Quick Navigation

Report Overview

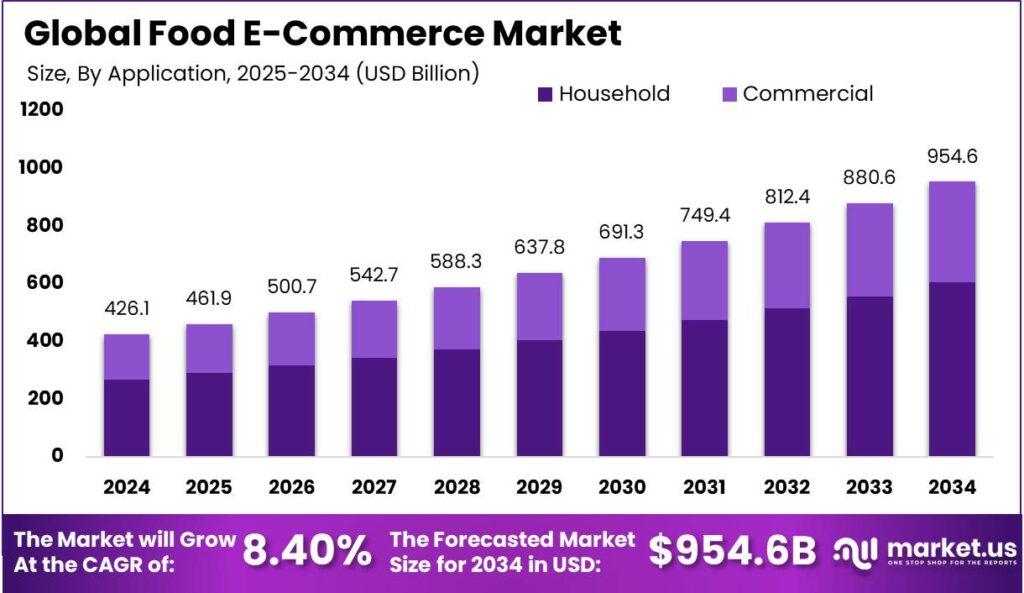

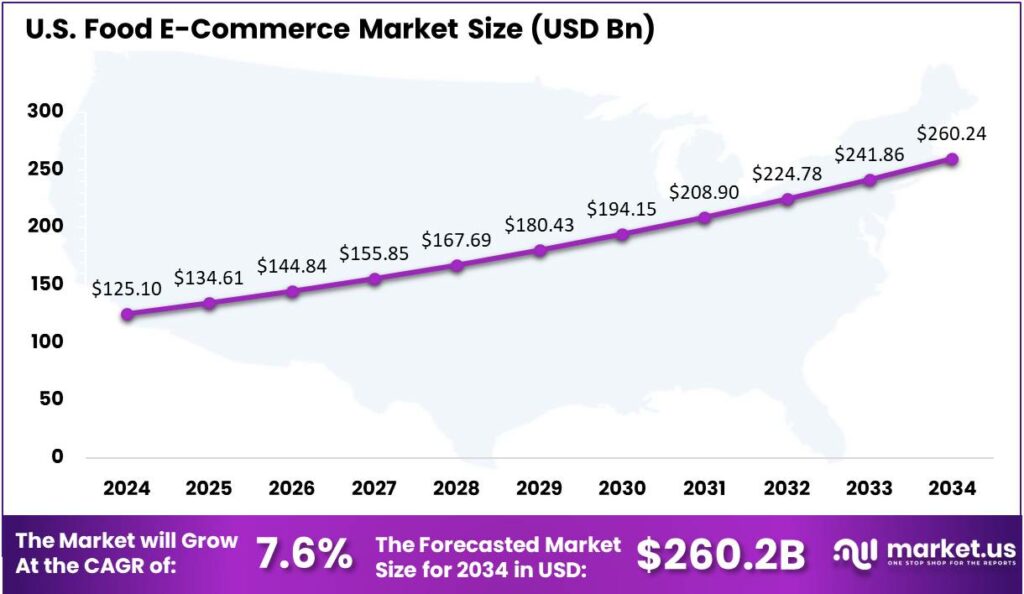

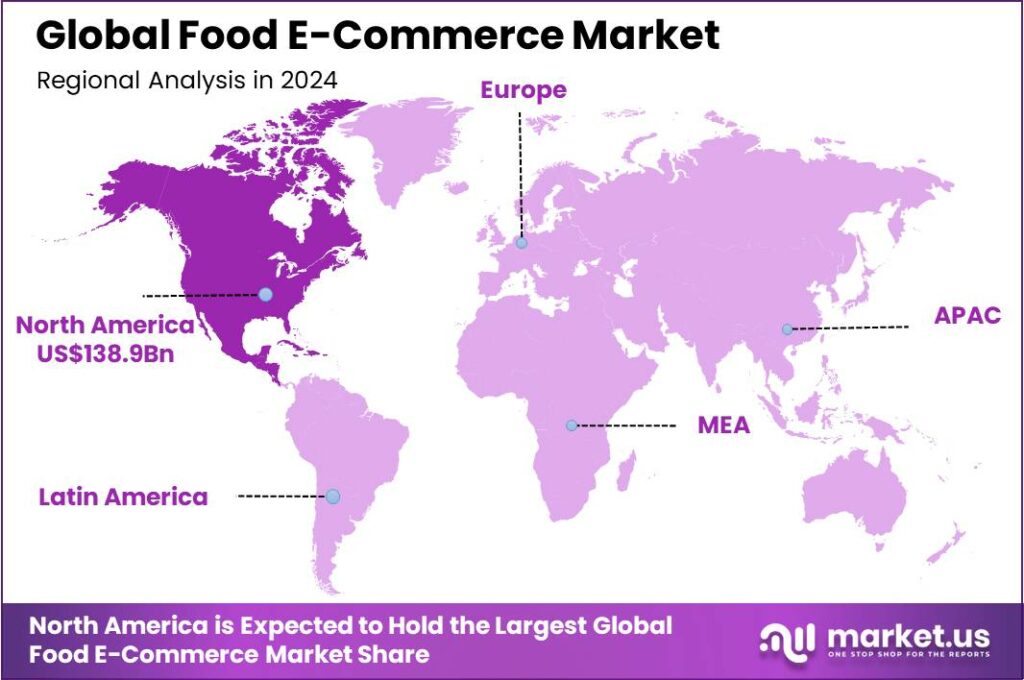

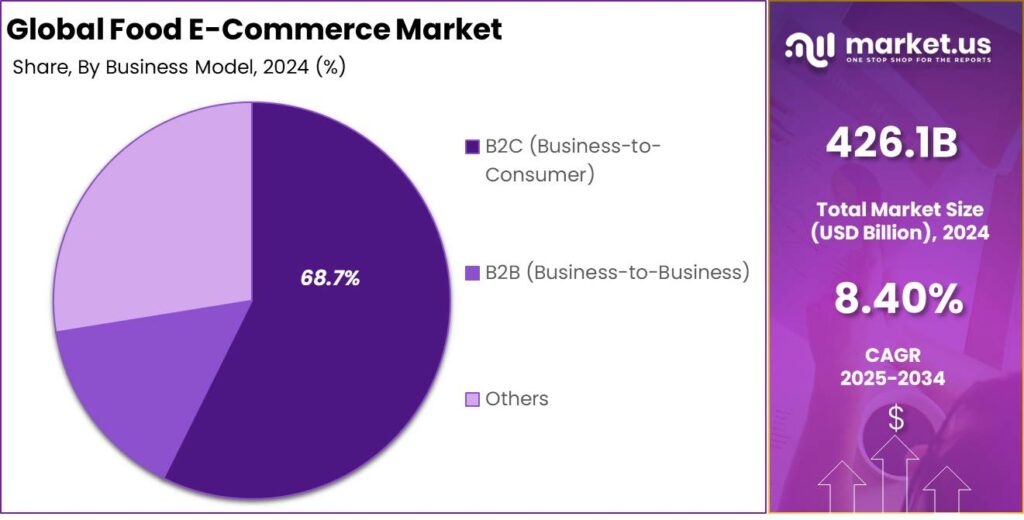

The Global Food E-Commerce Market size is expected to be worth around USD 954.6 Billion By 2034, from USD 426.1 Billion in 2024, growing at a CAGR of 8.40% during the forecast period from 2025 to 2034. In 2024, North America captured over 32.6% of the global food e-commerce market, generating approximately USD 138.9 billion in revenue, with the U.S. market valued at USD 125.1 billion.

Food e-commerce refers to the buying and selling of food products through online platforms. This encompasses a wide range of offerings, including groceries, meal kits, restaurant deliveries, and specialty food items. The primary objective is to provide consumers with convenient access to food products without the need to visit physical stores.

The global food e-commerce market has witnessed significant growth in recent years. Primary factors driving the growth of the food e-commerce market include shifts in consumer behavior and technological advancements. Urbanization and busy lifestyles have increased demand for online grocery services, with consumers preferring the convenience of shopping from home.

The demand for food e-commerce is further amplified by lifestyle changes and the need for time-saving solutions. Busy schedules and the desire for diverse food options have led consumers to prefer online platforms that offer a wide range of products and services. Moreover, the COVID-19 pandemic has accelerated the adoption of online food shopping, as consumers prioritize safety and convenience.

According to data from ecommercedb, the Indian food eCommerce market recorded a monthly revenue of approximately USD 690 million in April 2025, reflecting a 5.7% increase compared to March 2025. This steady rise demonstrates the continued consumer preference for digital grocery and meal delivery platforms, driven by convenience, time efficiency, and increasing mobile internet penetration across both urban and semi-urban regions.

Looking at the broader 12-month trend, October 2024 marked the peak in monthly revenue share, accounting for 10.9% of the total annual revenue for the Indian food eCommerce market in 2024. This spike aligns with India’s festive season, during which online food purchases – particularly of packaged goods and seasonal items – tend to surge.

Investment opportunities in the food e-commerce sector are huge, attracting venture capitalists and private equity firms. The market’s rapid growth and potential for scalability make it an appealing prospect for investors. Startups focusing on niche markets, sustainable practices, and innovative delivery models are particularly attractive, as they address specific consumer needs and preferences.

Key Takeaways

- The Global Food E-Commerce Market size is expected to reach around USD 954.6 Billion by 2034, up from USD 426.1 Billion in 2024, growing at a CAGR of 8.40% during the forecast period from 2025 to 2034.

- In 2024, the B2C (Business-to-Consumer) segment held a dominant market position, capturing more than a 68.7% share, driven primarily by increasing consumer demand for convenience, home delivery, and personalized food shopping experiences.

- In 2024, the Restaurant Meal Delivery segment held a dominant market position, capturing more than a 57.3% share of the food e-commerce market.

- In 2024, the Household segment held a dominant market position, capturing more than a 63.4% share of the global food e-commerce market.

- In 2024, North America held a dominant market position, capturing more than a 32.6% share of the global food e-commerce market, generating approximately USD 138.9 billion in revenue.

- In 2024, the U.S. Food E-Commerce market was valued at approximately USD 125.1 billion, indicating a strong foothold within the broader digital commerce ecosystem.

Key Features

- Subscriptions for Convenience: Food e-commerce sites often offer subscription services, like meal kits or regular grocery deliveries. This gives people an easy way to get their favorite foods delivered on a schedule, saves time, and helps businesses build loyal customers.

- Personalization and AI Recommendations: Personalized shopping is a big part of food e-commerce. Sites use your past orders and preferences to suggest new products, recipes. This makes shopping feel more personal and helps you discover new things easily.

- Transparent Sourcing and Sustainability: People want to know where their food comes from. Food e-commerce businesses share details about their suppliers, how food is grown or made, and use eco-friendly packaging. This builds trust and shows care for the environment.

- Flexible and Simple Checkout: A smooth checkout process is key. Sites offer many payment options (like credit cards, mobile wallets, or Buy Now, Pay Later), let you choose delivery times, and make it easy to save your info for future orders. This makes buying food online quick and stress-free.

- Focus on Health and Wellness: There’s a growing demand for healthy, organic, and specialty foods. Food e-commerce sites highlight these products and often provide detailed nutrition info, so you can make choices that fit your lifestyle.

U.S. Market Leadership

In 2024, the U.S. Food E-Commerce market was valued at approximately USD 125.1 billion, indicating a strong foothold within the broader digital commerce ecosystem. This valuation reflects the rapid digitalization of consumer habits, especially in grocery, meal kits, organic food subscriptions, and ready-to-eat products.

The market is projected to grow at a compound annual growth rate (CAGR) of 7.6%, suggesting a sustained upward trajectory through the coming years. This growth is being driven by several key factors, including rising internet penetration, changing dietary preferences, time-saving online ordering, and increasing consumer trust in the freshness and safety of delivered foods.

Additionally, food retailers and e-commerce players are increasingly investing in advanced technologies such as AI-powered personalization, real-time inventory systems, and data-driven demand forecasting. These innovations are enabling a more agile supply chain and improved customer satisfaction.

In 2024, North America held a dominant market position, capturing more than a 32.6% share of the global food e-commerce market and generating approximately USD 138.9 billion in revenue. This leadership is primarily attributed to the widespread digital infrastructure, high internet penetration, and well-established e-commerce platforms such as Amazon Fresh and Instacart.

Consumers across the U.S. and Canada have increasingly adopted online grocery shopping as part of their routine, driven by convenience, personalized offers, and rapid delivery options. The strong presence of tech-enabled logistics and cold chain capabilities has further enhanced customer confidence in ordering perishable items online.

Another factor behind North America’s lead is the evolving consumer behavior that favors health-oriented, organic, and ready-to-cook food products all of which are increasingly available through digital platforms. The pandemic has accelerated this shift, but it has since solidified into a long-term trend. Retailers and food delivery companies are investing in AI-driven recommendations, warehouse automation, and last-mile delivery optimization to enhance the customer experience.

Asia-Pacific shows strong growth but lags in market share due to logistical and regulatory challenges in rural areas. Europe sees steady adoption, especially in the U.K., Germany, and France, though fragmented markets hinder scalability. Latin America, the Middle East, and Africa are in early stages of food e-commerce growth, with infrastructure gaps but increasing smartphone use and digital payments driving potential.

Business Model Analysis

In 2024, the B2C (Business-to-Consumer) segment held a dominant market position, capturing more than a 68.7% share, primarily driven by increasing consumer demand for convenience, home delivery, and personalized food shopping experiences. The rise of mobile apps, increased internet access, and growing comfort with digital transactions have made it easier for consumers to order groceries, meal kits, and restaurant food from various platforms.

B2C platforms effectively use data analytics and AI to personalize product recommendations and promotions, driving customer engagement and repeat purchases. By analyzing buying behavior, platforms offer personalized bundles, products, and easy reordering. Targeted marketing and influencer partnerships attract tech-savvy younger consumers who prefer online shopping.

The surge in demand for healthy, organic, and specialty food products has also strengthened the position of the B2C model. Many niche brands and health-focused startups now sell directly to customers through their own websites or third-party marketplaces, avoiding the need for retail intermediaries. This direct connection allows companies to educate buyers about their products, offer trial packs, and build a loyal community of buyers.

The B2C model dominates the food e-commerce market due to its alignment with consumer expectations and convenience. Easy browsing, custom orders, and flexible deliveries make it the preferred choice. As the sector matures, innovations in fulfillment, support, and product range will strengthen B2C’s market leadership.

Type Analysis

In 2024, the Restaurant Meal Delivery segment held a dominant market position, capturing more than a 57.3% share of the food e-commerce market. This leadership can be attributed to several factors that collectively underscore its prominence.

The convenience offered by restaurant meal delivery services has significantly influenced consumer preferences. The ability to access a wide variety of cuisines from the comfort of one’s home aligns with the fast-paced lifestyles of modern consumers. This ease of access has been further enhanced by user-friendly mobile applications and platforms that streamline the ordering process.

The expansion of delivery infrastructure has played a crucial role. The proliferation of delivery personnel and the optimization of logistics have reduced delivery times, ensuring that meals arrive promptly and in optimal condition. This reliability has fostered consumer trust and repeat usage, reinforcing the segment’s market position.

Strategic partnerships between restaurants and delivery platforms have expanded the range of available options. Collaborations allow small and medium-sized eateries to reach a wider customer base without heavy investment in delivery systems, diversifying offerings and catering to various consumer tastes and preferences.

Application Analysis

In 2024, the Household segment held a dominant market position, capturing more than a 63.4% share of the global food e-commerce market. This strong lead is largely due to the growing consumer preference for convenience in day-to-day grocery shopping.

With busy lifestyles and limited time for in-store visits, households are increasingly turning to online platforms for their weekly or daily food needs. From fresh produce to packaged meals, e-commerce platforms now offer a wide variety of choices that cater directly to household consumption patterns, making digital shopping a practical and time-saving solution.

The segment’s dominance is driven by the widespread use of smartphones and apps, making online grocery shopping more accessible and appealing. Price comparison, reviews, and personalized recommendations attract households, while meal kit subscriptions, bulk discounts, and loyalty programs encourage repeat purchases, building a strong user base.

The increasing demand for healthy, organic, and dietary-specific foods is driving growth among household consumers. Many families prioritize nutrition, especially for children and seniors, prompting food e-commerce platforms to offer filters for gluten-free, vegan, low-carb, and allergen-free products to meet these needs.

Key Market Segments

By Business Model

- B2C (Business-to-Consumer)

- B2B (Business-to-Business)

- Others

By Type

- Online Grocery Delivery

- Meal Kits

- Restaurant Meal Delivery

- Others

By Application

- Household

- Commercial

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Convenience and Changing Consumer Behavior

The rise of food e-commerce is significantly driven by the increasing demand for convenience and evolving consumer behaviors. Modern consumers prioritize time-saving solutions, leading to a preference for online grocery shopping and food delivery services.

The integration of user-friendly apps and websites has boosted food e-commerce by offering personalized recommendations, subscription models, and flexible delivery options. Diverse payment methods and real-time order tracking enhance trust. Businesses are expanding their digital presence and optimizing supply chains to meet growing demand, aligning with consumers’ desire for quick and convenient shopping experiences.

Restraint

Logistical Challenges in Delivery Infrastructure

Despite its growth, food e-commerce faces logistical challenges, especially in delivery infrastructure. Timely and efficient delivery of perishable goods requires a robust logistics network. Issues like traffic congestion, poor road infrastructure, and limited access to certain areas can cause delays and higher operational costs.

Moreover, maintaining the quality and freshness of perishable items during transit necessitates specialized equipment and temperature-controlled environments, adding to the complexity. Small and medium-sized enterprises (SMEs) often lack the resources to invest in advanced logistics solutions, putting them at a disadvantage compared to larger players with established delivery networks.

Opportunity

Expansion into Rural and Underserved Markets

An emerging opportunity in the food e-commerce sector lies in expanding services to rural and underserved markets. These areas often lack access to a wide variety of fresh and affordable food options due to limited physical retail presence.

E-commerce platforms can bridge this gap by providing residents with access to a broader range of products delivered directly to their homes. The expansion into these markets not only meets the demand for convenience but also promotes inclusivity and supports local economies.

However, tapping into rural markets requires tailored strategies to address unique challenges such as lower population density, limited internet connectivity, and logistical complexities. Investments in infrastructure, localized marketing, and partnerships with local suppliers can enhance service delivery and customer engagement in these regions.

Challenge

Ensuring Quality and Safety of Perishable Goods

A critical challenge in food e-commerce is maintaining the quality and safety of perishable goods throughout the supply chain. Unlike non-perishable items, perishable foods are sensitive to time and temperature fluctuations, requiring stringent handling and storage protocols.

Maintaining the cold chain from storage to transportation to delivery is essential to prevent spoilage and ensure food safety. Any breach in this chain can lead to product degradation, posing health risks to consumers and potential legal liabilities for businesses.

Implementing effective cold chain logistics involves significant investment in specialized equipment, real-time monitoring systems, and trained personnel. Additionally, compliance with food safety regulations and standards adds layers of complexity to operations.

Emerging Trends

One prominent trend is the rise of quick commerce (q-commerce), where companies like Alibaba and JD.com are investing heavily to ensure deliveries within 30 to 60 minutes, catering to the growing demand for rapid fulfillment. In India, Amazon has initiated trials for 15-minute grocery deliveries, highlighting the global shift towards ultra-fast delivery services .

Personalization is becoming increasingly important in the food e-commerce sector. Retailers are leveraging AI and data analytics to offer tailored product recommendations and shopping experiences, enhancing customer engagement and satisfaction. Additionally, sustainability is at the forefront of consumer concerns.

Transparency in product information is also gaining traction. Consumers now seek detailed information on ingredients, sourcing, and nutrition, leading companies to offer comprehensive product descriptions and certifications. Additionally, the subscription model is growing in popularity, providing convenience and cost savings through regular deliveries of preferred products.

Business Benefits

Embracing food e-commerce offers numerous advantages for businesses. Operational efficiency is another significant benefit. E-commerce platforms streamline the ordering process, reduce manual errors, and enable automation of inventory management, leading to cost savings and improved accuracy .

Running an online food business reduces expenses related to physical storefronts, such as rent and utilities. This cost-saving enables businesses to invest in better services and products. For example, food e-commerce platforms often have lower overhead costs compared to traditional brick-and-mortar stores .

Online platforms often include tools to track stock levels in real time, helping businesses manage inventory efficiently. This feature reduces waste and ensures that popular items are always available. Advanced inventory management features allow restaurants to keep track of their stock in real time .

Key Player Analysis

The food e-commerce market is growing rapidly as more consumers choose to shop for groceries and food products online.

Amazon.com, Inc. is a global e-commerce leader with a strong foothold in the food and grocery space through its platforms like Amazon Fresh and Whole Foods. Its continuous investment in AI and automation also gives it a competitive edge. Amazon’s scale and efficiency make it one of the most dominant players in food e-commerce today.

Alibaba.com, is a major force in Asia’s e-commerce market. Alibaba’s platforms, like Tmall and Freshippo (Hema), blend online and offline shopping for fresh food. Leveraging technology and big data, Alibaba optimizes its supply chain and delivery services, reinventing food retail in China and globally with smart stores and a seamless digital experience.

Blink Commerce Private Limited, known for its fast grocery delivery under the brand Blinkit (formerly Grofers), is making waves in India’s food e-commerce sector. Blinkit focuses on hyperlocal delivery and partnerships with local stores, making it highly relevant for the Indian market. This quick commerce model is becoming a trendsetter in the industry.

Top Key Players in the Market

- AEON CO., LTD.

- Alibaba.com.

- Amazon.com, Inc.

- Blink Commerce Private Limited

- Instacart

- JD.com, Inc.

- Natures Basket Limited.

- Deliveroo PLC

- DoorDash Inc.

- Delivery Hero Group

- Just Eat Limited

- Uber Technologies Inc.

- Swiggy

- Zomato

- Delivery.com LLC

- Yelp Inc.

- Amazon.com Inc.

- Rappi Inc.

- Others

Top Opportunities for Players

The global food e-commerce market is undergoing rapid transformation, presenting several key opportunities for industry players.

- Rapid Growth in Quick Commerce: The demand for ultra-fast delivery services is reshaping the food e-commerce landscape. Companies like JD.com and Alibaba are investing heavily in “instant retail,” aiming to deliver products within 30 to 60 minutes. This shift caters to consumers’ increasing expectations for speed and convenience in their shopping experiences.

- Expansion into Regional Markets: Food delivery services are extending their reach beyond urban centers into regional and underserved areas. For instance, Uber Eats has expanded its operations into several regional towns in South Australia, tapping into new customer bases and supporting local businesses.

- Integration of AI and Personalization: Advancements in artificial intelligence are enabling more personalized shopping experiences. Retailers are leveraging AI to offer tailored product recommendations, optimize delivery routes, and enhance customer service, thereby increasing customer satisfaction and loyalty.

- Growth of Subscription-Based Models: Subscription services for food and beverages are gaining popularity, particularly among younger consumers. These models provide convenience and cost savings, encouraging repeat purchases and fostering brand loyalty. Companies offering meal kits, specialty foods, or regular grocery deliveries are well-positioned to capitalize on this trend.

- Emphasis on Health and Sustainability: Consumers are increasingly prioritizing health and environmental sustainability in their purchasing decisions. There is a growing demand for organic, high-protein, and low-sugar food options, as well as products with sustainable packaging. Food e-commerce platforms that align with these values can attract health-conscious and environmentally aware customers.

Recent Developments

- In February 2025, Prosus agreed to acquire Just Eat Takeaway.com for €4.1 billion, aiming to create a leading European food delivery platform. This move will expand Prosus’s footprint beyond its current food delivery operations outside Europe, building on its successful growth strategies, such as its collaboration with iFood in Brazil.

- In July 2024, Delivery Hero merged its business teams of foodora, Yemeksepeti, and foodpanda to boost operational efficiency and streamline processes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 426.1 Bn |

| Forecast Revenue (2034) | USD 954.6 Bn |

| CAGR (2025-2034) | 8.40% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Business Model (B2C (Business-to-Consumer), B2B (Business-to-Business), Others), By Type (Online Grocery Delivery, Meal Kits, Restaurant Meal Delivery, Others), By Application (Household, Commercial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | AEON CO., LTD., Alibaba.com., Amazon.com, Inc., Blink Commerce Private Limited, Instacart, JD.com, Inc., Natures Basket Limited., Deliveroo PLC, DoorDash Inc., Delivery Hero Group, Just Eat Limited, Uber Technologies Inc., Swiggy, Zomato, Delivery.com LLC, Yelp Inc., Amazon.com Inc., Rappi Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |