards more sustainable packaging solutions that offer reduced material usage without compromising protective features.

Cavitated films are particularly valued in this sector for their ability to be used in lightweight packaging designs that maintain structural integrity and visual appeal—key factors influencing consumer purchasing decisions.

Meanwhile, segments like Pharmaceuticals Cosmetics & Personal Care also leverage these films for their protective qualities, but their market shares are significantly smaller compared to Food & Beverages.

The Electrical and Electronics, as well as the Chemical sectors, utilize these films for specialized packaging that requires durability and resistance to harsh environments, further underscoring the versatility of cavitated films across diverse industries.

Key Market Segments

By Type

- BOPP

- PET

By Material

- Polypropylene (PP)

- Polyethylene (PE)

- Biaxially Oriented Polyester (BOPET)

- Polyamide (PA)

- Polystyrene (PS)

- Polyvinyl Chloride (PVC)

By Thickness

- Below 20 Microns

- 20-40 Microns

- 41-70 Microns

- Above 70 Microns

By Application

- Bags and Pouches

- Lamination

- Tapes

- Labels

- Wraps

- Others

By End Use

- Food & Beverages

- Pharmaceutical

- Cosmetics & Personal Care

- Electrical and Electronics

- Chemical

- Others

Driving Factors

Rising Demand for Lightweight Packaging Solutions

The cavitated films market is experiencing significant growth, largely driven by the increasing demand for lightweight packaging materials. Industries such as food and beverage, personal care, and pharmaceuticals are opting for cavitated films due to their reduced material usage without compromising package integrity.

This shift towards lightweight solutions not only helps in lowering transportation costs but also aligns with the global push towards sustainability by reducing the overall environmental impact of packaging.

Enhancements in Product Shelf Life and Protection

Cavitated films offer exceptional barrier properties, which are essential for extending the shelf life of perishable goods. The ability of these films to protect against moisture, oxygen, and other external factors makes them a preferred choice for manufacturers looking to ensure product integrity from production to consumer.

As consumer expectations for longer-lasting products increase, the demand for cavitated films continues to rise, thereby driving market expansion.

Adoption of Eco-Friendly Packaging Practices

Environmental concerns are steering both consumers and manufacturers towards more sustainable packaging options. Cavitated films are increasingly favored as they are often produced with recyclable materials and involve processes that generate less waste compared to traditional packaging films.

This adoption is supported by stringent environmental regulations and a growing consumer preference for green products, which in turn propels the market growth of cavitated films, marking them as a key player in the sustainable packaging industry.

Restraining Factors

High Production Costs Limit Market Accessibility

The production of cavitated films involves complex manufacturing processes and advanced materials, which can significantly increase production costs. These elevated costs may deter smaller manufacturers or those in developing regions from adopting cavitated film technology, limiting the market’s growth potential.

Additionally, the investment required for upgrading existing machinery to handle cavitated films can be substantial, posing a financial challenge for companies considering a transition to this technology.

Competition from Alternative Packaging Materials

Cavitated films face stiff competition from other innovative packaging solutions like biodegradable films and multi-layer laminate films, which may offer similar or better attributes at lower costs or with enhanced environmental benefits.

This competition can restrain the growth of the cavitated films market as manufacturers and consumers weigh the advantages and disadvantages of various options available to them. The presence of alternatives also provides opportunities for price and feature comparisons, which can hinder the adoption rate of cavitated films.

Regulatory and Environmental Compliance Challenges

Regulatory frameworks governing packaging materials are becoming increasingly stringent worldwide, focusing on the sustainability and recyclability of materials. While cavitated films are generally considered eco-friendly, the specifics of their production processes and material compositions must consistently adhere to evolving environmental standards.

Failure to comply with these regulations can result in penalties, product recalls, or bans, which can restrain market growth. Additionally, the necessity for continuous adaptation to regulatory changes can impose further financial and operational burdens on producers.

Growth Opportunity

Expansion into Emerging Markets Boosts Potential Revenue

The cavitated films market holds significant growth potential in emerging markets, where rapid industrialization and increasing consumer spending are prevalent. These regions are experiencing a surge in demand for packaged goods due to growing urban populations and rising income levels.

By expanding into these markets, companies can tap into new consumer bases eager for products that offer durability and sustainability, two key benefits of cavitated films. This strategic market expansion can drive considerable revenue growth and diversify the geographic footprint of businesses in the cavitated films industry.

Innovations in Biodegradable Cavitated Films Enhance Market Appeal

There is a growing opportunity for innovation in developing biodegradable cavitated films that meet both consumer demand for sustainability and industry needs for efficient packaging solutions. By focusing on research and development to create cavitated films that can degrade naturally without leaving harmful residues, manufacturers can not only comply with stringent environmental regulations but also attract a broader base of eco-conscious consumers.

This shift towards biodegradable options is expected to open new segments and increase market share in the competitive packaging industry.

Collaborations with Food and Beverage Giants Propel Growth

Partnering with major players in the food and beverage industry presents a lucrative growth opportunity for the cavitated films market. These industries require reliable and efficient packaging solutions that ensure product safety and extend shelf life.

By collaborating with these industry giants, cavitated film producers can secure large-volume orders and long-term contracts, which provide stable revenue streams and enhance market visibility. Such partnerships also facilitate tailored product development, aligning the properties of cavitated films closely with the specific packaging needs of these sectors.

Latest Trends

Shift Towards Ultra-Thin Cavitated Films for Cost Efficiency

A prominent trend in the cavitated films market is the shift towards the production of ultra-thin films. These films provide the same durability and protective qualities as thicker versions but use less material, resulting in cost savings for both manufacturers and end-users.

The trend towards thinner films not only supports cost-effective production practices but also aligns with sustainability goals by reducing the overall material footprint. This shift is driven by technological advancements in film production that allow for precise thickness control without compromising film integrity.

Increased Use of Cavitated Films in Flexible Packaging

There is a noticeable increase in the adoption of cavitated films within the flexible packaging sector. Flexible packaging, favored for its lightweight and reduced material use, is becoming more prevalent in various industries, including food, healthcare, and consumer goods.

Cavitated films are particularly suitable for this application due to their excellent barrier properties and ability to maintain product freshness. This trend is fueled by the growing consumer preference for convenient, durable, and sustainable packaging solutions, positioning cavitated films as a key component in the evolution of flexible packaging technologies.

Integration of Digital Printing Technology with Cavitated Films

The integration of digital printing technology with cavitated films is a developing trend that enhances the visual appeal and functionality of packaged goods. Digital printing on cavitated films allows for high-quality, customizable, and vibrant graphics that can be changed easily without significant downtime or expense.

This capability is particularly advantageous for brands that require fast turnaround for limited editions or personalized packaging campaigns. As digital printing technology advances, its application on cavitated films is expected to grow, offering significant marketing benefits and adding value to the traditional uses of these films.

Regional Analysis

The Asia-Pacific cavitated films market holds a 38.3% share, valued at USD 1.4 billion.

In Asia-Pacific, the region dominates the global market with a 38.3% share, translating to USD 1.4 billion. This leadership is driven by rapid industrialization, increasing consumer expenditure on packaged goods, and significant investments in packaging technologies. Countries like China and India are pivotal, with their expanding middle class and growing demand for sustainable packaging solutions.

North America follows, characterized by advanced technological adoption and stringent regulatory standards that foster innovations in eco-friendly packaging solutions. The U.S. leads in this region, focusing on sustainable and flexible packaging solutions that cater to the convenience and sustainability demands of consumers.

In Europe, the market is propelled by high environmental awareness and strict regulations regarding packaging materials. European countries are leaning heavily towards adopting materials that contribute to circular economy goals, boosting the demand for recyclable cavitated films.

The Middle East & Africa region, though smaller in market size, is witnessing gradual growth due to rising urbanization and improved retail infrastructure. Efforts to modernize packaging standards and enhance food safety are key drivers in this region.

Lastly, Latin America shows potential for growth with its increasing local manufacturing and rising consumer awareness about sustainable packaging. Countries like Brazil and Mexico are experiencing a shift towards modern retail formats, which in turn fuels the demand for advanced packaging materials like cavitated films.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the global cavitated films market, key players are leveraging their technological and innovation capabilities to secure and expand their market positions. Among these, Amcor plc stands out for its strategic focus on sustainability and innovation.

Amcor is harnessing advanced material science to develop lighter, more flexible, and recyclable cavitated films that meet stringent global standards for environmental responsibility. This approach not only caters to the growing consumer demand for sustainable packaging but also positions Amcor as a leader in eco-friendly packaging solutions.

Ampacet Corporation is another notable competitor, specializing in the production of innovative plastic compounds and masterbatch solutions, essential for enhancing the properties of cavitated films. Their focus on customization and functionality improvements in film applications enables them to meet diverse industry needs effectively.

Brückner Group GmbH, along with its subsidiary Brückner Maschinenbau GmbH, remains a formidable force, primarily due to their prowess in engineering and plant manufacturing. They offer a range of equipment and technologies that facilitate the production of high-quality cavitated films, emphasizing efficiency and performance.

CCL Industries and Cosmo Films Ltd. are also significant contributors to the market, with CCL Industries focusing on high-performance labels and packaging solutions, and Cosmo Films emphasizing innovations in barrier properties and film longevity.

Lastly, Exxon Mobil Corporation, through its chemical division, plays a critical role in providing the raw materials necessary for cavitated film production, such as high-grade polymers that enhance film characteristics.

Overall, these companies are not only driving the market through innovations and sustainability efforts but are also intensely competitive, continually adapting to the evolving demands of the packaging industry. This dynamic is crucial for understanding market trajectories and the areas of strategic investment necessary to maintain and grow market share in this industry.

Top Key Players in the Market

- Amcor plc

- Ampacet Corporation

- Brückner Group GmbH

- Brückner Maschinenbau GmbH

- Carrer Boters s/n

- CCL Industries

- CHIRIPAL POLY FILM

- Cosmo Films Ltd.

- Exxon Mobil Corporation

- Flex Films

- GCR Group

- Guangdong Decro Film

- Innovia Films

- Inteplast Group

- Jindal Poly Films

- JPFL Films Private Limited

- KristaFilms

- MANUCOR SPA.

- Megapolis Group

- Mitsui Chemicals

- Nahar PolyFilms Ltd.

- New Materials Co. Ltd.

- Oben Group

- Polinas

- POLYFIL

- Rowad National Plastic Co., Ltd.

- S.A. de C.V.

- SIBUR petrochemical group

- Silgan Holdings Inc.

- Süper Film Packaging Industry Inc.

- Transparent Paper Ltd.

- Vacmet India

- VALTEC ITALIA

- Vibac Group S.p.a.

- vpipl

- Yem Chio Co. Ltd.

Recent Developments

- In 2024, involved Brückner collaborated with Italian film producer IRPLAST to implement a new simultaneous LISIM® line for BOPP film production. This line is set to commence full operation by the end of 2025 and is expected to add 25,000 tonnes to the production capacity for specialty films. This project highlights Brückner’s continued innovation in film production technology, focusing on energy efficiency and high-quality standards.

- In 2024, Mitsui Chemicals includes the continuation of their efforts in recycling technologies, particularly in the joint development of a mono-material film packaging material that simplifies recycling processes by eliminating petroleum solvents from inks and adhesives, making it entirely recyclable

- In 2023, Amcor plc announced their focus on producing recyclable thermoforming films that significantly reduce the carbon footprint compared to previous materials. This development aligns with their sustainability targets set for 2025, aiming for all their packaging products to be recyclable or reusable.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 3.8 Billion |

| Forecast Revenue (2033) | USD 6.2 Billion |

| CAGR (2024-2033) | 5.0% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (BOPP, PET), By Material (Polypropylene (PP), Polyethylene (PE), Biaxially Oriented Polyester (BOPET), Polyamide (PA), Polystyrene (PS), Polyvinyl Chloride (PVC)), By Thickness (Below 20 Microns, 20-40 Microns, 41-70 Microns, Above 70 Microns), By Application (Bags and Pouches, Lamination, Tapes, Labels, Wraps, Others), By End Use (Food & Beverages, Pharmaceutical, Cosmetics & Personal Care, Electrical and Electronics, Chemical, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Amcor plc, Ampacet Corporation, Brückner Group GmbH, Brückner Maschinenbau GmbH, Carrer Boters s/n, CCL Industries, CHIRIPAL POLY FILM, Cosmo Films Ltd., Exxon Mobil Corporation, Flex Films, GCR Group, Guangdong Decro Film, Innovia Films, Inteplast Group, Jindal Poly Films, JPFL Films Private Limited, KristaFilms, MANUCOR SPA., Megapolis Group, Mitsui Chemicals, Nahar PolyFilms Ltd., New Materials Co. Ltd., Oben Group, Polinas, POLYFIL, Rowad National Plastic Co., Ltd., S.A. de C.V. , SIBUR petrochemical group, Silgan Holdings Inc., Süper Film Packaging Industry Inc., Transparent Paper Ltd., Vacmet India, VALTEC ITALIA, Vibac Group S.p.a., vpipl, Yem Chio Co. Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |