Quick Navigation

Report Overview

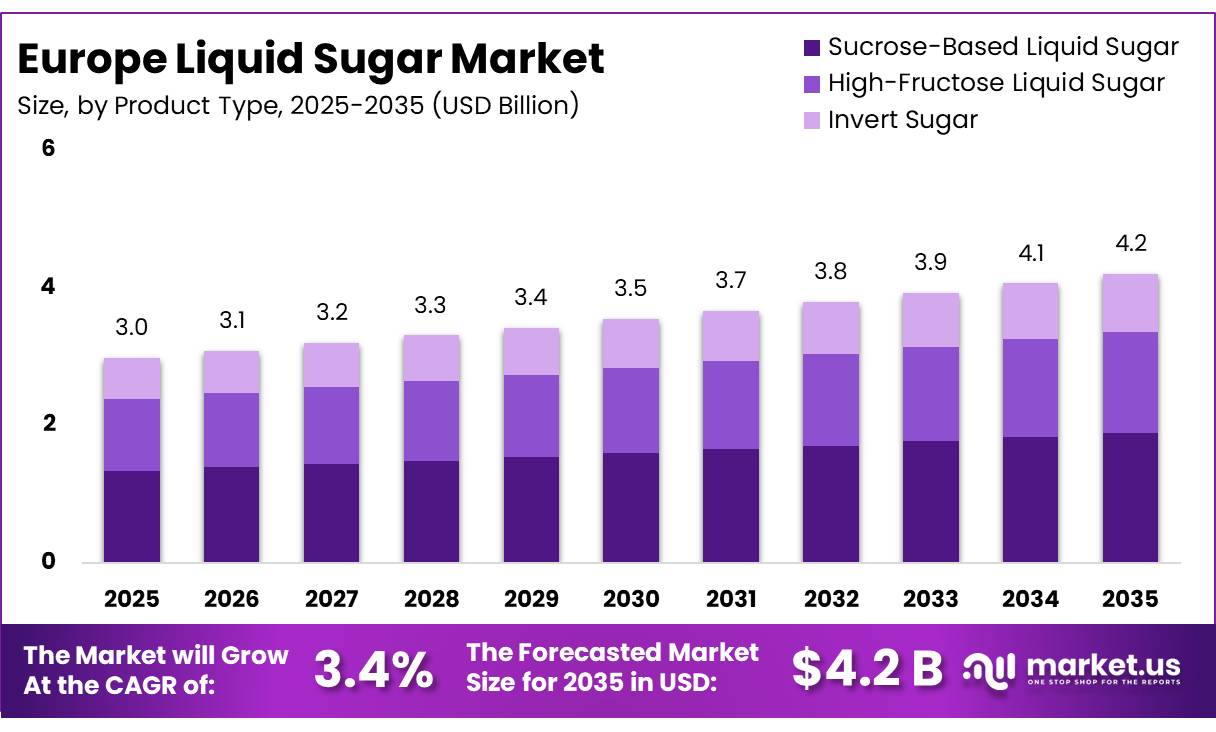

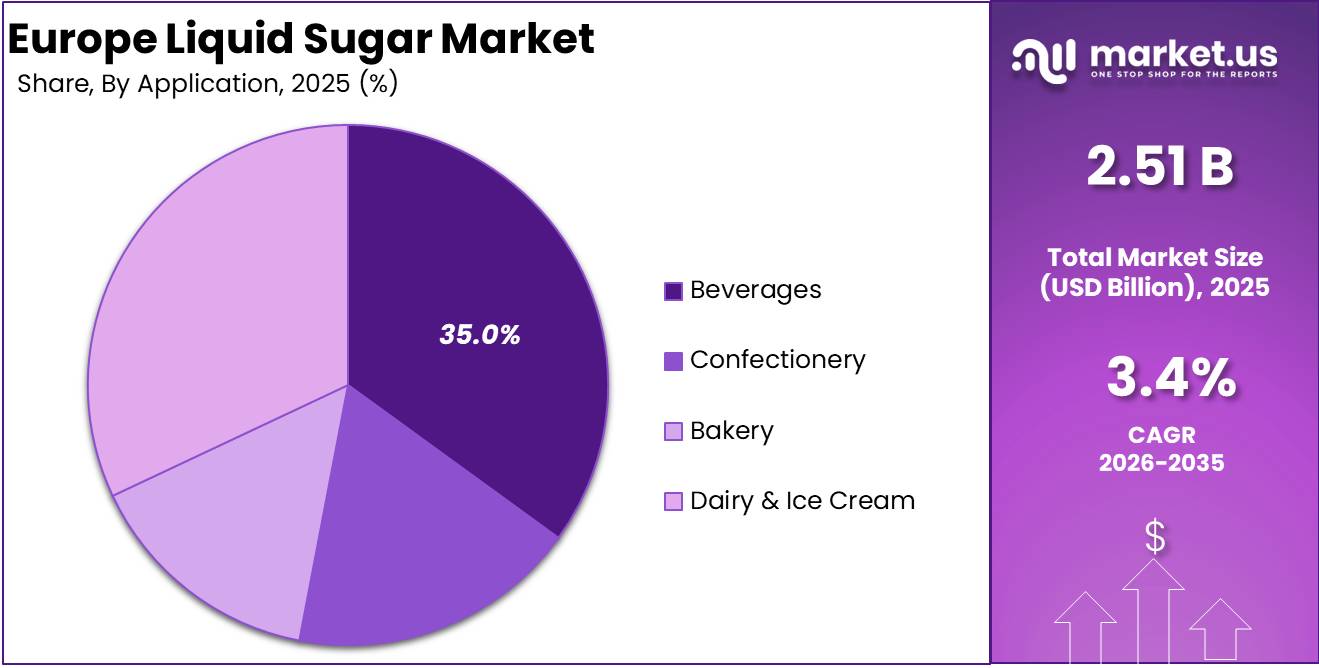

In 2025, the Europe Liquid Sugar Market was valued at USD 3.0 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 3.4%, reaching approximately USD 4.2 billion by 2035.

Europe Liquid Sugar refers to a sweet, syrupy solution made by dissolving sugars such as sucrose, glucose, or fructose in water. Commonly used in the beverage, bakery products, confectionery, and dairy industries, this product offers consistency in sweetness and flavor, enhancing product quality and shelf life.

FAO’s preliminary forecast for the 2025/26 season pegs global sugar production at 185.3 million tonnes, up 9.7 million tonnes, or 5.5 percent, from 2024/25, marking a new record level. The increase mainly stems from anticipated bumper harvests in several key producing countries. In Brazil, the world’s largest sugar producer and exporter, output is forecast to rise by around 4.0 percent year on year, recovering from weather-related reductions in 2024/25.

Key Takeaways

- The Europe liquid sugar market was valued at US 3.0 billion in 2025.

- Europe liquid sugar market is projected to grow at a CAGR of 3.4% and is estimated to reach USD 4.2 billion by 2035.

- On the basis of type, Sucrose-Based Liquid Sugar dominated the market, accounting 45% of the total market share.

- Based on the source, sugar beet-derived liquid sugar dominated the market, with a substantial market share of around 70%

- Based on the application, the beverages segment led the market, comprising 35% of the total market.

- Among the Category, the Conventional held a major share in the Europe liquid sugar market, accounting for 92% of the market share.

- Among the distribution channels, direct sales remained the most considerable within the market, accounting for around 62% of the revenue.

- In 2025, Germany was the most dominant country in the Europe liquid sugar market, accounting for 28% of the total regional consumption.

Growth factors for this market include the increasing automation in food processing and a strong trend towards natural and organic ingredients, which are pushing manufacturers to innovate and expand their liquid sugar product lines. The demand for liquid sugar is primarily fueled by the beverage industry, where it is indispensable for creating soft drinks, juices, and other flavored drinks.

The Europe Liquid Sugar Market is poised at a strategic intersection of evolving consumer preferences and stringent regulatory frameworks, presenting unique opportunities for industry players. The continent’s sugar consumption patterns, particularly in the realm of beverages, illustrate a significant demand vector.

National Library of Medicine indicates variable consumption rates of soft drinks, with average daily intakes of total soft drinks at 43 grams per day and median values at 29 grams per day. These beverages, often laden with added sugars, highlight the persistent demand for sweetened products despite health-centric shifts in consumer behavior.

Further shaping the market dynamics are the EU’s ambitious sustainability and renewable energy initiatives. The Circular Bio-based Europe Joint Undertaking (CBE JU), with a funding pool of €2 billion, underscores the commitment to fostering bio-based industries.

Notably, the €215.5 million allocation for 2023 to enhance wood-based value chains and retrofit biorefineries signifies a move towards more sustainable, high-value bio-based products.

Additionally, the EU’s Renewable Energy Directive II (RED II), aiming for a 14% renewable energy quota in the transport sector by 2030, could indirectly influence the liquid sugar sector by integrating sugar-derived biofuels into the energy mix.

This confluence of high consumption, substantial production capabilities, and forward-thinking environmental policies creates fertile ground for innovation and growth in the European liquid sugar market. Stakeholders are encouraged to leverage these insights to navigate the complexities of market expansion and sustainability challenges effectively.

By Type Analysis

Europe’s liquid sugar market sees liquid sucrose claiming a 45.0% share, indicating a strong preference.

In 2023, Liquid Sucrose held a dominant market position in the By Product Type segment of the Europe Liquid Sugar Market, with a 45.0% share. This dominance can be attributed to its extensive use in various food and beverage applications, where it is prized for its ability to enhance flavor without altering the product’s inherent properties.

The demand for Inverted Sugar Syrup has been bolstered by its use in products requiring high solubility and moisture retention, whereas Mixed Syrups have found niche applications where specific flavor profiles and functional properties are desired.

Overall, the market dynamics within the European liquid Sugar Market reflect a strong preference for product types that offer specific benefits such as taste enhancement, functional properties in food processing, and suitability for varied dietary requirements.

By Category Analysis

Conventional forms dominate the market, with an overwhelming 92.0% in Europe’s liquid sugar sales.

In 2023, Conventional held a dominant market position in the By Form segment of the European liquid Sugar Market, with an 92.0% share. This considerable market share is largely due to the widespread availability and cost-effectiveness of conventional liquid sugar, making it a preferred choice for large-scale manufacturers in the food and beverage industry.

Conventional liquid sugars are extensively used due to their versatility in various applications, including beverages, baked goods, and confectioneries, where they provide essential properties like sweetness, texture, and preservation.

The organic segment is driven by a growing segment of consumers willing to pay a premium for products perceived as healthier or more natural. This trend is supported by stricter EU regulations on organic farming and labeling, which bolster consumer confidence in organic products.

The stark contrast in market share between conventional and organic liquid sugars underscores the current market dynamics where price sensitivity and supply chain maturity favor conventional products, while niche markets that focus on product provenance and sustainability are emerging strongly.

By Source Analysis

Sugar Beet emerges as the chief source of Europe’s liquid sugar, comprising 70.0% of production.

In 2023, Sugar Beet held a dominant market position in the By Source segment of the Europe Liquid Sugar Market, with a 70.0% share. Sugarcane’s prominence in the market is attributed to its high efficiency in sugar production and its established agricultural and processing infrastructure.

This crop is favored for its ability to produce a greater volume of sugar per hectare compared to other sources, making it a cost-effective option for large-scale liquid sugar manufacturers.

This source is integral to the local economies and is heavily supported by European agricultural policies that aim to sustain the internal market and production capabilities.

This segment benefits from niche markets that are focused on sustainability and less common sugar varieties, often used in specific gourmet or health-oriented products.

By Application Analysis

In Europe, beverages lead as a primary application for liquid sugar, accounting for 35.0%.

In 2023, Beverages held a dominant market position in the By Application segment of the Europe Liquid Sugar Market, with a 35.0% share. This leading position is underscored by the widespread use of liquid sugar in various beverage formulations, ranging from soft drinks to alcoholic beverages, where it serves as a key ingredient for flavor enhancement, consistency, and fermentation processes.

The versatility and solubility of liquid sugar make it particularly suited for the beverage industry, ensuring a smooth blend with other components without sedimentation. This segmentation reveals a robust demand across diverse food sectors, each benefiting from the unique properties that liquid sugar offers.

By Distribution Channel Analysis

Direct sales are pivotal in Europe’s liquid sugar market, making up 62.0% of distribution.

In 2023, Direct Sales held a dominant market position in the By Distribution Channel segment of the Europe Liquid Sugar Market, with a 62.0% share. This significant market preference for direct sales channels is primarily driven by the bulk purchasing behaviors of large-scale food and beverage manufacturers and industrial buyers.

Direct sales channels offer these large purchasers cost efficiencies, customized product formulations, and reliable supply chains, which are crucial for maintaining production schedules and quality standards in industries heavily reliant on sugar inputs.

Retail sales benefit from the increasing consumer interest in gourmet cooking and artisanal baking, where liquid sugar is appreciated for its convenience and consistent quality. This segment also captures sales through online platforms and physical retail stores, providing accessibility to a wider range of customers, including those interested in niche and organic liquid sugar products.

The division between direct and retail sales highlights the dual nature of the market, where efficiency and customization drive large volume transactions, while accessibility and consumer preference bolster retail market strength.

Key Market Segments

By Type

- Sucrose-Based Liquid Sugar

- High-Fructose Liquid Sugar

- Invert Sugar

By Source

- Sugar Beet

- Sugarcane

By Category

- Conventional

- Organic

By Application

- Beverages

- Confectionery

- Bakery

- Dairy & Ice Cream

By Distribution Channel

- Direct Sales (B2B)

- Indirect/Distributors

Driving Factors

Rising Demand from the Food and Beverage Industry Drives the Europe Liquid Sugar Market

Rapid growth in food and beverage production across Europe is intensifying demand for liquid sugar, particularly for applications in carbonated drinks, bakery products, dairy, and confectionery manufacturing. Liquid sugar’s ease of handling, precise sweetness consistency, and direct integration into high-speed production lines make it a preferred choice over granulated alternatives.

Germany is the largest consumer of liquid sugar in Europe, accounting for around 3,200 thousand metric tons in 2023. France and the United Kingdom also represent major markets, with consumption ranging between 2,800–3,000 thousand metric tons and 2,200–2,500 thousand metric tons, respectively. This clearly highlights the strong demand base across leading European economies, mainly supported by large-scale food and beverage processing industries.

Soft drinks, fruit juices, and energy beverages rely heavily on liquid sweeteners for efficient mixing and consistent product quality. In 2024, Europe’s total food and beverage production output crossed 16.3 billion metric tons, while liquid sugar processing capacity reached more than 15.5 thousand metric tons, showing strong alignment between supply and demand. Additionally, the bakery and confectionery segment recorded over 13% growth in 2024, supported by automation and increased adoption of ready-to-use sweetener solutions in industrial production systems.

Restraining Factors

Health Concerns, Regulatory Pressure, and Alternative Sweeteners Restrain Europe Liquid Sugar Market Growth

The growth of the Europe liquid sugar market is facing challenges due to increasing health concerns associated with high sugar consumption. Consumers across the region are becoming more aware of issues such as obesity, diabetes, and other lifestyle-related diseases, which has led to a growing preference for low-sugar and sugar-free food and beverage products. This shift in consumer behavior is limiting the demand for traditional liquid sugar in several applications.

In addition, strict government regulations and sugar reduction policies in many European countries are creating pressure on food and beverage manufacturers to reduce sugar content in their products. Rising competition from alternative sweeteners such as stevia, artificial sweeteners, and natural sugar substitutes is also affecting market growth. Furthermore, fluctuations in raw material prices and high storage and transportation costs for liquid sugar continue to challenge manufacturers across the region

Growth Opportunity

Rising Demand for Convenience Foods, Beverages, and Innovative Sweetening Solutions Creating Growth Opportunities in Europe Liquid Sugar Market

Growing demand for convenience foods and ready-to-drink beverages is creating significant opportunities in the Europe liquid sugar market. Food and beverage manufacturers are increasingly adopting liquid sugar due to its easy blending, faster processing, and consistent sweetness in large-scale production applications. The European beverage industry continues to expand steadily, particularly in soft drinks, flavored beverages, bakery syrups, and dairy-based drinks, increasing the demand for liquid sweetening solutions across the region.

This growth is directly supporting the consumption of liquid sugar in processed food manufacturing and industrial beverage production. In addition, rising consumer preference for premium bakery, confectionery, and customized food products is further creating growth opportunities for manufacturers.

The increasing focus on innovative sweetening solutions, including organic and low-calorie liquid sugar variants, is also opening new opportunities for market players. Growing investments in advanced food processing technologies and sustainable production practices are expected to further support the expansion of the Europe liquid sugar market in the coming years.

Latest Trends

Growing Demand for Clean-Label and Convenient Sweetening Solutions.

The growing preference for clean-label and specialty sweetening solutions is emerging as a key trend in the Europe liquid sugar market. Food and beverage manufacturers are increasingly introducing organic, low-calorie, and naturally sourced liquid sugar products to meet changing consumer preferences for healthier and more transparent ingredients.

This trend is encouraging manufacturers to develop innovative liquid sugar formulations that offer better taste, texture, and processing efficiency while aligning with health-conscious consumption patterns. In addition, the rising popularity of premium beverages and artisanal bakery products is further increasing the use of customized liquid sweeteners.

At the same time, sustainability is becoming an important focus area across the European food industry. Manufacturers are increasingly investing in sustainable sourcing, efficient production technologies, and eco-friendly packaging solutions, which is shaping the future development of the liquid sugar market in the region.

Key Regions and Countries

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Key Players Analysis

In 2023, the Europe liquid sugar market is prominently shaped by several key players, each bringing unique strengths and strategies to the table. Companies like Archer Daniels Midland Company and Cargill Incorporated leverage their vast networks and comprehensive product portfolios to meet diverse customer needs across Europe.

Associated British Foods Plc and Südzucker AG stand out due to their deep integration across the sugar supply chain, from cultivation to distribution. These companies are not only major producers of liquid sugar but also key innovators in developing low-calorie and specialty liquid sugars, responding effectively to the growing health consciousness among European consumers.

Nordzucker AG and Tereos focus on expanding their footprint in emerging markets, utilizing their expertise in sugar production to tap into new segments that show increased demand for liquid sugar. Their strategic collaborations with food and beverage industries help secure stable demand channels and facilitate mutual growth.

Boettger Gruppe and Roquette Frères emphasize innovation in production techniques, which improve efficiency and product quality. Their approach not only addresses operational excellence but also enhances competitive positioning by adhering to stringent European standards for food safety and quality.

Top Key Players in the Market

- Archer Daniels Midland Company

- Associated British Foods Plc

- Boettger Gruppe

- Cargill Incorporated

- Cristal Union

- Galam Group

- Kent Foods Limited

- Louis Dreyfus Company B.V.

- Nordzucker AG

- Roquette Frères

- Sedamyl Group

- Sucroliq S.A.P.I DE C.V.

- Südzucker AG

- Nordzucker AG

- Sugar Australia Company Ltd

- Synova

- Tereos

- Toyo Sugar Refining Co. Ltd

- Zukan S.L.U.

Recent Developments

- July 2025: Cargill Incorporated and Domino Foods, Inc. are forming strategic partnerships with local farming cooperatives to secure sustainable, traceable sugar cane and beet supplies.July 2025: Archer Daniels Midland and Florida Crystals Corporation are unveiling modernized, automated processing lines to meet the rising global demand for certified organic and alternative sweetening solutions

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.0 Bn |

| Forecast Revenue (2035) | USD 4.2 Bn |

| CAGR (2026-2035) | 3.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Sucrose-Based Liquid Sugar, High-Fructose Liquid Sugar, Invert Sugar), By Source (Sugar Beet, Sugarcane), By Category (Conventional, Organic), By Application (Beverages, Confectionery, Bakery, Dairy & Ice Cream), By Distribution Channel (Direct Sales (B2B), Indirect/Distributors) |

| Regional Analysis | Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; |

| Competitive Landscape | Cargill, Incorporated, Archer Daniels Midland, Tate & Lyle PLC, Südzucker AG, Ingredion Incorporated, Associated British Foods, American Crystal Sugar, Purecane, Domino Foods, Inc., Florida Crystals Corporation, Wilmar International, Tereos S.A., Cosan S.A., Louis Dreyfus Company, Mitr Phol Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |