Quick Navigation

Report Overview

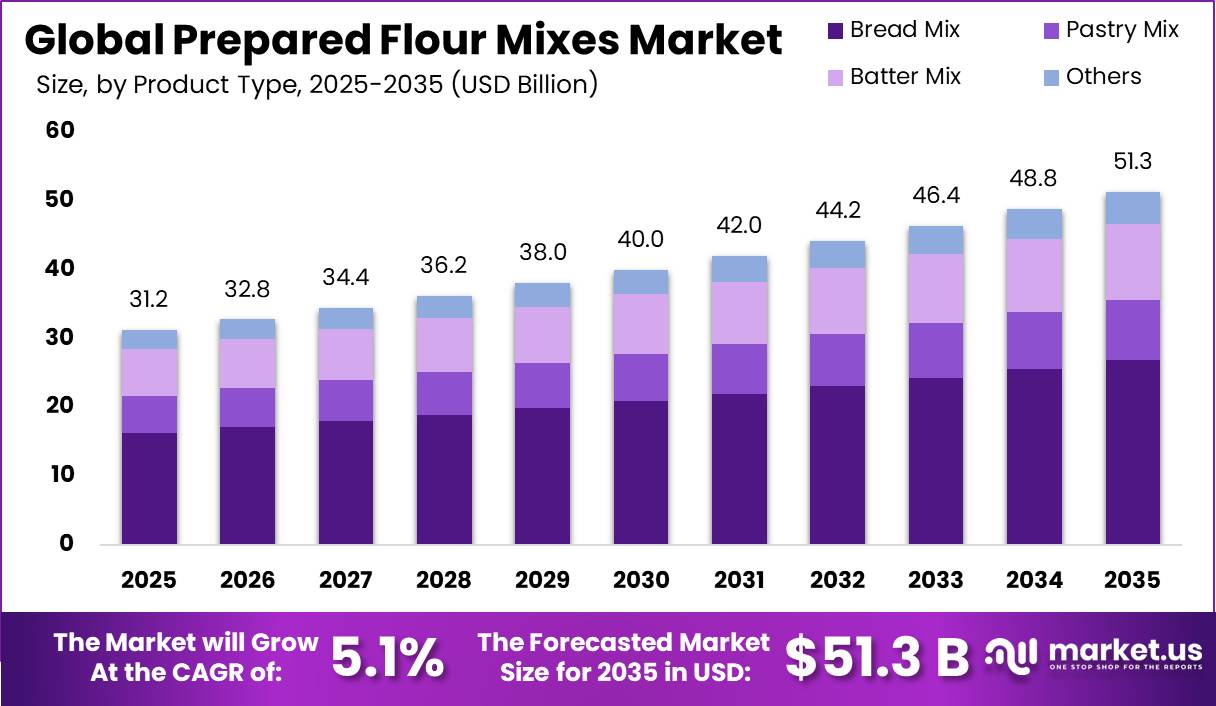

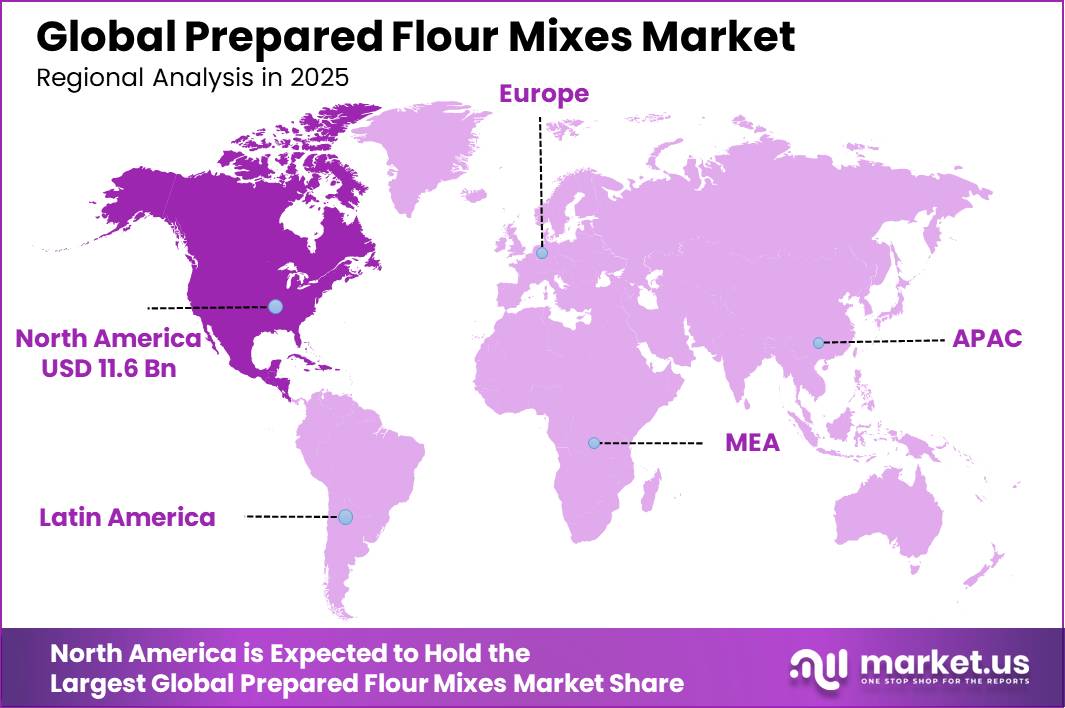

The Global Prepared Flour Mixes Market was valued at US$31.2 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 5.1%, reaching about US$51.3 billion by 2035. North America held a dominant market position, capturing more than a 37.2% share, holding USD 11.61 billion in revenue.

Prepared flour mixes are a value-added segment of the global food ingredients industry, supplying standardized blends for bakery, confectionery, convenience food, foodservice, retail, and industrial food processing applications. These products improve production efficiency, reduce preparation time, and ensure consistent product quality across commercial manufacturing. Industry expansion is supported by the steady growth of processed food consumption and increasing demand for convenient food solutions.

According to OECD-FAO Agricultural Outlook 2025–2034, global consumption of agricultural and fish commodities is projected to increase by 13% by 2034, while production is expected to grow by 14%, strengthening the raw material base for flour-based ingredient manufacturers. The industry is driven by rising consumption of bakery products, increasing demand for ready-to-use food ingredients, greater automation in food manufacturing, and growing consumer preference for clean-label, gluten-free, whole-grain, and protein-enriched formulations.

Prepared flour mixes enable manufacturers to maintain product consistency, reduce operational complexity, and improve production efficiency. OECD-FAO projects that global food consumption will increase by an average of 1.3% annually over the coming decade, reflecting sustained demand for processed cereal-based foods and bakery products.

Future growth opportunities are expected to emerge through innovations in functional, organic, fortified, and specialty flour mixes, along with sustainable sourcing practices and advanced food manufacturing technologies. Government initiatives such as the European Union’s Farm to Fork Strategy and the Common Agricultural Policy (CAP) continue to promote sustainable agriculture, resilient food supply chains, and improved food quality, creating a supportive environment for long-term growth in the prepared flour mixes industry.

Key Takeaways

- The global Prepared Flour Mixes market was valued at US$31.2 billion in 2025.

- The global battery separator market is projected to grow at a CAGR of 5.1% and is estimated to reach US$51.3 billion by 2035.

- Based on product, Bread Mix dominated the global prepared flour mixes market, accounting for approximately 52.3% of the total market share.

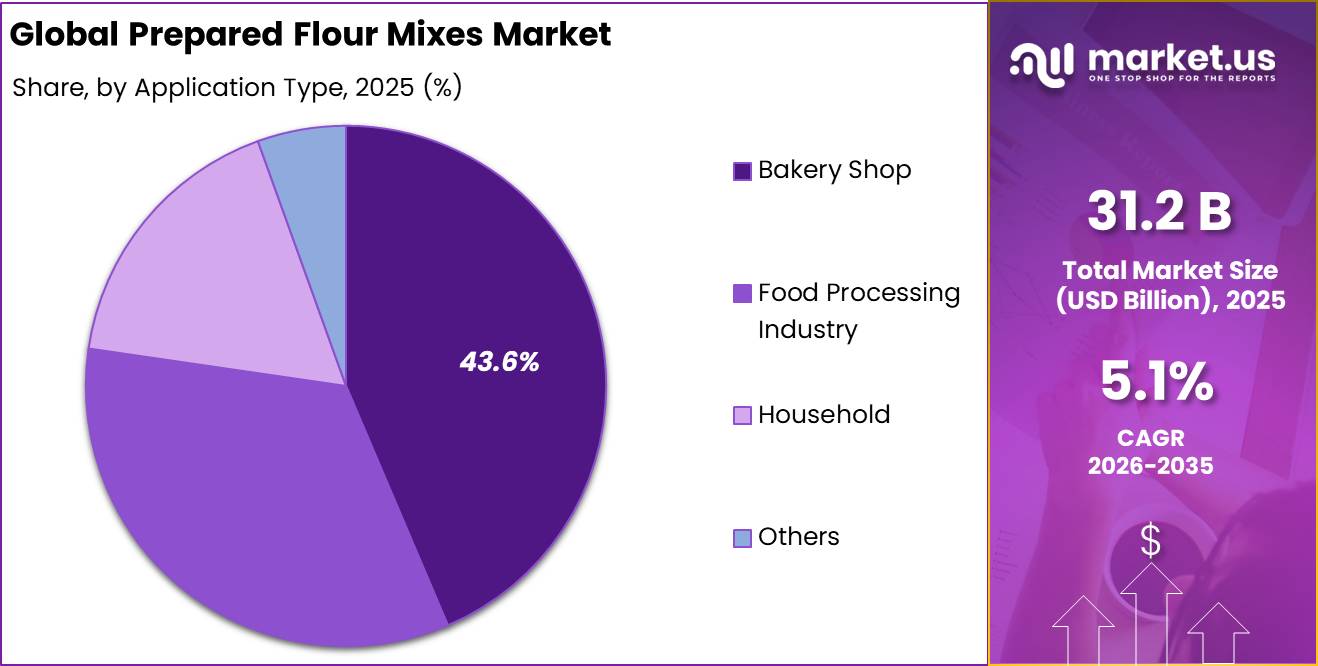

- Based on application, Bakery Shop held the largest market share, comprising nearly 43.6% of the global market.

- Based on specialty type, Conventional / Traditional prepared flour mixes represented the dominant segment, accounting for approximately 64.3% of the total market share.

- Based on distribution channel, Offline Retail dominated the market with around 56.7% share due to strong supermarket, hypermarket, and retail bakery product penetration globally.

- In 2025, North America dominated the global prepared flour mixes market, accounting for approximately 37.2% of the total market share.

Product Type Analysis

Bread Mix Represents the Dominant Segment in the Prepared Flour Mixes Market.

Bread Mix dominates the global flour mixes market with 52.3% market share, driven by high consumption of bread and bakery items in homes, industrial bakeries, restaurants, and cafes. These mixes provide efficiency, uniform composition, time savings, and enhanced product quality, making them favored in bakery production. Urbanization, changing lifestyles, and increasing demand for convenient bakery products have further boosted this commercial demand.

Innovation in whole grain, gluten-free, multi-grain, protein-fortified, and clean label bakery mixes is being witnessed in the specialty breads category as well. Usage of such mixes gets a further boost through investment in automation and quality. Batter mixes and pastry mixes continue their strong growth because of the growing demand for cake and pastry mixes.

Application Analysis

Bakery Shop Represents the Dominant Segment in the Prepared Flour Mixes Market.

The Bakery Shops have emerged as the most prevalent end-user category within the global ready-to-use flour mixes market, holding around 43.6% of the overall market share. The predominance of this category is mainly attributed to the fast growth of commercial bakeries, bakery shops, artisan bakery chains, cafes, and fast food joints.

Bakery shops have been utilizing ready-to-use flour mixes to make their production process more efficient and also reduce dependence on labor. The increased consumption of bakery products among consumers has boosted the commercial use of flour mixes in the bakery industry.

The industry is also benefiting from the rising trend among consumers to choose bakery products of high quality and tailor-made bakery products along with convenient methods of eating food. The bakery industry is shifting towards the use of specialized flour blends including gluten-free, multigrain, organic and high protein flour blends for meeting the demands of health-conscious consumers.

Specialty Analysis

Conventional / Traditional Represents the Leading Segment in the Prepared Flour Mixes Market.

Conventional prepared flour mixes dominate the global market, holding 64.3% of the share. Their popularity stems from consumer acceptance, affordability, and versatility in commercial bakeries and food processing. They are favored for baking performance, formula familiarity, and suitability for large-scale production. The continued global consumption of traditional breads, cakes, pastries, pancakes, and battered foods significantly fuels the demand for these mixes.

The market is benefiting from rising packaged food consumption, greater retail availability of baked goods, and a shift towards convenient baking. Specialty flour mixes like gluten-free, organic, and protein-enriched options are growing due to health consciousness, prompting manufacturers to invest in innovations in functional ingredients and fortified flour mixes globally.

Distribution Channel Analysis

Offline Retail Represents the Dominant Segment in the Prepared Flour Mixes Market.

Offline Retail forms the major distribution channel for prepared flour mixes across the world, accounting for 56.7% market share. The success of offline retail channels is largely attributed to the availability of supermarkets, hypermarkets, convenience stores, and bakery shops, which ensure easy access by consumers.

Offline retail is preferred because of product availability, convenience, brand recognition, and comparative analysis of ingredient composition and pricing. Also, penetration in bakery products drives strong sales performance in organized retail chains.

On the contrary, the B2B / Institutional segment is experiencing significant market demand owing to the rise in procurement of pre-packaged flour mixes by hotels, restaurants, cafes, fast food joints, and industrial bakeries where quality and efficiency must not be compromised during large-scale baking processes.

The Online Retail segment is experiencing rapid expansion owing to the rise in the number of e-commerce grocery stores, growing digitization in grocery shopping trends, and changing consumer demands towards convenient shopping options. Availability of customized and special mixes for baking, gluten-free foods, gourmet bakery items, and brands catering to bakeries through online channels is also contributing to growth within this segment.

Market Segment

By Product

- Bread Mix

- Pastry Mix

- Batter Mix

- Others

By Application

- Bakery Shop

- Food Processing Industry

- Household

- Others

By Specialty Type

- Conventional / Traditional

- Gluten-Free

- Organic / Non-GMO

- Protein-Enriched / Whole Grain

- Vegan / Plant-Based

- Others

By Distribution Channel

- Offline Retail

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Stores

- Others

- Online Retail

- B2B / Institutional

- Others

Challenge

Volatile wheat input economics continue to constrain prepared flour mixes growth, with benchmark wheat futures fluctuating within a 25-35% range and recording 8-10% year-on-year price swings into mid-2026, despite easing from above 600 to around 570 USc/bushel. This exceeds the 3-4% annual cost variation most pricing models can absorb.

The volatility causes a 3-5 percentage point swing in flour costs and a 1.5-2.0 percentage point change in total COGS, reducing gross margins by 120-180 basis points. It also lowers volume growth by about 1.4 percentage points, while hedge coverage has shortened from 6-9 months to 3-4 months due to supply uncertainty.

Manufacturers are addressing the challenge through multi-origin sourcing, recipes that can flex 5-8% between wheat, rye, and blended flours, and segmented pricing strategies. However, these changes require 2-4 years to implement, making this a medium-term growth restraint.

| Challenge | (~)% CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Volatile wheat input economics | -1.4% | North America, EU, APAC, MENA | Medium term (2-4 years) |

| Multi-node logistics and lead-time risk | -1.2% | APAC export hubs, EU, North America | Short term (≤ 2 years) |

| Health, clean-label and reformulation pressure | -1.0% | North America core, EU regulatory hubs | Long term (≥ 4 years) |

| Industrial bakery talent and capability gap | -0.8% | North America, Western Europe, urban APAC | Medium term (2-4 years) |

| Regulatory and fortification compliance creep | -0.7% | EU, South Asia, Africa, LATAM | Long term (≥ 4 years) |

| Digital demand volatility and channel complexity | -0.9% | Global urban markets, e-commerce corridors | Short-Medium term (≤ 4 years) |

Opportunity

Co-developed prepared flour mixes for foodservice, QSRs, coffee chains, and bakery cafés represent a significant growth opportunity, as current demand is still largely driven by retail and generic industrial sales. Industrial and foodservice channels already account for around 40-50% of mix demand in some categories, while many suppliers continue offering standardized products.

Customized mixes that reduce preparation time by 20-30% and cut wastage by 5-10% can help secure high-volume institutional contracts, adding several hundred thousand tons of annual demand and generating low to mid single-digit billion-dollar revenue opportunities by 2035. Longer contract terms of 3-5 years can also improve capacity utilization and reduce per-unit conversion costs by 5-10%.

Capturing this opportunity requires dedicated foodservice R&D, technical support, and joint product development with major chains. Early partnerships in North America, Europe, and leading APAC markets could provide an estimated 1.5 percentage point CAGR upside for participating manufacturers.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Functional & health-positioned mixes | +2.0% | North America, EU, urban APAC | Short-Medium term |

| Emerging-market household penetration | +1.8% | APAC emerging, LATAM, MEA | Medium-Long term |

| Foodservice & QSR co-developed mixes | +1.5% | North America, EU, Tier-1 APAC | Short-Medium term |

| Direct-to-consumer & subscription models | +1.2% | North America, EU, select APAC | Short-Medium term |

| Private label and contract manufacturing scale-up | +1.0% | North America, Europe, GCC | Medium term |

| Industrial & institutional baking solutions | +0.8% | Global industrial hubs | Long term |

Driver

Growing consumer demand and stricter nutrition regulations are driving manufacturers to reformulate prepared flour mixes with lower sugar, sodium, and additives while increasing whole grains, fiber, and fortification. Fortified products with iron, folic acid, and vitamins also support public health initiatives across Europe, North America, APAC, and Latin America.

Health-focused products such as organic, whole-grain, gluten-free, high-protein, and no-added-sugar mixes can command 10-30% higher prices than standard offerings, while maintaining stable demand through improved consumer retention and new customer adoption.

Manufacturers are also expanding sourcing of specialty flours such as spelt, rye, ancient grains, almond, and coconut flour to strengthen product differentiation. Over a 4+ year horizon, this trend is expected to add about 1.6 percentage points to CAGR, particularly in Europe, North America, and urban APAC markets.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience baking & time-poor households | +2.2% | North America core, EU, APAC corridors | Short-Medium term |

| Post-pandemic home baking normalization & premiumization | +1.9% | North America core, EU, Japan, Australia | Medium term |

| Foodservice & industrial bakery mix adoption | +2.5% | EU, APAC corridors, Middle East, Latin America | Medium-Long term |

| Retail channel expansion via modern trade & e-commerce | +1.8% | APAC corridors, Latin America, Africa urban | Short-Medium term |

| Product reformulation for health, clean label & fortification | +1.6% | EU, North America core, urban APAC | Medium-Long term |

| Price & margin resilience amid wheat and energy volatility | +1.3% | Global, with emphasis on EU, MENA, South Asia | Short-Medium term |

Restraint

Tightening trans-fat and sodium regulations are increasing reformulation requirements for prepared flour mixes, particularly in markets with limits of 2% or less on industrial trans-fats. Manufacturers typically require 12-24 months to reformulate each SKU, while sensory validation consumes around 1-3% of annual R&D budgets. Replacing traditional fats with specialty alternatives also raises functional fat costs by 8-12%.

These changes compress margins by an estimated 80-150 basis points because higher costs cannot be fully passed on in price-sensitive bakery markets. Plant retrofits can delay capacity expansion by 12-18 months, while production efficiency may temporarily decline from 80-85% to 70-75% during process adjustments.

Overall, stricter regulations are expected to reduce the baseline CAGR of the prepared flour mixes market by about 2.0 percentage points over a 5-7 year period, particularly in highly regulated regions.

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trans-fat and sodium regulation tightening | -2.0% | North America core, EU, India, urban APAC | Long term (≥ 4 years) |

| Wheat and edible oil input cost volatility | -1.8% | Global, with higher sensitivity in MENA, LATAM, South Asia | Medium term (2-4 years) |

| Private label and retailer margin pressure | -1.5% | North America, EU, UK, developed APAC | Medium term (2-4 years) |

| Supply chain complexity and lead-time risk | -1.2% | Global, especially APAC corridors and cross-border trade | Short-Medium term (≤ 4 years) |

| Health-centric demand shift from refined mixes | -1.0% | EU, North America, high-income APAC | Long term (≥ 4 years) |

| Regulatory and compliance overhead for small/mid players | -0.8% | Emerging markets (India, ASEAN, LATAM) | Short-Medium term (≤ 4 years) |

Geopolitical Impact Analysis

Disruptions in global grain trade and instability in agricultural supply chains affecting the market for prepared flour mixes.

The global market for prepared flour mixes is largely dependent on the political situation in the world, the agricultural trade policies in the international market, and the grain supply chain in the international market. Political instabilities, especially the ongoing Russia-Ukraine conflict, have had a large impact on the export of wheat, fertilizer prices, energy prices, and international shipping.

Also, pressure is rising in the market owing to rising transport costs, inflationary food prices, and instabilities in international food business operations. The rising costs of fueling vehicles and other logistical challenges continue to pose a threat to bakeries and food processing firms relying on the importation and distribution of grains. Furthermore, changing policies concerning food import/export and rising insecurity are causing firms to diversify their raw material sources.

On the other hand, governments and food companies from North America, Europe, and the Asia-Pacific region are gradually increasing their investments in the production of locally available grains, sustainability, and efficiency in the processing of food products. This increased emphasis on efficient processes, alternative grains, and sourcing from local sources would contribute significantly towards the stability of the global prepared flour mixes market in future.

Regional Analysis

North America Held the Largest Share of the Global Prepared Flour Mixes Market.

North America was the leader in the global market for prepared flour mixes, capturing around 37.2% of the market share. This dominance can be largely attributed to the presence of numerous industrial bakeries in North America, high consumption of packaged foods, and growing demand for convenience baking mixes in the US and Canada.

Consumers in North America are increasingly preferring ready-to-use bakery mixes, frozen bakery items, and convenience-oriented methods of preparing food products owing to their hectic schedules and preference for convenience products. Moreover, high penetration of supermarkets, hypermarkets, and organized retailers is further driving the popularity of prepared flour mixes among consumers.

Another important market would be Europe since this region has an established tradition of baking along with high demand for artisanal breads and the trend towards quality bakery raw material ingredients. The market in the Asia-Pacific region is undergoing fast expansion owing to urbanization, westernization of food consumption habits, and establishment of a chain of bakery retail stores in China, India, Japan, and other Southeast Asian countries.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global market of prepared flour blends exhibits moderate fragmentation and features the presence of multinational food ingredients producers, industrial bakery solutions providers, speciality bakeries and flour processors operating regionally, based on factors such as quality, innovation in formulas, distribution network, pricing, and availability of speciality ingredients. The primary source of competition in the market arises from growing global demand for convenience baked goods, speciality bakery solutions, clean-label formulas, and health-oriented prepared flour blends.

The industry is also seeing more investment in functional baking ingredients, protein-fortified flour mixes, sustainable grain sourcing, and high-end bakery products to cater to changing consumer preferences as well as healthy eating patterns. Moreover, collaboration between manufacturers of bakery ingredients, foodservice companies, superstores, and online groceries is likely to create even more competition in the global market for prepared flour mixes.

The Following are some of the Major Players in the Industry

- ADM (Archer Daniels Midland)

- Ardent Mills

- Associated British Foods plc

- Bakels Group

- Bay State Milling Company

- Bob’s Red Mill Natural Foods

- Chelsea Milling Company (JIFFY Mix)

- Conagra Brands, Inc. (Duncan Hines)

- Dawn Foods

- General Mills, Inc.

- King Arthur Baking Company

- Lesaffre

- Nisshin Seifun Group Inc.

- Pondan (PPMI)

- PURATOS

Key Development

- In March 2025, General Mills, Inc. expanded its baking solutions portfolio with increased focus on convenience-oriented and specialty baking products to address rising consumer demand for premium home baking and foodservice applications.

- In October 2024, PURATOS introduced new clean-label and health-focused bakery ingredient solutions, including specialty flour mixes designed for artisanal and functional bakery applications.

- In July 2024, ADM (Archer Daniels Midland) strengthened its food ingredient and grain processing capabilities through investments in sustainable sourcing and value-added bakery ingredient innovation to support the growing global bakery and processed food industries

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 31.2 Bn |

| Forecast Revenue (2035) | USD 51.3 Bn |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Bread Mix, Pastry Mix, Batter Mix, and Others), By Application (Bakery Shop, Food Processing Industry, Household, and Others), By Specialty Type (Conventional / Traditional, Gluten-Free, Organic / Non-GMO, Protein-Enriched / Whole Grain, Vegan / Plant-Based, and Others), By Distribution Channel (Offline Retail, Online Retail, B2B / Institutional, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | ADM (Archer Daniels Midland), Ardent Mills, Associated British Foods plc, Bakels Group, Bay State Milling Company, Bob’s Red Mill Natural Foods, Chelsea Milling Company (JIFFY Mix), Conagra Brands, Inc. (Duncan Hines), Dawn Foods, General Mills, Inc., King Arthur Baking Company, Lesaffre, Nisshin Seifun Group Inc., Pondan (PPMI), PURATOS |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |