Quick Navigation

Report Overview

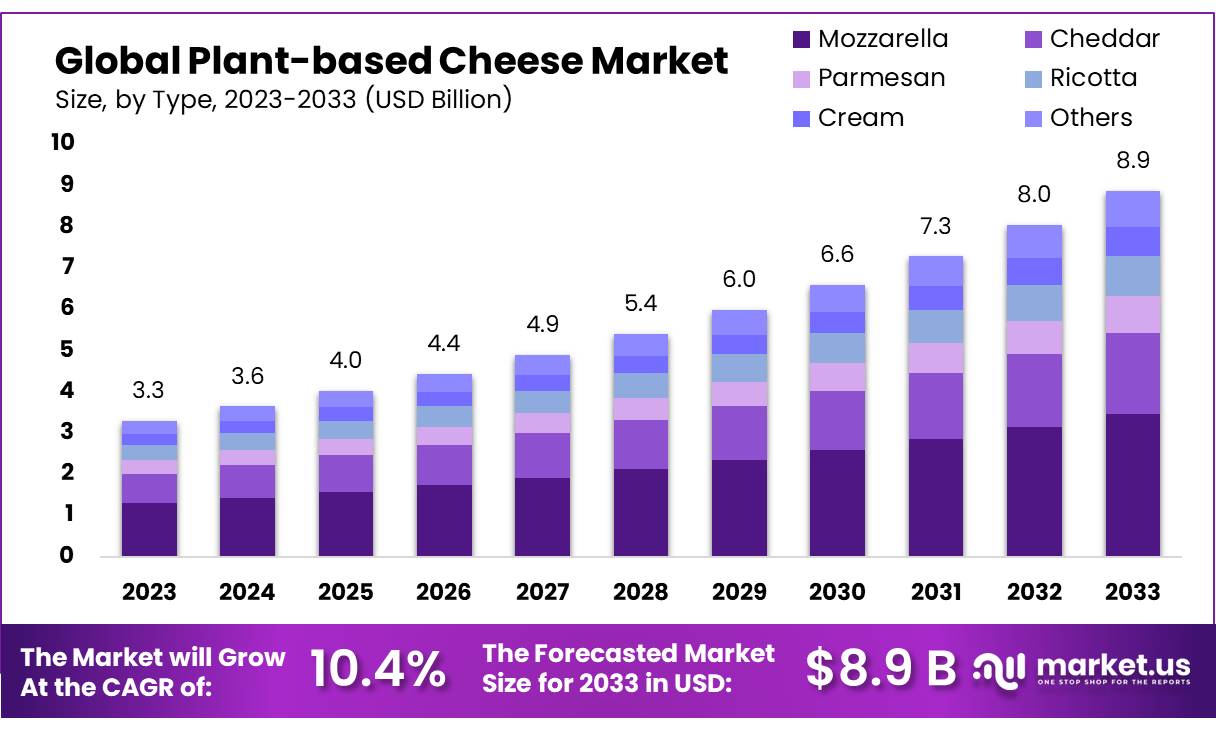

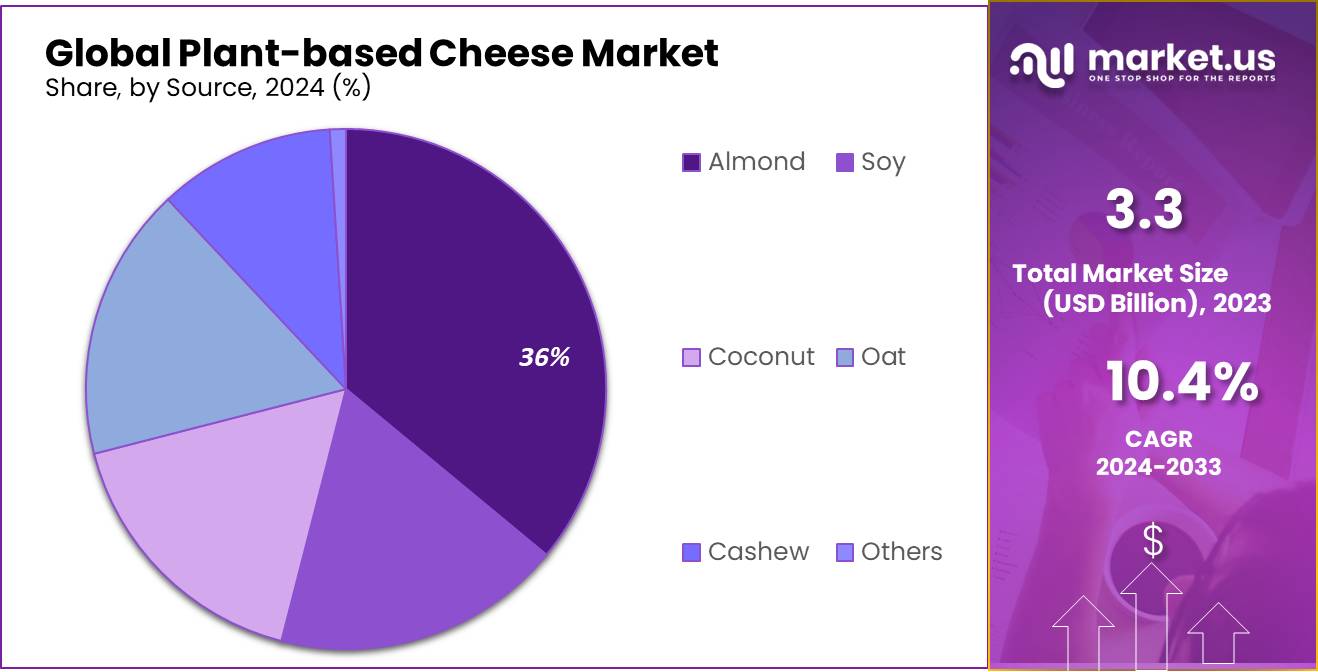

The Global Plant-based Cheese Market size is expected to be worth around USD 8.9 Bn by 2033, from USD 3.3 Bn in 2023, growing at a CAGR of 10.4% from 2024 to 2033.

Plant-based cheeses (PBC) made from nuts are rapidly gaining prominence as versatile dairy-free alternatives tailored to vegetarian and vegan diets. These products are crafted using plant-based ingredients, particularly nuts, and are marketed as suitable options for individuals with dietary restrictions or preferences. The preparation process typically involves blending or liquefying nuts, providing a base for further processing to mimic traditional cheese characteristics.

In the case of fermented PBC products, lactic acid bacteria (LAB) are used during fermentation to develop textures, flavors, and shapes similar to conventional cheeses. These are often formed into spreads or solid cheese-like forms. Non-fermented spreads or dips, on the other hand, are refrigerated immediately after preparation to maintain freshness, highlighting their perishable nature and shorter shelf life.

The demand for PBC is fueled by growing health awareness and dietary shifts. Approximately 65% of the global population experiences lactose intolerance, making dairy-free alternatives like PBC an attractive option. Additionally, the environmental footprint of dairy production is a concern for many consumers. Studies indicate that the production of plant-based cheese requires 50-70% less water and emits fewer greenhouse gases compared to dairy cheese. These factors resonate strongly with environmentally conscious consumers.

The increasing adoption of veganism and flexitarian diets further bolsters demand. In the United States, the number of consumers identifying as vegan or vegetarian doubled over the past decade, reaching 10% of the population in 2023. This shift reflects a broader movement toward plant-based foods, driven by health benefits, ethical considerations, and sustainability concerns.

Foodservice industry is a driver of plant-based cheese adoption. Vegan-friendly restaurants and fast-food chains have integrated PBC into their offerings, especially in menu items like pizzas, burgers, and pasta. For instance, global chains such as Domino’s and Pizza Hut introduced vegan cheese options in over 20 countries by 2023.

The retail segment, including supermarkets and specialty stores, accounts for 65-70% of total PBC sales. Simultaneously, e-commerce channels are emerging as critical distribution platforms, especially in regions where traditional retail infrastructure is limited. Online sales of PBC grew by 18% year-over-year in 2023, driven by increased digital penetration and convenience-seeking consumers.

The food technology are pivotal in addressing the taste and texture challenges of plant-based cheeses. Improved melting and stretching properties have been achieved, making PBC viable for culinary applications such as baked dishes. The rise of clean-label products, featuring organic, non-GMO, and allergen-free certifications, is shaping purchasing decisions. Soy-free and gluten-free PBC varieties complement nut-based options, catering to a broader consumer base.

Nut-based PBC, while appealing, differ nutritionally from dairy cheeses. Cashew-based PBC contains approximately 11% protein, while coconut-based varieties have lower protein levels, ranging from 0.11% to 0.6%. In comparison, dairy cheeses contain 10-2

% protein, highlighting a key area for nutritional enhancement in PBC.

The future of the PBC market lies in product diversification and expanded market reach. Foodservice establishments, including vegan-friendly restaurants, offer growth potential. Additionally, emerging markets in Asia-Pacific, where lactose intolerance rates exceed 90%, present untapped opportunities. Investment in targeted marketing campaigns emphasizing health and sustainability benefits, coupled with partnerships in the foodservice and retail sectors, will likely propel market expansion.

Key Takeaways

- Plant-based Cheese Market size is expected to be worth around USD 8.9 Bn by 2033, from USD 3.3 Bn in 2023, growing at a CAGR of 10.4%.

- Mozzarella segment held a dominant position in the plant-based cheese market, securing over a 39.1% share.

- almond-based cheeses held a dominant position in the plant-based cheese market, capturing more than a 36.1% share.

- unflavored segment held a dominant position in the plant-based cheese market, capturing more than a 63.2% share.

- shreds held a dominant market position in the plant-based cheese market, capturing more than a 38.1% share.

- sales of plant-based cheeses through hypermarkets and supermarkets held a dominant market position, capturing more than a 45.2% share.

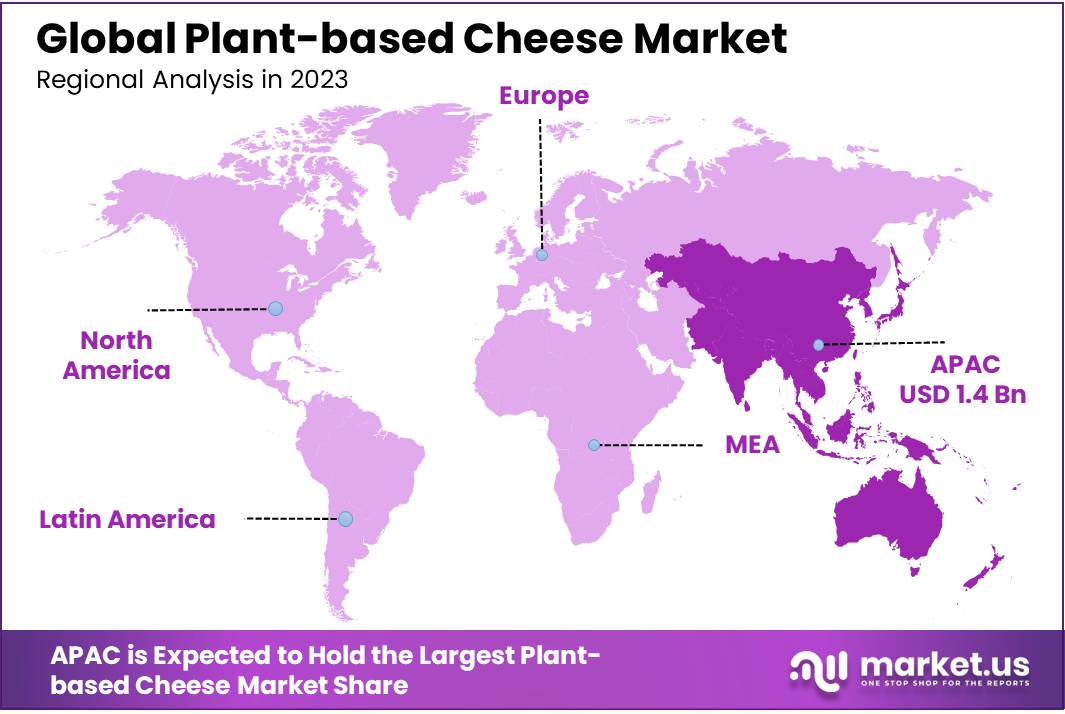

- Asia Pacific (APAC) is currently the dominating region, capturing a 45.3% market share, valued at approximately USD 1.4 billion.

By Type

In 2023, the Mozzarella segment held a dominant position in the plant-based cheese market, securing over a 39.1% share. This popularity can be attributed to mozzarella’s versatility in various culinary applications, especially in vegan pizzas and salads, which resonate well with consumers seeking dairy-free alternatives.

Cheddar followed closely, known for its qrich flavor and smooth texture that appeals to those looking for a hearty addition to sandwiches and burgers. The demand for plant-based cheddar has been steadily increasing as it offers a comforting taste similar to traditional cheddar without the use of animal products.

The Parmesan segment also carved out a niche, particularly among vegan and health-conscious consumers who desire a sprinkle of rich, nutty flavor over their pasta and risottos. Its granular texture and robust taste make it a favorite for those looking to enhance their meals with a guilt-free, sustainable option.

Ricotta’s share in the plant-based cheese market has grown to its light and creamy consistency, making it ideal for vegan versions of classic Italian dishes like lasagna and cannoli. Its adaptability in both sweet and savory recipes has helped it gain traction among a broad audience.

The Cream segment witnessed a surge in interest from consumers looking for lush, spreadable alternatives to dairy-based creams. Plant-based cream cheeses are increasingly popular in baking and as spreads, catering to the expanding vegan breakfast and snack market.

By Source

In 2023, almond-based cheeses held a dominant position in the plant-based cheese market, capturing more than a 36.1% share. This popularity is largely to the creamy texture and mild, versatile flavor of almond cheese, making it a favorite in both cooking and as a snack. It’s particularly well-received by those looking for a healthier alternative that doesn’t compromise on taste or texture.

Soy-based cheese also claimed a portion of the market. Known for its protein-rich profile, soy cheese caters to consumers prioritizing nutritional content. It’s widely used in various culinary styles, from sandwiches to ethnic dishes, appealing to a broad audience seeking dairy-free options.

Coconut cheese emerged as another preferred choice, appreciated for its slightly sweet flavor and smooth consistency. It’s an ideal ingredient in desserts and exotic dishes, offering a unique taste that stands out in the vegan cheese category.

Oat-based cheese is gaining traction for its environmental benefits and hypoallergenic properties. As more consumers become aware of oats’ sustainability and gentle nature on the stomach, its adoption in plant-based cheese formulations has been rising.

Cashew cheese boasts a rich, buttery flavor, making it popular among gourmet vegan cheese lovers. It is perfect for spreads, dips, and as a decadent topping on pizzas and pastas, providing a luxurious feel to everyday meals.

By Formulation

In 2023, the unflavored segment held a dominant position in the plant-based cheese market, capturing more than a 63.2% share. This preference is largely to the versatility of unflavored plant-based cheese, which can seamlessly substitute for traditional cheese in various recipes without altering the original flavors of dishes. Consumers appreciate the subtlety it offers, making it ideal for both cooking and direct consumption.

Flavored plant-based cheeses have carved out a substantial niche for themselves. These products cater to consumers looking for an adventurous taste experience and those who miss the specific flavors of traditional dairy cheeses. Varieties infused with herbs, spices, or even truffle offer a gourmet experience and are particularly popular in specialty dishes where cheese is the star ingredient.

By Form

In 2023, shreds held a dominant market position in the plant-based cheese market, capturing more than a 38.1% share. The convenience of shredded cheese, especially for culinary uses like topping pizzas, salads, and tacos, drives its popularity. It melts well and blends seamlessly into dishes, making it a favorite for both home cooks and professional kitchens seeking vegan options.

Blocks of plant-based cheese also maintain a presence in the market. These are appreciated by consumers who prefer to slice or grate their cheese fresh, depending on the usage. Blocks are versatile for both cold and cooked dishes, providing a solid texture that mimics traditional cheese.

Cubes are another form that appeals particularly to those looking for ready-to-eat snack options or ingredients that are easy to toss into salads. Their practicality for portion control also makes them a popular choice in the hospitality industry, such as in buffets and catering services.

Slices of plant-based cheese cater specifically to the sandwich and burger markets, where convenience and uniformity in portion size are crucial. They provide a quick, consistent way to enjoy cheese without the fuss of cutting or grating, ideal for fast-paced environments or simple at-home meal preparations.

By Distribution Channel

In 2023, sales of plant-based cheeses through hypermarkets and supermarkets held a dominant market position, capturing more than a 45.2% share. This channel’s success stems from its ability to offer a wide variety of plant-based cheese options under one roof, catering to the convenience of consumers looking to compare and purchase multiple products during their regular shopping trips. The visibility and accessibility of these products in large retail settings have contributed to their popularity.

Convenience stores also play a crucial role, especially for consumers seeking quick and easy access to plant-based cheeses. These outlets are ideal for on-the-go purchases and typically stock a smaller, select range of products catering to immediate neighborhood demand.

Specialty stores have carved out a niche by offering unique and gourmet plant-based cheese varieties that are sometimes not available in larger supermarkets. These stores often focus on high-quality, artisanal products, attracting a segment of consumers particularly interested in the distinct flavors and origins of plant-based cheeses.

Food and drink specialty stores, including those that focus specifically on vegan and vegetarian products, offer a curated selection that appeals to dietary-specific shoppers. These outlets provide expert advice and a tailored shopping experience, which is highly valued by consumers who are new to plant-based diets or looking to expand their culinary horizons.

Independent small groceries serve localized markets where larger chains may not reach. They often cater to specific community preferences and provide a personal touch, which can be important for consumers who value a closer connection with their food sources.

Online retail has shown growth, particularly appreciated for its convenience and the broader accessibility it offers. Consumers can shop from a wide array of plant-based cheese products from across the country or even internationally, enjoying direct-to-door delivery that fits busy lifestyles.

Key Market Segments

By Type

- Mozzarella

- Cheddar

- Parmesan

- Ricotta

- Cream

- Others

By Source

- Almond

- Soy

- Coconut

- Oat

- Cashew

- Others

By Formulation

- Flavored

- Unflavored

By Form

- Block

- Cubes

- Shreds

- Slice

- Others

By Distribution Channel

- Hypermarkets/Supermarkets

- Convenience Stores

- Specialty Stores

- Food & Drink Specialty Stores

- Independent Small Groceries

- Online Retail

- Others

Drivers

Growing Health Awareness and Dietary Shifts

One of the primary driving factors for the surge in the plant-based cheese market is the increasing health awareness among consumers worldwide. As people become more conscious of their dietary choices and their impacts on health and the environment, many are shifting towards plant-based diets. A number of consumers are reducing their dairy intake to lactose intolerance, dairy allergies, or the high cholesterol content in traditional cheese. Plant-based cheeses offer a viable alternative, providing similar textures and flavors without the associated health concerns of dairy.

According to the United Nations Food and Agriculture Organization (FAO), the demand for dairy alternatives is not just a trend but part of a broader movement towards plant-based diets, influenced by health, environmental, and ethical considerations. The FAO notes that plant-based diets can lead to lower rates of non-communicable diseases such as heart conditions, obesity, and type 2 diabetes. This endorsement by a major international body highlights the shift in consumer behavior towards healthier eating practices and supports the growth of the plant-based cheese market.

Governments around the world are also supporting this shift through various initiatives. For instance, Canada’s updated food guide recommends choosing protein foods that come from plants more often. This governmental endorsement of plant-based proteins indirectly boosts the market for plant-based cheeses as consumers look for dairy alternatives that fit the recommended dietary patterns. Such initiatives underscore the changing perception of what constitutes a healthy diet and help drive the adoption of plant-based cheese alternatives.

Moreover, environmental concerns play a crucial role in this dietary shift. The production of plant-based cheeses generally requires less water and results in lower greenhouse gas emissions compared to traditional dairy farming. This is in the context of global efforts to combat climate change. For example, a report by the Intergovernmental Panel on Climate Change (IPCC) suggests that shifting towards more plant-based diets could help mitigate climate change by reducing emissions from food production. Consumers aware of these facts are increasingly opting for plant-based cheeses as part of their contribution to environmental sustainability.

In addition, technological advancements in food processing have enabled manufacturers to improve the texture and taste of plant-based cheeses, making them more appealing to a broader audience. Innovations in food science are continually enhancing the palatability and variety of plant-based cheeses, which now include options that mimic mozzarella, cheddar, and even gourmet cheeses like camembert and gouda. These improvements are crucial in winning over consumers who might have been hesitant to taste or texture differences in earlier products.

Another supportive factor is the increasing availability and visibility of plant-based cheeses in mainstream retail channels. Supermarkets and grocery stores are expanding their dairy-free assortments in response to consumer demand, making these products more accessible to the average shopper. Online retail platforms also contribute to this trend by offering a wider range of plant-based cheese products, often accompanied by customer reviews that help new consumers navigate their choices.

Restraints

Sensory Differences and Consumer Acceptance

A major restraining factor in the growth of the plant-based cheese market is the sensory difference between plant-based and traditional dairy cheeses. Many consumers, particularly those who are not vegan or lactose intolerant, find that while plant-based cheeses can mimic the basic appearance and texture of dairy cheese, they often fall short in terms of taste, meltability, and mouthfeel. This sensory gap can discourage repeat purchases among new adopters who expect a direct substitute for dairy-based products.

Surveys from food industry analysts suggest that the flavor profile of plant-based cheeses is often the most critical barrier for consumers. While improvements have been made, achieving the rich, creamy taste of cheese made from cow’s milk remains challenging. Plant-based cheeses sometimes possess a nutty or artificial aftertaste, which can be off-putting to those accustomed to the flavor of traditional cheeses. According to a consumer survey by the Plant-Based Foods Association, over 30% of participants cited taste as the reason for their reluctance to switch to plant-based cheeses.

Texture is another area where plant-based cheeses often do not measure up. Dairy cheese has a unique ability to melt and stretch, a quality that is crucial in dishes like pizza and grilled cheese sandwiches. Although plant-based alternatives have evolved, many still do not offer the same melting qualities, which limits their use in cooking. A report by the Food and Agriculture Organization noted that texture mismatches are a hurdle in consumer acceptance of plant-based dairy alternatives.

Despite these challenges, the industry is making concerted efforts to bridge these gaps through food science and technology. Innovations in enzymatic treatments, protein isolates, and emulsification techniques have led to better textural properties and flavor profiles in plant-based cheeses. These advancements are crucial as they directly address consumer demands for better-tasting and more versatile products.

Price also plays a role in restraining the market growth of plant-based cheeses. Generally, they are more expensive than their dairy counterparts, which can be a deterrent for budget-conscious consumers. The higher price point is often to the complex manufacturing processes involved and the use of premium ingredients, such as cashews or almonds. Economic analyses from food industry reports indicate that the price of plant-based cheeses can be up to twice that of regular cheese, which makes them less accessible to a broader audience.

Awareness and availability are additional factors that can limit market growth. In some regions, consumers may not be as aware of plant-based cheeses, or these products may not be readily available in local stores. This lack of exposure means that many potential customers are simply not able to try these alternatives, thereby slowing market penetration.

Government initiatives aimed at promoting healthier diets and reducing animal agriculture’s environmental impact could support the plant-based cheese market. For example, the European Union’s Farm to Fork Strategy aims to make food systems fair, healthy, and environmentally-friendly, which includes supporting sustainable food production like plant-based products. These policies can help increase consumer awareness and acceptance of plant-based cheeses by emphasizing their health and environmental benefits.

Opportunity

Expansion into Emerging Markets

One of the most promising growth opportunities for the plant-based cheese market is its expansion into emerging markets. As global awareness of health, ethical, and environmental issues grows, so does the interest in plant-based diets, including in regions where dairy consumption has traditionally been low to cultural, economic, or dietary reasons.

In regions such as Asia and Latin America, lactose intolerance is prevalent, affecting a large percentage of the population. This physiological challenge presents a opportunity for plant-based cheese products as alternatives to dairy-based cheeses. Offering a lactose-free cheese alternative not only caters to this demographic’s dietary needs but also aligns with growing health-conscious trends globally.

These emerging markets are experiencing rapid urbanization and economic growth, which are contributing to changes in consumer lifestyles and dietary patterns. Middle-class consumers in these regions are increasingly exposed to global cuisines and are more open to trying new food products, including vegan and vegetarian options. The rising spending power in these economies also makes it feasible for consumers to explore premium and health-oriented food choices such as plant-based cheeses.

Governmental support for sustainable and health-promoting food options is another factor driving the growth of plant-based cheeses in these markets. For instance, countries like China and India have introduced national dietary guidelines that encourage the consumption of plant-based foods to improve public health outcomes and reduce the environmental impact of their food systems. These policies not only raise awareness but also foster a favorable environment for the growth of the plant-based food sector, including plant-based cheeses.

The increase in international travel and the global exchange of cultural practices also play roles in the spread of dietary trends. As people travel more and share their eating habits and preferences, the demand for diverse and adaptable food products, such as plant-based cheeses, rises. This global exchange is especially potent in emerging markets, where international influences are strong and growing.

The technological advancements in food processing and flavor enhancement are making plant-based cheeses more appealing to a broader audience. Innovations that improve taste, texture, and melting properties can make these products indistinguishable from their dairy counterparts, thus overcoming one of the major barriers to adoption.

Trends

Gourmet and Artisanal Plant-Based Cheeses

One of the latest trends in the plant-based cheese market is the rise of gourmet and artisanal products, which are elevating the perception and culinary applications of vegan cheeses. This trend is driven by consumer demand for higher-quality, more sophisticated alternatives that not only mimic traditional dairy cheeses in functionality but also in the richness of flavor and variety.

The emergence of gourmet plant-based cheeses is a response to the maturing palate of vegan and lactose-intolerant consumers who are looking for more than just a dietary substitute; they seek a culinary experience that rivals that of traditional cheese. These artisanal products often incorporate complex aging processes, natural fermentation, and the use of various nuts and plant-based milks, which help develop deeper flavors and more authentic textures.

According to a survey from the Vegan Society, there has been a increase in interest in plant-based diets, with the number of vegans in many Western countries doubling over the past few years. This shift is not just about avoiding animal products; it’s about embracing a plant-based lifestyle, which includes enjoying high-quality, delicious foods. Artisanal plant-based cheeses meet this demand by providing a luxury experience that appeals to both vegans and non-vegans alike.

The gourmet trend is also being supported by several high-profile chefs and restaurants, which have started to incorporate vegan cheeses into their menus. These culinary professionals are exploring the potential of these cheeses in fine dining, using them in sophisticated dishes and pairing them with wines, which traditionally would have called for dairy-based cheeses. This not only broadens the appeal of plant-based cheeses but also helps in changing consumer perceptions about vegan food being a compromise in taste or variety.

Moreover, government initiatives that promote healthy eating and environmental sustainability are indirectly supporting this trend. For example, the European Union’s strategies on sustainable food systems encourage the development of food products that are both health-friendly and environmentally friendly. Gourmet plant-based cheeses, which are often made from organic and locally sourced ingredients, align well with these policies.

Another important aspect of this trend is the use of traditional cheese-making techniques adapted for plant-based ingredients. Manufacturers are investing in research and development to craft cheeses that feature the ripening and textural qualities of traditional cheeses. This approach not only improves the sensory quality of plant-based cheeses but also increases their appeal among traditional cheese lovers.

Regional Analysis

In the plant-based cheese market, regional dynamics influence market growth and consumer preferences. Asia Pacific (APAC) is currently the dominating region, capturing a 45.3% market share, valued at approximately USD 1.4 billion. This dominance is largely driven by increasing lactose intolerance among the population, growing health consciousness, and rising veganism in countries like China, India, and Australia. The regional market benefits from a strong tradition of dairy-free diets and a vast consumer base seeking plant-based alternatives.

In North America, the market is propelled by a robust wellness culture and heightened awareness regarding animal welfare, which encourage the adoption of vegan and plant-based diets. The United States and Canada are seeing a surge in demand for plant-based cheese products in both retail and food service sectors, supported by innovative product offerings from key market players.

Europe also presents a growth opportunity for plant-based cheese, backed by stringent environmental regulations and government initiatives promoting sustainable agriculture. Countries like Germany, the UK, and France are leading in terms of consumer acceptance and product availability, driven by a well-established vegan community and strong ethical movements towards plant-based eating.

The Middle East & Africa and Latin America are emerging markets with potential for growth. Increasing urbanization, rising disposable incomes, and the gradual introduction of Western eating habits contribute to the rising demand for plant-based cheese. Although these regions currently hold smaller shares of the global market, their growth is expected to accelerate as awareness and availability of plant-based products increase.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The plant-based cheese market is characterized by a diverse array of key players, each contributing to the sector’s growth with innovative products and broad distribution networks. Companies like Daiya Foods Inc. and Miyoko’s Kitchen, Inc. are pioneers in the industry, known for their wide range of cheese alternatives that cater to various consumer preferences for taste, texture, and culinary use. Daiya’s offerings are particularly noted for their melting qualities, making them a favorite for vegan pizzas and casseroles, while Miyoko’s Kitchen brings artisanal flair to the market with gourmet cashew-based cheeses.

Danone S.A. and Kraft Heinz Company have also ventured into the plant-based cheese sector, leveraging their extensive distribution channels and brand recognition to capture market share. Danone, traditionally known for its dairy products, has embraced plant-based alternatives as part of its broader commitment to sustainability and health, offering a variety of non-dairy cheese products under its various brand umbrellas. Kraft Heinz entered the market with vegan versions of their classic cheese slices, targeting both health-conscious consumers and those with dietary restrictions.

Kite Hill and Field Roast are making notable strides in refining the sensory aspects of vegan cheese, focusing on achieving the authentic taste and texture that can compete with traditional dairy cheeses. These brands, along with others like Bute Island Foods Ltd. and Galaxy Nutritional Foods, Inc., emphasize the use of high-quality, natural ingredients to appeal to a market segment that values both ethical consumption and gourmet food experiences. As the demand for plant-based products continues to grow, these companies are poised to expand their presence and influence in the global market, driven by consumer trends toward healthier, sustainable choices.

Top Key Players

- Bute Island Foods Ltd.

- Daiya Foods Inc.

- Danone S.A.

- Farmstead

- Field Roast

- Galaxy Nutritional Foods, Inc.

- GreenSpace Brands

- Kinda Co.

- Kite Hill

- Kraft Heinz Company

- Mad Millie

- Miyoko’s Kitchen, Inc.

- Parmela Creamery

- Punk Rawk Labs

- Puris Foods

- Regal Vegan

- Reine Vegan Cuisine

- Tesco Free From

- The Gardener Cheese Company Inc.

- UPrise Foods

- Vermont

- WayFare Foods

Recent Developments

In 2024, Bute Island Foods undertook a rebranding to enhance its market presence, introducing a new logo and packaging designed to improve shelf visibility and appeal.

In 2023, Daiya made advancements by investing millions into fermentation technology, which aims to improve the taste, texture, and meltability of its cheese alternatives.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 3.3 Bn |

| Forecast Revenue (2033) | USD 8.9 Bn |

| CAGR (2024-2033) | 10.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Mozzarella, Cheddar, Parmesan, Ricotta, Cream, Others), By Source (Almond, Soy, Coconut, Oat, Cashew, Others), By Formulation (Flavored, Unflavored), By Form (Block, Cubes, Shreds, Slice, Others), By Distribution Channel (Hypermarkets/Supermarkets, Convenience Stores, Specialty Stores, Food and Drink Specialty Stores, Independent Small Groceries, Online Retail, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Bute Island Foods Ltd., Daiya Foods Inc., Danone S.A., Farmstead, Field Roast, Galaxy Nutritional Foods, Inc., GreenSpace Brands, Kinda Co., Kite Hill, Kraft Heinz Company, Mad Millie, Miyoko’s Kitchen, Inc., Parmela Creamery, Punk Rawk Labs, Puris Foods, Regal Vegan, Reine Vegan Cuisine, Tesco Free From, The Gardener Cheese Company Inc., UPrise Foods, Vermont, WayFare Foods |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |