Quick Navigation

Report Overview

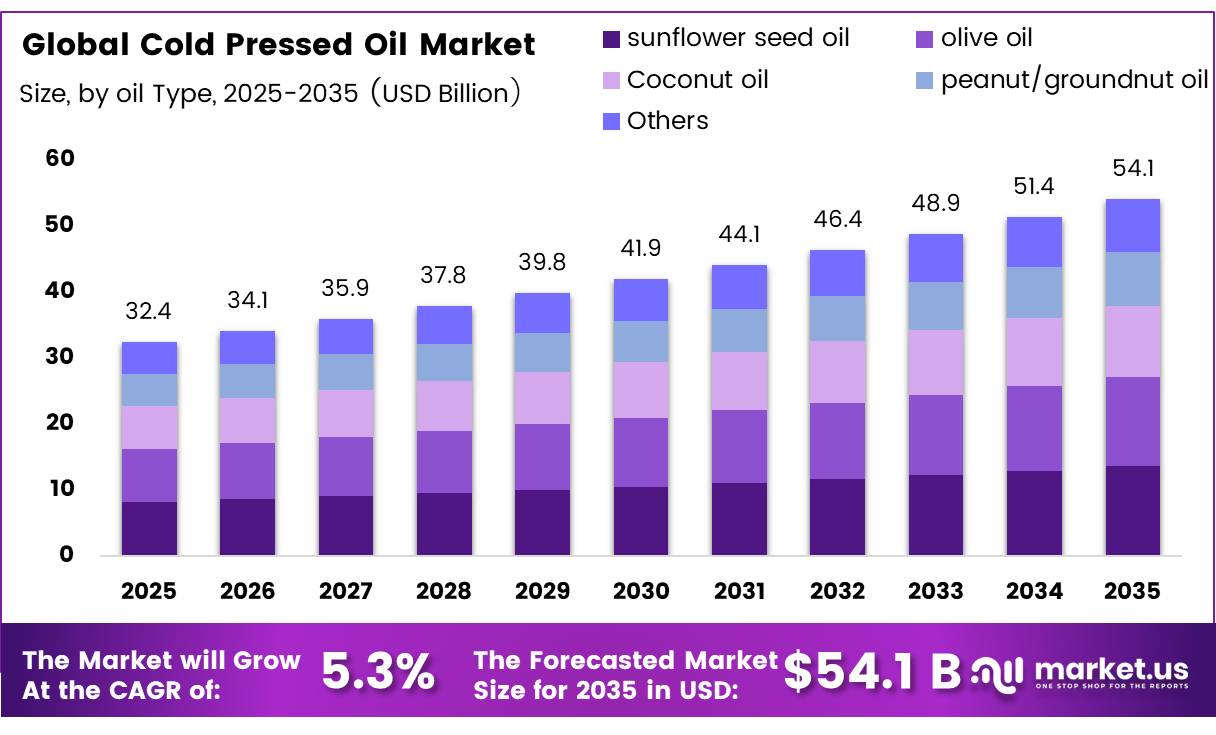

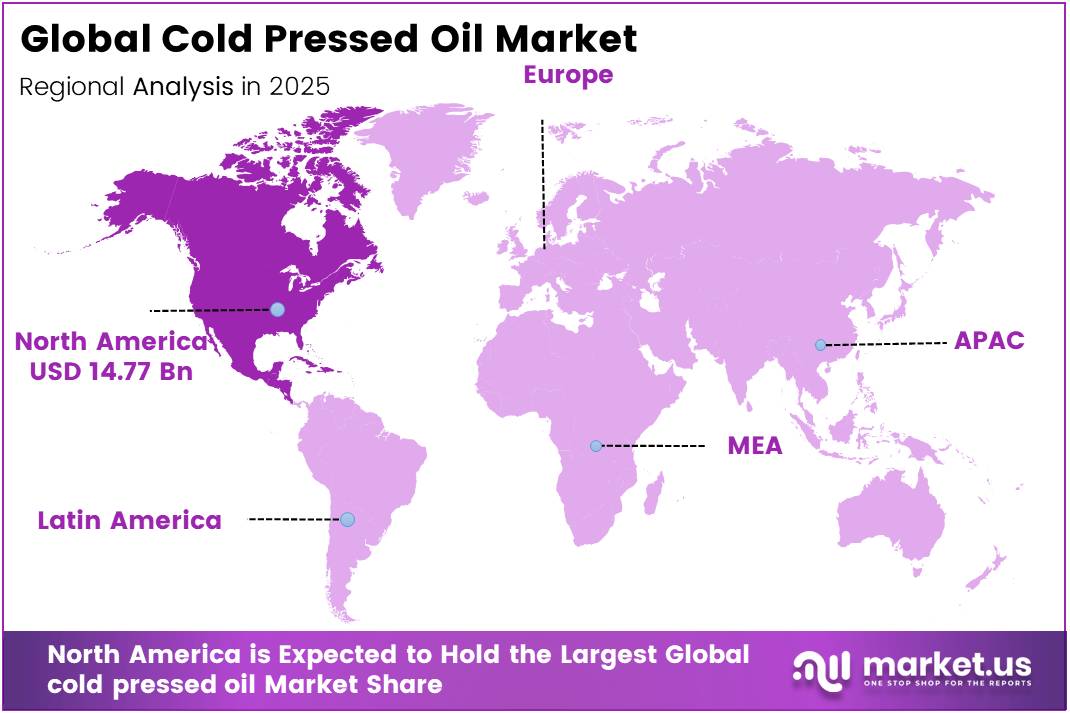

The global Cold Pressed Oil market was valued at USD 32.4 billion in 2025 and is expected to grow to USD 54.1 Billion in 2035. Between 2025 and 2035, this market is estimated to register a CAGR of 5.3%. In 2025, North America market, achieving over 45.6% share with a revenue of USD 14.77 Billion.

Cold pressed oil is a premium edible oil segment produced through mechanical extraction at low temperatures without the use of chemical solvents or extensive refining. The process helps retain natural antioxidants, vitamins, flavor compounds, and bioactive nutrients, making these oils increasingly preferred among health-conscious consumers.

- In January 2025, the International Olive Council (IOC) reported that global olive oil consumption was expected to reach 3,064,500 tonnes in the 2024/25 crop year, reflecting a 10% increase from the previous year.

- According to the International Olive Council (IOC) in January 2026, global olive oil production was provisionally estimated at 3,572,000 tonnes for the 2024/25 crop year, representing a 38% increase from the previous year. Subsequently, the IOC reported in February 2026 that global olive oil consumption reached 3,215,000 tonnes in the same crop year, reflecting a 15.3% increase compared with 2023/24.

Key Takeaways

- The global Cold Pressed Oil market was valued at USD 32.4 billion in 2025.

- The global market is projected to grow at a CAGR of 5.3% and is estimated to reach USD 54.1 billion by 2035.

- On the basis of oil type, sunflower seed oil dominated the market, constituting 30% of the total market share.

- Based on the nature, the organic dominated the market, with a substantial market share of around 45%.

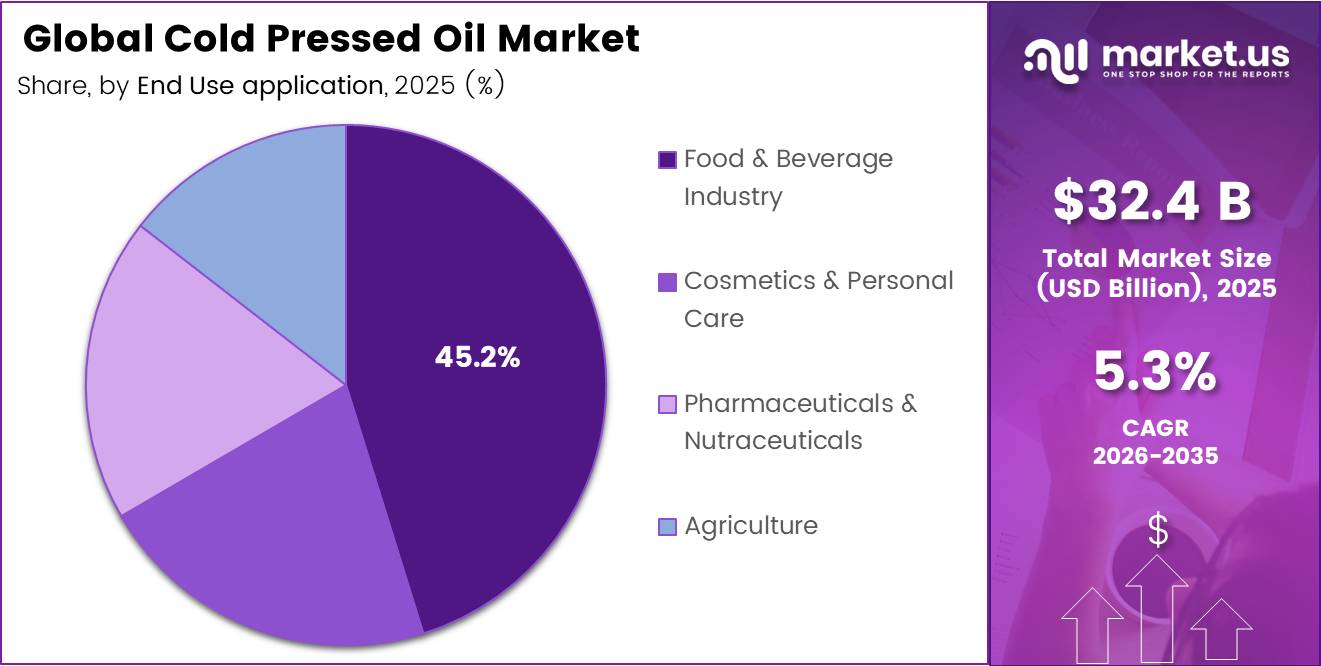

- Based on the end use application, Food & Beverage Industry led the market, comprising 45.2% of the total market.

- Among the distribution channel, online retail held a major share in the market, 35.6% of the market share.

- In 2025, the North America was the most dominant region in the market, accounting for 45.6% of the total global consumption.

The recovery in production and consumption highlights growing demand for premium and naturally processed edible oils, supporting the expansion of the cold pressed oil industry. These trends are encouraging investment in cold extraction technologies and value-added edible oil products.

Cold Pressed Oil Market Segment

By Oil Type Analysis

Sunflower Seed Oil represents dominant Segment in the Market.

Sunflower seed oil holds the largest share of the cold pressed oil market at 30.0%, a position reinforced by the sheer scale of its global agricultural base. According to the USDA Foreign Agricultural Service, April 2026, global sunflower seed oil production stood at 22.12 million metric tons in MY 2023/24, with output recorded at 20.47 million metric tons in MY 2024/25. The same publication notes that global sunflowerseed crush reached 48.38 million metric tons in MY 2024/25, reflecting sustained downstream processing demand.

Olive oil, representing a 25.0% share, is the fastest-growing segment within cold pressed oils. According to the USDA Economic Research Service, November 2024, global olive oil production is forecast to reach 3.1 million metric tons in MY 2024/25 a meaningful recovery after two consecutive drought-affected years that had driven global production as low as 2.4 million metric tons in MY 2023/24 With supply recovering, the EU’s domestic olive oil consumption alone is projected to grow 18% in MY 2024/25, while U.S. consumption is forecast to expand by 6% over the same period, reflecting broadening consumer interest in minimally processed, cold-pressed formats.

By Nature Analysis

Conventional Held a Major Share of Cold Pressed Oil Market

Conventional cold pressed oil holds the largest share of the market at 55.0%, underpinned by the vast scale of non-organic oilseed cultivation globally. According to the USDA NASS Crop Production Summary, January 2026, U.S. soybean production in 2025 totalled 4.26 billion bushels harvested across 80.4 million acres the overwhelming majority of which is conventionally farmed and feeds downstream oil processing including cold press applications The USDA ERS further noted, as of August 2025, that U.S. soybean harvested acreage has remained concentrated in high-yield conventional production systems, with an estimated 87.1 million acres recorded in 2024

Organic cold pressed oil, is the fastest-growing segment. The USDA NASS 2021 Organic Survey further recorded 17,445 certified organic farms in operation a 5% increase from 2019 signalling a steady expansion of the organic agricultural base supporting this segment.

End Use Application Analysis

Cold Pressed Oil Are Mostly Utilized in Food & Beverage.

The dominant segment is the Food & Beverage industry, holding a 45.2% share of the global cold pressed oil market. More and more people are choosing oils that are natural, minimally processed, and free from unnecessary additives. This shift toward cleaner, healthier eating habits has driven demand not just in households, but also in restaurants and among food manufacturers who want to meet that growing expectation.

The fastest growing segment is Cosmetics & Personal Care. The beauty industry is racing to catch up. Consumers are increasingly moving away from synthetic ingredients and turning to plant-based, chemical-free alternatives. Cold pressed oils known for their moisturizing, antioxidant, and skin-nourishing qualities are a natural fit for skincare formulations, making them a go-to choice for brands leaning into organic and sustainable beauty.

Distribution Channel Analysis

Online Retail Dominated the Cold Pressed Oil Market, While Specialty Stores Emerged as the Fastest-Growing Segment

Online retail commands the largest share of the cold pressed oil market at 35.6%, a position driven by consumers’ growing preference for convenient, comparison-friendly purchasing of specialty food products. According to the U.S. Census Bureau, May 2026, U.S. retail e-commerce sales for Q1 2026 reached USD 326.7 billion a 9.8% increase from Q1 2025 while total retail sales grew just 3.9% over the same period, underscoring the sustained structural shift of consumer spending toward digital channels. This divergence between e-commerce and overall retail growth reflects the degree to which online platforms have become the primary discovery and purchase touchpoint for health-oriented specialty products, including cold pressed oils.

Supermarkets and hypermarkets represent the fastest-growing offline channel. According to the USDA Economic Research Service, February 2024, approximately 1 in 5 U.S. grocery shoppers (19.3%) had purchased groceries online at least once in the prior 30 days meaning the overwhelming majority of food purchases still flow through physical retail formats. The sustained footfall in large-format grocery environments continues to position supermarkets and hypermarkets as a meaningful and expanding touchpoint for cold pressed oil discovery and repeat purchase.

Key Market Segments

By Oil Type

- Coconut oil

- olive oil

- sunflower seed oil

- peanut/groundnut oil

- Others

By Nature

- Organic

- Conventional

By End-Use Application

- Food & Beverage Industry

- Cosmetics & Personal Care

- Pharmaceuticals & Nutraceuticals

- Agriculture

By Distribution Channel

- Online Retail

- Supermarkets and Hypermarkets

- Departmental & Convenience Stores

- Specialty Stores

Drivers

Organic and premium grocery expansion

A second major driver is the expansion of organic and premium grocery channels, which gives cold-pressed oils shelf space and merchandising context that did not exist at the same scale a decade ago. The U.S. organic market reached $76.6 billion in 2025 according to the Organic Trade Association, while Germany’s organic sales hit a record EUR 17 billion in 2024 and were projected to rise further, supported by large retail chains. More broadly, global organic food markets are expanding at double-digit rates into 2035, reinforcing that premium, health-oriented packaged foods are gaining distribution breadth rather than remaining niche specialist products.

Cold-pressed oils benefit disproportionately from this because they sit naturally inside organic, natural, gourmet, and wellness aisles where consumers already expect premium pricing, smaller pack sizes, and provenance-led storytelling. This adds an estimated +1.5 percentage points to CAGR by lowering discovery friction, increasing premium retail penetration, and helping brands scale through modern trade rather than relying only on health stores or local specialty channels.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label and minimally processed food preference | +1.9% | North America core, Europe core, India metros, APAC urban | Short term (≤ 2 years) |

| Organic and premium grocery expansion | +1.5% | North America, Europe, India, affluent APAC | Medium term (2-4 years) |

| E-commerce and D2C premium oil discovery | +1.4% | India core, North America, Southeast Asia, Middle East urban | Short term (≤ 2 years) |

| Traditional oil revival in emerging markets | +1.3% | India core, Southeast Asia, Middle East, Africa spill-over | Medium term (2-4 years) |

| Wellness and personal-care cross-usage | +1.1% | North America, Europe, India, Japan, Korea | Medium term (2-4 years) |

| Premiumization within edible-oil baskets | +1.2% | Global, strongest in urban middle-income markets | Long term (≥ 4 years) |

Restraints

Feedstock and edible-oil price volatility

A second major restraint is raw-material and edible-oil price volatility, because cold-pressed oil producers operate with thinner processing buffers than heavily scaled refined-oil players and therefore pass volatility through more directly to end consumers. The FAO Vegetable Oil Price Index averaged 185.0 points in May 2026, down 4.6% month on month but still coming after several months of increases at the start of 2026, while sector commentary in India indicates edible-oil prices had been rising steadily since late OY2025 and accelerated in OY2026 due to global supply disruptions and biofuel demand.

Import-dependent markets feel this more acutely: where seed or crude-oil inputs are exposed to weather shocks, trade policy, freight swings, and currency depreciation, brand owners must either absorb margin compression or raise MRP in a category already carrying a premium. This creates a double penalty—higher procurement cost and weaker affordability—particularly for sunflower, sesame, groundnut, and specialty seed oils with smaller sourcing pools than commodity palm or soybean. The modeled drag is 1.4 percentage points because volatility reduces pricing confidence, complicates inventory planning, and discourages aggressive expansion into mainstream retail where stable price architecture is essential.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing and affordability gap | -1.8% | India, Southeast Asia, Africa, price-sensitive Europe | Short term (≤ 2 years) |

| Feedstock and edible-oil price volatility | -1.4% | Global, strongest in import-dependent Asia | Short term (≤ 2 years) |

| Shorter shelf life and oxidation risk | -1.2% | Global retail, e-commerce, warm-climate markets | Medium term (2-4 years) |

| Competition from refined low-cost oils | -1.1% | Global mass market, especially Asia and Africa | Medium term (2-4 years) |

| Limited mainstream distribution depth | -0.9% | Rural Asia, Africa, Latin America, value retail | Medium term (2-4 years) |

| Inconsistent consumer education and claims trust | -0.8% | North America, Europe, India, digital-first channels | Long term (≥ 4 years) |

Opportunity

Private-label premium retail partnerships

Private-label expansion is a clear whitespace because large retailers and specialty chains increasingly want premium, identity-preserved, organic, non-GMO, or high-oleic oils under their own banners, yet many cold-pressed oil producers still prioritize branded growth alone. Supplier-side market intelligence in 2026 explicitly notes rising private-label demand for specialty and identity-preserved oils, while broader private-label edible-oil playbooks show retailers can capture margins of roughly 25%–40% at the brand owner level and 15%–30% at retail when well-structured manufacturing partnerships are in place.

For cold-pressed oil processors, this is not a baseline driver because it requires deliberate channel strategy, B2B packaging capability, and quality assurance suited to retailer procurement rather than consumer brand-building. The upside is strategically attractive because private label can accelerate volume scale, improve plant utilization, lower go-to-market cost, and open access to premium retail shelves without the same level of consumer advertising spend. The modeled +1.4 percentage-point CAGR uplift reflects the fact that private-label cold-pressed oils remain underdeveloped in Europe, North America, and India’s modern trade, even though retailer demand for premium own-brand assortments is rising.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Nutraceutical and functional-oil extensions | +1.8% | North America, Europe, India, affluent APAC | Medium term (2-4 years) |

| D2C subscriptions and refill programs | +1.5% | India core, North America, Southeast Asia, GCC urban | Short term (≤ 2 years) |

| Private-label premium retail partnerships | +1.4% | Europe, North America, India modern trade | Short term (≤ 2 years) |

| Tier-2 and Tier-3 city penetration | +1.6% | India core, Southeast Asia, Africa urbanizing markets | Medium term (2-4 years) |

| Beauty and personal-care ingredient pivot | +1.1% | North America, Europe, Japan, Korea, India | Long term (≥ 4 years) |

| Specialty seed-oil portfolio expansion | +1.3% | North America, Europe, APAC health niches | Medium term (2-4 years) |

Challenges

Shelf-life and storage control

A recurring technical challenge is maintaining product integrity through storage and distribution, because cold-pressed oils are more vulnerable to oxidation, heat exposure, light damage, and off-flavor development than heavily refined oils. Scientific evidence on cold-pressed rapeseed oil shows that low-temperature storage at 4°C is optimal for maintaining quality, highlighting how sensitive these oils can be to storage conditions over time. Yet in real-world retail and e-commerce chains, products often move through ambient warehouses, non-temperature-controlled last-mile systems, and warm-climate shelves where exposure to light and heat is inconsistent and difficult to monitor.

This creates an operational mismatch: the category sells “freshness” and nutrient retention, but the distribution stack frequently behaves like a standard ambient grocery chain. As a result, brands face higher return rates, shorter effective sell-through windows, and more pressure to use expensive protective packaging or conservative expiry policies. The modeled drag of 0.9 percentage points on potential CAGR reflects that the market can keep growing, but doing so at scale requires better packaging science, better inventory rotation, and more disciplined storage control than many current distribution systems can reliably provide.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Adulteration and traceability gaps | -1.2% | India core, EU premium markets, APAC exports | Medium term (2-4 years) |

| Import-linked supply volatility | -1.0% | India, Middle East, Africa, import-heavy Asia | Medium term (2-4 years) |

| Shelf-life and storage control | -0.9% | Global, strongest in hot-climate retail | Medium term (2-4 years) |

| SME quality-control capability | -0.8% | India, Southeast Asia, Africa, fragmented producer bases | Long term (≥ 4 years) |

| Packaging-cost and format optimization | -0.7% | Global premium retail and e-commerce channels | Short term (≤ 2 years) |

| Consumer trust and label verification | -0.8% | North America, Europe, India, online-first markets | Medium term (2-4 years) |

Geopolitical Impact Analysis

Geopolitical situations are becoming more influential in the market for cold pressed oil. Political situations such as trade issues, wars, and alterations in export policy can result in disruption in the supply of raw materials as well as increase the cost of production. The war between Russia and Ukraine is an example where there have been problems with the supply of sunflower oil, and the restriction in the exporting of edible oils from producers such as India and Indonesia has affected the supply situation globally.

Disruptions in shipping channels, including those in the Red Sea, have also led to an increase in transport prices and delays in delivery of cold pressed oils. Key ingredients such as coconut in Southeast Asia, olive in the Mediterranean, and sesame and mustard in India make up the main raw materials used. Any changes in the form of political unrest or trade policies in any of these regions would immediately impact the availability and price of these products. Moreover, growing tension between countries would mean unpredictability in terms of trade regulations.

Regional Analysis

North America leads the market with a 45.6% share, supported by strong consumer preference for healthy and natural food products. The growing popularity of organic diets, clean-label products, and premium cooking oils continues to drive demand across the region. In addition, advanced retail networks, higher health awareness, and increasing spending on wellness products are strengthening market growth.

Europe remains another important market for cold-pressed oils, driven by rising demand for sustainable, plant-based, and minimally processed products. Consumers in the region are increasingly choosing natural oils for both food and personal care applications, while strict quality standards and growing environmental awareness continue to support product adoption.

Key Regions and Countries Covered

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The cold-pressed oil business is still fragmented to some degree, with no one firm controlling a large majority market share globally. The leading firms vary according to regions, product category, and channel of distribution. There is greater brand concentration within premium and organic products, but traditional and regional oils have remained scattered among smaller firms. The fragmented nature of the industry means that quality of product, visibility in the supply chain, and choice of channel are often more important than size alone when it comes to market position.

The market for cold-pressed oils is one in which competition consists of a tiered structure in which size, focus, and technology compete together. In a situation where the regional market share distribution still stands, efforts at investment in sourcing, product development, omni-channel selling, and sustainability have already begun to shift competitive dynamics. Businesses that ensure consistent quality along with branding and consumer awareness will benefit most from this dynamic change in competitiveness.

The Major Players In The Industry

- Cargill, Incorporated

- Wilmar International Limited

- Archer Daniels Midland Company

- Bunge Limited

- Louis Dreyfus Company

- CHS Inc.

- Fuji Oil Holdings Inc.

- Olam Group Limited

- Marico Limited

- Adani Wilmar Limited

- Patanjali Foods Limited

- Ruchi Soya Industries Limited

- Savola Group

- Associated British Foods plc

- Conagra Brands, Inc.

- Other Players

Key Development

- In May 2024, Adani Wilmar Limited launched Fortune Pehli Dhaar First-Pressed Mustard Oil in bottles and pouches, targeting consumers seeking traditionally extracted, minimally processed cold pressed oil formats marking a direct expansion into the premium cold pressed segment within its branded edible oil portfolio.

- In June 2025, Marico Limited launched the Saffola Dual Seed Cold Pressed Oils range, including a mustard variant, expanding its product portfolio to address growing consumer demand for health-focused, cold pressed cooking oils across mainstream retail channels

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 32.4 Bn |

| Forecast Revenue (2035) | USD 54.1 Bn |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Oil Type (Coconut oil, olive oil, sunflower seed oil, peanut/groundnut oil, Others), By Nature (Conventional, Organic), By End Use Application(Food & Beverage Industry, Cosmetics & Personal Care, Pharmaceuticals & Nutraceuticals, Agriculture), By Distribution Channel(Online Retail, Supermarkets and Hypermarkets , Departmental & Convenience Stores, Specialty Stores) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Cargill, Incorporated, Wilmar International Limited, Archer Daniels Midland Company, Bunge Limited, Louis Dreyfus Company, CHS Inc., Fuji Oil Holdings Inc., Olam Group Limited, Marico Limited, Adani Wilmar Limited, Patanjali Foods Limited, Ruchi Soya Industries Limited, Savola Group, Associated British Foods plc, Conagra Brands, Inc. Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |