Quick Navigation

- Report Overview

- Key Takeaways

- By Product Type Analysis

- By Protein Source Analysis

- By Flavour Analysis

- By Packaging Type Analysis

- By End-User Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

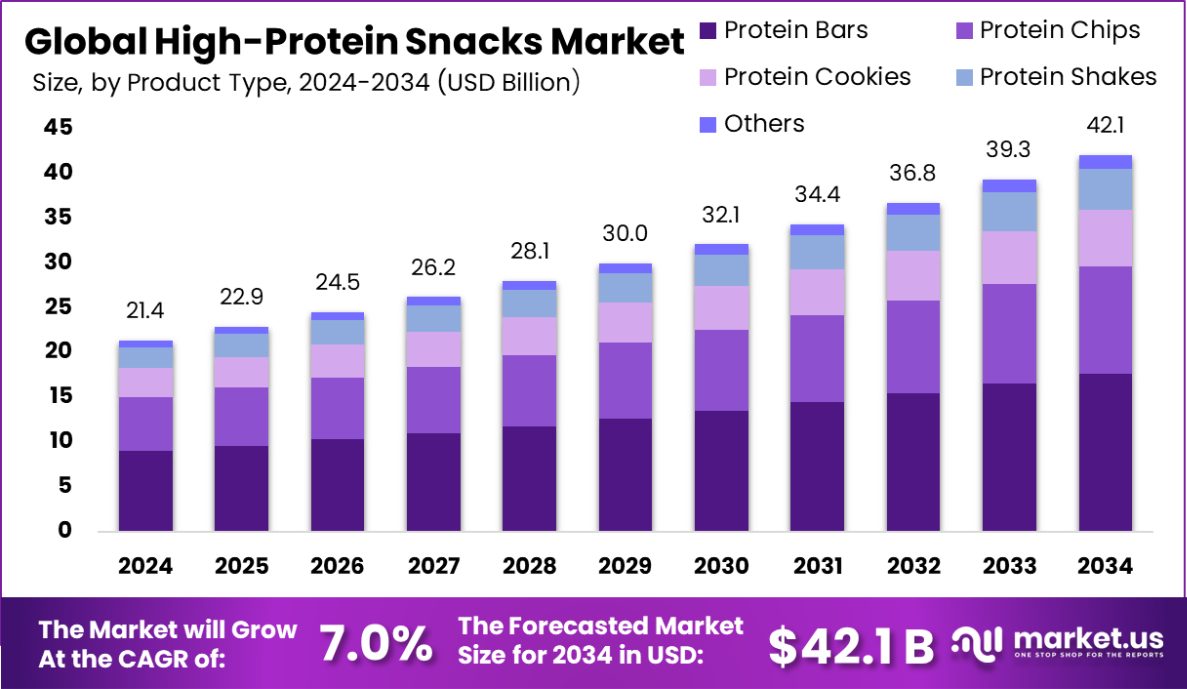

Global High-Protein Snacks Market is expected to be worth around USD 42.1 billion by 2034, up from USD 21.4 billion in 2024, and grow at a CAGR of 7.0% from 2025 to 2034. With a 41.1% market share, North America’s High-Protein Snacks Market was valued at USD 8.7 billion in 2024.

High-protein snacks are nutrient-dense food options designed to provide sustained energy and muscle support while promoting satiety. These snacks cater to fitness enthusiasts, health-conscious individuals, and busy consumers looking for convenient, protein-rich alternatives to traditional snacks. With 90% of adults, 83% of adolescents, and 97% of children snacking daily, the demand for high-protein snacks has surged.

In the Island of Ireland, 37% of adults view protein bars as a healthy choice, while 28% have purchased them, with the 25-34 age group showing the highest adoption at 42%. Consumers worldwide are shifting toward functional snacking, making high-protein options a crucial segment in the evolving food industry.

The rising health consciousness and emphasis on protein intake drive market growth as more consumers seek balanced nutrition. In India, 43% of respondents eat almonds in the morning, and 24% incorporate them into breakfast, indicating a strong preference for natural high-protein options.

Additionally, 55% of Indians consider almonds an ideal daytime snack, reflecting the growing inclination toward plant-based protein sources. This trend aligns with the increasing preference for clean-label, non-GMO, and minimally processed foods, further boosting demand.

Opportunities lie in innovation, with brands expanding beyond protein bars to include fortified nuts, chips, and dairy-based snacks. Given that 25-to 34-year-olds are the primary buyers of protein bars, brands can develop targeted marketing strategies to attract younger demographics.

Moreover, the increasing adoption of plant-based and allergen-free protein snacks presents growth avenues for manufacturers aiming to cater to diverse dietary needs. The market’s expansion is fueled by growing urbanization, rising disposable incomes, and the need for convenient yet nutritious snacking options.

Key Takeaways

- Global High-Protein Snacks Market is expected to be worth around USD 42.1 billion by 2034, up from USD 21.4 billion in 2024, and grow at a CAGR of 7.0% from 2025 to 2034.

- Protein bars dominate the high-protein snacks market, holding a significant share of 42.5% by product type.

- Whey-based high-protein snacks are preferred, accounting for 52.3% of the market by protein source.

- Chocolate is the most popular flavor in the high-protein snacks market, with a preference rate of 37.9%.

- Single serve packaging is overwhelmingly favored in the market, comprising 63.3% of high-protein snack packaging types.

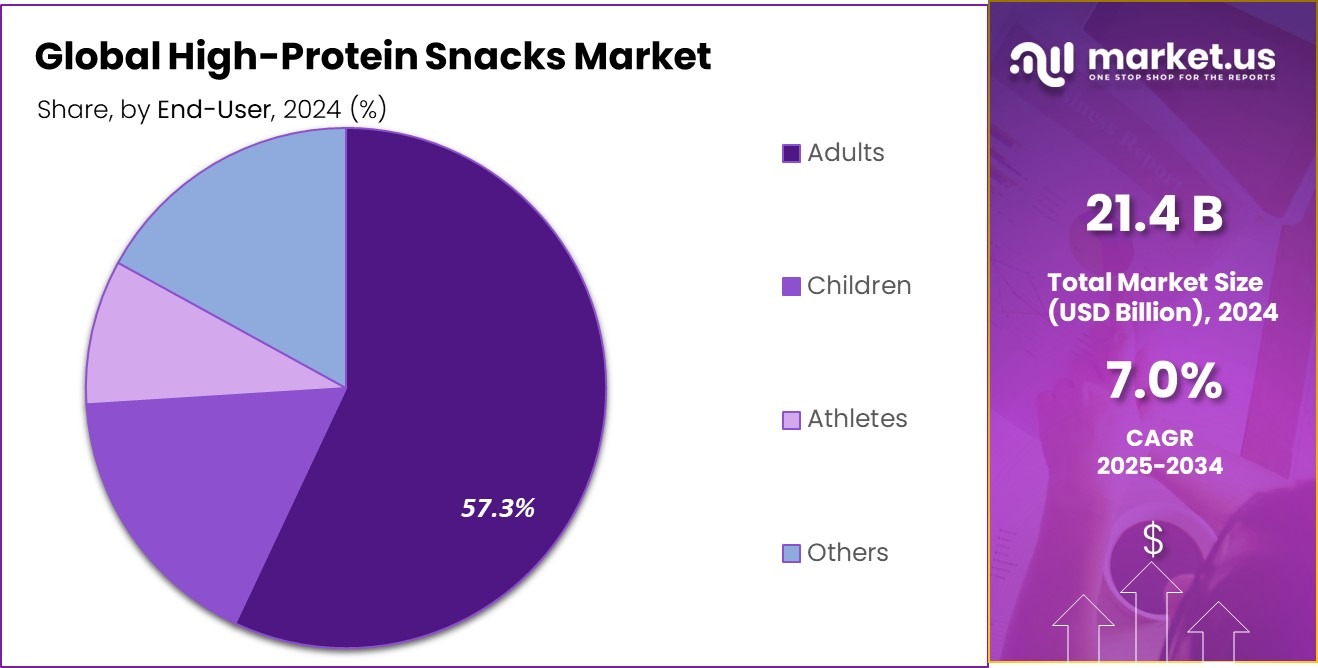

- Adults are the primary consumers of high-protein snacks, making up 57.3% of the market by end-user.

- Supermarkets and hypermarkets are key distribution channels, representing 36.6% of high-protein snack sales.

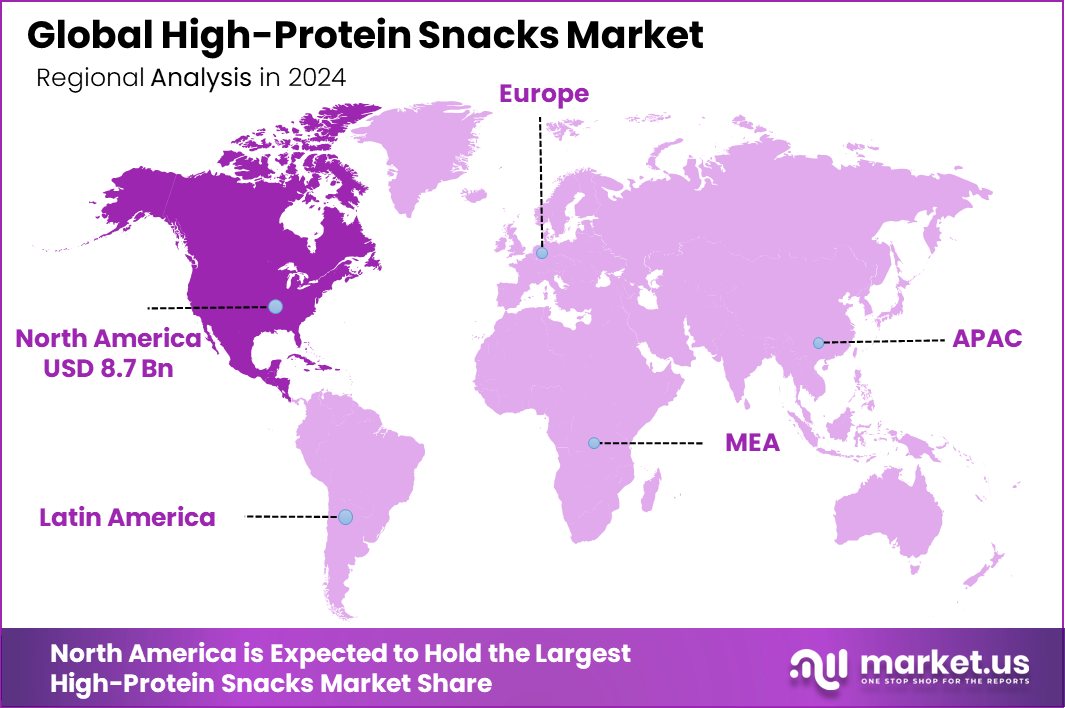

- The High-Protein Snacks Market in North America reached USD 8.7 billion, capturing a 41.1% market share.

By Product Type Analysis

Protein bars dominate the High-Protein Snacks Market, holding a 42.5% share.

In 2024, Protein Bars held a dominant market position in the By Product Type segment of the High-Protein Snacks Market, with a 42.5% share. This significant market share underscores the popularity of protein bars among consumers seeking convenient and effective ways to incorporate high-quality protein into their diets. Protein bars have been particularly favored for their portability and ease of consumption, making them an ideal choice for on-the-go nutrition for athletes, busy professionals, and health-conscious individuals alike.

The appeal of protein bars extends beyond mere convenience. Manufacturers have innovatively expanded the range of flavors and formulations, catering to a broader palette and dietary needs, including gluten-free, vegan, and low-sugar options. This versatility has enhanced their appeal across various demographic segments, further solidifying their position in the market.

The success of protein bars in the high-protein snacks market is also a reflection of the growing trend toward health and wellness, where consumers increasingly opt for snacks that offer nutritional benefits without sacrificing taste or convenience. As this trend continues to evolve, protein bars are likely to maintain their market dominance, driven by consumer demand for healthier snacking options and continuous product innovation.

By Protein Source Analysis

Whey protein is the leading source in the market, with 52.3% dominance.

In 2024, Whey held a dominant market position in the By Protein Source segment of the High-Protein Snacks Market, with a 52.3% share. This dominance is largely attributed to whey’s well-established reputation as a high-quality, complete protein source containing all essential amino acids. Its efficacy in muscle repair and growth makes it highly popular among athletes and fitness enthusiasts, who are key consumer segments in the high-protein snacks market.

The popularity of whey protein is also bolstered by its versatile application in various snack formats, including bars, shakes, and even baked goods, allowing consumers to enjoy a variety of taste profiles and textures. The wide acceptance of whey protein is further supported by substantial scientific backing, which reassures consumers of its health benefits, particularly in weight management and muscle building.

Moreover, the ongoing innovation in flavor and product development in whey-based snacks has helped maintain its appeal and market share. Manufacturers continue to introduce new products that cater to evolving consumer preferences for healthier snack options that do not compromise on taste. This ongoing product evolution keeps the whey segment vibrant and maintains its strong position in the market.

By Flavour Analysis

Chocolate flavor is preferred by 37.9% of consumers in the High-Protein Snacks Market.

In 2024, Chocolate held a dominant market position in the By Flavour segment of the High-Protein Snacks Market, with a 37.9% share. The strong preference for chocolate-flavored high-protein snacks can be attributed to their widespread consumer appeal, offering a balance between indulgence and nutrition. Chocolate remains a classic choice in the functional food segment, as it enhances the taste profile of protein-rich snacks while maintaining a sense of familiarity for consumers.

The dominance of the chocolate flavor is evident across various high-protein snack formats, including bars, shakes, yogurts, and protein powders. Manufacturers have capitalized on this demand by developing an array of chocolate-based variants, including dark chocolate, milk chocolate, and chocolate-infused combinations with nuts, caramel, and fruit flavors. These innovations have further reinforced consumer interest and driven market growth.

Additionally, chocolate-flavored high-protein snacks appeal to both fitness-conscious individuals and general consumers looking for healthier alternatives to traditional sweet snacks. The ability to combine great taste with high nutritional value makes chocolate the preferred flavor choice in the market.

As consumer preferences continue to evolve, chocolate is expected to maintain its leading position, supported by continuous product development and increasing demand for indulgent yet health-focused snack options.

By Packaging Type Analysis

Single serve packaging is most popular, capturing 63.3% of the market.

In 2024, Single Serve held a dominant market position in the By Packaging Type segment of the High-Protein Snacks Market, with a 63.3% share. The strong preference for single-serve packaging is driven by the increasing consumer demand for convenience and portion-controlled snacking. With busy lifestyles and on-the-go consumption trends rising, single-serve packaging provides a practical solution for individuals seeking quick and nutritious options without the need for preparation.

The popularity of single-serve packaging is particularly evident in protein bars, ready-to-drink protein shakes, and snack-sized nut or yogurt packs. Consumers favor these formats as they offer precise portioning, reducing the risk of overconsumption while maintaining freshness. Additionally, single-serve packs cater to fitness enthusiasts and working professionals who require easy-to-carry snacks that fit seamlessly into their daily routines.

Manufacturers continue to innovate within this segment by introducing eco-friendly and sustainable packaging solutions to align with growing environmental concerns. The dominance of single-serve packaging is also reinforced by increasing demand in retail and e-commerce channels, where grab-and-go options remain a priority for consumers. As convenience remains a key factor in purchasing decisions, single-serve packaging is expected to sustain its leading market position in the coming years.

By End-User Analysis

Adults are the primary end-users, making up 57.3% of the market segment.

In 2024, Adults held a dominant market position in the By End-User segment of the High-Protein Snacks Market, with a 57.3% share. This dominance is primarily driven by the increasing health consciousness among adults, who actively seek high-protein snacks to support weight management, muscle recovery, and overall well-being. The rising prevalence of lifestyle-related health concerns, including obesity and diabetes, has further accelerated the adoption of protein-rich diets among this demographic.

Adults are the primary consumers of high-protein snacks due to their busy lifestyles, which demand convenient and nutritious food options. Working professionals and fitness enthusiasts, in particular, favor protein bars, shakes, and yogurt as on-the-go meal replacements or post-workout recovery solutions. The appeal of high-protein snacks is also growing among aging populations who seek functional foods that aid in maintaining muscle mass and overall health.

Manufacturers are responding to this demand by offering diverse product formulations, including plant-based, low-sugar, and clean-label options, catering to the varied dietary preferences of adult consumers. The dominance of the adult segment is expected to continue as awareness of protein’s health benefits rises and the demand for functional, convenient nutrition remains strong in the global market.

By Distribution Channel Analysis

Supermarkets and hypermarkets distribute 36.6% of high-protein snacks.

In 2024, Supermarkets/Hypermarkets held a dominant market position in the By Distribution Channel segment of the High-Protein Snacks Market, with a 36.6% share. This dominance is largely attributed to the wide product availability, competitive pricing, and the ability to offer consumers a direct purchasing experience.

Supermarkets and hypermarkets provide an extensive range of high-protein snacks, including protein bars, shakes, nuts, and yogurts, allowing customers to compare brands, flavors, and nutritional content before making a purchase.

The strong market presence of supermarkets and hypermarkets is also driven by their strategic partnerships with leading high-protein snack brands. Promotional campaigns, in-store discounts, and dedicated health food aisles further encourage consumer purchases, making these retail outlets a preferred shopping destination. Additionally, impulse buying plays a crucial role, as high-protein snacks are often placed near checkout counters and in prominently displayed sections.

Supermarkets and hypermarkets continue to benefit from consumer preferences for bulk purchases and the ability to physically assess product quality. While online sales are growing, brick-and-mortar stores remain a dominant distribution channel due to the convenience of immediate product availability. As consumer demand for high-protein snacks rises, supermarkets and hypermarkets are expected to maintain their strong foothold in the market.

Key Market Segments

By Product Type

- Protein Bars

- Protein Chips

- Protein Cookies

- Protein Shakes

- Others

By Protein Source

- Whey

- Plant-Based

- Beef

- Others

By Flavour

- Chocolate

- Vanilla

- Barbecue

- Others

By Packaging Type

- Single Serve

- Multi-Pack

- Others

By End-User

- Adults

- Children

- Athletes

- Others

By Distribution Channel

- Online Stores

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Others

Driving Factors

Rising Health Consciousness Boosts High-Protein Snack Demand

Consumers are becoming more health-conscious, leading to a significant rise in demand for high-protein snacks. People now prioritize nutrition over traditional snacking, opting for protein-rich options that support weight management, muscle recovery, and overall wellness.

The growing awareness of lifestyle diseases like obesity and diabetes has pushed individuals to seek healthier alternatives, making high-protein snacks a preferred choice. Additionally, social media and fitness influencers play a crucial role in educating consumers about protein’s benefits, further driving market growth.

Brands are responding by launching innovative, clean-label, and functional snacks to meet evolving preferences. As health trends continue to shape food choices, the demand for convenient, high-protein snacks is expected to expand, fueling market growth in the coming years.

Restraining Factors

High Costs of Protein Snacks Limit Adoption

The high price of protein snacks is a major challenge limiting their widespread adoption. Compared to regular snacks, high-protein options often come with a premium price due to the cost of quality protein sources, such as whey, plant-based proteins, and collagen.

This makes them less affordable for price-sensitive consumers, particularly in developing regions. Additionally, specialized ingredients, research-backed formulations, and clean-label production methods contribute to higher costs.

While demand for high-protein snacks is growing, affordability remains a key concern, preventing mass-market penetration. To address this, manufacturers are exploring cost-effective ingredient sourcing and production techniques. However, until prices become more competitive, the premium nature of high-protein snacks may slow their growth, particularly among budget-conscious consumers.

Growth Opportunity

Expanding Plant-Based Protein Options Drive Growth

The rise of plant-based diets presents a major growth opportunity for the high-protein snacks market. More consumers are shifting toward plant-based eating due to health, environmental, and ethical concerns, increasing the demand for protein snacks made from sources like pea, soy, and almonds. Manufacturers are responding by developing innovative plant-based products that offer the same protein benefits as traditional dairy-based options.

Additionally, the improved taste and texture of plant-based proteins are making these snacks more appealing to a broader audience. As vegan and flexitarian lifestyles gain popularity, companies investing in plant-based high-protein snacks can capture a growing consumer base. This trend is expected to fuel market expansion, particularly in regions where plant-based eating is rapidly increasing.

Latest Trends

Clean Label and Natural Ingredients Gain Popularity

Consumers are increasingly looking for high-protein snacks made with clean-label and natural ingredients. This trend is driven by a growing awareness of artificial additives, preservatives, and excessive sugar content in processed foods. Shoppers now prefer snacks with simple, recognizable ingredients, free from artificial flavors, colors, and sweeteners. Brands are responding by formulating high-protein snacks with organic, non-GMO, and minimal ingredient lists to meet consumer expectations.

Additionally, the demand for sugar-free and low-carb options is rising, especially among health-conscious individuals and fitness enthusiasts. As transparency in food labeling becomes a key purchasing factor, manufacturers focusing on clean-label high-protein snacks will gain a competitive edge in the market. This trend is expected to shape future product innovation and marketing strategies.

Regional Analysis

In 2024, North America led the High-Protein Snacks Market with a 41.1% share, generating USD 8.7 billion.

In 2024, North America dominated the High-Protein Snacks Market, holding a 41.1% share and generating USD 8.7 billion in revenue. The region’s leadership is driven by strong consumer demand for health-focused snacks, a well-established fitness culture, and the presence of key industry players. The increasing preference for protein-rich diets among U.S. and Canadian consumers further fuels market growth.

Europe follows as a key market, with growing awareness of functional foods and a rising vegan population supporting demand for plant-based protein snacks. The increasing emphasis on clean-label products and protein-enriched foods contributes to sustained market expansion across Germany, the U.K., and France.

Asia Pacific is emerging as a high-growth region, propelled by rising disposable incomes, urbanization, and an expanding health-conscious consumer base. Countries like China, Japan, and India are witnessing a surge in demand for protein snacks, particularly among younger demographics and working professionals.

The Middle East & Africa and Latin America represent smaller yet steadily growing markets, driven by urbanization and shifting dietary habits. Increasing penetration of international health food brands and the rising adoption of protein snacks in countries like Brazil and the UAE are fostering regional growth.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, Nestlé S.A. continued to strengthen its position in the high-protein snacks market through strategic innovations in functional nutrition. The company’s focus on clean-label protein products and plant-based alternatives has resonated well with health-conscious consumers, driving its global market presence.

PepsiCo, Inc. leveraged its strong distribution network and brand portfolio to expand its footprint in the protein snack segment. The company’s acquisitions and product launches in protein-packed chips and snack bars have helped it capture a growing consumer base seeking convenient, high-protein options.

The Kellogg Company capitalized on increasing consumer demand for protein-enriched cereals and snack bars. With a focus on innovation and fortified products, Kellogg’s high-protein offerings have gained traction, especially in North America and Europe, where demand for functional foods remains strong.

General Mills, Inc. has expanded its high-protein snack portfolio, particularly through its well-established brands in the yogurt and snack bar segments. The company’s emphasis on natural ingredients and sustainable sourcing has strengthened its market appeal, catering to the clean-label trend.

Hormel Foods Corporation has maintained steady growth by focusing on meat-based high-protein snacks. With a strong demand for jerky and protein-rich ready-to-eat products, Hormel continues to attract fitness enthusiasts and on-the-go consumers.

Tyson Foods, Inc. remains a dominant player in the meat protein snack segment, benefiting from its expertise in protein processing. The company’s commitment to high-protein innovations in packaged meats and alternative protein snacks positions it well for future market expansion.

Top Key Players in the Market

- Nestlé S.A.

- PepsiCo, Inc.

- The Kellogg Company

- General Mills, Inc.

- Hormel Foods Corporation

- Tyson Foods, Inc.

- Clif Bar & Company

- Quest Nutrition, LLC

- The Hershey Company

- Mondelez International, Inc.

- Danone S.A.

- Unilever PLC

- Mars, Incorporated

- Abbott Laboratories

- Glanbia plc

- Premier Nutrition Corporation

- Kind LLC

- Blue Diamond Growers

- Post Holdings, Inc.

- Bumble Bee Foods, LLC

Recent Developments

- In January 2025, Ferrero Group signed an agreement to acquire Power Crunch, a protein snack company known for its wafer bars and high-protein crisps.

- In November 2024, Post Holdings reported strong growth in its Post Consumer Brands segment, which includes protein-rich cereals and snacks, with net sales increasing 35.5% to $4.11 billion for the fiscal year 2024.

- In July 2024, Danone announced plans to expand its high-protein dairy strategy, focusing on low-sugar, high-protein formulations like its Too Good yogurt brand.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 21.4 Billion |

| Forecast Revenue (2034) | USD 42.1 Billion |

| CAGR (2025-2034) | 7.0% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Protein Bars, Protein Chips, Protein Cookies, Protein Shakes, Others), By Protein Source (Whey, Plant-Based, Beef, Others), By Flavour (Chocolate, Vanilla, Barbecue, Others), By Packaging Type (Single Serve, Multi-Pack. Others), By End-User (Adults, Children, Athletes, Others), By Distribution Channel (Online Stores, Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Nestlé S.A., PepsiCo, Inc., The Kellogg Company, General Mills, Inc., Hormel Foods Corporation, Tyson Foods, Inc., Clif Bar & Company, Quest Nutrition, LLC, The Hershey Company, Mondelez International, Inc., Danone S.A., Unilever PLC, Mars, Incorporated, Abbott Laboratories, Glanbia plc, Premier Nutrition Corporation, Kind LLC, Blue Diamond Growers, Post Holdings, Inc., Bumble Bee Foods, LLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |