Quick Navigation

Report Overview

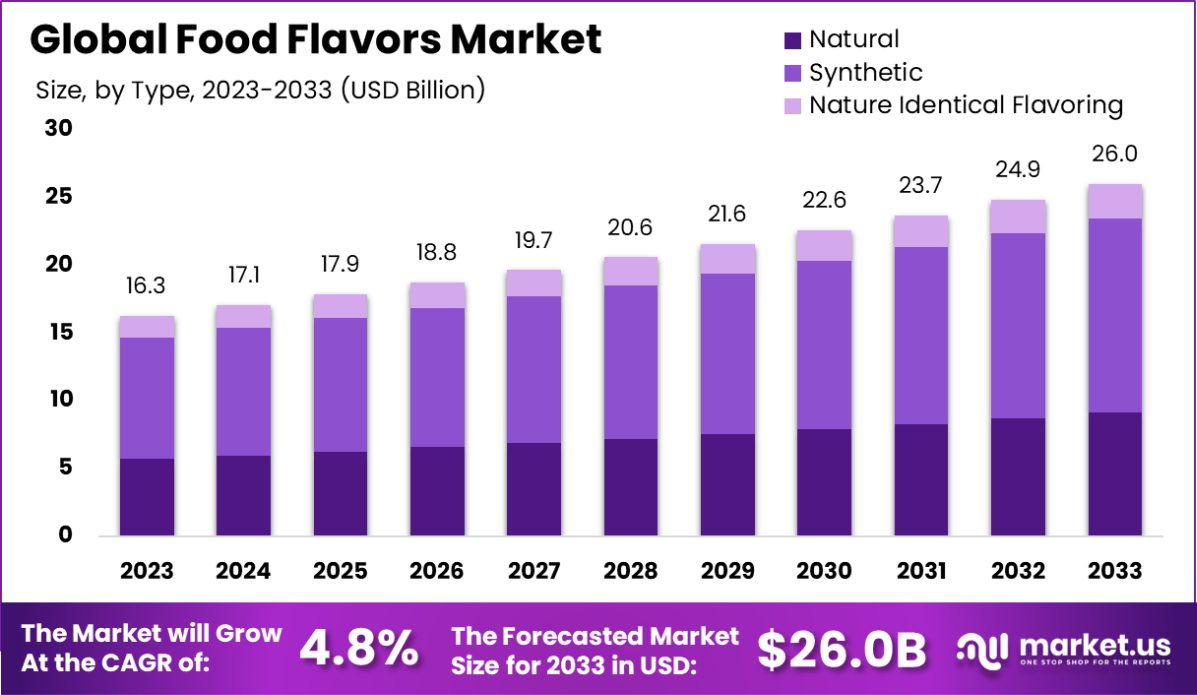

The Global Food Flavors Market is expected to be worth around USD 26.0 Billion by 2033, up from USD 16.3 Billion in 2023, and grow at a CAGR of 4.8% from 2024 to 2033. Asia-Pacific Food Flavors Market: 36.6% share, USD 5.9 billion.

Food flavors are additives used to enhance the taste and aroma of food products. They can be derived from natural sources like plants and animals or synthesized chemically. These flavors are crucial in making food products more appealing and can be found in a variety of forms such as liquid, powder, and paste.

The food flavors market is a sector within the food and beverage industry focused on the development, production, and distribution of flavoring agents. This market caters to a wide range of applications including processed foods, beverages, dairy products, and confectioneries. Growth in this market is driven by consumer demand for new and exotic flavors, increased consumption of processed foods, and technological advancements in flavor extraction and synthesis.

The demand for clean label products and natural flavors is a significant growth driver in the food flavors market. Consumers increasingly prefer foods with natural ingredients and transparent labeling, pushing manufacturers to innovate with natural flavorings sourced from fruits, vegetables, and herbs.

The rising global consumption of convenience foods and ready-to-eat products boosts the demand for food flavors. As lifestyles become busier, consumers seek quick meal solutions that do not compromise on taste, leading to greater use of flavors in food processing.

Emerging markets offer substantial opportunities for the food flavors industry due to changing dietary patterns and growing middle-class populations. These regions are witnessing a shift towards Westernized diets, creating new avenues for flavor manufacturers to introduce diversified and culturally adapted flavor products.

The Food Flavors Market in India presents a dynamic growth opportunity, underscored by robust import figures and significant contributions to the national economy. In 2023, India’s imports of consumer-oriented foods, including food flavors, reached an impressive $7 billion from January to November, with the United States accounting for 15% of these imports.

This trend is indicative of the increasing globalization of taste preferences among Indian consumers and the growing acceptance of international cuisines and flavors.

Further bolstering the market’s potential is the pivotal role of the food processing industry in India’s economic landscape. Contributing nearly 13% to the country’s Gross Domestic Product, the industry is a critical component of India’s economic framework, enhancing the demand for innovative and high-quality food flavors. Additionally, consumer spending patterns provide further insights into market opportunities.

In 2023, expenditures on food accounted for 35-40% of total consumer spending in India. This substantial portion reflects the importance of food consumption in the daily lives of Indian consumers and underscores the expansive potential for market penetration and growth by food flavor manufacturers.

Strategically, companies in the food flavors sector should consider these metrics to tailor their market entry and expansion strategies. The data suggests a robust market receptivity and an evolving palate among Indian consumers, which are ripe for the introduction of diverse and innovative flavor offerings.

Harnessing this potential will require a keen understanding of local tastes and preferences, coupled with an agile approach to product development and marketing strategies.

Key Takeaways

- The Global Food Flavors Market is expected to be worth around USD 26.0 Billion by 2033, up from USD 16.3 Billion in 2023, and grow at a CAGR of 4.8% from 2024 to 2033.

- Synthetic food flavors dominate the market with a significant share of 55.6%.

- Powdered forms lead in food flavor applications, constituting 65.6% of the market.

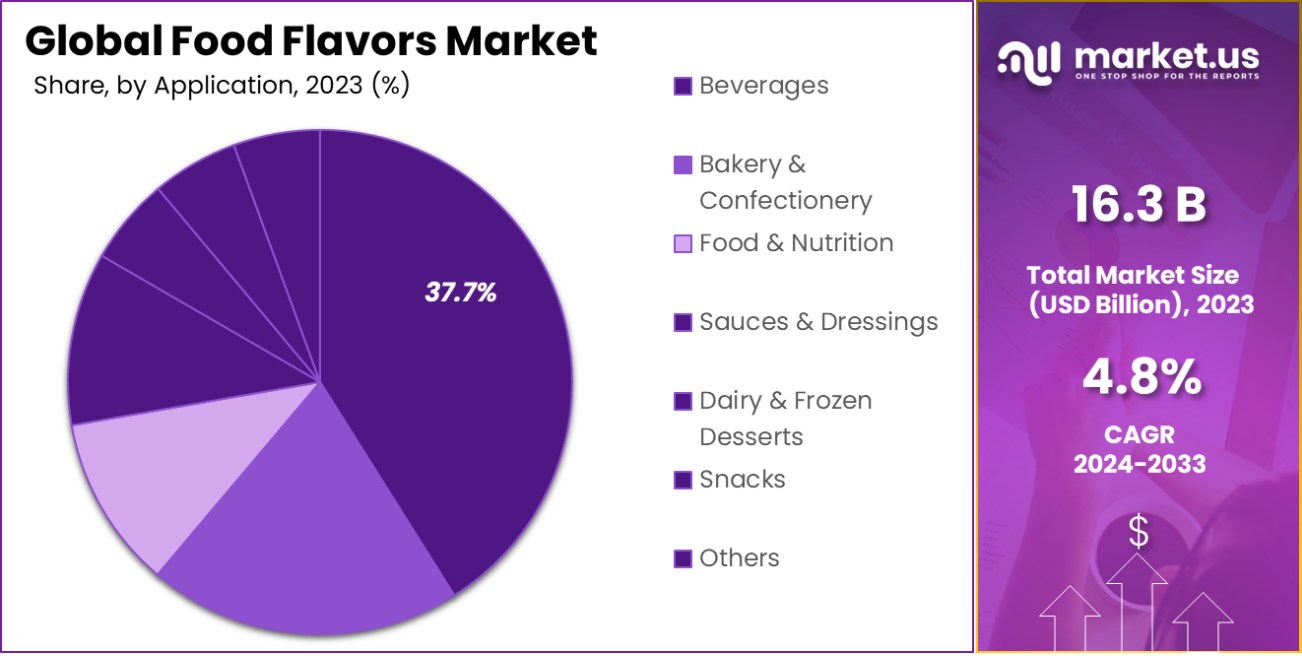

- Beverages are a major application segment for food flavors, holding a 37.7% share.

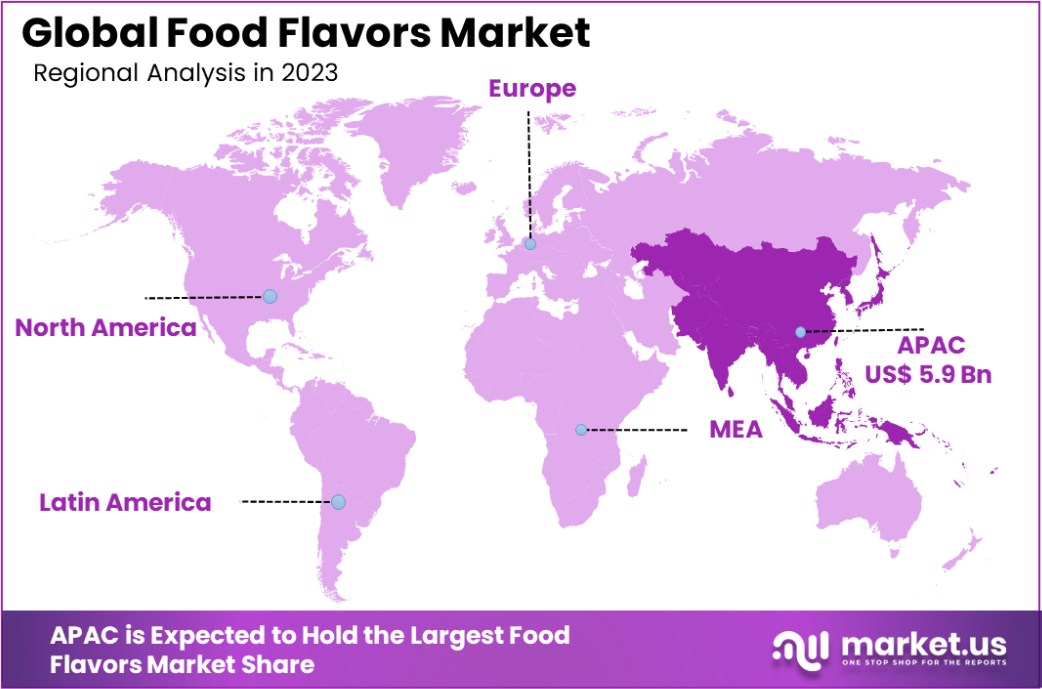

- In 2023, Asia-Pacific dominated the Food Flavors Market with 36.6%, reaching USD 5.9 billion.

Strategic Business Review of Food Flavors

A strategic business review of the food flavors industry reveals its integral role in enhancing consumer products across a multitude of sectors including beverages, dairy, confectionery, and bakery.

As taste continues to be a paramount driver of consumer preference, the demand for innovative and authentic flavor profiles is on the rise. This demand is not only driven by the pursuit of sensory enhancement but also by the growing consumer inclination towards health-conscious and ethically sourced products.

The industry is witnessing a shift towards natural and organic flavors, spurred by the global health trend and regulatory support. Companies are investing in research and development to create complex flavor profiles that can replicate traditional tastes using natural sources. This includes botanical extracts and essential oils, which are gaining popularity due to their perceived health benefits and sustainability.

Additionally, technological advancements such as flavor encapsulation and microencapsulation are playing a crucial role in extending the shelf life and stability of flavors, thus enabling their use in a wider range of products. The use of artificial intelligence and machine learning in flavor development is also emerging as a significant trend, offering new opportunities for personalization and innovation in flavor creation.

In response to global economic dynamics and evolving consumer tastes, companies are also focusing on strategic expansions and collaborations to enhance their global footprint and product offerings. This approach is crucial in maintaining competitiveness and meeting the diverse taste preferences of a global audience.

By Type Analysis

Synthetic flavors dominate the Food Flavors Market, holding a significant share of 55.6%.

In 2023, Synthetic held a dominant market position in the “By Type” segment of the Food Flavors Market, with a 55.6% share. The Synthetic type is favored for its consistent quality and ability to replicate a wide range of flavors.

Following Synthetic, the Natural segment accounted for 30.2% of the market. Consumers’ growing preference for products with natural ingredients, driven by health consciousness and clean label trends, supports this segment’s substantial market share.

Meanwhile, Nature Identical Flavoring, which combines elements of both synthetic and natural flavors, captured 14.2% of the market. This segment appeals to manufacturers looking for cost-effective solutions that still meet consumer demands for authenticity and safety in flavor profiles.

Overall, the Food Flavors Market is influenced by a blend of consumer preferences for naturalness and innovation in flavor technologies. As the market evolves, the interplay between these segments is expected to shift, with natural and nature-identical flavors potentially gaining ground due to increasing consumer scrutiny regarding ingredient sourcing and manufacturing processes.

By Form Analysis

Powdered forms are most prevalent in the Food Flavors Market, accounting for 65.6% of the market.

In 2023, Powder held a dominant market position in the “By Form” segment of the Food Flavors Market, with a 65.6% share. Powdered flavors are highly sought after for their long shelf life and ease of storage, making them ideal for use in dry mixes, baking goods, and spice blends.

The remaining market share was captured by Liquid flavors, which accounted for 34.4%. Liquid forms are preferred in beverage applications, dairy products, and confectioneries due to their superior ability to blend seamlessly into the base product, offering consistency in taste and distribution.

The preference for Powder over Liquid can be attributed to the versatility and economic advantages it provides to manufacturers. Powder flavors are easier to handle during the manufacturing process and reduce transportation costs because of their lighter weight and compact nature.

However, the demand for Liquid flavors is also significant, driven by their effectiveness in applications where a homogenous blend is critical. As the market progresses, innovations in flavor encapsulation and delivery technologies are likely to enhance the appeal and functional properties of both forms, potentially altering their current market shares.

By Application Analysis

In the Food Flavors Market, beverages are a leading application area, representing 37.7% of the market.

In 2023, Beverages held a dominant market position in the “By Application” segment of the Food Flavors Market, with a 37.7% share. The demand in this category is primarily driven by the proliferation of new beverage launches, including energy drinks, and health-oriented and functional beverages, which frequently leverage innovative and exotic flavor profiles.

Following Beverages, the Snacks segment accounted for 21.5% of the market, buoyed by consumer preferences for flavorful and diverse snack options. Bakery and Confectionery claimed 15.3%, where flavors play a crucial role in differentiating products on crowded store shelves.

Dairy and Frozen Desserts and Sauces and Dressings captured 12.8% and 8.4% respectively. These segments benefit from the continual introduction of new flavors that cater to changing consumer tastes and the rising trend of at-home cooking and baking. Food and Nutrition, which includes staples and nutritional products, held the smallest share at 4.3%, reflecting a more conservative application of flavoring compared to more indulgent categories.

As beverage companies continue to innovate with healthy and indulgent options, the flavor market in this segment is expected to maintain its lead, fueled by consumer demand for new sensory experiences and cleaner labels.

Key Market Segments

By Type

- Natural

- Synthetic

- Nature Identical Flavoring

By Form

- Powder

- Liquid

By Application

- Food & Nutrition

- Bakery & Confectionery

- Beverages

- Sauces & Dressings

- Dairy & Frozen Desserts

- Snacks

- Others

Driving Factors

Rising Consumer Demand for Clean Label Products

Consumers are increasingly seeking transparency in their food purchases, opting for products that contain natural and understandable ingredients. This shift has propelled manufacturers to reformulate their offerings to include natural and organic flavors, which are perceived as healthier alternatives to synthetic options.

As the clean label trend continues to grow, it drives significant innovation and development in the Food Flavors Market, particularly within segments like beverages and health-oriented foods, where consumer scrutiny is highest.

Expansion of Global Food and Beverage Industries

The global expansion of the food and beverage industry, fueled by rising populations and economic growth in emerging markets, is a major driver for the Food Flavors Market. As companies enter new regions, they adapt their products to suit local tastes and preferences, necessitating a diverse range of flavors.

This expansion not only broadens the geographic footprint of flavor companies but also enhances the demand for customized and region-specific flavor solutions, thus pushing the boundaries of flavor science and application.

Technological Advancements in Flavor Production

Technological innovations in the production and processing of food flavors have enabled manufacturers to create more complex and stable flavoring solutions. Advances in encapsulation technologies, for instance, allow flavors to be more effectively integrated into food and beverage products, enhancing taste profiles and extending shelf life.

These technological strides facilitate the development of flavors that are both cost-effective and high in quality, meeting the dual demands of the industry for efficiency and consumer appeal.

Restraining Factors

Stringent Regulations on Food Flavoring Additives

Stringent regulations governing the use of food flavoring additives pose significant challenges to the Food Flavors Market. Regulatory bodies across the world, such as the FDA in the United States and EFSA in Europe, have set strict guidelines on the types and quantities of flavors that can be used in food products.

These regulations aim to ensure safety and transparency but can limit innovation and extend the time and cost involved in bringing new flavors to market. Companies must navigate these complex regulatory landscapes, which can hinder rapid product development and deployment.

Volatility in Raw Material Prices

The Food Flavors Market is heavily dependent on the availability and cost of raw materials, which are subject to fluctuations due to various factors including weather conditions, political instability, and economic turbulence.

Ingredients used in natural flavors, such as fruits, spices, and herbs, can experience significant price volatility, which impacts production costs and ultimately, product pricing. This unpredictability can restrain market growth as manufacturers struggle to maintain consistent pricing and supply chain stability.

Increasing Consumer Skepticism Towards Artificial Additives

There is a growing consumer skepticism towards artificial additives, including synthetic flavors, driven by health and wellness trends. Consumers are becoming more health-conscious and are often wary of products containing artificial and chemical ingredients, associating them with potential health risks.

This shift in consumer preference challenges the market for synthetic flavors, compelling companies to invest more in research and development of natural and organic alternatives, which may be more costly and complex to produce.

Growth Opportunity

Growing Demand for Exotic and Ethnic Flavors

The increasing consumer interest in global cuisine offers a significant growth opportunity for the Food Flavors Market. As people become more adventurous with their eating habits, the demand for exotic and ethnic flavors continues to rise.

This trend is particularly evident in Western markets, where there is a growing appetite for authentic Asian, African, and Latin American cuisines. Flavor manufacturers can capitalize on this trend by expanding their product lines to include these diverse and rich flavors, catering to both restaurants and home cooks looking to explore new culinary landscapes.

Health-Conscious Trends Boosting Natural Flavors

Health-conscious trends are profoundly influencing consumer choices, leading to a surge in demand for natural and organic food products. This shift provides a lucrative growth opportunity for the Food Flavors Market, particularly in the development and sale of natural flavors.

Manufacturers that can innovate and produce high-quality natural flavorings that meet consumer expectations for health without compromising on taste are well-positioned to capture and expand their market share. This trend is also encouraging the reformulation of existing products to better align with the health preferences of today’s consumers.

Technological Innovations in Flavor Enhancement and Sustainability

Technological advancements present a vast growth opportunity in the Food Flavors Market, especially through innovations that enhance flavor delivery and sustainability. Techniques such as microencapsulation, advanced extraction methods, and biotechnology enable more effective flavoring solutions that are also environmentally friendly.

These technologies not only improve the sensory profiles of food and beverages but also help in reducing environmental impact by optimizing resource use and decreasing waste. Flavor companies that invest in these technologies can gain a competitive edge by offering superior products that are both tasty and sustainable.

Latest Trends

Plant-Based Innovations Drive Flavor Developments

The rising popularity of plant-based diets has become a significant trend in the Food Flavors Market. As consumers increasingly opt for vegetarian and vegan options, the demand for flavors that enhance plant-based products has surged.

Manufacturers are responding by creating robust, meat-like flavors to improve the taste profiles of plant-based meats and other vegan products. This trend not only caters to vegetarians and vegans but also attracts flexitarians who are reducing their meat consumption for health or environmental reasons.

Fusion Flavors Blend Culinary Traditions

Fusion cuisine, which combines elements from different culinary traditions, is a growing trend influencing the Food Flavors Market. This trend reflects globalized eating habits and the desire for novelty and exotic taste experiences.

As consumers become more open to new flavors and food combinations, flavor manufacturers are innovating by blending traditional flavors in unexpected ways, creating unique and exciting taste experiences. This approach not only revitalizes existing product lines but also attracts adventurous consumers eager to explore new culinary horizons.

Clean Label and Transparency Becoming Standard

The demand for clean-label products, which are free from artificial ingredients and additives, continues to shape industry trends. Consumers are increasingly scrutinizing product labels, seeking transparency and simplicity in the ingredients used.

This trend has prompted flavor manufacturers to develop and promote natural flavors and transparent labeling practices. By aligning with this trend, companies can build trust and loyalty with health-conscious consumers, positioning themselves as leaders in a market that values purity and authenticity.

Regional Analysis

In 2023, the Asia-Pacific Food Flavors Market reached USD 5.9 billion, representing 36.6% of the global market share.

In the global landscape, the Food Flavors Market is strategically divided among several key regions: North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

Dominating these regions, Asia-Pacific stands out with a commanding 36.6% market share, valued at USD 5.9 billion, driven by expanding urbanization, growing middle-class consumption, and regional culinary diversity that demands innovative flavor solutions.

North America follows, with a robust demand linked to trends in health-conscious eating and a preference for natural and organic products. Europe’s market is bolstered by stringent EU regulations favoring natural over synthetic flavors, aligning with a surge in clean label products.

Meanwhile, the Middle East & Africa is experiencing gradual growth, influenced by increasing disposable incomes and a growing affinity for Westernized food preferences. Latin America, though smaller in comparison, shows potential through its rich agricultural base, offering unique opportunities for natural flavor extraction and exports.

Collectively, these regions depict a dynamic and diverse palette of growth opportunities and challenges, reflecting the complex interplay of cultural, economic, and regulatory factors shaping the food flavor industry.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global Food Flavors Market is marked by the influence of several key players, each contributing uniquely to industry dynamics. Among these, Givaudan International SA continues to lead with its innovative approach and commitment to sustainability, aligning its operations with consumer demands for natural and organic flavors.

Firmenich SA, another giant, excels in leveraging cutting-edge technologies such as artificial intelligence to develop flavors that resonate with contemporary consumer palates and preferences.

International Flavors & Fragrances (IFF) stands out for its strategic mergers and acquisitions, notably its merger with DuPont’s Nutrition & Biosciences division, enhancing its capabilities and market reach. This move strategically positions IFF to harness synergies across a broader product portfolio in the nutrition and food ingredients sector.

Meanwhile, Symrise AG remains a strong contender, focusing on high-growth markets and investing significantly in R&D to create differentiated products that meet complex consumer demands.

The Kerry Group, known for its clean-label solutions, taps into consumer trends toward health and wellness. Its dedication to natural ingredients and taste innovation helps maintain its competitive edge. In contrast, newer entrants like Huabao International Holdings Limited focus on expanding their footprint in Asia-Pacific, capitalizing on regional growth opportunities.

Companies like Bell Flavors and Fragrances and T. Hasegawa continue to innovate in flavor profiles by incorporating local and exotic elements, ensuring relevance in diverse markets. On the other hand, McCormick & Company leverages its strong brand reputation and extensive distribution network to drive growth, particularly in the consumer segment.

Overall, these companies’ strategic initiatives—from sustainability efforts to technological advancements and market expansion strategies—shape the competitive landscape of the Food Flavors Market, driving forward industry standards and consumer satisfaction.

Top Key Players in the Market

- Archer Daniels Midland

- Bell Flavors and Fragrances

- DuPont

- Firmenich SA

- Frutarom Industries Ltd.

- Givaudan International SA

- Huabao International Holdings Limited

- International Flavors & Fragrances

- Kerry Group, Plc.

- MANE

- McCormick & Company

- Robertet SA

- S H Kelkar and Company Limited.

- Sensient Technologies Corporation

- Symrise AG.

- Synergy Flavors Inc.

- T. Hasegawa

- Taiyo International

- Takasago International Corporation

Recent Developments

- In 2023, Archer Daniels Midland (ADM) enhanced its food flavors sector by acquiring UK-based FDL and Revela Foods, focusing on innovative flavor solutions and expanding capabilities in global markets, particularly for plant-based and protein-rich foods.

- In 2023, Bell Flavors & Fragrances introduced alcohol-inspired flavors during the Regional IFT Roadshow, appealing to sober-curious trends. By 2024, they launched trends through their Spark platform, focusing on ‘phygital’ experiences, sustainability, and personalized health innovations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 16.3 Billion |

| Forecast Revenue (2033) | USD 26.0 Billion |

| CAGR (2024-2033) | 4.8% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Natural, Synthetic, Nature Identical Flavoring), By Form (Powder, Liquid), By Application (Food and Nutrition, Bakery and Confectionery, Beverages, Sauces and Dressings, Dairy and Frozen Desserts, Snacks, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Archer Daniels Midland, Bell Flavors and Fragrances, DuPont, Firmenich SA, Frutarom Industries Ltd., Givaudan International SA, Huabao International Holdings Limited, International Flavors & Fragrances, Kerry Group, Plc., MANE, McCormick & Company, Robertet SA, S H Kelkar and Company Limited., Sensient Technologies Corporation, Symrise AG., Synergy Flavors Inc., T. Hasegawa, Taiyo International, Takasago International Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |