Quick Navigation

Report Overview

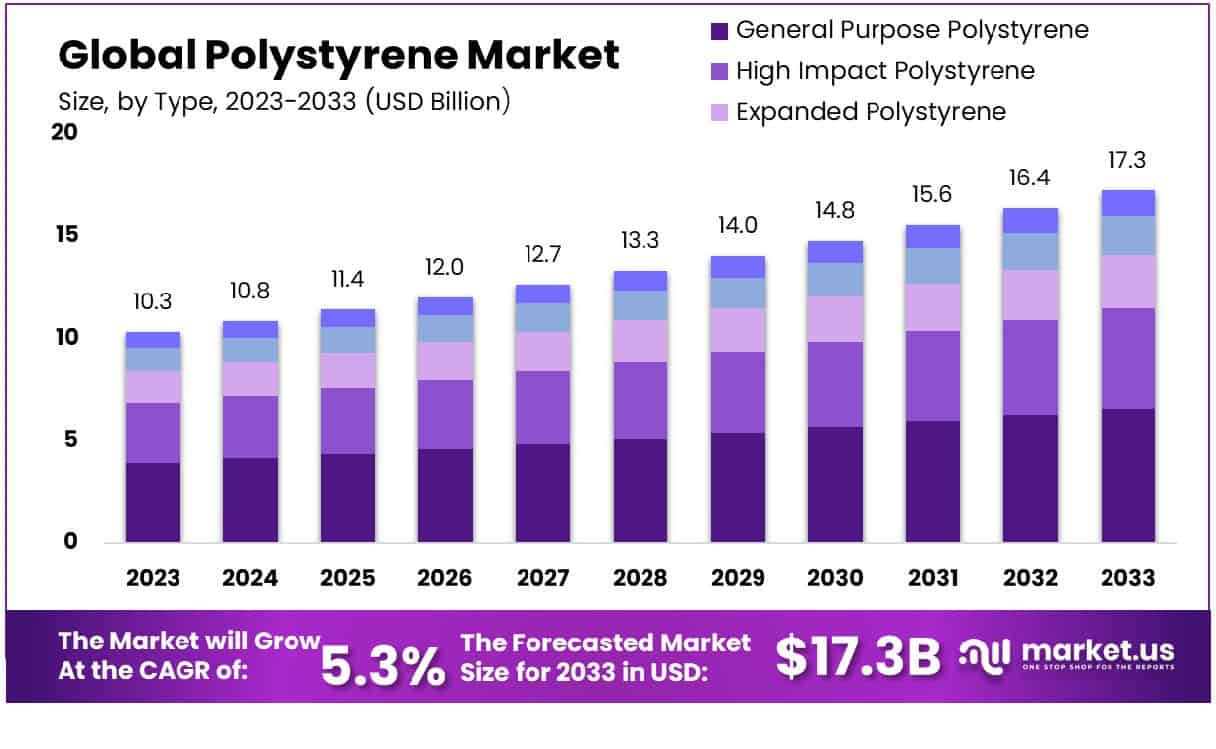

The Global Polystyrene Market size is expected to be worth around USD 17.3 Billion by 2033, From USD 10.3 Billion by 2023, growing at a CAGR of 5.3% during the forecast period from 2024 to 2033.

The Polystyrene Market encompasses the production, distribution, and application of a versatile synthetic polymer primarily utilized in consumer products, packaging, and construction materials. This market is characterized by its segments: General Purpose Polystyrene (GPPS), High Impact Polystyrene (HIPS), and Expanded Polystyrene (EPS), each catering to specific industry requirements due to their unique properties such as durability, insulation, and cost-effectiveness.

Key drivers include the demand from packaging industries and construction sectors worldwide. Market dynamics are influenced by regulatory frameworks regarding sustainability and recycling, as organizations and leaders continuously seek innovative, environmentally friendly alternatives to traditional polystyrene solutions.

The Polystyrene market is exhibiting robust growth dynamics, driven by expanding applications across various industries including packaging, construction, and consumer products. As global economies evolve, the demand for versatile and cost-effective materials such as polystyrene has intensified. Notably, in 2023, the eWASA recycling organization in South Africa achieved a commendable 31% recycling rate for polystyrene, surpassing governmental targets. This milestone not only underscores the advancements in recycling technologies but also reflects a growing environmental stewardship within the industry.

Furthermore, the global consumption of Expanded Polystyrene (EPS) has witnessed a significant uptick, escalating by over 500,000 tons from 2018 to 2022, culminating at approximately 7.2 million tonnes in the latter year. This surge is attributable to the material’s insulating properties and lightweight nature, making it indispensable in construction and packaging sectors.

The market’s trajectory suggests a sustained expansion, bolstered by innovations in product development and recycling methods. However, environmental regulations and the push towards sustainable alternatives pose challenges, urging companies to innovate and adapt in the competitive landscape. The strategic focus for stakeholders in the Polystyrene market should therefore encompass both growth and sustainability, optimizing production processes and enhancing recycling rates to align with global environmental goals.

Key Takeaways

- The Global Polystyrene Market is projected to grow from USD 10.3 billion in 2023 to USD 17.3 billion by 2033, at a CAGR of 5.3%.

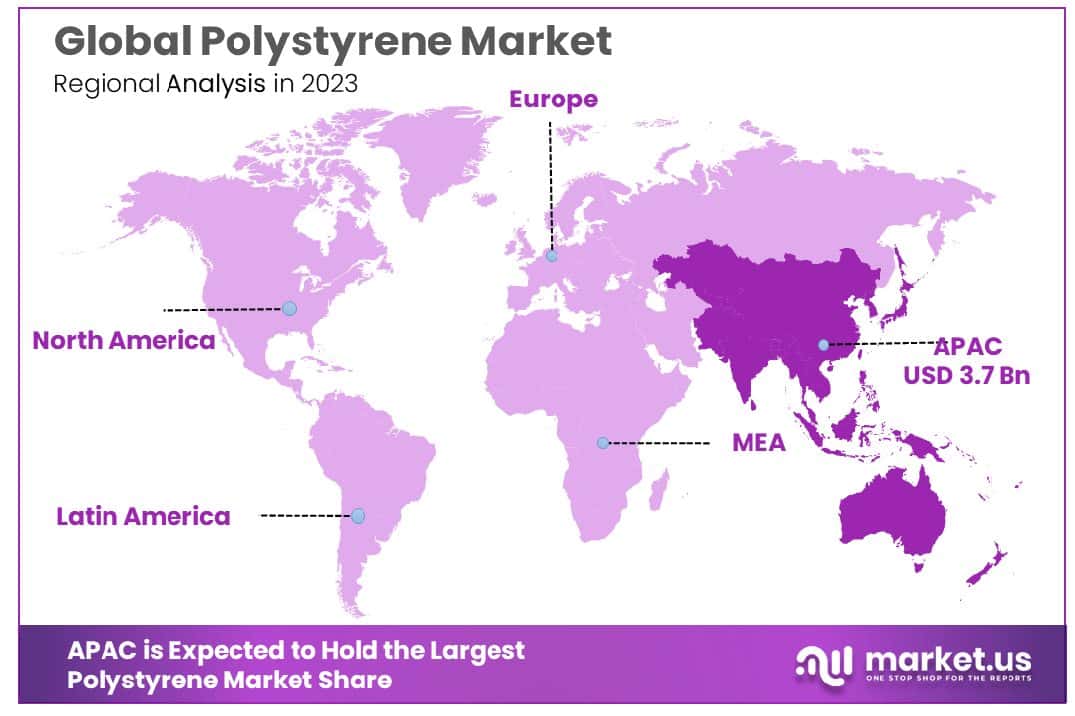

- Asia-Pacific dominates the polystyrene market with 36.5%, valued at USD 3.7 billion.

- High Impact Polystyrene holds 38.2% market share by type.

- Foams represent 33.2% of the market by form type.

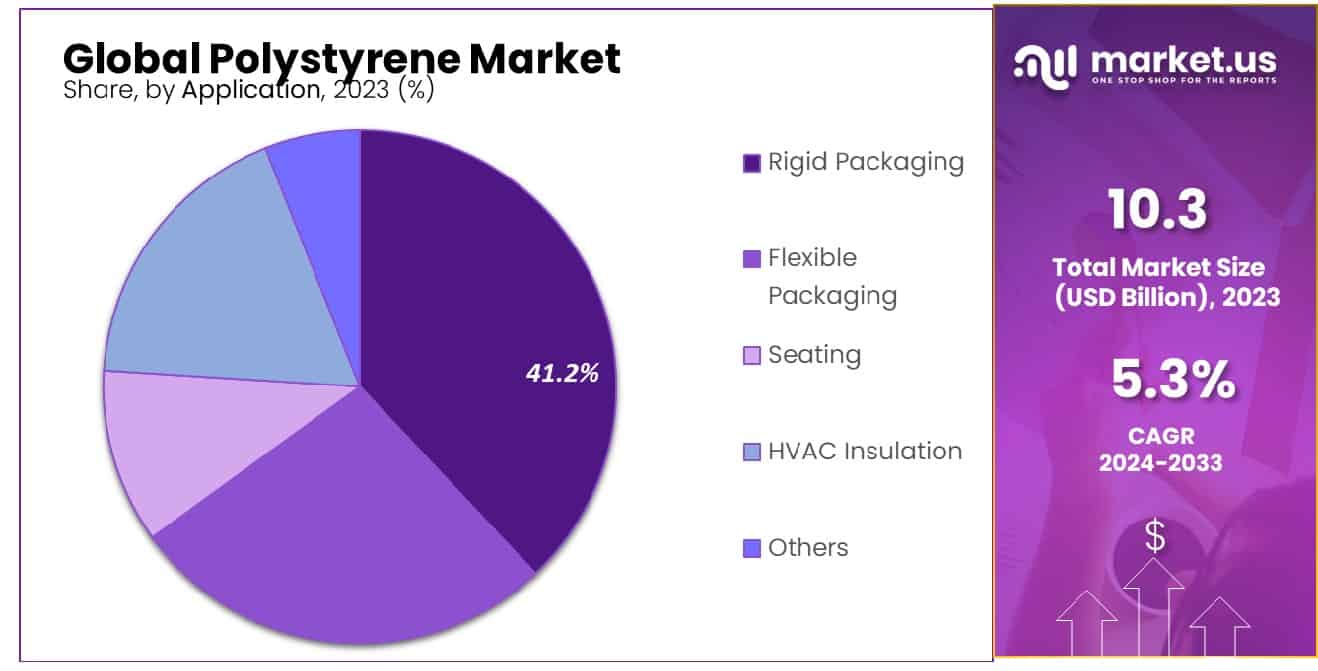

- Rigid Packaging applications lead with a 41.2% market share.

- Packaging as an end-use industry commands a 35.5% share.

Driving Factors

Increasing Demand from the Packaging Industry

The polystyrene market is experiencing substantial growth driven by the increasing demand from the packaging industry. As companies continuously seek lightweight and cost-effective materials to optimize logistics and reduce expenses, polystyrene emerges as a preferred choice. This synthetic polymer, known for its excellent rigidity and insulation properties, is integral in manufacturing various packaging solutions, including protective packaging for shipping, food-grade containers, and casing for sensitive electronics.

The use of polystyrene helps minimize transportation costs and enhances the efficiency of packaging systems, thereby driving its demand. Moreover, as the global trade and e-commerce sectors expand, the need for reliable and affordable packaging options is likely to escalate, further boosting the polystyrene market.

Expansion of the Construction Sector

The growth of the construction industry, particularly in emerging economies, is another critical factor fueling the demand for polystyrene, especially in its expanded form (EPS). EPS is favored in construction due to its lightweight nature, thermal insulation properties, and ease of installation, making it ideal for applications in insulation boards, panels, and concrete forms.

As urbanization progresses and infrastructural development initiatives increase, the demand for energy-efficient building solutions also rises. EPS’s role in reducing energy consumption for heating and cooling through better insulation correlates directly with green building trends and regulatory standards promoting energy efficiency. This alignment with sustainability goals further enhances the market potential for expanded polystyrene in the construction sector.

Rise of the Consumer Electronics Market

The burgeoning consumer electronics market significantly contributes to the growth of the polystyrene industry. Polystyrene’s properties, such as durability and lightweight nature, make it an excellent choice for manufacturing various components of consumer electronics. These include housings, structural parts, and insulation for items like televisions, computers, and household appliances.

As the global demand for consumer electronics continues to surge, driven by technological advancements and increasing consumer spending power, the need for materials that can provide protection, thermal management, and cost-efficiency in manufacturing processes grows. This trend not only supports the polystyrene market growth but also encourages innovations within the sector to meet the evolving requirements of the electronics industry.

Restraining Factors

Environmental Regulations and Concerns Over Polystyrene Waste

The growth of the polystyrene market faces significant constraints due to environmental regulations and increasing public scrutiny over the sustainability of materials. Polystyrene, particularly in its disposable forms, is notorious for its low biodegradability and substantial contribution to global plastic waste. Regulatory bodies worldwide have been imposing stricter controls on the use of non-biodegradable plastics, including polystyrene, in an effort to mitigate environmental damage.

Such regulations can lead to reductions in polystyrene demand, particularly in regions with aggressive waste reduction targets and bans on certain types of plastic products. Furthermore, the consumer shift towards more sustainable alternatives is prompting manufacturers to explore and invest in eco-friendly materials, potentially diverting market share from traditional polystyrene products. This environmental pushback is a pivotal factor that could temper market growth, necessitating innovation and adaptation within the industry.

Volatility in Raw Material Prices

Another key challenge affecting the polystyrene market is the volatility in raw material prices. Polystyrene production heavily depends on styrene, a derivative of benzene and ethylene, whose prices are subject to fluctuations in the global oil market. This volatility can significantly impact production costs, making budgeting and pricing strategies more complex for manufacturers.

High variability in styrene prices can lead to reduced profit margins or increased product prices, potentially decreasing polystyrene’s competitiveness against alternative materials. Such economic pressures may inhibit the growth of the polystyrene market, particularly during periods of economic downturn or when lower-cost substitutes are available.

By Type Analysis

High Impact Polystyrene accounts for 38.2% of the market by type due to its durability.

In 2023, Impact Polystyrene held a dominant market position in the “By Type” segment of the Polystyrene Market, capturing more than a 38.2% share. This category was followed by General Purpose Polystyrene, Expanded Polystyrene, Extruded Polystyrene, and Others in terms of market penetration and revenue.

Impact Polystyrene, or High Impact Polystyrene (HIPS), is extensively utilized for its robustness and impact resistance, qualities that are indispensable in products requiring durability under stress, such as appliance housings, toys, and automotive parts. The resilience and easy processing of HIPS have driven its adoption across various manufacturing sectors, underpinning its market leadership.

General Purpose Polystyrene (GPPS) is known for its clarity and rigidity, making it ideal for applications requiring visual appeal and precision, such as laboratory ware and food packaging. Despite its broad utility, it ranks just below HIPS due to its lower impact resistance.

Expanded Polystyrene (EPS) follows closely, favored in packaging and building industries for its lightweight and insulative properties. It is particularly prevalent in the construction sector for thermal insulation systems and in packaging for protective padding.

Extruded Polystyrene (XPS) is another key segment, utilized mainly in building applications for insulation due to its moisture resistance and thermal properties. XPS provides significant energy efficiency benefits, which sustain its demand for green building initiatives.

By Form Type Analysis

Foams represent 33.2% of the market by form type, popular for insulation and packaging.

In 2023, Foams held a dominant market position in the “By Form Type” segment of the Polystyrene Market, capturing more than a 33.2% share. This segment was followed by Films and Sheets, Injection Molding, and Others in terms of market share and utilization.

Foams, particularly expanded polystyrene (EPS) and extruded polystyrene (XPS), are highly valued for their lightweight, insulating properties, and structural strength. The extensive use of polystyrene foams in packaging, construction, and insulation applications drives this segment. The construction industry’s growing emphasis on thermal insulation and energy efficiency has particularly bolstered the demand for polystyrene foam products.

Films and Sheets constitute the next significant segment. These products are essential in the packaging industry, offering versatile solutions for food packaging, medical packaging, and industrial applications. The ability of polystyrene films and sheets to be customized to specific barrier properties enhances their appeal across various sectors.

Injection Molding, another crucial form type, utilizes polystyrene for creating complex and high-volume products such as consumer electronics, household goods, and automotive components. The segment benefits from polystyrene’s excellent moldability and aesthetic finish, making it a preferred choice for manufacturers seeking cost-effective, high-performance materials.

The “Others” category comprises a diverse range of applications, including extrusion and blow molding, showcasing polystyrene’s versatility. This segment captures niche markets where the unique properties of polystyrene can be tailored to meet specific industrial needs.

By Application Analysis

Rigid packaging leads application segments, comprising 41.2% of the market, essential for transport safety.

In 2023, Rigid Packaging held a dominant market position in the “By Application” segment of the Polystyrene Market, capturing more than a 41.2% share. This was followed by Flexible Packaging, Seating, HVAC Insulation, and Others in terms of their respective market contributions.

The predominance of Rigid Packaging is primarily driven by its critical role in protecting and preserving a wide array of consumer products, from food items to electronics. Polystyrene’s properties such as moisture resistance, strength, and affordability contribute significantly to its preferred use in this sector. The ongoing innovations in food safety and consumer packaging standards have further cemented its substantial market share.

Following Rigid Packaging, Flexible Packaging holds a significant portion of the market. This segment benefits from polystyrene’s versatility and lightweight nature, making it ideal for reducing shipping costs and enhancing product shelf life, particularly in perishable goods.

Seating applications, incorporating polystyrene for its cushioning and comfort properties, represent another important application area. The automotive and furniture industries, where comfort combined with durability is paramount, extensively utilize polystyrene.

HVAC Insulation is another key area, with polystyrene being employed due to its excellent insulation properties, contributing to energy efficiency in building designs. This segment’s growth is supported by increasing regulations on energy savings and environmental sustainability.

The “Others” category encapsulates a range of niche applications where polystyrene’s unique attributes, such as structural strength and thermal resistance, are leveraged, highlighting the material’s adaptability across various industrial applications.

By End-Use Analysis

The packaging industry is the largest end-use sector, holding 35.5% of the market share.

In 2023, Industry Packaging held a dominant market position in the “By End-Use” segment of the Polystyrene Market, capturing more than a 35.5% share. This segment was followed by Electronics, Building & Construction, Consumer Goods & Appliances, and Others in terms of market share and revenue generation.

The substantial share of the Packaging sector can be attributed to the extensive application of polystyrene in food and beverage packaging, owing to its lightweight, cost-effective, and insulation properties. The rise in consumer demand for packaged foods and the shift towards convenient packaging solutions has significantly driven the growth of polystyrene usage in this industry.

Electronics emerged as the second-largest segment, with polystyrene being utilized primarily for protective housing and components in consumer electronics. The material’s properties such as rigidity and shock absorption make it ideal for safeguarding delicate electronic components.

The Building & Construction segment also showed notable growth, driven by the increasing use of polystyrene as an insulation material in residential and commercial construction buildings. The energy efficiency requirements and green building standards have further bolstered the demand for polystyrene in this segment.

Consumer Goods & Appliances, although smaller in comparison, leveraged polystyrene for its versatility and aesthetic qualities, particularly in household items and appliances where durability and longevity are paramount.

The “Others” category, which includes various niche applications, maintained a steady market presence, showcasing the adaptability of polystyrene across diverse industries. This segment’s performance is closely tied to innovations and the development of new applications that exploit the unique characteristics of polystyrene.

Key Market Segments

By Type

- General Purpose Polystyrene

- High Impact Polystyrene

- Expanded Polystyrene

- Extruded Polystyrene

- Others

By Form Type

- Foams

- Films, and Sheets

- Injection Molding

- Others

By Application

- Rigid Packaging

- Flexible Packaging

- Seating

- HVAC Insulation

- Others

By End-Use Industry

- Packaging

- Electronics

- Building & Construction

- Consumer Goods & Appliances

- Others

Growth Opportunities

Development of Recyclable and Eco-Friendly Polystyrene Products

In 2023, the polystyrene market has a significant growth opportunity in the development of recyclable and eco-friendly products. As environmental concerns and regulatory pressures intensify, the demand for sustainable materials is escalating. Innovations in polystyrene recycling technologies and the production of bio-based polystyrene are pivotal. These advancements can potentially transform polystyrene’s market image from an environmental liability to a more sustainable option, aligning with global sustainability goals.

Such innovations not only cater to the eco-conscious consumer base but also open new applications in industries actively seeking greener alternatives. Companies investing in these technologies are likely to gain competitive advantages, securing a foothold in markets with stringent environmental regulations and high consumer awareness.

Expansion into Emerging Markets

Emerging markets present another lucrative avenue for polystyrene growth in 2023. As urbanization continues to accelerate and industrial activities expand in these regions, the demand for polystyrene in construction, packaging, and consumer goods is expected to rise. These markets often have less stringent environmental regulations, providing an initial entry point with traditional polystyrene products.

However, the long-term strategy should also include sustainable solutions to preempt future regulatory changes and shifting consumer preferences. Establishing production facilities and distribution networks in these regions can reduce logistics costs and improve market responsiveness, facilitating deeper market penetration and enhanced growth prospects in untapped markets.

Latest Trends

Adoption of High Impact Polystyrene (HIPS) for Improved Product Durability

In 2023, one of the prominent trends in the global polystyrene market is the increased adoption of High Impact Polystyrene (HIPS). Recognized for its enhanced durability and toughness, HIPS is becoming a preferred material in various manufacturing sectors, including automotive, electronics, and consumer products. This shift is driven by the need for materials that offer better performance and longer lifespan while maintaining cost efficiency.

HIPS’s ability to absorb impacts without cracking or breaking under stress makes it ideal for producing durable goods, from automotive parts to robust packaging solutions. The growing preference for HIPS underscores a market trend towards materials that not only meet functional requirements but also extend the lifecycle of end products, thereby reducing waste and enhancing consumer satisfaction.

Increasing Use of Polystyrene in 3D Printing Applications

Another significant trend is the increasing use of polystyrene in 3D printing applications. As 3D printing technology evolves, its integration into mainstream manufacturing and prototyping processes continues to expand. Polystyrene is particularly advantageous in this field due to its ease of processing and fine-detail rendering capabilities.

Its application in 3D printing opens up new avenues for customized manufacturing, rapid prototyping, and complex part production. As industries seek more versatile and cost-effective solutions for on-demand manufacturing, polystyrene’s role within the 3D printing realm is expected to grow, further diversifying its uses and enhancing its market reach.

Regional Analysis

The Asia-Pacific polystyrene market dominates with a 36.5% share, valued at USD 3.7 billion.

Asia-Pacific emerges as the dominant region in the polystyrene market, accounting for approximately 36.5% of the market share, valued at USD 3.7 billion. This region’s leadership is driven by rapid industrialization, expanding manufacturing sectors, and significant investments in infrastructure development, particularly in China, India, and Southeast Asia. The high demand in packaging, electronics, and construction sectors supports the robust market size and growth trajectory in this region.

North America, led by the United States, maintains a steady growth pattern, supported by advanced manufacturing techniques and a resurgence in domestic production capabilities. The region focuses on innovative polystyrene applications such as in insulation products for energy-efficient buildings and lightweight materials for automotive parts, aligning with stricter environmental regulations and sustainability trends.

Europe witnesses moderate growth, heavily influenced by stringent environmental policies that curb the use of traditional polystyrene products. European market players are pivoting towards recyclable and bio-based polystyrene solutions to comply with EU directives on single-use plastics and circular economy models, which stimulate R&D and eco-friendly product offerings.

Middle East & Africa and Latin America are experiencing gradual growth. These regions benefit from increasing urbanization and a rising middle class, which boost demand for consumer goods and packaging made from polystyrene. However, market expansion is somewhat restrained by less-developed recycling infrastructures and fluctuating economic conditions.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

Key Players Analysis

In 2023, the global polystyrene market is defined by strategic initiatives from key players aiming to enhance market position and adapt to evolving industry demands. Companies like Total, Trinseo, and Versalis SpA are leveraging their capacities to innovate and meet the growing demand for sustainable and high-performance polystyrene products. Total and Trinseo, in particular, are making significant strides in developing recycling technologies and introducing renewable polystyrene to cater to the sustainability trend.

Alpek S.A.B. de CV and INEOS Styrolution Group GmbH are expanding their market reach by enhancing their production capabilities and forming strategic partnerships to ensure a stable supply chain and access to emerging markets. Their focus remains on optimizing manufacturing processes and exploring new applications in sectors such as 3D printing and high-performance consumer goods.

BASF SE and LG Chem continue to focus on R&D to push the boundaries of polystyrene’s applications, particularly in advanced electronics and automotive parts. Their efforts are crucial in positioning polystyrene as a key material in high-growth industries.

Americas Styrenics LLC (AmSty) and CHIMEI are strengthening their market presence by focusing on niche markets where polystyrene’s unique properties, like clarity and ease of use in manufacturing, are highly valued.

Lastly, companies like KUMHO PETROCHEMICAL and SABIC are actively investing in global expansion strategies to exploit untapped markets, especially in Asia and Africa, where industrial and urban development is driving demand.

These key players are not just responding to current market conditions but are also shaping the future landscape of the polystyrene industry through strategic innovations, sustainability efforts, and global expansion.

Market Key Players

- Atlas Molded Products

- Alpek S.A.B. de CV

- Total

- Trinseo

- Versalis SpA

- Americas Styrenics LLC (AmSty)

- BASF SE

- CHIMEI

- INEOS Styrolution Group GmbH

- Innova

- Formosa Chemicals & Fibre Corp.

- INEOS Styrolution Group GmbH

- KUMHO PETROCHEMICAL

- LG Chem

- SABIC

- Synthos

Recent Development

- In 2024, Versalis is investing approximately €80 million in its Ravenna site to expand the production of high-added-value elastomers, indicating a focus on enhancing its production capabilities and specializing its portfolio towards sustainable mobility products

- In December 2023, Alpek S.A.B. de C.V. reported a 10.13% increase in its share price. However, specific revenue growth percentages for recent years are not directly provided in the latest data.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 10.3 Billion |

| Forecast Revenue (2033) | USD 17.3 Billion |

| CAGR (2024-2033) | 5.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type(General Purpose Polystyrene, High Impact Polystyrene, Expanded Polystyrene, Extruded Polystyrene, Others), By Form Type(Foams, Films, and Sheets, Injection Molding, Others), By Application(Rigid Packaging, Flexible Packaging, Seating, HVAC Insulation, Others), By End-Use Industry(Packaging, Electronics, Building & Construction, Consumer Goods & Appliances, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Atlas Molded Products, Alpek S.A.B. de CV, Total, Trinseo, Versalis SpA, Americas Styrenics LLC (AmSty), BASF SE, CHIMEI, INEOS Styrolution Group GmbH, Innova, Formosa Chemicals & Fibre Corp., INEOS Styrolution Group GmbH, Innova, KUMHO PETROCHEMICAL, LG Chem, SABIC, Synthos |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The Global Polystyrene Market Size is USD 10.3 Billion in 2023.

The Global Polystyrene Market is expected to grow at a CAGR of 5.3% (2024-2033).

Market.US has segmented the Global Polystyrene Market by geographic (North America, Europe, APAC, South America, and Middle East and Africa). By Type(General Purpose Polystyrene, High Impact Polystyrene, Expanded Polystyrene, Extruded Polystyrene, Others), By Form Type(Foams, Films, and Sheets, Injection Molding, Others), By Application(Rigid Packaging, Flexible Packaging, Seating, HVAC Insulation, Others), By End-Use Industry(Packaging, Electronics, Building & Construction, Consumer Goods & Appliances, Others)

The China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Rest of APAC are leading key areas of operation for Global Polystyrene Market.

Atlas Molded Products, Alpek S.A.B. de CV, Total, Trinseo, Versalis SpA , Americas Styrenics LLC (AmSty), BASF SE, CHIMEI, INEOS Styrolution Group GmbH, Innova, Formosa Chemicals & Fibre Corp., INEOS Styrolution Group GmbH,KUMHO PETROCHEMICAL, LG Chem, SABIC, Synthos, Total, Trinseo, Versalis SpA