Quick Navigation

Report Overview

The Global Syngas Market size is expected to be worth around USD 98.4 Bn by 2033, from USD 53.4 Bn in 2023, growing at a CAGR of 6.3% during the forecast period from 2024 to 2033.

Syngas (Synthesis Gas) is a mixture of gases, primarily composed of hydrogen (H₂), carbon monoxide (CO), and often carbon dioxide (CO₂), that can be used as an intermediate for producing a wide range of chemicals, fuels, and energy. It is typically produced through the gasification of carbon-containing materials such as coal, natural gas, biomass, or even waste materials.

The process involves reacting these materials with oxygen and steam at high temperatures to produce syngas, which can then be used in various industrial applications, including electricity generation, chemical production (like methanol, ammonia, and synthetic fuels), and refining processes.

The energy and chemicals industries are the primary consumers of syngas. For example, in the United States, syngas is widely used for the production of methanol and ammonia, key components in fertilizers and chemicals. The U.S. Department of Energy (DOE) has allocated USD 3 billion for research and development in gasification technologies to support clean energy solutions, including syngas utilization.

In the European Union, syngas plays a role in the production of low-carbon synthetic fuels, aligning with the EU’s goal to become carbon-neutral by 2050, as part of its Green Deal. This push for low-emission energy alternatives has led to an increase in syngas-based projects, particularly in the renewable energy sector, with investments expected to exceed EUR 1.5 billion by 2025.

China, as the world’s largest producer of syngas, exported USD 2.5 billion worth of syngas-based products in 2023. Simultaneously, regions like the Middle East and North Africa (MENA) are increasing their syngas production capacity, with investments in new gasification plants.

For example, Saudi Arabia’s Aramco has invested USD 5 billion in syngas production and related infrastructure, supporting the country’s energy diversification efforts.

In terms of innovation, companies are focusing on improving the efficiency and environmental sustainability of syngas production. For instance, Shell has invested USD 1.3 billion in gasification technology aimed at increasing the yield of syngas while reducing CO₂ emissions.

Air Products and China National Petroleum Corporation (CNPC) entered into a strategic partnership in 2023 to develop syngas production technologies, with the goal of improving energy efficiency and advancing clean hydrogen production.

This partnership is expected to help meet the growing global demand for syngas in the energy transition, which is a key factor behind the USD 2.6 billion in investments announced for syngas-based clean energy projects in 2024.

Key Takeaways

- Syngas Market size is expected to be worth around USD 98.4 Bn by 2033, from USD 53.4 Bn in 2023, growing at a CAGR of 6.3%.

- Petroleum Byproducts held a dominant market position, capturing more than a 43.3% share.

- Steam Reforming held a dominant market position, capturing more than a 37.2% share.

- Fixed Bed held a dominant market position, capturing more than a 38.2% share.

- Methanol held a dominant market position, capturing more than a 34.2% share.

- North America, the syngas market dominates with a commanding 52.5% share, valued at USD 28.01 billion.

By Feedstock

In 2023, Petroleum Byproducts held a dominant market position, capturing more than a 43.3% share. This is mainly due to the established infrastructure and extensive use of petroleum byproducts in the production of syngas, especially in refineries and petrochemical plants.

Petroleum byproducts, such as naphtha and heavy oils, are widely available and offer a reliable feedstock for syngas production, making them the preferred choice in many regions. Their cost-effectiveness and availability in countries with well-developed oil refining industries further strengthen their market dominance.

Coal, while representing a smaller share compared to petroleum byproducts, continues to be a significant feedstock for syngas production. Coal gasification is a well-established process, particularly in regions like China and India, where coal is abundant and cheap.

The rise in coal-to-chemical technologies, especially for producing synthetic fuels and chemicals, has driven the demand for coal as a feedstock. Despite environmental concerns surrounding coal usage, its cost advantages and the need for energy security in certain regions continue to make it a key feedstock for syngas production.

Natural Gas is another key feedstock gaining traction. As natural gas prices remain relatively low in certain regions, it has become a competitive alternative for syngas production. The U.S. and parts of Europe have seen an increase in the use of natural gas for producing syngas due to its cleaner burning properties compared to coal. Natural gas is also increasingly being used for integrated chemical production processes, contributing to its growing share in the market.

Biomass/Waste is seeing steady growth in the syngas sector due to the global push for sustainable energy solutions. Biomass and waste-derived syngas production is a more environmentally friendly option, aligning with government regulations on renewable energy and waste management.

By Process

In 2023, Steam Reforming held a dominant market position, capturing more than a 37.2% share. This process is widely used for producing syngas from natural gas due to its efficiency and cost-effectiveness. Steam reforming is a mature technology that converts methane into hydrogen and carbon monoxide, which are key components of syngas.

Its dominance is supported by the abundance of natural gas and the well-established infrastructure in regions like North America and the Middle East. Steam reforming is also highly favored in the chemical industry for producing hydrogen and ammonia.

Partial Oxidation follows as a key process, contributing a significant share to the market. This method involves the partial combustion of hydrocarbons, such as petroleum byproducts and natural gas, to produce syngas.

It offers advantages in terms of simplicity and faster reaction times compared to other methods. Partial oxidation is especially popular in integrated refineries and petrochemical plants, where it can quickly generate syngas for downstream chemical production. The process is increasingly used in regions with limited natural gas supply, as it can utilize various feedstocks, including heavy oils.

Autothermal Reforming is another important process in syngas production, gaining ground due to its ability to combine steam and oxygen to produce syngas efficiently. This process is particularly used for producing hydrogen and synthetic fuels. While it currently holds a smaller market share, it is growing due to its environmental benefits and higher energy efficiency compared to traditional methods. As the demand for cleaner energy solutions rises, autothermal reforming is expected to see increased adoption, especially in industries focused on sustainable fuel production.

Biomass Gasification is also a notable process, driven by the growing interest in renewable energy and waste-to-energy solutions. Biomass, including agricultural residues and organic waste, is increasingly used as a feedstock for syngas production. While it represents a smaller portion of the market, the segment is expected to grow rapidly due to government incentives and increasing investments in renewable energy technologies. As countries focus on reducing carbon footprints, biomass gasification offers a sustainable pathway for producing syngas from renewable resources.

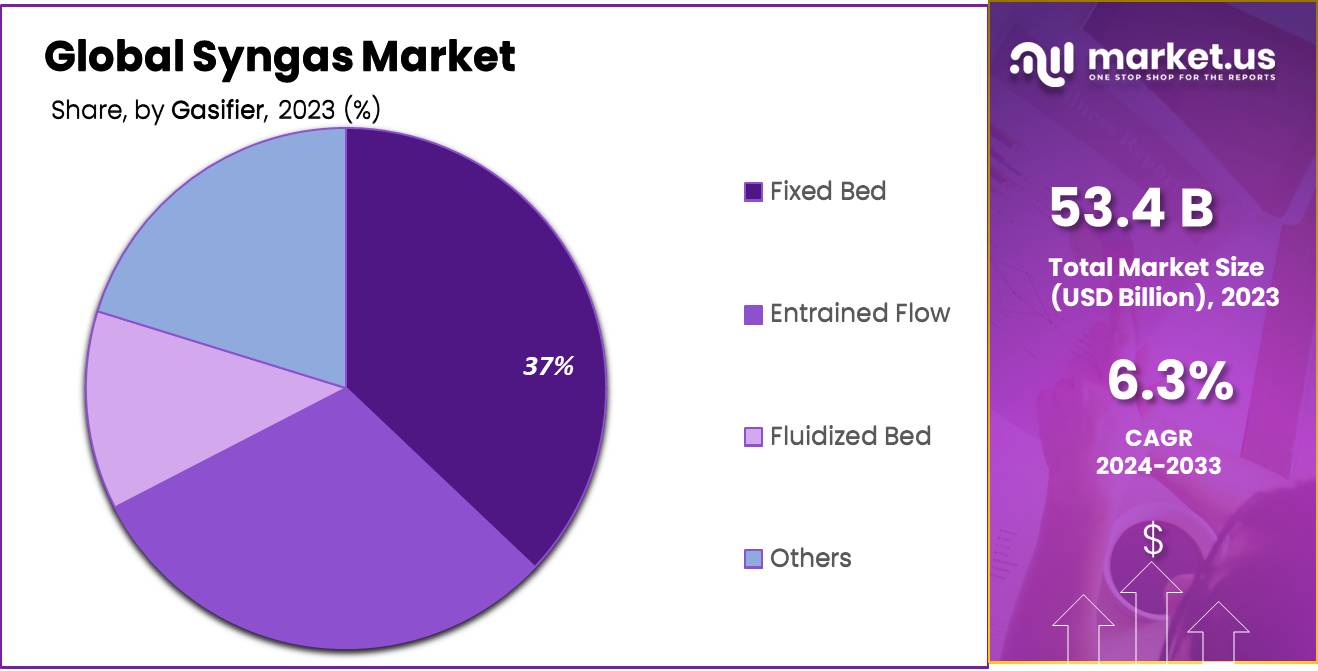

By Gasifier

In 2023, Fixed Bed held a dominant market position, capturing more than a 38.2% share. Fixed bed gasifiers are one of the oldest and most commonly used technologies in syngas production. This process involves feeding feedstock, such as coal or biomass, into a fixed bed where gasification occurs.

Fixed bed gasifiers are preferred for small to medium-scale applications due to their simplicity, reliability, and low operational costs. They are widely used in regions where biomass and coal are the primary feedstocks, making them a popular choice in both developing and developed countries.

Entrained Flow Gasifiers are another important segment, accounting for a significant share of the market. Entrained flow gasification operates at higher temperatures and pressures compared to fixed bed systems, offering greater efficiency and better syngas quality.

This technology is commonly used in large-scale gasification plants, especially for coal and petroleum byproduct feedstocks. As a result, entrained flow gasifiers are particularly favored in energy-intensive industries and regions with large coal reserves, such as China and India. These systems offer a more efficient conversion process, but their high capital costs can be a limiting factor for widespread adoption.

Fluidized Bed Gasifiers also hold a notable share of the market, offering flexibility in the types of feedstock they can process, including biomass, waste materials, and coal. Fluidized bed technology is gaining popularity due to its ability to maintain consistent temperature and flow conditions, resulting in improved syngas quality. This makes them ideal for applications in renewable energy and waste-to-energy projects.

By Application

In 2023, Methanol held a dominant market position, capturing more than a 34.2% share. Methanol is one of the largest applications of syngas, as it is produced by catalytically converting syngas into methanol. This chemical is a critical raw material used in producing a wide range of products, including plastics, paints, adhesives, and antifreeze.

The growing demand for methanol in the production of fuels and chemicals, especially in the automotive and construction industries, has significantly driven the demand for syngas. Furthermore, the increasing use of methanol as an alternative fuel in the shipping industry and its role in producing methyl alcohol have contributed to this dominant market share.

Ammonia follows as another key application of syngas, holding a significant share in the market. Ammonia is primarily used in the production of fertilizers, which are crucial for agriculture. The global push for increasing food production to meet the needs of a growing population has spurred the demand for ammonia.

In 2023, the ammonia sector accounted for a substantial portion of the syngas market, driven by its essential role in the agricultural industry. The demand for ammonia is projected to grow further, especially in regions with large agricultural sectors, such as Asia-Pacific and North America.

Hydrogen is emerging as an increasingly important application of syngas, particularly in the energy and transportation sectors. With the push towards cleaner energy sources, hydrogen production from syngas is being considered a critical pathway. The demand for hydrogen is growing due to its potential in fuel cells and its use in the refining and chemical industries. As hydrogen is gaining traction as a clean alternative fuel, its share in the syngas market is expected to increase over the coming years.

Electricity production from syngas also holds a significant share, particularly in regions with abundant coal and biomass resources. Syngas is used in gas turbine power plants, where it is burned to generate electricity. The increasing demand for decentralized energy production and the adoption of syngas in combined-cycle power plants has made this application increasingly important. Additionally, the use of syngas to produce Synthetic Natural Gas (SNG) is growing as it provides a cleaner alternative to traditional natural gas.

Key Market Segments

By Feedstock

- Petroleum Byproducts

- Coal

- Natural Gas

- Biomass/ Waste

- Others

By Process

- Steam Reforming

- Partial Oxidation

- Autothermal Reforming

- Biomass Gasification

- Others

By Gasifier

- Fixed Bed

- Entrained Flow

- Fluidized Bed

- Others

By Application

- Methanol

- Ammonia

- Hydrogen

- Liquid Fuels

- Direct Reduced Iron

- Synthetic Natural Gas

- Electricity

- Others

Drivers

Global Energy Transition and Clean Energy Initiatives

The transition towards cleaner energy is one of the most significant drivers of the syngas market. In 2023, global investments in clean energy reached approximately USD 1.1 trillion, according to the International Energy Agency (IEA). Syngas, with its ability to produce low-carbon fuels like hydrogen and synthetic natural gas (SNG), is positioned as a key technology in this shift.

Hydrogen, produced via syngas from natural gas (commonly known as “blue hydrogen”), is expected to play a central role in decarbonizing sectors such as transportation, industrial heating, and energy storage.

The IEA forecasts that by 2030, the global hydrogen market will be valued at USD 300 billion, with syngas-based hydrogen being a major contributor to this growth. Governments are offering subsidies and incentives to encourage the development of technologies such as syngas to meet clean energy targets.

Rising Demand for Synthetic Fuels and Chemical Production

Syngas is a vital feedstock for producing synthetic fuels, which are increasingly in demand due to the need for cleaner alternatives to traditional petroleum-based fuels. In 2023, global production of synthetic fuels from syngas reached approximately 10.5 million barrels per day (bpd), according to the U.S. Energy Information Administration (EIA).

The process of converting syngas into synthetic fuels offers a pathway to produce cleaner fuels with fewer emissions compared to conventional fossil fuels. Additionally, syngas is critical in producing ammonia for fertilizers and methanol for a variety of chemical products.

The global fertilizer market, which consumed around 200 million metric tons of ammonia in 2023, relies heavily on syngas as a feedstock. This sustained demand for chemicals and fuels produced via syngas is a key factor driving the market’s growth.

Supportive Government Regulations and Incentives

Governments worldwide are driving the demand for syngas through favorable policies and incentives designed to support clean energy solutions. For instance, in 2023, the U.S. government allocated USD 8.5 billion towards research and development of carbon capture and utilization (CCU) technologies, many of which utilize syngas.

The European Union’s Green Deal, which aims for a 55% reduction in greenhouse gas emissions by 2030, includes syngas as a key element for clean hydrogen production and carbon capture solutions. Similarly, China, the world’s largest producer of syngas-based synthetic fuels, has committed to investing USD 4.6 billion in syngas and hydrogen technologies as part of its green energy transition.

Technological Innovations in Syngas Production

Technological advancements in syngas production processes, such as improved gasification technologies and more efficient reactors, are making syngas production more economically viable. In 2023, global investments in syngas-based technologies reached USD 2.3 billion, driven by both private and public sector players.

One of the most notable innovations is the development of advanced gasifiers and autothermal reforming processes, which improve the efficiency of syngas production and reduce carbon emissions. Companies in regions like Europe and North America are also forming partnerships to develop next-generation syngas technologies that can produce hydrogen with lower environmental impacts.

Restraints

High Initial Capital Investment in Gasification Plants

The construction of a syngas production facility, whether using coal, natural gas, or biomass, requires substantial upfront capital. For instance, the cost of building an integrated gasification combined cycle (IGCC) plant can exceed USD 2.5 billion for large-scale operations.

According to the U.S. Department of Energy (DOE), the capital cost of IGCC plants, which are used for syngas production, is approximately USD 3,000 per installed kW, making them significantly more expensive than traditional combustion power plants. The high capital investment required for gasification infrastructure often makes it a less attractive option compared to alternative energy technologies that require lower initial investments.

Operational Costs and Efficiency Challenges

In addition to the high initial investment, operating a syngas production plant can also be expensive. For example, syngas production from coal or biomass requires large quantities of feedstock, and the preparation of these materials can involve additional costs for transportation, drying, and handling.

The U.S. Energy Information Administration (EIA) reports that biomass gasification costs can range from USD 70 to USD 130 per MWh, which can be significantly higher than natural gas-fired power generation. Furthermore, the maintenance and operation of gasifiers, which require high temperatures (up to 1,500°C for some systems), add to the operational costs.

Environmental Regulations and Compliance Costs

Environmental regulations also play a role in the high operational costs of syngas plants. Syngas production from coal and biomass is subject to strict environmental standards, especially regarding carbon emissions and the handling of waste products.

According to the European Union’s Industrial Emissions Directive, companies involved in syngas production must comply with emissions limits for pollutants such as sulfur dioxide (SO₂), nitrogen oxides (NOₓ), and particulate matter, which can increase operational costs. In some cases, companies must invest in additional technologies, such as carbon capture and storage (CCS) systems, to meet these regulations.

Market Competition from Alternative Technologies

Another challenge to the growth of the syngas market comes from the increasing competition from alternative energy technologies that are more cost-effective and scalable. For example, renewable energy sources like wind and solar power have seen dramatic cost reductions in recent years.

The International Renewable Energy Agency (IRENA) reports that the levelized cost of electricity (LCOE) from solar power fell by 89% from 2010 to 2020. In comparison, the costs associated with syngas production remain relatively high, making it harder for syngas to compete in the growing renewable energy market.

Opportunity

Global Shift Toward Hydrogen as Clean Energy Source

According to the International Energy Agency (IEA), hydrogen demand is expected to double by 2030. Syngas plays a crucial role in the production of hydrogen, particularly blue hydrogen, produced from natural gas via steam reforming.

This process uses syngas as an intermediate to extract hydrogen while capturing and storing carbon dioxide (CO₂), making it a pivotal solution in reducing greenhouse gas emissions. With growing hydrogen production capacity, syngas is expected to see continued demand in the coming years, especially as governments increase funding for clean hydrogen initiatives.

In the U.S., the Hydrogen Energy Earthshot initiative aims to reduce hydrogen production costs to USD 1 per kilogram by 2030, further boosting syngas demand for hydrogen production.

Government Policies and Subsidies for Clean Energy

Government policies are increasingly favoring syngas as a critical technology for achieving sustainability and clean energy goals. For instance, in Europe, the European Union (EU) has set an ambitious Green Deal, aiming to cut emissions by 55% by 2030 compared to 1990 levels. As part of this transition, the EU is focusing on scaling up the use of clean hydrogen, which is produced from syngas.

The EU’s Hydrogen Strategy for a Climate-Neutral Europe outlines plans to invest €430 billion in clean hydrogen technologies by 2030, creating significant opportunities for syngas-based hydrogen production. Similarly, in Asia, countries like China and Japan are focusing on hydrogen as part of their future energy systems, which is likely to drive further syngas demand for hydrogen production.

Technological Advancements and Cost Reductions

Advancements in syngas production technology are also opening up new opportunities for growth. Continuous research and development are making syngas production more efficient and cost-effective. For example, gasification technologies such as autothermal reforming and biomass gasification are being optimized to reduce operational costs and improve overall efficiency.

The U.S. Department of Energy (DOE) has allocated USD 100 million for clean energy research and development projects, including syngas and hydrogen production, as part of its “Clean Hydrogen Program.”

Additionally, partnerships between major industrial players and startups focusing on syngas and hydrogen production are leading to breakthrough innovations. These advancements are expected to reduce the cost of hydrogen production via syngas, making it a more competitive option in the global energy market.

Expanding Role in Industrial Decarbonization

Another growth opportunity lies in the increasing role of syngas in industrial decarbonization. Industries such as steel production, cement, and chemicals are some of the largest industrial emitters of CO₂. Syngas, particularly through the production of synthetic natural gas (SNG) and methanol, is being increasingly used as a cleaner alternative in these high-emission sectors.

The International Energy Agency (IEA) estimates that syngas-based synthetic fuels could reduce CO₂ emissions in the industrial sector by up to 25% by 2050. Many industrial players are investing in syngas technologies to reduce their carbon footprint and comply with stricter emission regulations.

As these industries continue to adopt syngas-based solutions, there will be a significant increase in syngas demand. Governments are also incentivizing this transition through various green subsidies and emission reduction programs.

For example, the Carbon Clean Solutions company recently announced a partnership to scale syngas technologies for industrial decarbonization projects, highlighting the growing industrial demand for syngas-based solutions.

Trends

Rising Demand for Low-Carbon Syngas Production

The growing demand for low-carbon solutions is significantly driving the adoption of CCU technologies in syngas production. According to the International Energy Agency (IEA), the global demand for hydrogen—produced from syngas—will require 9 million tonnes of blue hydrogen by 2030, representing a substantial increase in syngas-based hydrogen production.

Blue hydrogen involves using syngas and employing carbon capture technologies to prevent the release of carbon dioxide into the atmosphere. This trend aligns with the global climate targets of limiting global warming to 1.5°C by 2050. Governments around the world, including the European Union, are offering incentives for companies to adopt CCU technologies, further boosting the demand for syngas.

Government Regulations and Investments in Carbon Capture Projects

Government regulations are playing a crucial role in promoting the integration of CCU technologies with syngas production. For example, the U.S. Department of Energy (DOE) has committed USD 2.5 billion in 2023 to support the development of CCUS (Carbon Capture, Utilization, and Storage) projects. This funding is directed toward advancing technologies that can capture and utilize carbon emissions from industrial sources, including syngas plants.

The European Commission has also outlined plans to boost the CCU sector, with an investment of EUR 5 billion by 2025 in the EU’s Green Deal to facilitate the adoption of cleaner technologies, including syngas production for hydrogen and synthetic fuels. These investments are encouraging syngas producers to incorporate carbon capture technologies in their operations, aligning with global sustainability goals.

Technological Advancements in Carbon Capture Utilization

Technological innovations are making carbon capture more feasible and cost-effective, driving the shift toward syngas production with integrated CCU systems. The advancements in membrane technology, solvent-based capture systems, and direct air capture methods are reducing the cost of capturing CO₂ from syngas production processes.

For instance, new catalysts and membrane technologies have significantly improved the efficiency of carbon capture systems, making it more economically viable for syngas producers to integrate CCU. This has been particularly beneficial for industries that are heavily reliant on syngas, such as the chemicals and power generation sectors.

The increasing focus on sustainable chemicals and green fuels is also contributing to the demand for syngas produced with carbon capture. Major companies like Shell, Equinor, and Chevron are actively pursuing partnerships and investing in CCU projects to reduce their carbon footprints while maintaining production levels. In fact, Shell announced in 2023 an investment of USD 1.4 billion in a large-scale CCU project aimed at producing low-carbon hydrogen from syngas.

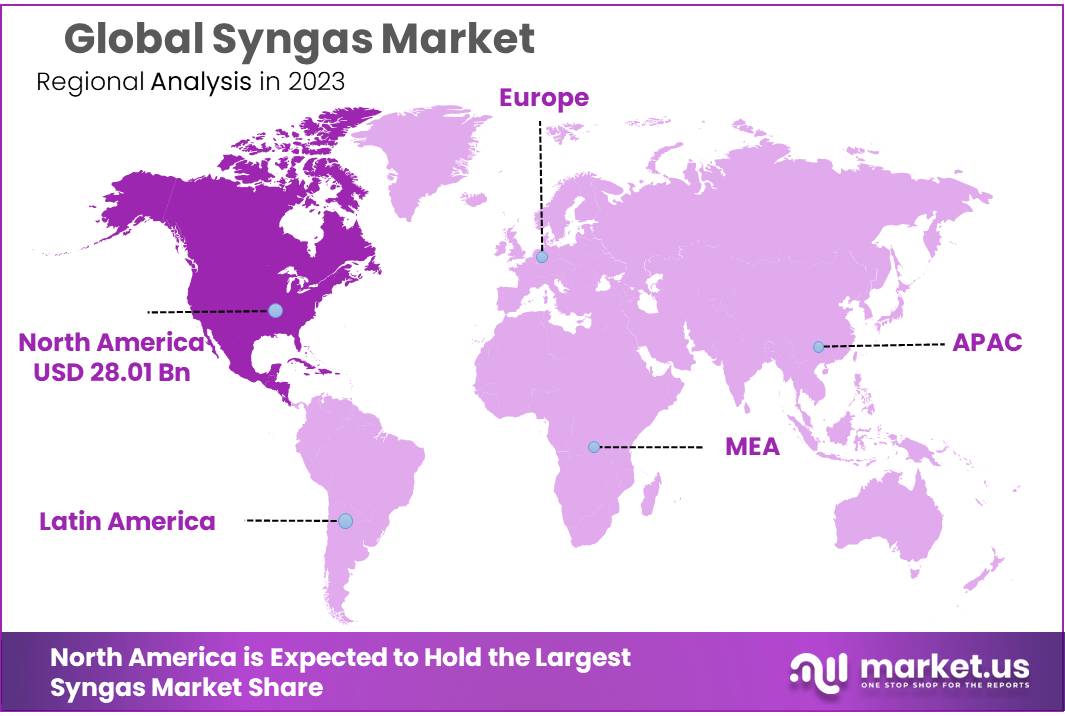

Regional Analysis

The syngas market exhibits distinct characteristics across various global regions, reflecting diverse industrial dynamics, resource availability, and technological advancements. In North America, the syngas market dominates with a commanding 52.5% share, valued at USD 28.01 billion.

This region’s leadership stems from extensive investments in gasification technology and the presence of major players in the chemical and energy sectors. The adoption of syngas is propelled by the shift towards cleaner energy sources and the growing demand for high-value chemicals and fuels.

Europe, with its stringent environmental regulations, focuses on sustainable energy practices, making syngas an integral part of its renewable energy strategy. The market here benefits from advanced technological infrastructure and government incentives promoting the reduction of carbon footprints, thereby driving the demand for syngas in chemical manufacturing and power generation.

The Asia Pacific region is witnessing rapid growth in the syngas market due to increasing energy demands and industrialization, particularly in emerging economies like China and India. The availability of abundant raw materials such as coal and biomass, coupled with technological advancements in gasification methods, supports the region’s expanding syngas production capabilities. This region is anticipated to surpass others in terms of growth rate, driven by escalating energy consumption and ongoing infrastructure developments.

The Middle East & Africa, with its significant natural gas reserves, is gradually adopting syngas technology to diversify its energy sources and reduce reliance on crude oil. The growth in this region is supported by the rising demand for ammonia-based fertilizers and methanol, which are produced using syngas.

Latin America, though smaller in market size compared to other regions, is exploring syngas applications due to increasing local energy requirements and the potential for biomass gasification, given its vast agricultural landscape. The development of this market is pivotal for regional energy security and sustainability.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The syngas market is highly competitive, with several key players driving innovation and technological advancements in the sector. Air Liquide, a global leader in industrial gases, plays a significant role in syngas production through its advanced gasification technologies and partnerships with large-scale industrial players.

The company’s focus on clean energy solutions, including hydrogen production via syngas, has contributed to its strong position in the market. Similarly, Air Products and Chemicals Inc., another major player, provides comprehensive syngas solutions and is actively involved in projects related to hydrogen production and carbon capture, enhancing its presence in the growing demand for low-carbon syngas.

Linde Plc and KBR Inc. are also major contributors to the syngas market, leveraging their strong capabilities in gasification and process engineering to offer syngas production technologies. Linde’s innovations in oxygen and hydrogen production through syngas are significant, while KBR’s expertise in integrated gasification combined cycle (IGCC) technologies has positioned it as a key player for producing clean syngas.

Sasol, a major South African chemical company, specializes in coal-to-liquid (CTL) and gas-to-liquid (GTL) technologies, which are central to syngas production for both fuel and chemical applications. Methanex Corporation, the world’s largest producer of methanol, also relies heavily on syngas for methanol synthesis, reinforcing its importance in the syngas market.

Top Key Players

- A.H.T Syngas Technology NV

- Air Liquide

- Air Products and Chemicals Inc.

- Airpower Technologies Limited

- Chiyoda Corporation

- Dow Inc.

- John Wood Group PLC

- KBR Inc.

- Linde Plc

- Maire Tecnimont Spa

- Methanex Corporation

- Sasol

- Shell Plc

- Synthesis Energy Systems Inc.

- The Linde Group

- Topsoe AS

- Yankuang Group

Recent Developments

In 2023, A.H.T Syngas Technology NV reported a 15% increase in revenue compared to the previous year, with a focus on expanding its presence in European and North American markets.

In 2024 Air Liquide, the company aims to further strengthen its leadership position by investing USD 2.3 billion into projects focused on clean energy, carbon capture, and hydrogen infrastructure.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 53.4 Bn |

| Forecast Revenue (2033) | USD 98.4 Bn |

| CAGR (2024-2033) | 6.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Feedstock (Petroleum Byproducts, Coal, Natural Gas, Biomass/ Waste, Others), By Process (Steam Reforming, Partial Oxidation, Autothermal Reforming, Biomass Gasification, Others), By Gasifier (Fixed Bed, Entrained Flow, Fluidized Bed, Others), By Application (Methanol, Ammonia, Hydrogen, Liquid Fuels, Direct Reduced Iron, Synthetic Natural Gas, Electricity, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | A.H.T Syngas Technology NV, Air Liquide, Air Products and Chemicals Inc., Airpower Technologies Limited, Chiyoda Corporation, Dow Inc., John Wood Group PLC, KBR Inc., Linde Plc, Maire Tecnimont Spa, Methanex Corporation, Sasol, Shell Plc, Synthesis Energy Systems Inc., The Linde Group, Topsoe AS, Yankuang Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |