Quick Navigation

Report Overview

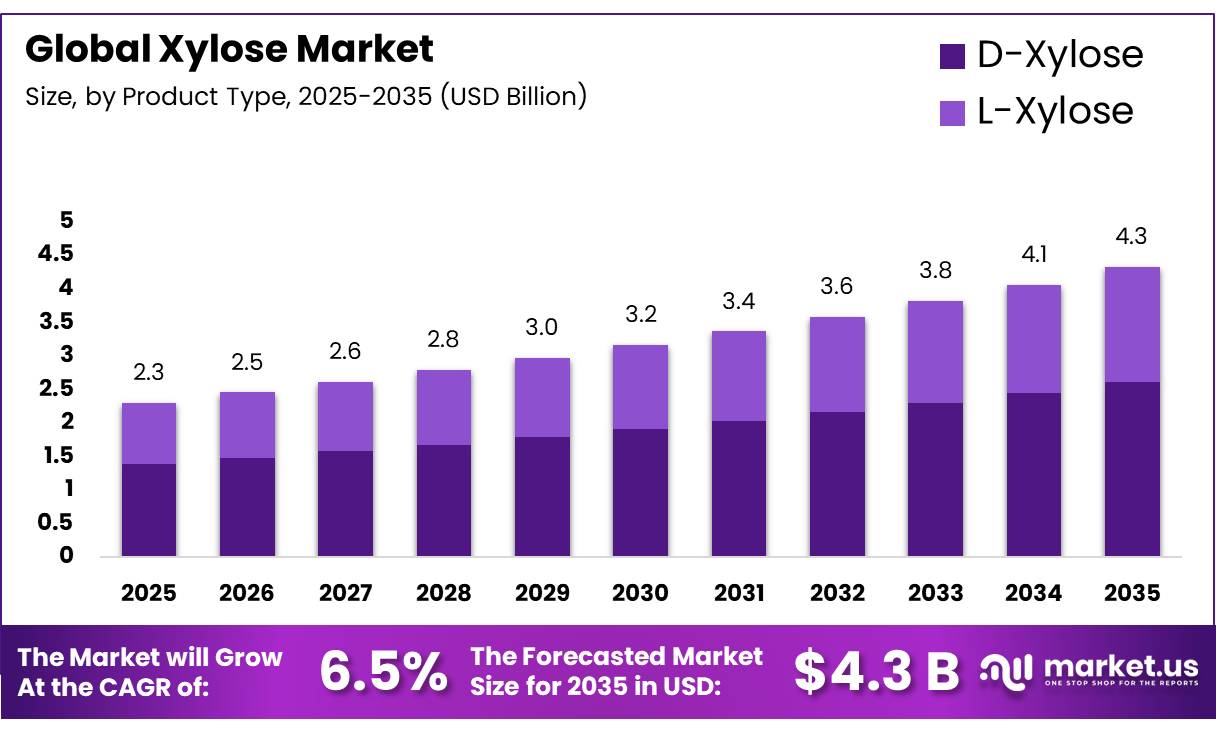

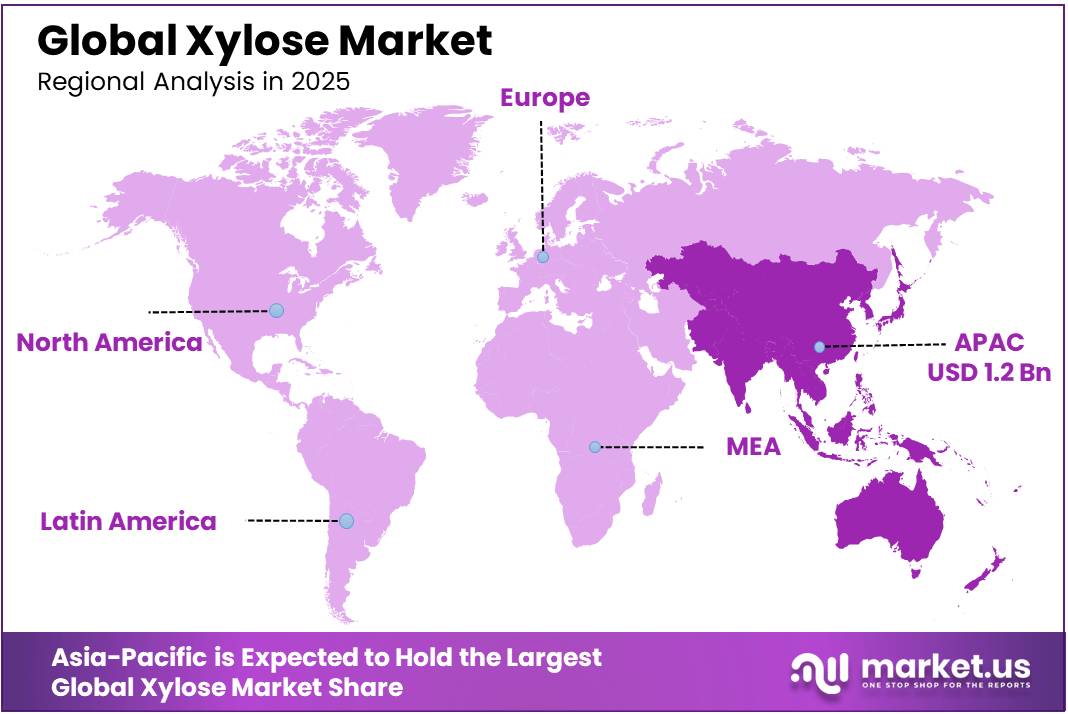

In 2025, the Global Xylose Market was valued at USD 2.3 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 6.5%, reaching about USD 4.3 billion by 2035. In 2025, Asia Pacific led the market, achieving over 52.0% share with a revenue of USD 1.2 Billion.

Xylose is a naturally occurring five-carbon sugar (pentose) widely found in hemicellulose-rich biomass such as corn cobs, hardwoods, agricultural residues, and sugarcane bagasse. It serves as a critical intermediate in the production of xylitol, bio-based chemicals, pharmaceuticals, food ingredients, and renewable fuels. The growing emphasis on sustainable ingredients and biomass utilization has increased industrial interest in xylose extraction and conversion technologies.

- In March 2024, according to the U.S. Department of Energy (DOE), lignocellulosic biomass represents the largest renewable carbon source available for industrial applications, with the United States alone generating more than 1 billion dry tons of biomass resources annually under long-term sustainable scenarios.

Key Takeaways

- The Global Xylose Market was valued at USD 2.3 billion in 2025.

- The global Xylose market is projected to grow at a CAGR of 6.5% and is estimated to reach USD 4.3 billion by 2035.

- D-Xylose is the dominant product type, accounting for 60.3% of the market in 2025, driven by its widespread use as a sugar substitute and flavoring precursor across food processing and pharmaceutical manufacturing.

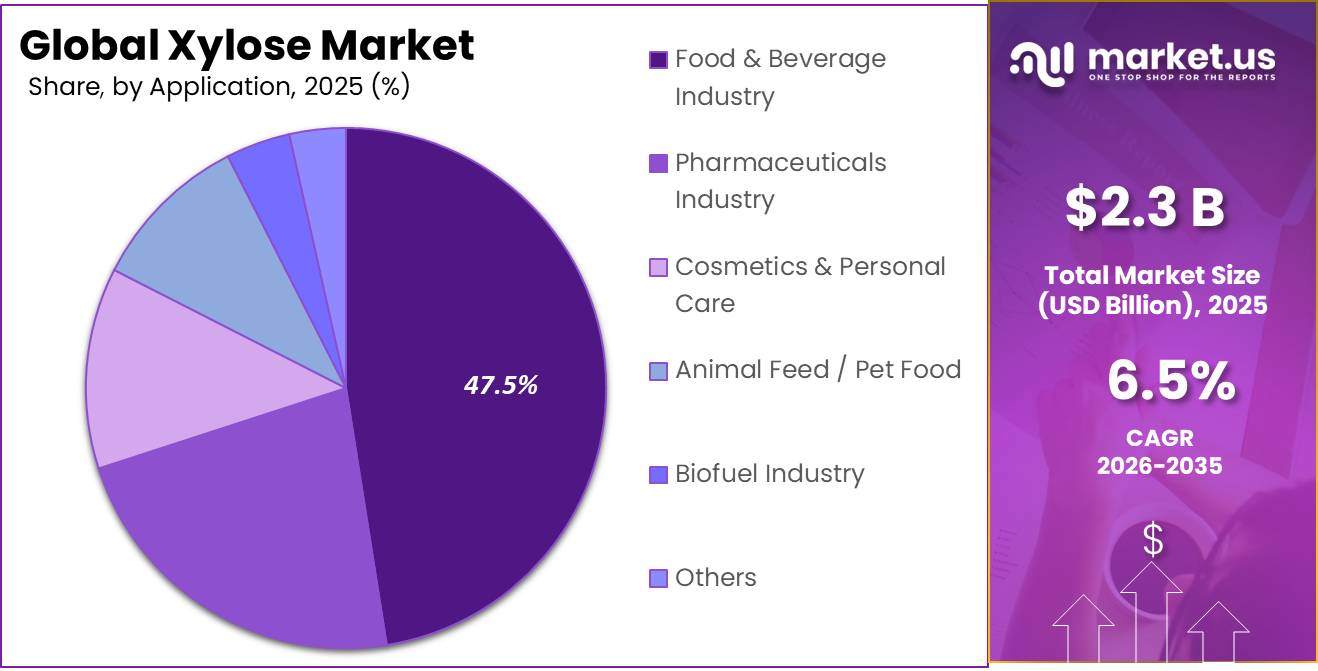

- Food & Beverage Industry is the dominant application segment at 47.5%, driven by the extensive use of xylose as a low-calorie sweetener and Maillard reaction agent in processed food formulations.

- Powder form is the dominant form at 85.1%, driven by its superior shelf stability, ease of handling, and compatibility with dry-blending operations across food and pharmaceutical manufacturing.

- Corncobs is the dominant source at 50.4%, driven by their high hemicellulose content and abundant availability as an agricultural byproduct across major xylose-producing regions.

- Asia Pacific holds the largest regional share at 52.0%, driven by the concentration of xylose production capacity and raw material availability particularly corncob processing across China and other major biomass-rich economies in the region.

The industrial landscape for xylose is strongly linked to advancements in biorefinery operations and the expanding market for low-calorie sweeteners. Xylose is the primary feedstock used in xylitol manufacturing, a sweetener extensively utilized in sugar-free foods, chewing gums, and oral care products. The European Food Safety Authority (EFSA) recognizes xylitol’s contribution to maintaining tooth mineralization and reducing dental plaque formation, supporting its growing application in food and healthcare sector. U.S. regulation permits xylitol as a food additive for special dietary uses under 21 CFR 172.395. It should not be described simply as an FDA GRAS classification.

The xylose demand is the increasing global shift toward healthier food formulations and sugar reduction strategies.

- In January 2026, the World Health Organization reaffirmed that free sugars should remain below 10% of total daily energy intake, equal to about 50 grams or 12 teaspoons for a person consuming 2,000 calories per day. WHO added that reducing intake to 5% or less, around 25 grams or 6 teaspoons, may deliver further health benefits. This guidance continues to encourage food and beverage reformulation and supports demand for reduced-sugar ingredients such as xylitol derived from xylose.

Future opportunities are expected to emerge from sustainable aviation fuel, bioethanol, and biochemical production pathways that utilize pentose sugars. As industries seek greater utilization of lignocellulosic feedstocks, xylose is becoming increasingly important in integrated biorefineries that aim to maximize biomass value. Continuous advancements in enzymatic hydrolysis, microbial fermentation, and biomass processing technologies are expected to strengthen xylose’s role as a key renewable platform sugar in the global food, chemical, and bio-based industrial ecosystem.

Xylose Market Segmentation

Product Type Analysis

D-Xylose dominates the market with a 60.3% share due to its extensive use in food sweeteners and bio-based manufacturing

In 2025, D-Xylose held a dominant market position, capturing 60.3% share. The segment’s strong position was supported by its widespread commercial use as the primary feedstock for xylitol production and other bio-based ingredients. D-Xylose is commonly produced from agricultural biomass such as corn cobs and hardwood residues, making it the most accessible and economically viable form of xylose for industrial applications.

- The availability of raw materials remained favorable, with the Food and Agriculture Organization (FAO) reporting global maize production of approximately 1.22 billion tonnes in 2024, providing a significant source of biomass for xylose extraction. These factors helped D-Xylose maintain its leading position across food, pharmaceutical, and industrial biotechnology applications during 2025.

L-Xylose is the fastest growing segment in 2026. Growth of the segment is being driven by increasing interest in specialty sugars used in advanced biochemical research, pharmaceutical development, and high-value bio-based products. Although its commercial scale remains smaller than D-Xylose, ongoing innovation in biotechnology and carbohydrate processing is expanding its application scope. As investments in sustainable bioeconomy projects continue to increase, the segment is expected to benefit from broader development of specialty bio-based chemicals and innovative industrial applications.

Application Analysis

Food & Beverage Industry dominates the market with a 47.5% share due to rising demand for sugar alternatives and functional ingredients

In 2025, Food & Beverage Industry held a dominant market position, capturing a 47.5% share. The segment continued to lead the market as xylose remained an important raw material for producing xylitol and other specialty sweeteners used in sugar-free and reduced-sugar food products. Demand was supported by the expanding global food processing sector and growing interest in healthier ingredient formulations.

- According to the United States Department of Agriculture (USDA), global sugar production for the 2025/26 season reached approximately 189.3 million metric tons, encouraging food manufacturers to develop alternative sweetening solutions that can help reduce sugar content in finished products.

Pharmaceuticals Industry is the fastest growing segment in 2026. Growth is being supported by increasing utilization of specialty sugars and carbohydrate-based compounds in pharmaceutical research and formulation development. Xylose is used in various biochemical and analytical applications, while advances in biotechnology are creating new opportunities for its use in specialty healthcare products. Rising investment in pharmaceutical innovation and bio-based ingredient development continues to support demand from the sector.

Form Analysis

Powder form dominates the market with an 85.1% share due to its ease of storage, handling, and industrial use

In 2025, Powder held a dominant market position, capturing more than 85.1% share. The segment remained the preferred form of xylose across food, pharmaceutical, and biotechnology industries because of its longer shelf life, ease of transportation, and compatibility with large-scale manufacturing processes. Powdered xylose is widely used in xylitol production, food ingredient formulations, and fermentation applications, where accurate dosing and stable storage conditions are important. The segment also benefited from the expanding global processed food industry.

- The Food and Agriculture Organization (FAO) estimated global cereal production at approximately 2.85 billion tonnes in 2024, supporting the availability of agricultural feedstocks used in bio-based sugar production. These factors helped powdered xylose maintain its leading position across industrial applications during 2025.

Liquid is the fastest growing segment in 2026. The segment is gaining momentum due to its suitability for industrial fermentation, biotechnology processes, and liquid ingredient formulations. Liquid xylose can be directly incorporated into bioprocessing systems, reducing additional dissolution steps and improving operational efficiency in certain applications. Growing investments in bio-based chemicals, renewable fuels, and advanced fermentation technologies are creating new opportunities for liquid-form xylose.

Source Analysis

Corncobs dominate the market with a 50.4% share due to their high xylose content and wide availability

In 2025, Corncobs held a dominant market position, capturing more than a 50.4% share. The segment maintained its leading position because corncobs are among the most widely used raw materials for commercial xylose extraction. They contain significant amounts of hemicellulose, which can be efficiently processed into xylose and further converted into value-added products such as xylitol. The strong availability of corn-based agricultural residues continued to support the segment’s growth.

- According to the United States Department of Agriculture (USDA), global corn production for the 2025/26 marketing year is projected to reach approximately 1.27 billion metric tons, ensuring a substantial supply of corncob feedstock for industrial applications.

Wheat Straw is the fastest growing segment in 2026. Growth of the segment is being supported by rising interest in the utilization of agricultural by-products for sustainable chemical and ingredient production. Wheat straw contains substantial hemicellulose content, making it a suitable feedstock for xylose extraction and biorefinery applications. Increasing efforts to reduce agricultural waste and improve biomass utilization are encouraging manufacturers to explore wheat straw as an alternative source of xylose. As investments in renewable materials and circular bioeconomy projects continue to expand, wheat straw is expected to gain greater importance in commercial xylose production.

Key Market Segments

By Product Type

- D-Xylose

- L-Xylose

By Application

- Food & Beverage Industry

- Pharmaceuticals Industry

- Cosmetics & Personal Care

- Animal Feed / Pet Food

- Biofuel Industry

- Others

By Form

- Powder

- Liquid

By Source

- Corncobs

- Wheat Straw

- Cottonseed Hulls

- Others

Driver Analysis

Biorefinery valorization of hemicellulose streams

A structural medium-term driver is the shift from single-output biomass processing toward multi-product biorefinery monetization, where xylose becomes a higher-value outlet for the hemicellulose fraction rather than a by-product with weak pricing power. USDA-linked research notes that around 30% of plant carbohydrates are made from xylose and that effective recovery of hemicellulose sugars is critical for good total-sugar yields, while USDA training materials on crop residues describe corn stover as roughly 45% cellulose, 30% hemicellulose, and 25% lignin.

That composition matters because every percentage-point gain in hemicellulose conversion raises the revenue density of a residue-processing asset without requiring a proportional increase in feedstock collection cost. Commercially, this pushes producers toward integrated models spanning furfural, xylitol intermediates, fermentation substrates, and specialty ingredients, improving return on capital and making xylose capacity additions more financeable; this underpins the estimated +1.6 percentage-point uplift over the medium term.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Added-sugar compliance demand in reformulated foods | +1.9% | North America core, EU, APAC packaged food hubs | Short term |

| Corn abundance lowers carbohydrate feedstock risk | +1.4% | U.S. core, Latin America spill-over, APAC importers | Short term |

| Biorefinery valorization of hemicellulose streams | +1.6% | North America core, EU biobased cluster, China industrial corridors | Medium term |

| Label-led shift toward low-calorie sweetener systems | +1.2% | U.S. core, Canada, Western Europe | Medium term |

| Novel-food and ingredient authorization friction in EU | +0.8% | EU constrained, North America and Asia relatively advantaged | Medium term |

| Residue-to-chemical policy support for biomass utilization | +1.1% | U.S. bioeconomy regions, EU circular economy zones, Brazil spill-over | Long term |

Restraint Analysis

Low xylan conversion yields

A second major restraint is the still-imperfect efficiency of converting hemicellulose into marketable xylose at industrially attractive yields, because USDA ARS research continues to frame recalcitrant xylan structures as a technical barrier and explicitly targets improved enzyme systems to increase sugar availability in biorefinery processes. Separate USDA ARS commercial-integration work indicates that even for optimized pretreatment and hydrolysis, development targets are only to maintain at least 70% of original hemicellulose during pretreatment, achieve at least 50 g/L of total sugars in hydrolysate, and exceed 75% of theoretical sugar yields, which implies that material losses and process inefficiencies remain economically relevant at demonstration-to-commercial scale.

For xylose producers, every 5 to 10 percentage-point shortfall versus theoretical recovery can dilute plant contribution margins through higher enzyme loading, more severe pretreatment, lower throughput utilization, and elevated wastewater handling, while also making downstream purification less competitive against established sweetener alternatives. The resulting effect is slower scale-up, longer payback periods, and more conservative offtake contracting, supporting a -1.7 percentage-point drag on forecast CAGR over the medium.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU novel-food barrier | -2.1% | EU core, UK spill-over | Medium term |

| Low xylan conversion yields | -1.7% | North America core, China, EU biorefineries | Medium term |

| Weak scale economics | -1.4% | North America, EU, APAC corridors | Long term |

| Food-label reformulation complexity | -1.1% | U.S. core, Canada, Western Europe | Short term |

| Residue logistics bottleneck | -1.3% | U.S. Midwest core, Brazil, China inland | Medium term |

| Commodity-linked price pressure | -0.9% | Global, especially import-dependent APAC | Short term |

Opportunity Analysis

Xylitol-chain integration

The most commercially attractive adjacent white space is forward integration from xylose into xylitol or other higher-value derivatives, because USDA ARS publications explicitly identify xylose as a five-carbon sugar that can be biochemically converted into a wide array of products rather than sold only as a standalone ingredient. This matters strategically because xylose as a primary product can face price ceilings, but integrated conversion into derivatives improves revenue per ton of recovered pentose, spreads fixed pretreatment and purification costs across a richer product slate, and can expand EBITDA margins by an estimated 500 to 900 basis points for assets that achieve stable hydrogenation or fermentation yields and commercial offtake.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| EU authorization unlock | +2.3% | EU core, UK spill-over | Medium term |

| Xylitol-chain integration | +1.9% | North America core, China, EU specialty ingredients | Medium term |

| Residue biorefinery clustering | +1.7% | U.S. Midwest, Brazil, China inland | Long term |

| Reformulation platform sales | +1.5% | U.S. core, Canada, Western Europe | Short term |

| Fermentation-grade monetization | +1.2% | North America, EU biotech hubs, APAC industrial biotech | Medium term |

| Ag-waste M&A roll-up | +1.0% | North America core, EU circular-economy zones | Long term |

Challenges Analysis

Xylan conversion inefficiency

The central technical challenge is that xylose output remains constrained by incomplete conversion of xylan-rich biomass, because USDA ARS research still frames recalcitrant xylan structures as a core bottleneck and continues to prioritize enzyme systems that improve sugar release for biorefinery processes.

For commercial plants, this translates into lower mass yield, higher enzyme loading, more off-spec hydrolysate, and a 6 to 12 percent hit to effective throughput versus theoretical design cases, which then compresses gross margin and lengthens payback periods on new capacity. Because the industry can keep selling into existing channels while engineering improves incrementally, this is a challenge rather than a hard restraint, but it still imposes roughly -1.8 percentage points of CAGR friction through 2026–2030.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Xylan conversion inefficiency | -1.8% | North America core, EU biorefineries, APAC industrial biotech | Medium term |

| Residue collection variability | -1.4% | U.S. Midwest, Brazil, China inland | Medium term |

| Food-grade quality drift | -1.2% | North America core, EU food hubs, Japan/Korea | Short term |

| Low commercial enzyme depth | -1.1% | North America, EU, China biotech clusters | Long term |

| Label-claim execution risk | -0.9% | U.S. core, Canada, Western Europe | Short term |

| Site-level sustainability limits | -0.8% | U.S. corn belt, EU circular zones | Long term |

Geopolitical Impact Analysis

Rising Trade Uncertainty and Supply Chain Pressures Influence the Xylose Market.

The current geopolitical tensions and ongoing conflicts in parts of Eastern Europe and the Middle East have created new challenges for the global xylose market in 2025 and 2026. Higher freight costs and shipping disruptions have increased the expense of moving agricultural feedstocks such as corn and wheat residues, which are widely used in xylose production. Several manufacturers have faced longer delivery times for raw materials and processing chemicals due to congestion at key logistics hubs and changes in trade flows. At the same time, volatility in energy prices has raised production costs for biomass processing facilities, particularly in regions that rely on imported fuel and industrial inputs.

The market has also witnessed a gradual shift toward regional sourcing strategies. Producers are increasingly seeking local agricultural residues to reduce dependence on long-distance supply chains and improve supply security. This trend has encouraged investments in domestic biomass utilization and biorefinery projects across several countries. Demand for xylose remains supported by its role in food ingredients, xylitol production, and bio-based chemicals. As companies strengthen supply chain resilience and diversify sourcing networks, the market is expected to maintain stable growth while adapting to the evolving geopolitical landscape.

Regional Analysis

Asia-Pacific Leads the Xylose Market with a 52.0% Share, Supported by Strong Agricultural Feedstock Availability.

Asia-Pacific emerged as the dominant region in the global xylose market, accounting for 52.0% of the market and reaching a value of approximately USD 1.2 billion in 2025. The region’s leadership is largely attributed to its extensive agricultural production, particularly corn and other biomass feedstocks used in commercial xylose extraction. Countries across the region continue to benefit from well-established food ingredient, sweetener, and biochemical manufacturing industries that consume significant volumes of xylose and its derivatives.

North America represented a significant market for xylose, supported by advanced biorefinery infrastructure and growing demand for sustainable ingredients. Europe also maintained a notable market presence, driven by strong bioeconomy policies and increasing investments in renewable materials. Initiatives under the European Union’s Circular Bio-based Europe program continue to encourage the commercialization of biomass-derived chemicals and ingredients.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global xylose market exhibits a moderately consolidated structure, where a limited number of established manufacturers account for a significant share of commercial production, while several regional suppliers and specialty ingredient companies serve specific end-use industries. The market is neither fully fragmented nor highly monopolistic, as production requires access to agricultural feedstocks, processing expertise, and established distribution networks. Large companies benefit from integrated supply chains, advanced bioprocessing capabilities, and long-standing relationships with food, pharmaceutical, and industrial customers.

Among the key global players, Shandong Longlive Bio-Technology Co., Ltd., Cargill, Incorporated, and Archer-Daniels-Midland Company (ADM) are recognized for their strong presence in biomass processing, specialty ingredients, and value-added carbohydrate products. These companies continue to focus on production efficiency, product quality, and expansion of bio-based portfolios to strengthen their market positions. Strategic partnerships, technology investments, and capacity improvements remain common approaches among major participants seeking to meet growing demand from food, pharmaceutical, and biotechnology industries.

The Major Players In The Industry

- DuPont de Nemours, Inc.

- International Flavors & Fragrances Inc. (IFF)

- Shandong Longlive Bio-Technology Co., Ltd.

- Futaste Co., Ltd.

- Zhejiang Huakang Pharmaceuticals Co., Ltd.

- Cargill, Incorporated

- Archer-Daniels-Midland Company (ADM)

- Ingredion Incorporated

- Prinova

- Xyleco, Inc.

- Inolex

- Wego Chemical Group

- Silver Fern Chemical

- Xylitol Canada, Inc.

- Danisco

- Others

Key Development

- In June 2026, Ingredion Incorporated announced a recommended all-cash acquisition of Tate & Lyle PLC, valuing the transaction at approximately USD 5.0 billion. The acquisition broadens Ingredion’s specialty ingredients platform across texturants, sugar reduction, and recipe development directly strengthening its position in the functional carbohydrate and sugar reduction segment relevant to the xylose market.

- In May 2026, International Flavors & Fragrances Inc. entered into a definitive agreement to sell its food ingredients business to funds advised by CVC Capital Partners, valuing the transaction at approximately USD 4.3 billion. IFF retained an approximately 10% minority equity interest in the business. The divestiture marks a significant portfolio transformation, with IFF sharpening its focus on higher-growth, higher-margin segments, including Taste, Scent, and Health & Biosciences.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.3 Bn |

| Forecast Revenue (2035) | USD 4.3 Bn |

| CAGR (2026-2035) | 6.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (D-Xylose and L-Xylose), By Application (Food & Beverage Industry, Pharmaceuticals Industry, Cosmetics & Personal Care, Animal Feed / Pet Food, Biofuel Industry, and Others), By Form (Powder and Liquid), By Source (Corncobs, Wheat Straw, Cottonseed Hulls, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | DuPont de Nemours, Inc., International Flavors & Fragrances Inc. (IFF), Shandong Longlive Bio-Technology Co., Ltd., Futaste Co., Ltd., Zhejiang Huakang Pharmaceuticals Co., Ltd., Cargill, Incorporated, Archer-Daniels-Midland Company (ADM), Ingredion Incorporated, Prinova, Xyleco, Inc., Inolex, Wego Chemical Group, Silver Fern Chemical, Xylitol Canada, Inc., Danisco, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |