Quick Navigation

Report Overview

The Global Pentane Plus Market size is expected to be worth around USD 219.3 Million by 2033, From USD 132.1 Million by 2023, growing at a CAGR of 5.2% during the forecast period from 2024 to 2033.

The Pentane Plus Market encompasses the global trade and utilization of a hydrocarbon mixture primarily composed of pentane and heavier hydrocarbons. This market is integral to the petrochemical industry, serving as a key raw material for the production of high-octane gasoline, petrochemical feedstocks, and various industrial solvents.

The demand for Pentane Plus is driven by its application in oil refineries, natural gas processing, and its role in enhancing gasoline performance. Market growth is influenced by factors such as increasing energy demands, advancements in extraction technologies, and fluctuations in crude oil prices.

The Pentane Plus market is witnessing notable growth, driven by increased natural gas production and consumption, especially in the United States. In 2023, the U.S. set new records for natural gas consumption, reaching 89.1 billion cubic feet per day (Bcf/d), reflecting a 4% average annual increase since 2018.

This surge is largely attributed to the electric power sector, which experienced a 7% rise in consumption, reaching 35.4 Bcf/d. The robust demand for natural gas in power generation underscores the importance of Pentane Plus, a key component in the natural gas liquids (NGL) stream, used extensively in gasoline blending and as a petrochemical feedstock.

Despite the overall growth, the residential and commercial sectors in the U.S. saw declines in natural gas consumption by 10% and 6% respectively, indicating a shift in usage patterns that could impact the Pentane Plus market. However, these declines are offset by the continued expansion in industrial applications and power generation.

Globally, natural gas production has remained stable with significant increases in North America, the Middle East, China, and Australia, compensating for the declines in Russia. The European Union’s natural gas demand has notably decreased, with a 13% drop in 2022 and a further 7.4% decline in 2023, reflecting a shift towards alternative energy sources and increased energy efficiency measures.

Given these dynamics, the Pentane Plus market is expected to benefit from the growing industrial and power generation demands, particularly in regions with stable or increasing natural gas production. Market participants should focus on leveraging these trends to capture growth opportunities in the evolving energy landscape, while also being mindful of the regional consumption shifts and their potential impacts on demand.

Key Takeaways

- Market Growth: The Global Pentane Plus Market size is expected to be worth around USD 219.3 Million by 2033, From USD 132.1 Million by 2023, growing at a CAGR of 5.2% during the forecast period from 2024 to 2033.

- Regional Dominance: The Pentane Plus Market in North America accounts for 48.6%, valued at USD 64.2 million.

- Segmentation Insights:

- By Product Type: N-Pentane accounts for 45.8% of the market share.

- By Application: N-Pentane is primarily used as a blowing agent.

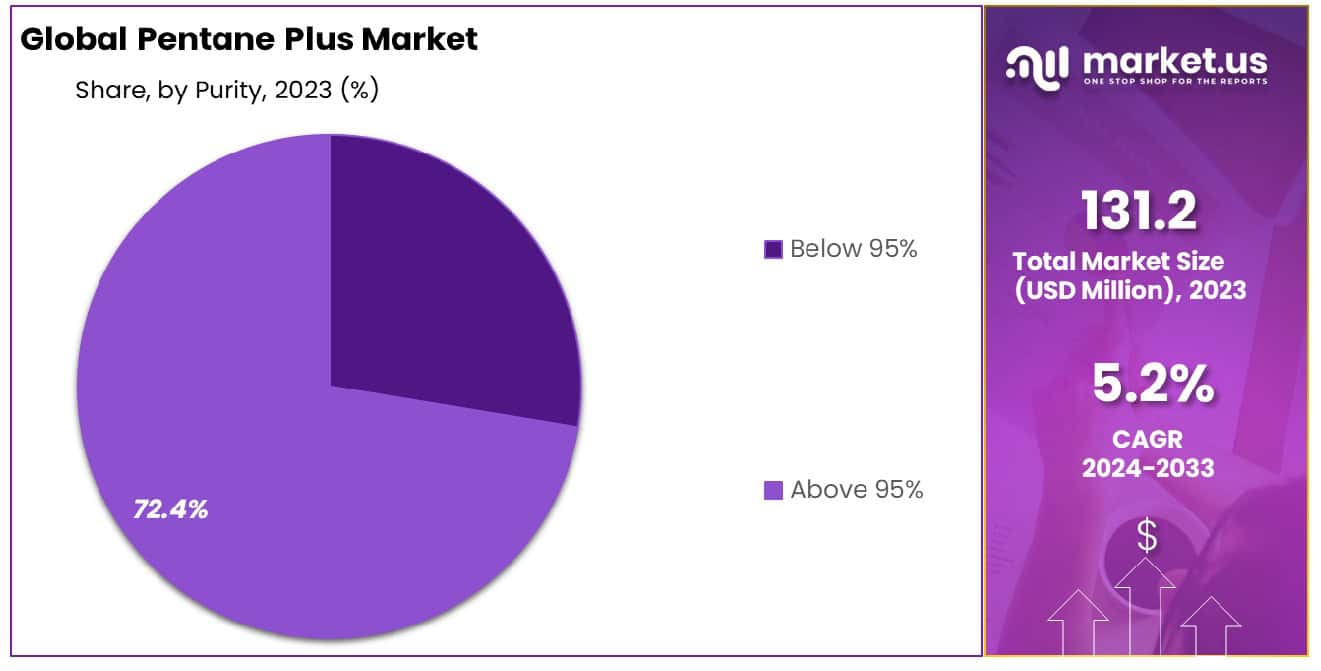

- By Purity: N-Pentane with above 95% purity represents 72.4% of the market.

- Growth Opportunities: In 2023, the global Pentane Plus market saw growth due to new chemical applications and expansion in emerging markets, driven by industrial growth, urbanization, and demand for eco-friendly products.

Driving Factors

Increasing Demand for Natural Gas Liquids (NGLs)

The rising demand for natural gas liquids (NGLs) significantly propels the growth of the Pentane Plus Market. NGLs, including ethane, propane, butane, and pentane, are crucial feedstocks in petrochemical production and are essential for various industrial applications. The global market has seen an upswing due to the versatile use of NGLs in producing high-value chemicals, plastics, and synthetic materials.

This surge is primarily driven by the increasing global consumption of petrochemical products and the expansion of the shale gas industry, particularly in North America. As pentane plus is a component of NGLs, its market benefits from this overall rising demand, leading to enhanced production capacities and investments in related infrastructure.

Expansion of the Petrochemical Industry

The expansion of the petrochemical industry acts as a cornerstone for the growth of the Pentane Plus Market. The petrochemical sector, which converts raw materials like NGLs into essential chemicals, fuels, and industrial products, is experiencing robust growth. This expansion is driven by rising demand for consumer goods, automotive components, and construction materials.

Pentane plus, as a vital feedstock in petrochemical processes, finds extensive applications in the production of ethylene, propylene, and other critical chemicals. The increased production capacities in the petrochemical industry necessitate a higher supply of pentane, thereby fueling market growth.

Rising Energy Consumption Globally

The global increase in energy consumption is a pivotal factor driving the growth of the Pentane Plus Market. As economies expand and industrialization progresses, the demand for energy-intensive processes and products escalates. This rise is particularly evident in emerging economies where rapid industrialization and urbanization are prevalent.

Pentane Plus is utilized in various energy-related applications, including enhanced oil recovery (EOR) and as a solvent in natural gas processing. The surge in energy consumption, coupled with the need for efficient and high-yield extraction methods, bolsters the demand for pentane plus, driving its market expansion.

Restraining Factors

Volatility in Crude Oil Prices

Volatility in crude oil prices is a significant restraining factor impacting the growth of the Pentane Plus Market. The pricing of pentane plus is closely tied to the fluctuations in crude oil prices, given that pentane plus is a byproduct of crude oil refining. Sharp changes in crude oil prices can lead to uncertainty in the cost structure and profitability of pentane plus production.

For instance, the crude oil price dropped drastically in 2020 due to reduced demand amid the COVID-19 pandemic, causing significant disruptions in the supply chain and pricing of petrochemical products. Such volatility can deter investments in pentane plus production facilities and can lead to instability in market operations. Companies may find it challenging to plan long-term strategies and investments under such uncertain conditions, thereby restraining market growth.

Environmental Concerns and Regulatory Challenges

Environmental concerns and regulatory challenges present another substantial restraint on the growth of the Pentane Plus Market. The production and use of pentane plus, like other hydrocarbons, contribute to smart greenhouse gas emissions and environmental pollution. As global awareness and concern about climate change rise, regulatory bodies are imposing stricter environmental regulations and emission standards.

For example, the European Union’s stringent regulations on volatile organic compounds (VOCs) emissions can significantly affect the operations of companies involved in the production and use of pentane plus. Compliance with such regulations often requires significant investments in cleaner technologies and processes, which can increase operational costs.

Additionally, potential regulatory changes can create uncertainty in the market, as companies must continuously adapt to evolving standards. These environmental and regulatory pressures can limit the expansion capabilities of companies, restraining market growth.

By Product Type Analysis

N-Pentane holds a 45.8% market share due to its versatile applications and efficiency in various industries.

In 2023, N-Pentane held a dominant market position in the By Product Type segment of the Pentane Plus Market, capturing more than a 45.8% share. The market was segmented into N-Pentane, Isopentane, and Neopentane, with N-Pentane emerging as the leading product type due to its extensive use in the polymer and chemical industries.

N-Pentane, a highly volatile hydrocarbon, is widely utilized as a blowing agent in the production of polystyrene and polyurethane foams. Its low boiling point and excellent solvency properties make it an ideal choice for applications requiring quick evaporation and high purity. The rising demand for lightweight and energy-efficient insulation materials in the construction and refrigeration industries has significantly bolstered the consumption of N-Pentane. Furthermore, its use as a solvent in chemical synthesis and in the extraction of essential oils has contributed to its market dominance.

Isopentane, while also gaining traction, held a smaller market share compared to N-Pentane. Its application as a refrigerant and blowing agent in the production of expandable polystyrene foam has driven its demand. However, the relatively higher cost and lower availability of Isopentane compared to N-Pentane have restrained its market growth.

Neopentane, the least prominent segment, accounted for the smallest share of the market. Despite its superior chemical stability and lower reactivity, the limited application scope and higher production costs have confined its use to niche markets, such as specialty chemicals and advanced materials.

The robust growth in the construction and automotive sectors, along with increasing environmental regulations promoting the use of eco-friendly blowing agents, is expected to further enhance the market share of N-Pentane in the coming years. Additionally, ongoing advancements in chemical synthesis processes and the expanding application of pentanes in various industrial sectors are projected to drive the overall growth of the Pentane Plus Market.

By Application Analysis

Blowing Agent usage is significant, contributing to market demand for N-Pentane in the manufacturing and insulation sectors.

In 2023, the Blowing Agent held a dominant market position in the By Application segment of the Pentane Plus Market. This segment, which also includes Solvent, Fuel Additive, Chemical Intermediates, and Others, captured a significant market share due to its extensive use in various industrial applications.

The Blowing Agent segment’s dominance can be attributed to its critical role in the production of foam products, particularly polystyrene and polyurethane foams. These foams are essential for insulation in the construction and refrigeration industries, where energy efficiency and lightweight materials are paramount. The increasing demand for energy-efficient buildings and refrigeration systems has driven the consumption of pentane-based blowing agents, solidifying their market leadership.

The Solvent segment also holds a substantial market share, primarily due to pentane’s excellent solvency properties and low toxicity. It is widely used in the pharmaceutical industry for drug formulation and in laboratories for chemical synthesis and extractions. The demand for high-purity solvents in these sectors has contributed to the steady growth of this segment.

Fuel Additive, another significant application segment, utilizes pentane to enhance the performance and efficiency of gasoline. Its ability to increase octane ratings and reduce knocking in engines has made it a valuable additive in the automotive industry. However, this segment holds a smaller share compared to blowing agents and solvents.

The Chemical Intermediate segment involves pentane’s use in the synthesis of various chemicals and polymers. Its application in producing high-value chemicals and materials for industrial processes has supported its market presence, though it remains less dominant than the primary segments.

Lastly, the Others category encompasses miscellaneous applications such as laboratory reagents and cleaning agents. While important, this segment captures the smallest share due to its limited application scope.

The growing construction and automotive industries, coupled with advancements in chemical synthesis, are expected to further drive the demand for pentane-based blowing agents. The emphasis on energy efficiency and environmental sustainability will likely enhance the market position of this segment in the coming years, supporting the overall growth of the Pentane Plus Market.

By Purity Analysis

Purity above 95% captures 72.4% of the market, ensuring high-quality standards and performance in end products.

In 2023, the “Above 95%” purity segment held a dominant market position in the By Purity segment of the Pentane Plus Market, capturing more than a 72.4% share. The market was segmented into “Below 95%” and “Above 95%”, with the latter emerging as the leading category due to its extensive application in high-purity demanding industries.

The “Above 95%” purity segment includes pentane products with purity levels exceeding 95%, which are essential for applications requiring high chemical stability and minimal impurities. This segment’s dominance is primarily driven by its significant use in the production of polystyrene and polyurethane foams, where high-purity pentane is crucial for achieving optimal product performance and consistency. The construction and refrigeration industries, which rely heavily on these foams for insulation purposes, have contributed to the increasing demand for high-purity pentane.

Moreover, the “Above 95%” purity pentane is preferred in the pharmaceutical and laboratory sectors due to its superior solvent properties and low toxicity, ensuring precise and safe chemical reactions and extractions. The growing focus on energy efficiency and environmental sustainability has further propelled the adoption of high-purity pentane as a more eco-friendly blowing agent compared to traditional chlorofluorocarbons (CFCs).

On the other hand, the “Below 95%” purity segment, while still significant, accounted for a smaller market share. This category is typically utilized in applications where ultra-high purity is not as critical, such as in general cleaning solvents and certain industrial processes. However, the lower performance efficiency and potential for higher impurities have limited its broader adoption.

The increasing demand for high-performance materials, stringent environmental regulations, and technological advancements in the chemical industry are expected to further enhance the market share of the “Above 95%” purity segment in the coming years. Additionally, the expanding application of high-purity pentane in various emerging sectors is projected to drive the overall growth of the Pentane Plus Market.

Key Market Segments

By Product Type

- N-Pentane

- Isopentane

- Neopentane

By Application

- Blowing Agent

- Solvent

- Fuel Additive

- Chemical Intermediate

- Others

By Purity

- Below 95%

- Above 95%

Growth Opportunities

Development of New Applications in Chemical Industries

The global Pentane Plus market has witnessed significant growth opportunities in 2023, driven largely by the development of new applications within chemical industries. Pentane Plus, a blend of hydrocarbons, is primarily used as a blowing agent in the production of polystyrene foam. However, recent advancements have expanded its utility into other chemical applications such as solvents, and refrigerants, and as an intermediate in the synthesis of various chemicals.

The increased focus on environmentally friendly and energy-efficient products has bolstered the demand for Pentane Plus, particularly in sectors aiming to reduce greenhouse gas emissions. Innovations in chemical processing technologies have enabled the efficient use of Pentane Plus, enhancing its appeal in the global market. Additionally, stringent regulations on alternative chemicals have propelled industries to adopt Pentane Plus, further driving its market growth.

Expansion in Emerging Markets

The expansion into emerging markets has been a pivotal factor in the growth of the Pentane Plus market in 2023. Countries in the Asia-Pacific region, including China, India, and Southeast Asian nations, have exhibited robust industrial growth, leading to a surge in demand for Pentane Plus. The burgeoning construction and automotive industries in these regions have significantly contributed to the increased consumption of polystyrene foam, where Pentane Plus is a key component.

Moreover, the favorable economic conditions and governmental policies promoting industrialization and infrastructural development have provided a conducive environment for the market’s expansion. The rising disposable incomes and urbanization in these emerging markets have also fueled the demand for consumer goods and appliances, further driving the market for Pentane Plus. Consequently, these factors collectively underscore the substantial growth opportunities present in the global Pentane Plus market.

Latest Trends

Adoption of Advanced Extraction Technologies

The global Pentane Plus market in 2023 is experiencing significant trends, notably the adoption of advanced extraction technologies. These innovations have revolutionized the efficiency and cost-effectiveness of extracting Pentane Plus from natural gas and crude oil. Techniques such as cryogenic distillation and advanced separation methods have enhanced the purity and yield of Pentane Plus, making it more attractive for industrial applications.

These technologies also contribute to reducing environmental impact by minimizing waste and energy consumption during the extraction process. Companies are increasingly investing in state-of-the-art extraction facilities to stay competitive and meet the growing demand for high-purity Pentane Plus.

The push towards sustainable practices in the petrochemical industry further accelerates the adoption of these technologies, aligning with global environmental regulations and standards. This trend is expected to continue as technological advancements progress, offering substantial benefits in terms of operational efficiency and environmental sustainability.

Increasing Investments in Infrastructure Development

Another prominent trend in the global Pentane Plus market in 2023 is the increasing investments in infrastructure development. This includes the expansion of production facilities, storage capacities, and distribution networks to meet the rising demand for Pentane Plus in various regions.

Governments and private sector players are channeling significant funds into upgrading and expanding infrastructure to support the burgeoning petrochemical industry. In emerging markets, particularly in Asia-Pacific and Latin America, infrastructure development is pivotal in boosting the local supply chain and enhancing market accessibility.

These investments not only improve the availability of Pentane Plus but also stabilize its pricing by reducing supply chain bottlenecks. The focus on robust infrastructure ensures a reliable supply of Pentane Plus, catering to the growing needs of industries such as construction, automotive, and consumer goods. As a result, this trend plays a critical role in the sustained growth and stability of the Pentane Plus market globally.

Regional Analysis

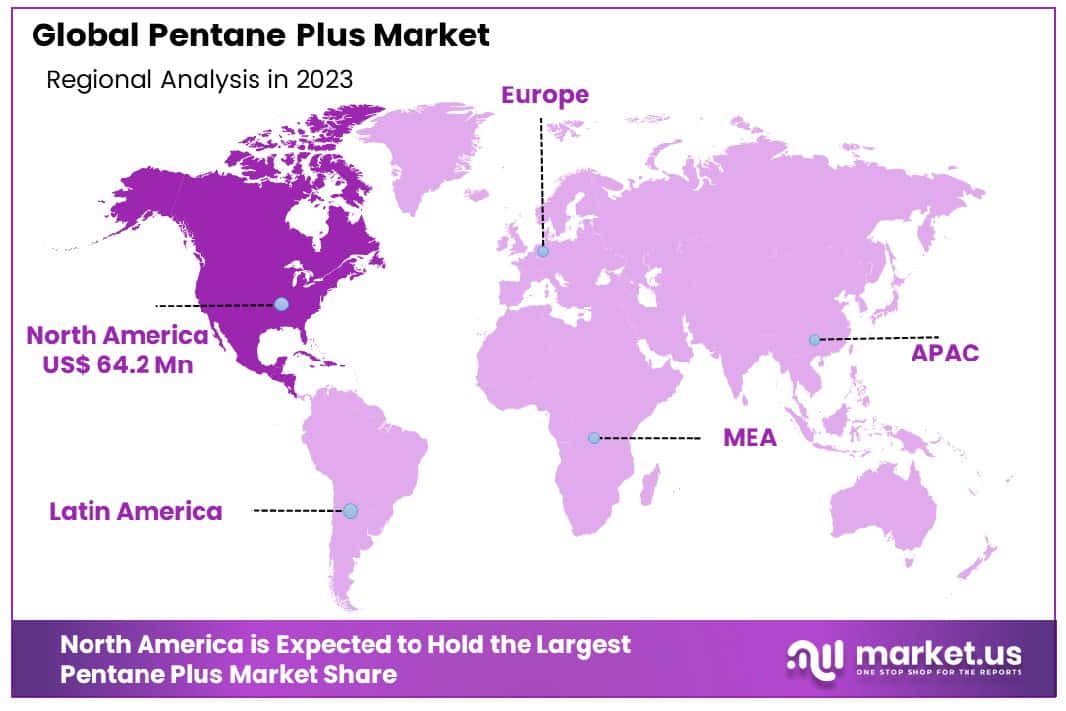

In North America, the Pentane Plus market accounts for 48.6%, valued at USD 64.2 million.

The Pentane Plus market demonstrates significant regional variations in demand and application, driven by the diverse industrial landscapes across North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

In North America, which dominates the global market with a substantial 48.6% share valued at USD 64.2 million, the robust petrochemical and energy sectors drive the demand for Pentane Plus. This region benefits from extensive shale gas production and a well-established infrastructure, fostering continuous growth.

Europe follows with its focus on sustainable and efficient chemical processes. Countries like Germany and the Netherlands are key players, leveraging advanced technologies in petrochemical manufacturing. The market in Europe is driven by stringent environmental regulations, pushing for the use of Pentane Plus as a cleaner alternative in various applications.

The Asia Pacific region is experiencing rapid growth, supported by expanding industrial activities in China, India, and Southeast Asia. The booming construction and automotive industries, coupled with increasing urbanization, are significant factors contributing to the rising demand. Additionally, investments in chemical manufacturing and a shift towards alternative fuels are further propelling market expansion.

In the Middle East & Africa, abundant natural resources and a strong focus on petrochemical exports underpin the market. Countries such as Saudi Arabia and the UAE are notable contributors, leveraging their vast oil and gas reserves. The region’s strategic initiatives to diversify economies beyond oil are also fostering market growth.

Latin America, with Brazil and Mexico at the forefront, shows moderate growth driven by the region’s industrialization and infrastructure development. The focus on enhancing energy efficiency and sustainability in industrial applications is a key driver in this region.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

Key Players Analysis

In 2023, the global Pentane Plus market was significantly influenced by the strategic activities and market positions of leading companies, each contributing to the sector’s dynamic landscape. ExxonMobil Corporation, a prominent player, continues to leverage its vast resources and advanced refining technologies, ensuring a steady supply of high-quality Pentane Plus. Royal Dutch Shell Plc and Chevron Corporation similarly maintain robust positions through integrated operations and strategic investments in petrochemical advancements.

Phillips 66 and TotalEnergies SE are noteworthy for their emphasis on sustainable practices and innovation, aligning with global shifts towards cleaner energy solutions. Their efforts in enhancing production efficiency and minimizing environmental impact are pivotal to their market leadership.

SABIC and PTT Global Chemical Public Company Limited, representing significant players from the Middle East and Asia, are capitalizing on their resource-rich regions and expanding production capacities to meet rising global demand. Their focus on diversifying product portfolios and strengthening global supply chains bolsters their competitive edge.

INEOS Group Holdings S.A. and Gazprom Neft PJSC are also key contributors, utilizing advanced chemical processing capabilities and extensive distribution networks to enhance market presence. Idemitsu Kosan Co., Ltd. and Indian Oil Corporation Limited (IOCL) are leveraging their strategic locations and refining expertise to cater to the burgeoning demand in Asia.

CNPC and Bharat Petroleum Corporation Limited are reinforcing their positions through significant investments in infrastructure and technology, aimed at optimizing production processes. Reliance Industries Limited continues to be a dominant force in the Indian market, driven by its extensive refining capabilities and strategic market expansions. Maruzen Petrochemical Co., Ltd. rounds out this list with its focus on high-efficiency production techniques and commitment to sustainability.

Market Key Players

- ExxonMobil Corporation

- Royal Dutch Shell Plc

- Chevron Corporation

- Phillips 66

- TotalEnergies SE

- SABIC

- PTT Global Chemical Public Company Limited

- INEOS Group Holdings S.A.

- Gazprom Neft PJSC

- Idemitsu Kosan Co., Ltd.

- Indian Oil Corporation Limited (IOCL)

- CNPC

- Bharat Petroleum Corporation Limited

- Reliance Industries Limited

- Maruzen Petrochemical Co., Ltd.

Recent Development

- In December 2021, Equinor and Exxon Mobil are advancing carbon capture and storage (CCS) projects globally, focusing on reducing greenhouse gas emissions and enhancing energy sustainability.

- In January 2021, Iran aims to eliminate gas flaring by March 2023, enhancing revenue through the Bidboland Gas Refinery. Persian Gulf Petrochemical Industries Company (PGPIC) is expanding its capacity to process ethane, butane, propane, and pentane, with plans for additional projects in the West Karun region.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 132.1 Million |

| Forecast Revenue (2033) | USD 219.3 Million |

| CAGR (2024-2033) | 5.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type(N-Pentane, Isopentane, Neopentane), By Application(Blowing Agent, Solvent, Fuel Additive, Chemical Intermediate, Others), By Purity(Below 95%, Above 95%) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | ExxonMobil Corporation, Royal Dutch Shell Plc, Chevron Corporation, Phillips 66, TotalEnergies SE, SABIC, PTT Global Chemical Public Company Limited, INEOS Group Holdings S.A., Gazprom Neft PJSC, Idemitsu Kosan Co., Ltd., Indian Oil Corporation Limited (IOCL), CNPC, Bharat Petroleum Corporation Limited, Reliance Industries Limited, Maruzen Petrochemical Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The Global Pentane Plus Market is expected to grow at a CAGR of 5.2% (2024-2033).

Market.US has segmented the Global Pentane Plus Market by geographic (North America, Europe, APAC, South America, and Middle East and Africa). By Product Type(N-Pentane, Isopentane, Neopentane), By Application(Blowing Agent, Solvent, Fuel Additive, Chemical Intermediate, Others), By Purity(Below 95%, Above 95%)

ExxonMobil Corporation, Royal Dutch Shell Plc, Chevron Corporation, Phillips 66, TotalEnergies SE, SABIC, PTT Global Chemical Public Company Limited, INEOS Group Holdings S.A., Gazprom Neft PJSC, Idemitsu Kosan Co., Ltd., Indian Oil Corporation Limited (IOCL), CNPC , Bharat Petroleum Corporation Limited , Reliance Industries Limited, Maruzen Petrochemical Co., Ltd.

The US, Canada, Mexico are leading key areas of operation for Global Pentane Plus Market.

The Global Pentane Plus Market Size is USD 132.1 Million in 2023.