Quick Navigation

- Report Overview

- Key Takeaways

- Product Type Analysis

- Application Analysis

- Stabilizer Type Analysis

- End Use Industry Analysis

- Key Market Segments

- Driver Analysis

- Restraint Analysis

- Opportunity Analysis

- Challenges Analysis

- Geopolitical Impact Analysis

- Regional Analysis

- Key Players Analysis

- Key Development

- Report Scope

Report Overview

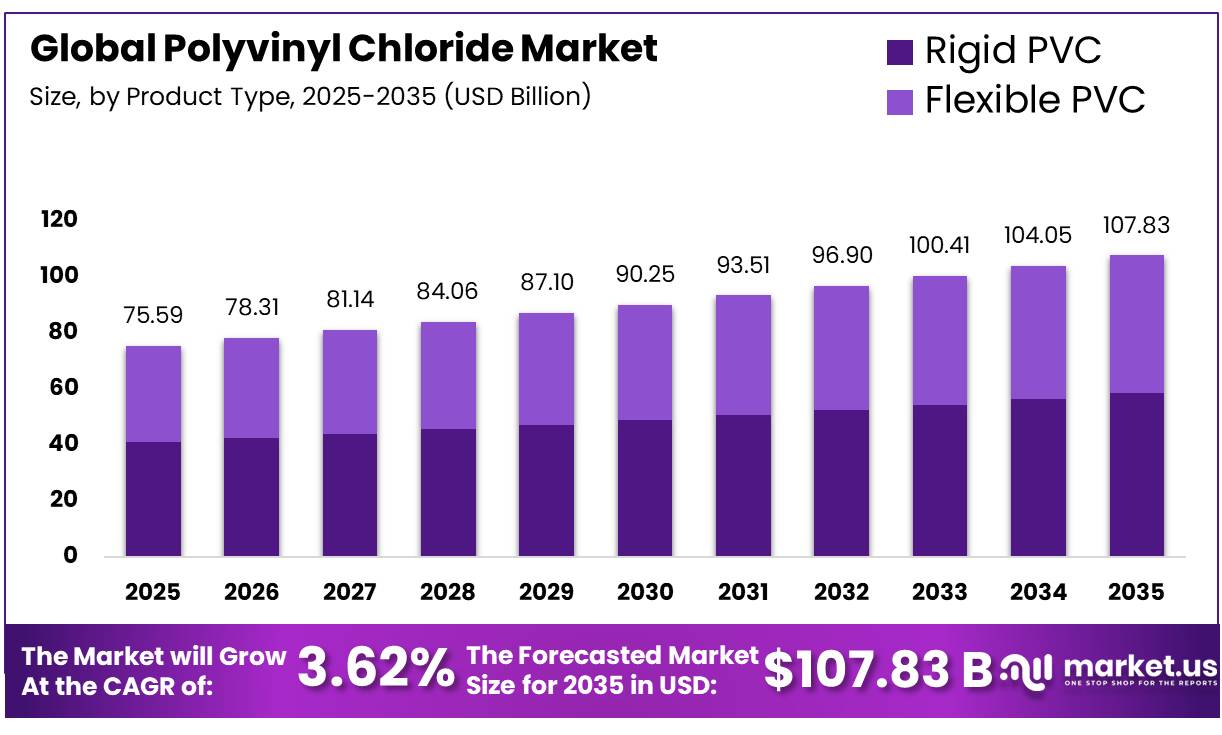

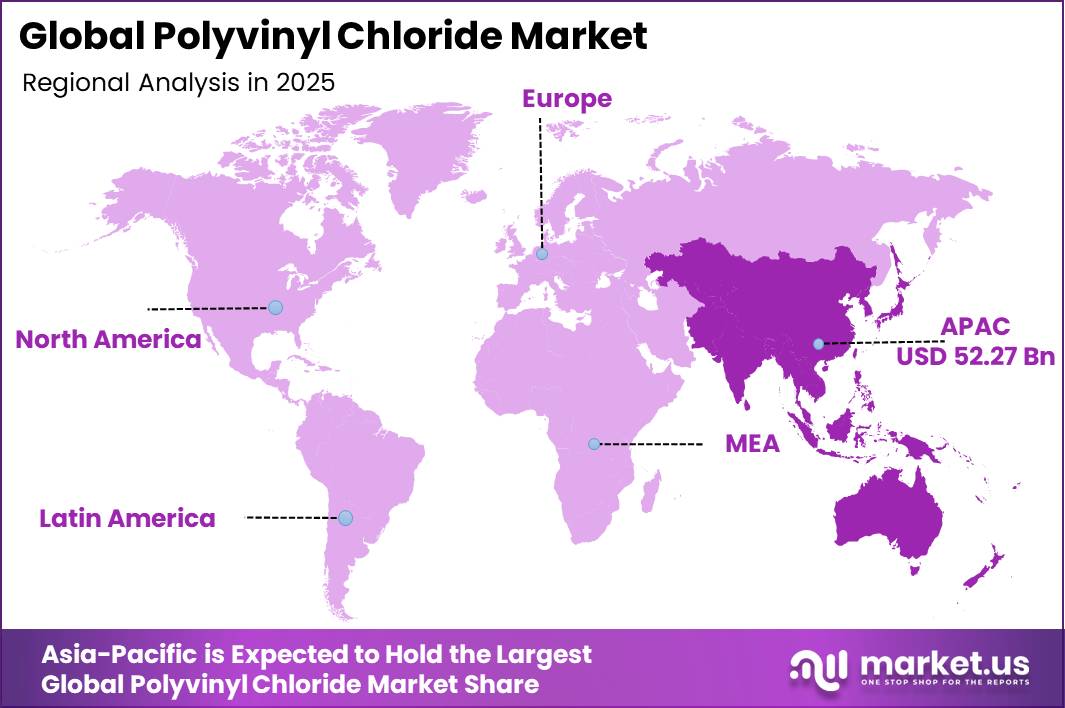

In 2025, the Global Polyvinyl Chloride Market was valued at US$75.59 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 3.62%, reaching about US$107.83 billion by 2035. In 2025, Asia Pacific led the market, achieving over 69.14% share with a revenue of US$52.27 billion.

Polyvinyl chloride (PVC) is one of the most widely used thermoplastics in the world and is produced by polymerizing vinyl chloride monomer (VCM). Unlike many other plastics, PVC has a unique raw material composition, with around 57% derived from common salt and 43% from oil or natural gas. This lower dependence on fossil-based feedstocks makes it an important material for industries seeking durable and cost-effective plastic solutions.

PVC is available in both rigid and flexible forms and is widely used in pipes, fittings, window profiles, flooring, roofing membranes, cable insulation, medical tubing, packaging, and automotive components. According to PlasticsEurope (2026), PVC is the third most-produced synthetic polymer globally, after polyethylene and polypropylene.

- According to Euro Chlor, April 2026, European chlorine production reached 629,642 tonnes, reflecting the large upstream production capacity supporting the PVC industry.

- VinylPlus progress Report 2026 reported that imported virgin PVC, PVC compounds, and PVC contained in finished products accounted for 19% of the European PVC market in 2025, highlighting the region’s continued dependence on imports.

Key Takeaways

- The Global Polyvinyl Chloride Market was valued at USD 75.59 billion in 2025.

- The market is projected to grow at a CAGR of 3.62% and is estimated to reach USD 107.83 billion by 2035.

- Rigid PVC dominated by product type at 54.23% in 2025, driven by extensive use in pipes, profiles, and fittings.

- Pipes, profiles & fittings dominated by application at 45.17%, driven by infrastructure and building construction demand.

- Calcium-based (Ca-Zn) stabilizers dominated by stabilizer type at 51.54%, driven by growing adoption as a safer alternative to lead-based systems.

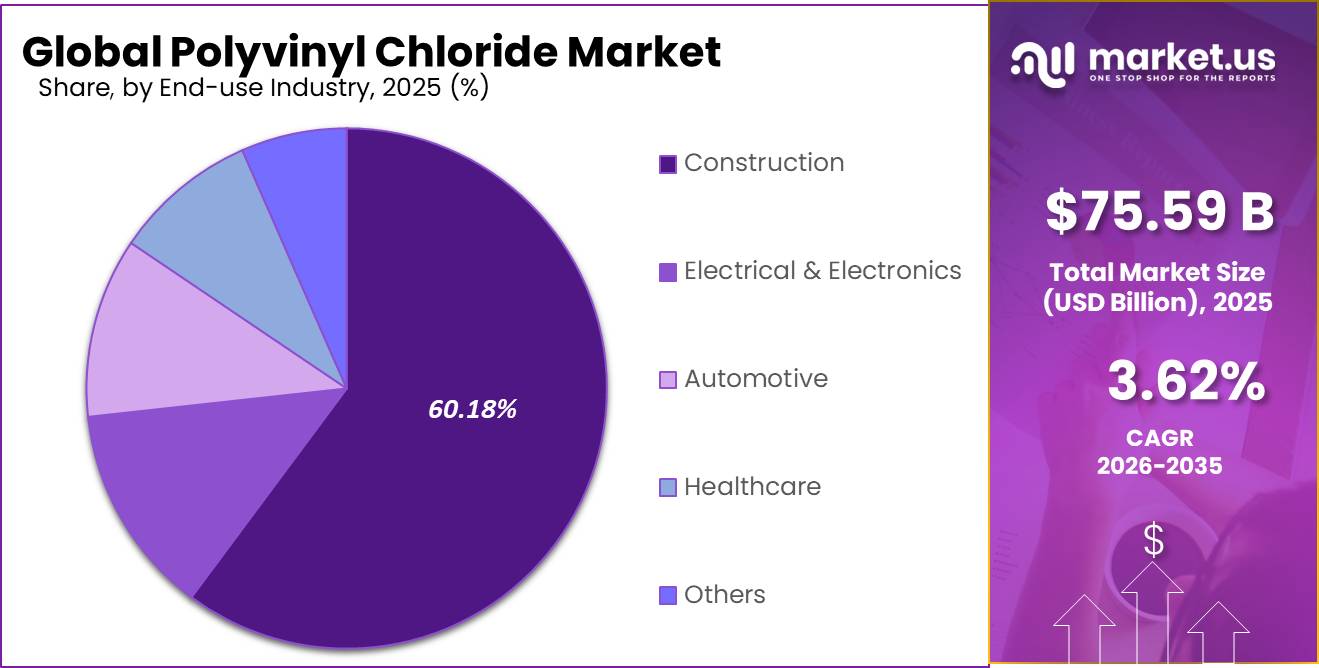

- Construction dominated by end use industry at 60.18%, driven by rising demand for PVC pipes, fittings, window profiles, and flooring.

- Asia-Pacific dominated regionally at 69.14%, driven by large-scale construction activity and expanding manufacturing capacity across China, India, and Southeast Asia.

PVC production begins with the chlor-alkali process, where salt is converted into chlorine, caustic soda, and hydrogen. Chlorine is then combined with ethylene to produce ethylene dichloride (EDC), which is further processed into vinyl chloride monomer before being polymerized into PVC resin. A strong chlor-alkali industry is therefore essential for PVC manufacturing.

The construction industry continues to be the largest consumer of PVC because the material offers corrosion resistance, long service life, low maintenance costs, and easy installation. It is widely used in water pipes, drainage systems, electrical conduits, flooring, roofing membranes, and window profiles. Growing electrification is also increasing demand for PVC in cable insulation and electrical conduit applications. The material is widely preferred because it provides excellent insulation, flame resistance, durability, and cost efficiency.

- According to the International Energy Agency (IEA, Electricity 2026 Report), global electricity demand is expected to grow by an average of 3.6% per year between 2026 and 2030.

Sustainability and recycling are becoming increasingly important across the PVC value chain. Manufacturers are investing in recycled materials, energy-efficient production technologies, and lower-carbon manufacturing processes to meet environmental regulations and customer expectations. Recycling technologies continue to improve, companies that strengthen recycled material use, enhance energy efficiency, and develop circular manufacturing systems are expected to remain well positioned for long-term growth.

- According to the VinylPlus Progress Report 2026, Europe recycled 765,972 tonnes of PVC waste during 2025, representing a 5.7% increase compared with 2024. Under the company’s 2030 Commitment, the organization aims to use at least 1 million tonnes of recycled PVC annually by 2030.

Product Type Analysis

Rigid PVC Dominates the Polyvinyl Chloride Market with 54.23% Share Due to Strong Demand for Durable Infrastructure Materials

In 2025, Rigid PVC held a dominant market position, capturing more than a 54.23% share of the global Polyvinyl Chloride (PVC) market. The segment maintained its leading position because rigid PVC is widely used in water supply pipes, sewer systems, window and door profiles, electrical conduits, and industrial applications where high strength, durability, and corrosion resistance are essential. Its long service life, low maintenance requirements, and cost-effectiveness make it the preferred choice for construction and infrastructure projects worldwide.

- According to the U.S. Environmental Protection Agency (EPA), the 7th Drinking Water Infrastructure Needs Survey and Assessment, released in 2025, estimates that the United States requires USD 625 billion in drinking water infrastructure investment over the next 20 years to maintain and upgrade existing systems.

Flexible PVC is the fastest growing segment in the global Polyvinyl Chloride (PVC) market due to its excellent flexibility, lightweight nature, and strong insulation properties. It is increasingly used in wire and cable insulation, medical tubing, blood bags, flooring, automotive interiors, packaging films, and consumer products. Growing investments in power infrastructure, healthcare facilities, and electric vehicle charging networks are driving the demand for flexible PVC products.

Application Analysis

Pipes, Profiles & Fittings Dominates the Polyvinyl Chloride Market with 45.17% Share Driven by Strong Construction Demand

In 2025, Pipes, Profiles & Fittings held a dominant market position, capturing more than a 45.17% share of the global Polyvinyl Chloride (PVC) market. The segment maintained its leadership because PVC is widely used in water supply pipelines, drainage systems, window profiles, door frames, electrical conduits, and building fittings due to its durability, corrosion resistance, and low maintenance requirements. Continued investments in residential, commercial, and public infrastructure projects supported steady demand for these products throughout the year. Government-backed infrastructure spending also strengthened consumption.

- According to the U.S. Census Bureau and the U.S. Department of Housing and Urban Development, privately owned housing starts reached a seasonally adjusted annual rate of 1.177 million units in May 2026, supporting demand for PVC pipes, profiles, doors, windows and fittings used in residential construction.

Films & Sheets is the fastest growing segment in the Polyvinyl Chloride (PVC) market during 2025, supported by increasing demand from packaging, healthcare, construction, and industrial applications. PVC films and sheets are widely used because they offer excellent transparency, durability, moisture resistance, and ease of processing. Growing demand for protective packaging, medical packaging materials, laminated sheets, and flexible construction products continues to support market expansion. In addition, higher industrial production and infrastructure activities are creating new opportunities for PVC sheet applications across multiple sectors.

Stabilizer Type Analysis

Calcium-based (Ca-Zn) Stabilizers dominate with a 51.54% share due to the shift toward safer PVC formulations

In 2025, Calcium-based (Ca-Zn) Stabilizers held a dominant market position, capturing more than a 51.54% share. The segment remained ahead because these stabilizers provide effective heat protection without relying on lead-based compounds. They are widely used in PVC pipes, profiles, flooring, cables and other construction products. Regulatory controls have strengthened their adoption.

- The World Health Organization reported in June 2026 that lead exposure was linked to more than 3.5 million deaths globally in 2023 and confirmed that no level of lead exposure is known to be harmless.

End Use Industry Analysis

Construction Dominates the Polyvinyl Chloride Market with 60.08% Share Backed by Strong Infrastructure and Housing Projects

In 2025, Construction held a dominant market position, capturing more than a 60.08% share of the global Polyvinyl Chloride (PVC) market. The segment maintained its leading position because PVC remains one of the most widely used materials in residential, commercial, and infrastructure projects. It is extensively used in pipes, window and door profiles, flooring, roofing membranes, wall panels, electrical conduits, and drainage systems due to its durability, corrosion resistance, long service life, and low maintenance requirements.

- According to the U.S. Census Bureau, total U.S. construction spending reached a seasonally adjusted annual rate of USD 2.1724 trillion in April 2026, including USD 909.9 billion in residential construction, reflecting sustained demand for building materials such as PVC.

Electrical & Electronics is the fastest growing segment in the global Polyvinyl Chloride (PVC) market due to the increasing need for reliable insulation materials in power transmission, communication networks, consumer electronics, and industrial electrical systems. PVC is widely used for wire and cable insulation, electrical conduits, connectors, and protective coverings because of its excellent electrical insulation, flame resistance, durability, and cost efficiency.

- According to the U.S. Energy Information Administration (EIA) in April 2026, after nearly 15 years of relatively flat electricity consumption, U.S. electricity demand has increased by an average of 2.1% per year in recent years, supporting continued investments in power infrastructure and driving demand for PVC-insulated wires, cables, and electrical conduits.

Key Market Segments

By Product Type

- Rigid PVC

- Flexible PVC

By Application

- Pipes, Profiles & Fittings

- Films & Sheets

- Cables & Wires

- Flooring

- Packaging

- Others

By Stabilizer Type

- Calcium-based (Ca-Zn) Stabilizers

- Lead-based Stabilizers

- Organotin Stabilizers

- Others

By End Use Industry

- Construction

- Electrical & Electronics

- Automotive

- Healthcare

- Others

Driver Analysis

Water-grid buildout and rural pipe connectivity demand

India’s rural water rollout remains one of the clearest volume supports for PVC pipe demand because the Jal Jeevan Mission moved from only 17% rural tap-water coverage at launch in August 2019 to about 15.69 crore connected households out of 19.36 crore, or 81.02%, by 10 February 2026, implying 12.56 crore incremental household connections added during the program and more than 2.72 lakh villages reported at full coverage.

Strategically, this driver supports a roughly +1.4 percentage-point lift to PVC market CAGR because it converts public capex into repetitive off-take for pipe converters, rewards producers with strong tender qualification and compound formulation capability, and creates follow-on aftermarket demand in gaskets, joints, repair lengths, and small-diameter service lines across India and neighboring South Asian procurement ecosystems.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-grid buildout and rural pipe connectivity demand | +1.4% | India core, South Asia spill-over | Short term (≤ 2 years) |

| Public infrastructure and utility construction pipeline | +1.1% | North America core, India, selected EU corridors | Medium term (2-4 years) |

| Lead-free compliance and specification renewal in PVC applications | +0.9% | EU core, India regulated tenders, export-linked Asia | Short term (≤ 2 years) |

| Trade protection lifting regional PVC margins | +0.7% | EU core, US export chain, MENA rerouting | Medium term (2-4 years) |

| Vinyl chloride regulatory scrutiny accelerating asset upgrades | +0.5% | North America core, multinational supply chains | Medium term (2-4 years) |

| Energy-cost and chlor-alkali integration advantage | +0.8% | US Gulf Coast, Middle East, China cost clusters, EU deficit zones | Long term (≥ 4 years) |

Restraint Analysis

Construction demand softness

PVC’s largest end-use pool remains building products, so even modest construction deceleration has an outsized volume effect: U.S. building permits in June 2026 ran at 1.367 million SAAR, 3.0% below May and 2.3% below June 2025, while June 2025 euro-area construction output had already fallen 0.8% month on month after a 2.1% decline in May, signaling stop-start project execution rather than a clean recovery.

For pipe, siding, window profile, wire-and-cable conduit, and flooring suppliers, that translates into lower plant operating rates, higher fixed-cost absorption pressure, and slower inventory turns; in market terms, a 2% to 4% swing in housing-linked demand typically strips roughly 0.8 to 1.3 percentage points from near-term PVC volume growth because construction applications consume a large share of rigid resin demand and distributors respond by stretching reorder cycles rather than rebuilding stock aggressively.

The strategic damage is not only top-line: lower throughput compresses converter EBITDA through weaker spread capture, raises working-capital intensity as finished-goods days extend by an estimated 10 to 20 days in soft channels, and delays incremental debottlenecking or compounding CapEx because management teams will not commit new assets until permit issuance and project starts show at least two to three consecutive quarters of stability.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction demand softness | -1.1% | North America core, EU | Short term (≤ 2 years) |

| Lead-in-PVC compliance costs | -0.8% | EU core, UK-linked exports | Medium term (2-4 years) |

| Vinyl chloride regulatory risk | -0.7% | North America core | Medium term (2-4 years) |

| Energy-intensive chlor-alkali volatility | -0.9% | EU, North America, Northeast Asia | Short term (≤ 2 years) |

| Tariff and import-duty friction | -0.6% | India, North America, select APAC corridors | Medium term (2-4 years) |

| Construction-cycle fragmentation | -0.5% | EU, North America | Long term (≥ 4 years) |

Opportunity Analysis

Rural-urban water grid packages

This is not a present driver because baseline PVC demand already reflects normal irrigation, housing, and civic pipe consumption; the opportunity is the still-underpenetrated shift from commodity pipe sales to programmatic water-network packages tied to India’s last-mile connectivity gap and urban wastewater build-out.

The Jal Jeevan Mission dashboard and related government reporting indicate that rural household tap-connection rollout has moved into a late-stage execution phase with roughly 15.8 crore households connected by mid-2026, while AMRUT 2.0 carries an indicative outlay of about ₹2.77 lakh crore to ₹2.99 lakh crore for universal urban water supply and sewerage/septage coverage across statutory towns and 500 cities, creating a large addressable pipe-and-fittings opportunity beyond current baseline demand.

The white space is in converting fragmented public tenders into integrated district packages spanning potable water, sewer laterals, and maintenance contracts; if organized PVC converters localize diameters, reduce installation leakage losses by 2% to 4%, and attach annuity-style aftersales worth 6% to 8% of project value, the addressable upside in India and adjacent South Asian markets could support around 1.9 percentage points of incremental CAGR over baseline within a short execution window.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Lead-pipe replacement systems | +1.6% | North America core | Short term (≤ 2 years) |

| Rural-urban water grid packages | +1.9% | India, South Asia, APAC emerging | Short term (≤ 2 years) |

| Circular PVC compounding platforms | +1.4% | EU core, UK | Medium term (2-4 years) |

| Ethane-to-PVC export arbitrage | +1.2% | U.S. Gulf Coast, Latin America, Africa | Medium term (2-4 years) |

| Medical-grade flexible PVC expansion | +0.9% | Asia, Middle East, Africa | Medium term (2-4 years) |

| PVC retrofit-for-efficiency solutions | +1.1% | EU, North America, developed APAC | Long term (≥ 4 years) |

Challenges Analysis

Capacity ramp‑up and asset reliability

Large‑scale capacity additions in Asia Pacific and the Middle East, encouraged by national industrial and petrochemical policies, introduce a multi‑year phase of ramp‑up risk where plants operate below nameplate capacity and face reliability issues that ripple across regional PVC supply. In India alone, studies project nearly 2.5 million tonnes of new domestic PVC capacity by FY 2026–27, effectively more than doubling prior production levels and shifting the supply mix from roughly 38% domestic to about 74% domestic within three financial years.

Globally, PVC plants are capital‑intensive assets with typical nameplate capacities of 300,000–400,000 tonnes per year, and early‑phase utilization rates often sit 10–20 percentage points below design due to learning curves, feedstock imbalances, and maintenance stabilisation. Each 10 percentage‑point gap between nameplate and actual throughput equates to 30,000–40,000 tonnes of “latent” capacity per plant, which must be bridged through incremental investments in reliability engineering, spare parts inventory, and process control upgrades, pushing unit fixed costs higher by USD 15–25 per tonne in the ramp‑up window.

Because several of these expansions cluster in emerging industrial corridors with infrastructure and utility constraints, unplanned outages and deratings can knock 5–10% of regional supply offline for weeks at a time, forcing downstream sectors such as construction and pipe manufacturing to absorb intermittent shortages and pricing spikes. Strategically, producers must budget for longer commissioning times, more conservative utilization targets in their financial models, and overlapping maintenance schedules across sites, a pattern that moderates the speed at which incremental demand can be captured and trims potential CAGR by about 0.9 percentage points over a four‑year horizon as the asset base gradually matures.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Import-dependent resin sourcing | -0.8% | India, South Asia, MENA | Medium term (2–4 years) |

| Volatile cross-regional PVC pricing | -0.6% | Asia export hubs, EU, US | Medium term (2–4 years) |

| Evolving toxics & worker safety rules | -0.7% | US, EU regulatory cores | Long term (≥ 4 years) |

| Capacity ramp-up and asset reliability | -0.9% | Asia Pacific, Middle East | Long term (≥ 4 years) |

| Logistics bottlenecks & port congestion | -0.5% | Global trade lanes, APAC–EU | Short term (≤ 2 years) |

| Specialized workforce & safety skills gap | -0.4% | Global, especially emerging Asia | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Ongoing Geopolitical Conflicts Continue to Reshape the Global Polyvinyl Chloride Supply Chain

The ongoing geopolitical conflicts, including the Russia–Ukraine war and the continuing tensions in the Middle East, are influencing the global Polyvinyl Chloride (PVC) market by affecting raw material supply, energy costs, and international trade. PVC production depends on chlorine, ethylene, and electricity, making manufacturers sensitive to disruptions in energy markets. Higher natural gas and electricity prices in parts of Europe have increased production costs, leading some producers to reduce operating rates or rely more on imports.

Freight costs and insurance premiums have also remained elevated, putting pressure on manufacturers and converters. Despite these challenges, demand from construction, water infrastructure, and electrical applications has remained relatively stable in many regions due to ongoing public infrastructure investments. Several PVC producers have responded by diversifying raw material sourcing, increasing inventory levels, and shifting exports to more stable markets to reduce supply risks.

Asia, particularly China, has continued to play an important role in balancing global supply through steady production and exports. While geopolitical uncertainty is expected to keep costs volatile in the near term, continued infrastructure spending and the expansion of water, housing, and power projects are helping the PVC market maintain stable growth prospects.

Regional Analysis

Asia-Pacific Dominates the Polyvinyl Chloride Market with a 69.14% Share, Reaching USD 75.59 Billion

In 2025, Asia-Pacific held a dominant market position, accounting for more than 69.14% of the global Polyvinyl Chloride (PVC) market, with a market value of USD 52.27 billion. The region’s leadership is supported by its large PVC production capacity, rapid urbanization, and strong demand from construction, infrastructure, electrical, automotive, and packaging industries. China remains the largest producer and consumer of PVC, while India, Japan, South Korea, and Southeast Asian countries continue to expand manufacturing and infrastructure investments.

- According to China’s National National Bureau of Statistics of China, fixed-asset investment increased by 3.7% during 2025, reflecting continued spending on infrastructure and industrial projects. In India, the Ministry of Statistics and Programme Implementation (MOSPI) in May 2025 reported that the country’s economy grew by 6.5% in FY 2024–25, supported by higher investments in construction and infrastructure.

North America is expected to register the fastest growth in the Polyvinyl Chloride (PVC) market during the forecast period. Growth is being supported by increasing investments in water infrastructure, residential construction, renewable energy projects, and modernization of electrical networks. Demand for PVC pipes, fittings, cable insulation, and building materials continues to rise as aging infrastructure is replaced and new development projects accelerate across the United States and Canada. Government funding is also creating long-term opportunities for PVC manufacturers.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global Polyvinyl Chloride (PVC) market demonstrates a moderately consolidated (oligopolistic) structure, with a limited number of large multinational manufacturers accounting for a significant share of global production, while several regional producers serve domestic and neighboring markets. Leading companies compete through capacity expansion, backward integration into chlorine and ethylene production, product innovation, and long-term supply agreements with construction, electrical, healthcare, and packaging industries.

Xinjiang Zhongtai Chemical Co., Ltd. operates one of China’s largest integrated PVC manufacturing businesses, supported by chlor-alkali production and large-scale capacity exceeding 2 million tonnes per year. INEOS Group Holdings S.A. remains a leading European producer with integrated chlorine, vinyls, and PVC operations across multiple countries and annual chemical sales exceeding EUR 60 billion. OxyChem (Occidental Petroleum) supplies North American markets through vertically integrated chlor-alkali and vinyl operations, supported by 20+ manufacturing facilities.

LG Chem Ltd. manufactures PVC for construction and industrial applications while generating more than KRW 48 trillion in annual revenue. Reliance Industries Ltd. is India’s largest PVC producer, supported by petrochemical operations that reported revenue above INR 10 trillion in FY 2025. Orbia (formerly Mexichem S.A.B. de C.V.) operates PVC and pipe businesses across 40+ countries, serving infrastructure and building markets through its Building & Infrastructure division.

The Major Players in The Industry

- Shin-Etsu Chemical Co., Ltd.

- Westlake Corporation

- Formosa Plastics Corporation

- Xinjiang Zhongtai Chemical Co., Ltd.

- INEOS Group Holdings S.A.

- OxyChem (Occidental Petroleum)

- LG Chem Ltd.

- Reliance Industries Ltd.

- Mexichem S.A.B. de C.V. (Orbia)

- Solvay S.A.

- Hanwha Solutions Corporation

- Other Key Players

Key Development

- In March 2026, Shin-Etsu Chemical Co., Ltd., through its U.S. subsidiary Shintech Inc., announced a USD 3.4 billion expansion at its integrated production site in Plaquemine, Louisiana. The project includes a second ethylene unit and a fourth chlor-alkali and vinyl chloride monomer plant, strengthening the company’s raw-material supply for PVC production.

- In January 2026, OxyChem recorded a major ownership change when Berkshire Hathaway completed its acquisition of the chemical business from Occidental Petroleum for USD 9.7 billion. The transaction placed one of North America’s top three polyvinyl chloride producers within Berkshire’s industrial manufacturing portfolio

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 75.59 Bn |

| Forecast Revenue (2035) | USD 107.83 Bn |

| CAGR (2026-2035) | 3.62% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Rigid PVC and Flexible PVC), By Application (Pipes, Profiles & Fittings, Films & Sheets, Cables & Wires, Flooring, Packaging, and Others), By Stabilizer Type (Calcium-based (Ca-Zn) Stabilizers, Lead-based Stabilizers, Organotin Stabilizers, and Others), By End Use Industry (Construction, Electrical & Electronics, Automotive, Healthcare, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Shin-Etsu Chemical Co., Ltd., Westlake Corporation, Formosa Plastics Corporation, Xinjiang Zhongtai Chemical Co., Ltd., INEOS Group Holdings S.A., OxyChem (Occidental Petroleum), LG Chem Ltd., Reliance Industries Ltd., Mexichem S.A.B. de C.V. (Orbia), Solvay S.A., Hanwha Solutions Corporation, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |