Quick Navigation

- Report Overview

- Key Takeaways

- By Source Type Analysis

- By Product Analysis

- By Function Analysis

- By Type Analysis

- By Manufacturing Process Analysis

- By Grade Analysis

- By Application Analysis

- By End-Use Industry Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

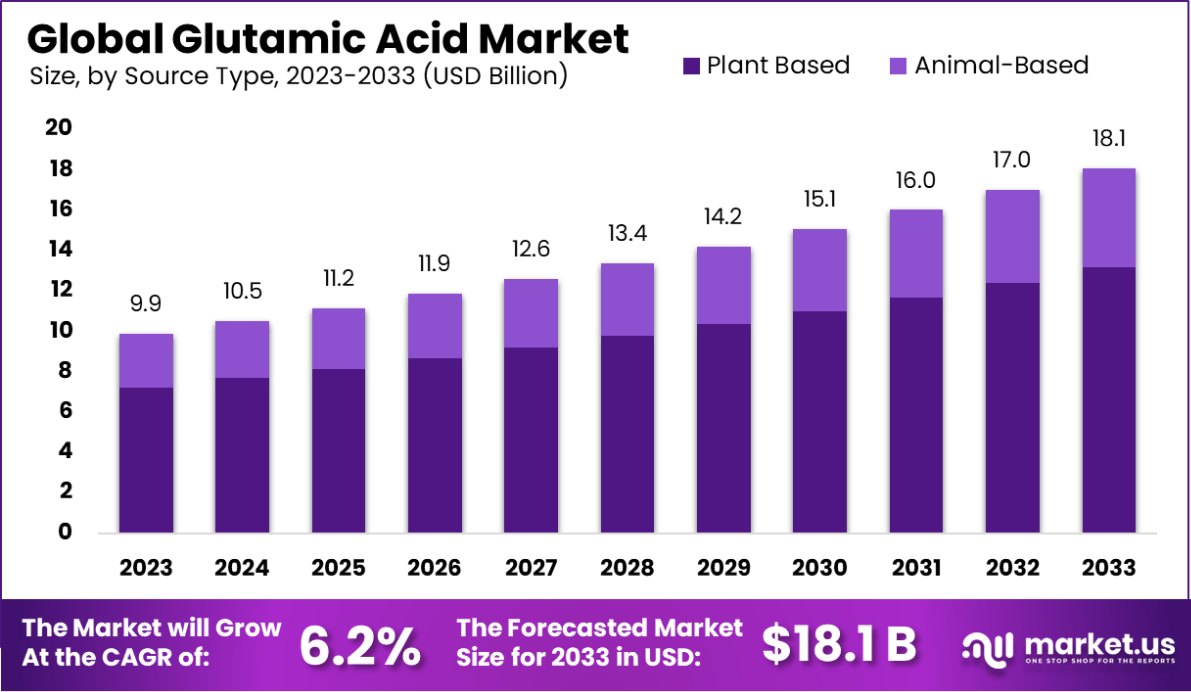

The Global Glutamic Acid Market is expected to be worth around USD 18.1 Billion by 2033, up from USD 9.9 Billion in 2023, and grow at a CAGR of 6.2% from 2024 to 2033.

Glutamic Acid is a naturally occurring amino acid found in protein-rich foods like meat, fish, and some vegetables. It is primarily used in the food industry as a flavor enhancer, commonly known as monosodium glutamate (MSG). Additionally, glutamic acid plays a key role in metabolism and is used in the pharmaceutical, agriculture, and biotechnology industries.

The demand for glutamic acid is increasing due to its widespread use in food processing, where it enhances taste and reduces sodium content. As consumer preference shifts toward processed and convenience foods, global glutamic acid production has been rising.

The growing trend toward plant-based protein and clean-label products presents opportunities to develop new glutamic acid applications in food and beverages, alongside potential uses in bio-based polymers.

The Glutamic Acid market is poised for steady growth driven by its diverse applications across food, pharmaceuticals, and biotechnology. As an essential amino acid naturally found in foods like meats, dairy, and vegetables, glutamic acid, particularly in its L-glutamic acid form, plays a pivotal role in human metabolism. Its use as a flavor enhancer in the food industry, especially in processed foods, remains a primary driver of demand.

According to jn.nutrition.org, the average daily intake of glutamic acid for a 70-kg individual is approximately 28 grams, sourced both from dietary intake and the breakdown of gut proteins. This widespread presence and turnover of glutamic acid in the human body underline its fundamental biological importance.

Additionally, glutamic acid, which typically contains between 98.5% and 101.5% purity of C5H9NO4 when calculated on a dried basis (ipc.gov.in), continues to be a critical component for enhancing flavor and improving food texture in the global market.

The expanding demand for processed and convenience foods, driven by a fast-paced lifestyle and urbanization, is accelerating glutamic acid consumption. Moreover, the increasing shift toward plant-based and clean-label products presents further growth opportunities. The pharmaceutical and biotechnology sectors are also leveraging glutamic acid for its role in metabolic pathways, which adds another layer of growth potential.

As the global glutamic acid production capacity expands, companies have an opportunity to tap into both emerging markets and innovation in applications, including its use in bio-based polymers and nutraceuticals.

Enhanced analytical techniques, such as the Van Slyke manometric apparatus, have improved the precision of glutamic acid quantification, contributing to its rising utility in research and development.

Key Takeaways

- The Global Glutamic Acid Market is expected to be worth around USD 18.1 Billion by 2033, up from USD 9.9 Billion in 2023, and grow at a CAGR of 6.2% from 2024 to 2033.

- The global glutamic acid market is predominantly driven by plant-based sources, accounting for 73.4%.

- Biosynthesis contributes significantly to glutamic acid production, representing 67.6% of the market share.

- Plant growth stimulants comprise 25.7% of the glutamic acid market, highlighting agricultural demand.

- L-Glutamic acid dominates the market, with 88.3% of total production attributed to this type.

- Fermentation is the leading manufacturing process for glutamic acid, with 68.4% of global production.

- Food-grade glutamic acid holds a substantial market share of 58.4%, ensuring safety for consumption.

- Flavor enhancers account for 46.7% of glutamic acid applications, emphasizing its role in food processing.

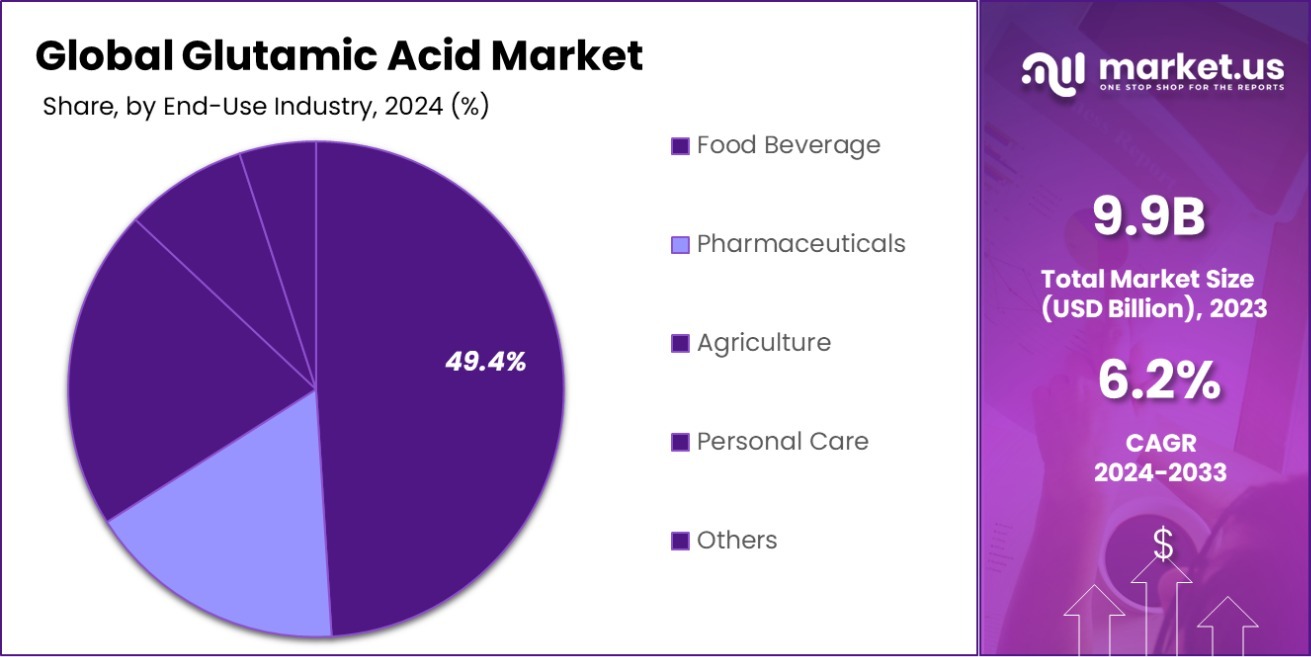

- The food and beverage industry represents 49.4% of the glutamic acid market, driving demand.

- The Asia-Pacific glutamic acid market holds a 43.3% share, valued at USD 4.2 billion.

By Source Type Analysis

The glutamic acid market is primarily driven by plant-based sources, comprising 73.4% of the total production.

In 2023, Plant-Based sources held a dominant market position in the By Source Type segment of the Glutamic Acid Market, accounting for a significant 73.4% share. This trend is primarily attributed to the growing consumer preference for plant-derived products, driven by increasing health consciousness and the rising popularity of vegan and vegetarian diets.

Plant-based glutamic acid is typically derived from natural sources such as corn, sugar beets, and tapioca, which provide a sustainable and cost-effective alternative to animal-based products.

The demand for plant-based glutamic acid is expected to continue expanding, supported by the increasing adoption of clean-label ingredients and the growing inclination toward natural food additives that align with environmental and ethical considerations.

Conversely, Animal-Based glutamic acid holds a smaller but notable share of the market. In 2023, it accounted for approximately 26.6% of the segment. Animal-based glutamic acid is traditionally produced through the hydrolysis of animal proteins, particularly from sources like meat and fish.

Although this source type has been historically prevalent, its market share has been gradually declining as consumers increasingly demand plant-derived alternatives, spurred by concerns regarding animal welfare and sustainability.

By Product Analysis

Biosynthesis is a dominant method in glutamic acid production, contributing 67.6% of the overall market share.

In 2023, Biosynthesis held a dominant market position in the By Product segment of the Glutamic Acid Market, commanding a substantial 67.6% share. This dominant position is primarily driven by the increasing demand for naturally derived glutamic acid, which aligns with consumer preferences for cleaner, more sustainable products.

Biosynthesis involves the fermentation of natural substrates such as carbohydrates, using microorganisms like bacteria or yeast to produce glutamic acid. This method is widely favored due to its eco-friendly production process, lower energy consumption, and the growing trend of plant-based and natural food additives.

As sustainability and clean-label products become a higher priority for consumers and manufacturers alike, biosynthesis is expected to maintain a strong foothold in the market.

In contrast, Industrial Synthesis accounted for a smaller portion of the market, with a share of approximately 32.4% in 2023. Industrial synthesis typically involves the use of chemical processes, often derived from petroleum-based feedstocks, to produce glutamic acid. While this method has been historically prevalent due to its cost-effectiveness and scalability, it faces growing challenges.

These include increasing concerns over the environmental impact of synthetic production methods and a rising preference for naturally sourced ingredients. As a result, industrial synthesis is likely to experience slower growth compared to biosynthesis in the coming years.

By Function Analysis

Plant growth applications hold a significant portion of the glutamic acid market, accounting for 25.7% of total demand.

In 2023, Plant Growth held a dominant market position in the By Function segment of the Glutamic Acid Market, with a notable 25.7% share. This function’s prominence can be attributed to the increasing use of glutamic acid as a growth promoter in agricultural applications. Glutamic acid plays a critical role in stimulating plant growth and enhancing the efficiency of nutrient uptake.

It is used in various fertilizers and biostimulants to improve crop yields and support plant health, particularly in the context of sustainable agriculture. The rise in demand for organic and eco-friendly farming practices, along with the need for higher crop productivity, has significantly contributed to the growth of this segment.

Other functional applications of glutamic acid, such as NMR Spectroscopy, Nutrient, Flavor Enhancer, Detoxifying Agent, Neurotransmitter, and Metabolism, hold smaller but noteworthy shares in the market. NMR Spectroscopy and Nutrient applications utilize glutamic acid for its chemical properties in analytical procedures and as an essential amino acid in human nutrition, respectively.

Flavor Enhancer is a widely recognized function, with glutamic acid being a key component in the production of monosodium glutamate (MSG) for food seasoning.

Although these functions contribute to market diversification, the Plant Growth segment remains the largest due to the growing emphasis on agricultural productivity and sustainable farming practices.

By Type Analysis

L-Glutamic acid represents the largest segment, with 88.3% of the market focusing on this specific type.

In 2023, L-Glutamic Acid held a dominant market position in the By Type segment of the Glutamic Acid Market, with a substantial 88.3% share. This dominance can be attributed to L-glutamic acid’s widespread use in various industries, particularly in food and beverage applications, where it serves as a key flavor enhancer in the form of monosodium glutamate (MSG).

Its natural occurrence in proteins and its essential role in human metabolism contribute to its preference over other forms. Additionally, L-glutamic acid is extensively used in the pharmaceutical and nutraceutical sectors due to its benefits as an amino acid, aiding in protein synthesis and neurotransmitter function.

The growing consumer demand for natural and clean-label ingredients further boosts the adoption of L-glutamic acid, reinforcing its market leadership.

In contrast, DL-Glutamic Acid, which accounts for the remaining 11.7% of the market in 2023, is a synthetic form of glutamic acid composed of both L- and D-forms. DL-Glutamic Acid is typically used in industrial applications, including animal feed and certain chemical processes.

However, it is less favored in food applications due to its lower bioavailability and functional properties compared to L-glutamic acid. The relatively smaller share of DL-Glutamic Acid in the market reflects the growing preference for natural, high-quality ingredients across various sectors.

Overall, L-Glutamic Acid is expected to maintain its dominant position, driven by its versatility and alignment with consumer trends favoring natural products.

By Manufacturing Process Analysis

Fermentation remains the leading manufacturing process for glutamic acid, contributing 68.4% to the industry’s overall production.

In 2023, Fermentation held a dominant market position in the By Manufacturing Process segment of the Glutamic Acid Market, with a commanding 68.4% share. This dominance is largely driven by the increasing preference for bio-based, sustainable production methods that align with the rising demand for clean-label and natural products.

The fermentation process involves the use of microorganisms, such as bacteria or yeast, to convert raw materials like glucose or starch into glutamic acid. This method is widely favored for its cost-effectiveness, scalability, and lower environmental impact compared to traditional chemical synthesis.

The growth of the plant-based and organic food sectors, along with greater consumer awareness of sustainability issues, has further strengthened the position of fermentation as the primary production method.

In contrast, Chemical Synthesis accounted for a smaller share of the market, with approximately 31.6% in 2023. Chemical synthesis involves the use of synthetic chemicals and processes to produce glutamic acid, which is often derived from petroleum-based feedstocks. While chemical synthesis is still widely used due to its efficiency and ability to meet large-scale production needs, it faces increasing competition from fermentation methods due to growing environmental and sustainability concerns.

Looking ahead, the fermentation segment is expected to continue dominating the market, driven by the shift towards more sustainable, natural, and bio-based production methods in line with consumer trends and regulatory pressures.

By Grade Analysis

The food grade segment of glutamic acid makes up 58.4% of the market, highlighting its wide use.

In 2023, Food Grade held a dominant market position in the By Grade segment of the Glutamic Acid Market, accounting for 58.4% of the market share. This leadership is primarily driven by the widespread use of food-grade glutamic acid as a flavor enhancer in processed foods, including snacks, soups, sauces, and seasonings.

Additionally, food-grade glutamic acid is a key ingredient in the production of monosodium glutamate (MSG), which remains a popular additive in the global food industry.

The increasing demand for convenience foods, along with rising consumer preference for savory and umami flavors, further reinforces the growth of this segment. As clean-label trends and natural ingredient sourcing gain prominence, food-grade glutamic acid is expected to maintain its dominant position.

Pharmaceutical Grade glutamic acid, which accounted for a smaller share of the market, serves specialized applications in the pharmaceutical industry, including its use in intravenous nutrition solutions and amino acid supplements. This segment represents around 20.3% of the market in 2023, driven by the growing demand for amino acid-based therapies and treatments.

Feed Grade, which made up approximately 21.3% of the market, is used primarily in animal nutrition. This segment is influenced by the expansion of the livestock industry and the need for cost-effective feed additives to enhance animal growth and health.

Overall, the food-grade segment is poised for continued dominance, driven by strong consumer demand and its broad application across the food and beverage industry.

By Application Analysis

Flavor enhancer applications dominate the glutamic acid market, making up 46.7% of its overall demand and usage.

In 2023, Flavor Enhancer held a dominant market position in the By Application segment of the Glutamic Acid Market, capturing a substantial 46.7% share. This dominance is largely attributed to the widespread use of glutamic acid, primarily in the form of monosodium glutamate (MSG), as a key ingredient in enhancing the umami flavor of a variety of food products.

MSG is commonly used in processed foods such as snacks, soups, sauces, and seasonings to improve taste perception. The growing consumer demand for savory, rich flavors, combined with the increasing popularity of convenience foods, has solidified the position of flavor enhancers in the glutamic acid market.

Additionally, the clean-label trend and the preference for naturally derived flavor additives continue to drive the adoption of glutamic acid-based flavor enhancers in the food industry.

Nutritional Supplement applications, accounting for approximately 25.5% of the market in 2023, are another significant contributor to glutamic acid demand. Glutamic acid is used in amino acid-based supplements, which support muscle health, protein synthesis, and overall metabolic function.

The Pharmaceutical Ingredient and Animal Feed Additive segments represent smaller shares of the market, at 15.8% and 12.0% respectively. Glutamic acid’s use in pharmaceuticals focuses on its role in intravenous nutrition solutions, while in animal feed, it is used to enhance growth and health in livestock.

Overall, the flavor enhancer application remains the dominant driver of glutamic acid consumption, with strong growth prospects fueled by evolving food trends.

By End-Use Industry Analysis

The food and beverage industry is the primary end-use sector, accounting for 49.4% of glutamic acid consumption.

In 2023, Food & Beverage held a dominant market position in the By End-Use Industry segment of the Glutamic Acid Market, with a significant 49.4% share. This dominance is primarily driven by the extensive use of glutamic acid, especially in the form of monosodium glutamate (MSG), as a flavor enhancer in processed foods.

MSG is widely utilized to improve the umami flavor in a range of food products, including snacks, soups, sauces, ready-to-eat meals, and seasonings.

The increasing demand for convenience foods, coupled with the growing consumer preference for savory flavors, continues to bolster the food & beverage sector’s share of the glutamic acid market. Additionally, the clean-label movement and rising consumer awareness of natural food ingredients are expected to support continued growth in this segment.

Pharmaceuticals, accounting for approximately 23.2% of the market share in 2023, remains another key end-use industry for glutamic acid. It is used in pharmaceutical formulations, particularly in amino acid-based intravenous solutions and supplements that support metabolic and neurological health.

The Agriculture sector, representing around 15.1% of the market, uses glutamic acid primarily as a plant growth promoter and in agricultural biostimulants. Personal Care applications, though smaller at 12.3%, utilize glutamic acid for its moisturizing and conditioning properties in skin care products and hair care products.

Overall, the food & beverage industry is expected to maintain its leadership position, driven by evolving consumer preferences for flavor enhancement and the continued growth of processed food consumption.

Key Market Segments

By Source Type

- Plant Based

- Animal-Based

By Product

- Biosynthesis

- Industrial Synthesis

By Function

- Plant Growth

- NMR Spectroscopy

- Nutrient

- Flavor Enhancer

- Detoxifying Agent

- Neurotransmitter

- Metabolism

- Others

By Type

- L-Glutamic Acid

- DL-Glutamic Acid

By Manufacturing Process

- Fermentation

- Chemical Synthesis

By Grade

- Food Grade

- Pharmaceutical Grade

- Feed Grade

By Application

- Flavor Enhancer

- Nutritional Supplement

- Pharmaceutical Ingredient

- Animal Feed Additive

- Others

By End Use Industry

- Food Beverage

- Pharmaceuticals

- Agriculture

- Personal Care

- Others

Driving Factors

Increasing Demand for Umami Flavors in Food Products

The rising consumer preference for savory, umami-rich flavors has significantly boosted the demand for glutamic acid, particularly in the form of monosodium glutamate (MSG). As consumers increasingly seek enhanced taste experiences in a variety of processed foods, glutamic acid plays a key role in delivering deep, satisfying flavors.

The popularity of convenience foods, such as snacks, soups, sauces, and ready-to-eat meals, further strengthens the demand for glutamic acid as a flavor enhancer, making it indispensable in modern food formulations.

Growth of Plant-Based and Clean-Label Trends

As consumers shift toward healthier, sustainable, and plant-based diets, the demand for natural ingredients, including glutamic acid, has surged. The increasing popularity of plant-based products, such as vegan snacks and meat alternatives, is fueling the need for naturally sourced glutamic acid.

Clean-label trends, where consumers seek products with fewer synthetic additives and preservatives, further drive this shift. As more food manufacturers adopt clean-label and natural ingredients, the market for plant-based glutamic acid is expected to grow, supported by the rising preference for plant-derived products.

Expanding Use of Glutamic Acid in Pharmaceuticals

The use of glutamic acid in pharmaceuticals is another critical factor driving its market growth. Glutamic acid plays a vital role in several medical and nutritional applications, particularly in amino acid-based intravenous solutions and dietary supplements.

As the global healthcare sector continues to expand, the demand for glutamic acid as a nutritional supplement and as part of therapeutic treatments for metabolic and neurological disorders has risen. This growing application in the pharmaceutical industry contributes significantly to the overall demand for glutamic acid, particularly in amino acid therapies.

Restraining Factors

High Production Costs and Raw Material Prices

The high costs associated with producing glutamic acid pose a significant challenge to market growth. The manufacturing process involves the use of specialized equipment, high-energy consumption, and raw materials such as glucose or starch, which are subject to price fluctuations.

As the cost of these raw materials increases, manufacturers may face pressure to raise the prices of glutamic acid, which could reduce demand from price-sensitive customers in industries like food and beverages, pharmaceuticals, and animal feed. This cost factor is a key restraint in the market.

Stringent Regulatory Standards and Compliance Challenges

Regulatory standards surrounding the production and use of glutamic acid are becoming increasingly stringent, particularly in food and pharmaceuticals. Manufacturers must comply with safety regulations, quality control standards, and certifications required by local and international authorities.

These compliance requirements increase operational costs and often involve lengthy approval processes, delaying the time-to-market for new products. Additionally, countries may have different standards, making global trade and distribution more complex and costly. These regulatory challenges act as a restraint on the growth of the glutamic acid market.

Consumer Health Concerns Over Additives and Chemicals

There is growing consumer awareness regarding the potential health risks associated with artificial additives, including glutamic acid, commonly known as monosodium glutamate (MSG). Some individuals report sensitivity to glutamate, experiencing headaches, sweating, or other adverse effects.

As a result, many consumers avoid foods and products containing glutamic acid, particularly in regions with high health consciousness. This shift in consumer preference towards natural and preservative-free alternatives poses a challenge to glutamic acid producers, especially in the food and beverage industry where it is widely used as a flavor enhancer.

Growth Opportunity

Rising Demand for Processed Foods and Beverages

The growing global preference for convenience and processed foods is driving the demand for glutamic acid as a flavor enhancer. With the increasing consumption of ready-to-eat meals, snacks, and beverages, glutamic acid is used to improve the taste and palatability of these products.

This trend is particularly notable in emerging economies, where busy lifestyles and rising disposable incomes lead to higher consumption of packaged and processed foods. This shift presents significant growth opportunities for glutamic acid producers, especially in the food and beverage sector.

Expanding Applications in Pharmaceutical and Nutritional Products

Glutamic acid’s versatility extends beyond the food industry into pharmaceuticals and nutritional supplements. It is used in the formulation of amino acid-based therapies, supporting metabolic health, and aiding in recovery for certain medical conditions.

As healthcare systems worldwide focus on improving nutrition and treating deficiencies through supplements, glutamic acid is increasingly being incorporated into specialized formulations. This expanding application in the health and wellness industry presents new growth opportunities, especially as the global demand for dietary supplements continues to rise, particularly among aging populations.

Advancements in Biotechnology and Sustainable Production Methods

Technological advancements in biotechnology are offering new opportunities for glutamic acid production. Innovations such as fermentation-based methods using microorganisms have made the production of glutamic acid more sustainable, cost-effective, and environmentally friendly.

As these production techniques improve, they can reduce the reliance on chemical methods and provide more eco-conscious solutions. These advancements not only help in meeting the increasing demand but also cater to the growing consumer preference for natural and bio-based ingredients. The shift toward sustainable production is expected to foster long-term growth in the glutamic acid market.

Latest Trends

Increased Use of Natural and Plant-Based Glutamic Acid

There is a growing trend toward the use of natural, plant-based glutamic acid, driven by consumer preferences for clean-label and organic products. This shift is particularly noticeable in the food and beverage industry, where consumers are seeking more natural alternatives to synthetic additives.

Companies are increasingly adopting plant-based fermentation processes to produce glutamic acid, which aligns with the demand for sustainable and non-GMO ingredients. As awareness of plant-based diets rises, this trend is likely to become a dominant force in shaping the glutamic acid market.

Growing Popularity of Glutamic Acid in Health Supplements

The use of glutamic acid in health supplements is becoming a notable trend, especially in the wellness and fitness markets. Glutamic acid, as a key amino acid, plays a crucial role in muscle recovery, metabolic function, and overall health. As the global health and fitness market continues to expand, glutamic acid is increasingly included in sports nutrition products, protein powders, and other dietary supplements.

This trend is expected to grow in line with the rising interest in personal health and fitness, fueling demand for glutamic acid in the nutritional supplement sector.

Expansion of Glutamic Acid Use in Animal Feed

Another emerging trend in the glutamic acid market is its increasing use in animal feed, particularly for poultry and livestock. Glutamic acid helps improve feed quality by enhancing the flavor, nutritional profile, and overall digestibility of animal diets.

As the global demand for animal protein rises with the growing population, the need for efficient and cost-effective animal feed solutions is growing. This trend is opening up new opportunities for glutamic acid suppliers, especially as the livestock industry continues to expand in emerging markets with a rising demand for meat and dairy products.

Regional Analysis

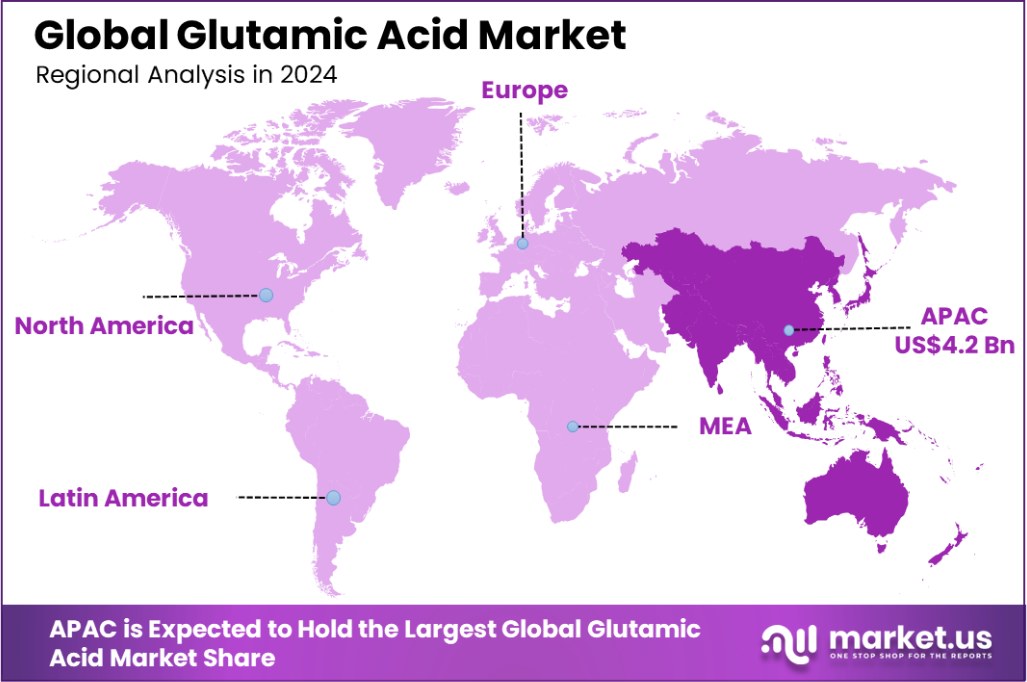

The Asia-Pacific glutamic acid market holds a 43.3% share, valued at USD 4.2 billion.

The Glutamic Acid Market is segmented by region, with Asia-Pacific, North America, Europe, the Middle East & Africa, and Latin America contributing to the global market dynamics.

Asia-Pacific is the dominating region, holding a significant market share of 43.3%, valued at USD 4.2 billion. The region’s dominance can be attributed to the increasing demand for processed foods, the rise of fast food culture, and growing consumer preference for convenience in countries like China, Japan, and India. Additionally, the expansion of the pharmaceutical and animal feed additives sectors further supports the region’s leadership.

North America follows closely, driven by robust demand in the food and beverage industries, particularly in the United States. The market is projected to grow as consumers shift towards savory and processed foods, boosting the need for glutamic acid as a flavor enhancer. North America contributes approximately 25% of the global market share.

Europe holds a notable market position, accounting for around 20% of the global share. The growth is primarily fueled by the increasing use of glutamic acid in the pharmaceutical and food industries, with countries like Germany, France, and the UK leading the market.

Latin America and Middle East & Africa together contribute a smaller share, but both regions are expected to witness steady growth, driven by expanding food processing industries and rising awareness of the benefits of glutamic acid in health supplements and animal feed.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global glutamic acid market in 2023 remains highly competitive, with several key players dominating various market segments. Leading companies such as Ajinomoto Co., Inc., Kyowa Hakko Bio Co., Ltd., and Evonik Industries AG continue to leverage their established brand recognition, robust production capabilities, and expansive distribution networks to maintain market leadership.

Ajinomoto Co., Inc., a pioneer in the production of glutamic acid, continues to hold a significant share, thanks to its long-standing presence and continuous innovation in flavor-enhancing products. The company’s commitment to sustainability and plant-based production methods positions it well in an evolving market that increasingly favors natural ingredients.

Kyowa Hakko Bio Co., Ltd., another major player, is focusing on expanding its glutamic acid portfolio for diverse applications, including pharmaceuticals, nutrition, and animal feed. With a strong emphasis on biotechnology and fermentation processes, the company is well-positioned to cater to the growing demand for bio-based glutamic acid.

Evonik Industries AG continues to strengthen its market position through strategic partnerships and technological advancements in the bioengineering of amino acids. Their expertise in the industrial production of amino acids provides them with a competitive edge, particularly in the Asia-Pacific region, where demand for both industrial and consumer-grade glutamic acid is rising.

Companies like Bachem AG and Global Bio-chem Technology Group Company Limited are increasingly expanding their reach into emerging markets, capitalizing on the growing demand in sectors such as healthcare, animal nutrition, and processed foods. Ningxia EPPEN Bioengineering Stock Co., Ltd. and Sichuan Tongsheng Amino Acid Co., Ltd. are also making strides in China, benefiting from the country’s vast food processing and pharmaceutical industries.

The global glutamic acid market remains diverse, with both established players and emerging companies working to address the growing demand for cost-effective, sustainable, and high-quality glutamic acid solutions.

Top Key Players in the Market

- Ajinomoto Co., Inc.

- Akzo Nobel N.V.

- Bachem AG

- Bio-chem Technology Group Company

- Evonik Industries AG

- Global Bio-chem Technology Group Company Limited

- Iris Biotech GmbH

- Kyowa Hakko Bio Co., Ltd

- Ningxia EPPEN Bioengineering Stock Co., Ltd

- Ottokemi; Hefei TNJ Chemical Industry Co., Ltd.

- Sichuan Tongsheng Amino Acid Co., Ltd

- Suzhou Yuanfang Chemical Co., Ltd.

- Wuhan Amino Acid Bio-Chemical Co., Ltd

- FUFENG GROUP

- AMINO GmbH

- Hefei TNJ Chemical Industry Co., Ltd

- Medinex

- Haihang Industry

Recent Developments

- In 2024, Kyowa Hakko continued to innovate, introducing advanced fermentation processes to enhance production efficiency and sustainability. They also formed strategic partnerships with key food and beverage brands to expand their market presence.

- In 2023, Haihang reported a substantial increase in production volumes, expanding its market presence in the Asia-Pacific region. The company has also forged strategic partnerships with global food manufacturers to enhance its distribution network and cater to the growing demand for glutamic acid in the food and beverage industries.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 9.9 Billion |

| Forecast Revenue (2033) | USD 18.1 Billion |

| CAGR (2024-2033) | 6.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source Type (Plant Based, Animal-Based), By Product (Biosynthesis, Industrial Synthesis), By Function (Plant Growth, NMR Spectroscopy, Nutrient, Flavor Enhancer, Detoxifying Agent, Neurotransmitter, Metabolism, Others), By Type (L-Glutamic Acid, DL-Glutamic Acid), By Manufacturing Process (Fermentation, Chemical Synthesis), By Grade (Food Grade, Pharmaceutical Grade, Feed Grade), By Application (Flavor Enhancer, Nutritional Supplement, Pharmaceutical Ingredient, Animal Feed Additive, Others), By End Use Industry (Food Beverage, Pharmaceuticals, Agriculture, Personal Care, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Ajinomoto Co., Inc., Akzo Nobel N.V., Bachem AG, Bio-chem Technology Group Company, Evonik Industries AG, Global Bio-chem Technology Group Company Limited, Iris Biotech GmbH, Kyowa Hakko Bio Co., Ltd, Ningxia EPPEN Bioengineering Stock Co., Ltd, Ottokemi; Hefei TNJ Chemical Industry Co., Ltd., Sichuan Tongsheng Amino Acid Co., Ltd, Suzhou Yuanfang Chemical Co., Ltd., Wuhan Amino Acid Bio-Chemical Co., Ltd, FUFENG GROUP, AMINO GmbH, Hefei TNJ Chemical Industry Co., Ltd, Medinex, Haihang Industry |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |