Quick Navigation

Report Overview

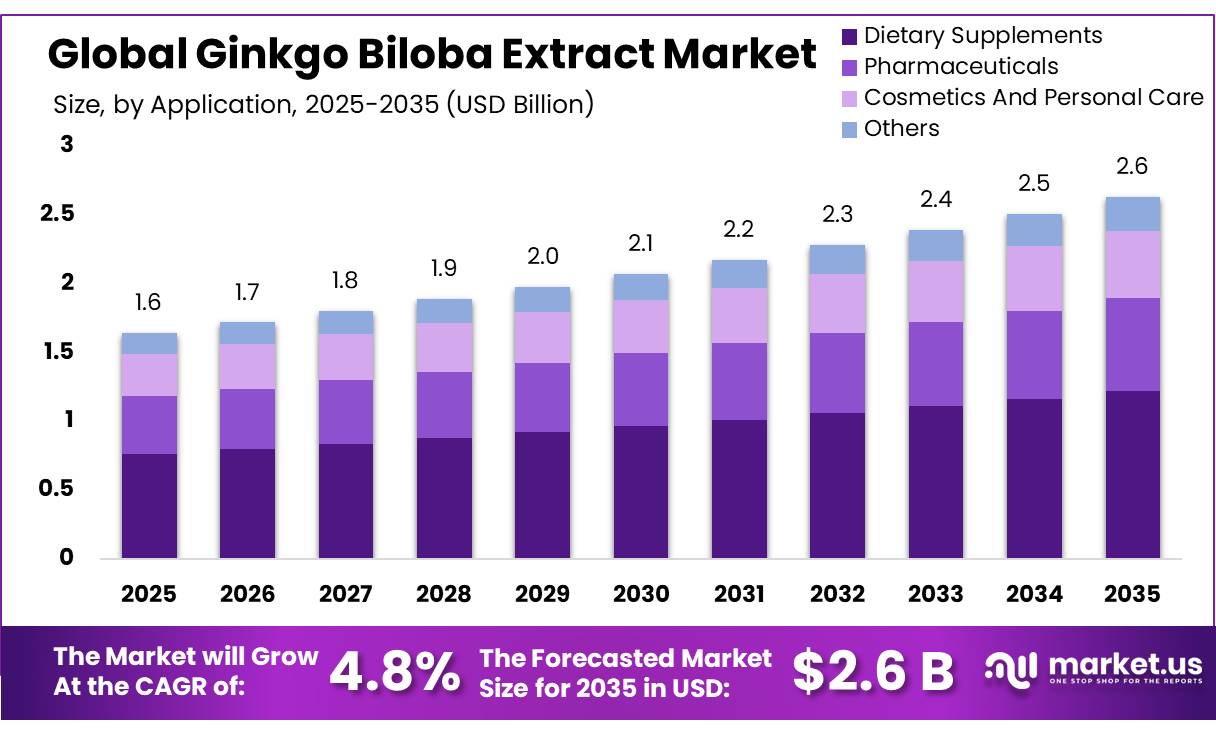

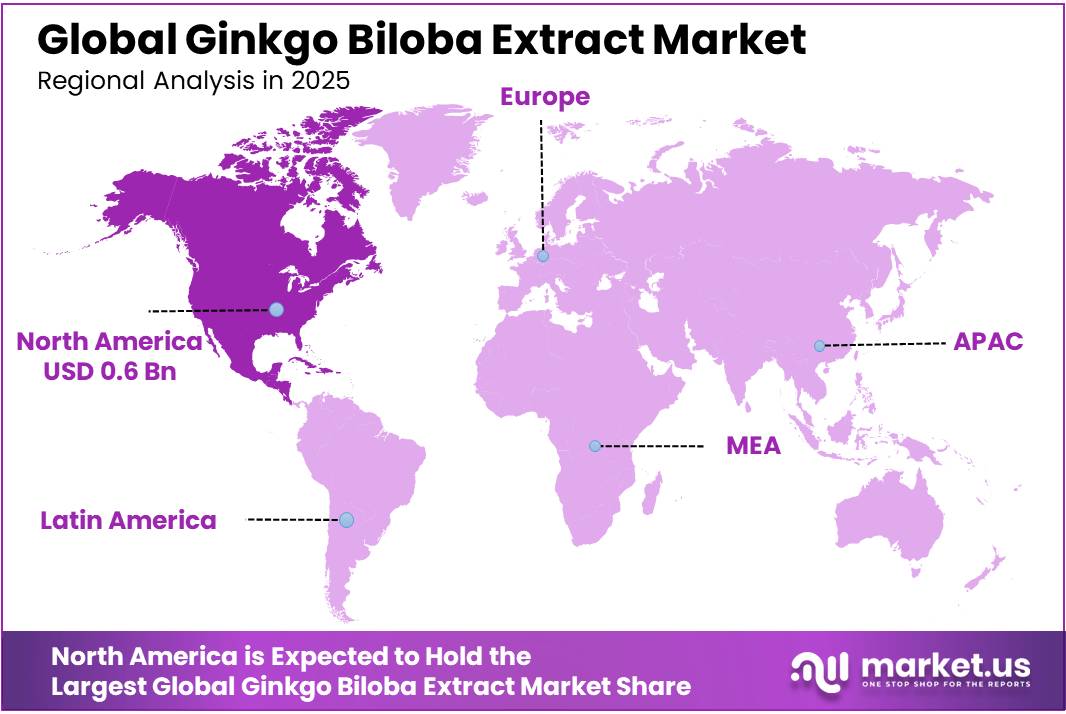

In 2025, the Global Ginkgo Biloba Extract Market was valued at USD 1.6 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 4.8%, reaching about USD 2.6 billion by 2035. North America held a dominant market position, capturing more than a 34.3% share, holding USD 0.6 billion in revenue.

The Ginkgo biloba extract industry serves dietary supplements, herbal medicines, functional beverages, and feed applications. In April 2024, the European Food Safety Authority assessed a dry extract as a sensory feed additive, confirming the ingredient’s relevance beyond human nutrition. Production centers on dried leaf processing, solvent extraction, purification, concentration, and standardization of flavonoid glycosides and terpene lactones.

- The European Medicines Agency defines a refined dry extract with a drug-extract ratio of 35–67:1 using 60% acetone, while its monograph lists 120–240 mg per single dose and 240 mg daily for well-established medicinal use.

Demand is supported by ageing populations and continued consumer interest in cognitive-health products. The United Nations projects the population aged 65 years or above to increase from 761 million in 2021 to 1.6 billion by 2050. Separately, the World Health Organization reported in March 2025 that 57 million people had dementia in 2021, with nearly 10 million new cases annually. These figures create commercial interest, although manufacturers must avoid overstating benefits. The U.S. National Center for Complementary and Integrative Health states that evidence remains inconclusive and that a study involving more than 3,000 adults found no reduction in dementia incidence.

The industrial environment is therefore shaped by quality assurance, regulatory classification, and responsible claims. In the United States, supplements are not approved by the FDA before sale, placing safety and labeling responsibility on manufacturers. In Europe, medicinal positioning requires compliance with established herbal standards and national authorization pathways.

Future opportunities are expected in clinically supported formulations, low-residue extraction, authenticated botanical sourcing, and standardized combination products. Producers strengthening analytical verification, disclosing active-compound profiles, and building application-specific evidence should gain trust across pharmacies, specialty nutrition channels, and regulated healthcare markets. This direction should also support premium positioning, stronger supply agreements, and broader international distribution over time.

Key Takeaways

- The global Ginkgo Biloba Extract market was valued at USD 1.6 billion in 2025.

- The global market is projected to grow at a CAGR of 4.8% and is estimated to reach USD 2.6 billion by 2035.

- Based on product, the Standardized Extract segment dominated the global ginkgo biloba extract market, accounting for approximately 68.4% of the total market share.

- Based on application, Dietary Supplements held the largest market share, comprising nearly 46.4% of the global market due to rising consumer demand for cognitive wellness and herbal healthcare products.

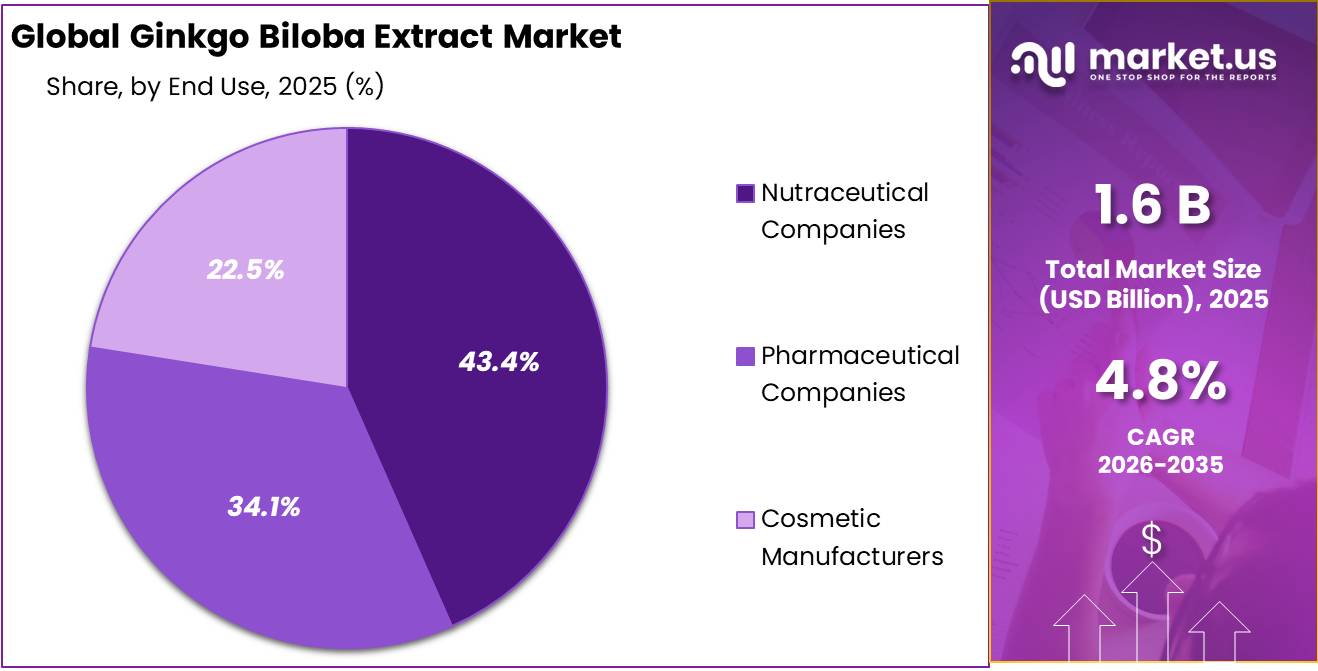

- Based on end use, Nutraceutical Companies represented the dominant segment, accounting for approximately 43.4% of the total market share.

- Based on form, the Powder segment dominated the market with around 61.2% share owing to its higher stability, ease of formulation, and wider utilization across capsules, tablets, and functional food products.

- Based on distribution channel, Distributors accounted for the largest share in the global ginkgo biloba extract market, representing approximately 41.8% of the total market.

- In 2025, North America dominated the global ginkgo biloba extract market, accounting for approximately 34.3% of the total market share due to strong nutraceutical consumption and growing demand for plant-based wellness products.

Ginkgo Biloba Extract Market Segmentation

Product Analysis

Standardized Extract leads with 68.4% due to consistent quality and reliable active-compound levels.

In 2025, Standardized Extract held a dominant market position, capturing more than a 68.4% share. In June 2025, its leadership remained supported by demand from dietary supplement, pharmaceutical, and herbal wellness manufacturers seeking consistent concentrations of flavonoid glycosides and terpene lactones. Standardized formulations are easier to use in product development, dosage planning, and quality testing.

Non Standardized Extract gained attention in June 2025 among herbal brands and traditional product makers. Its appeal came from simpler processing, flexible formulation use, and suitability for less regulated wellness products. Demand remained concentrated in niche botanical blends, local retail channels, and cost-sensitive applications where active-compound consistency was not essential.

Application Analysis

Dietary Supplements lead with 46.4% as consumers prefer convenient botanical wellness products.

In 2025, Dietary Supplements held a dominant market position, capturing more than a 46.4% share. In June 2025, the segment remained strong as consumers increasingly selected ginkgo biloba capsules, tablets, powders, and liquid supplements for wellness routines. Manufacturers favored this application because it supports flexible dosage formats, clear product positioning, and broad availability across pharmacies, specialty nutrition stores, and online channels.

Pharmaceuticals gained momentum in June 2025 as producers explored standardized ginkgo biloba formulations for regulated healthcare products. The segment benefited from stronger quality controls, clinical evaluation, and demand for consistent active ingredients. Its growth was supported by established herbal medicine use and increasing focus on evidence-based botanical treatments globally.

End-Use Analysis

Nutraceutical Companies lead with 43.4% due to strong demand for botanical wellness products.

In 2025, Nutraceutical Companies held a dominant market position, capturing more than a 43.4% share. In June 2025, these companies remained the leading end users of ginkgo biloba extract because of its broad use in capsules, tablets, powders, and liquid supplements. The segment benefited from rising consumer interest in plant-based wellness, cognitive support, and daily health products.

Pharmaceutical Companies gained steady momentum in June 2025 as demand increased for controlled, standardized, and clinically evaluated herbal formulations. Their growth was supported by stricter quality testing, regulated manufacturing practices, and continued research into botanical ingredients for healthcare applications.

Form Analysis

Powder leads with 61.2% because it offers easy handling, stable storage, and flexible formulation.

In 2025, Powder held a dominant market position, capturing more than a 61.2% share. In June 2025, the segment remained used across dietary supplements, nutraceutical products, and herbal formulations. Manufacturers preferred powder because it is easier to measure, blend, transport, and store during production. It also supports capsules, tablets, drink mixes, and functional food products, giving producers flexibility in product development.

Liquid gained interest in June 2025, supported by demand for drops, tinctures, beverages, and fast-mixing formulations. Its appeal came from convenient dosing, easier absorption, and suitability for consumers who prefer alternatives to tablets or capsules. The form also supported product innovation across wellness and herbal drink categories.

Distribution Channel Analysis

Distributors lead with 41.8% because they provide broad market access and reliable product availability.

In 2025, Distributors held a dominant market position, capturing more than a 41.8% share. In June 2025, the segment remained the preferred channel for supplying ginkgo biloba extract to nutraceutical, pharmaceutical, and herbal product manufacturers. Distributors supported the market through established supplier networks, bulk inventory management, regional warehousing, and timely delivery. They also helped smaller buyers access different extract grades and forms without placing large direct orders.

Direct Sales gained momentum in June 2025 as large manufacturers sought closer supplier relationships, better pricing control, and customized product specifications. This channel also supported long-term contracts, transparent sourcing, faster technical communication, and improved coordination between extract producers and industrial buyers.

Key Market Segments

By Product

- Standardized Extract

- Non Standardized Extract

By Application

- Dietary Supplements

- Pharmaceuticals

- Cosmetics And Personal Care

- Others

By End Use

- Nutraceutical Companies

- Pharmaceutical Companies

- Cosmetic Manufacturers

By Form

- Powder

- Liquid

By Distribution Channel

- Direct Sales

- Distributors

- Online Platform

Driver Analysis

Aging Population & Rising Dementia Burden

The single most structurally durable demand driver for ginkgo biloba extract is the irreversible global demographic inversion now underway. According to the World Health Organization (WHO), the number of people aged 60 years or older reached 1.1 billion in 2023 and is projected to nearly double to 2.1 billion by 2050, with the cohort aged 80 or older expected to more than triple between 2023 and 2060 to 545 million.

The dementia burden compounds this dynamic: WHO confirmed that 57 million people globally had dementia as of 2021, with nearly 10 million new cases added annually, while Alzheimer’s Disease International projects this figure to reach 78 million by 2030 and 139 million by 2050, implying one new case every 3.2 seconds.

In the United States specifically, the Alzheimer’s Association estimates 7.4 million Americans aged 65 and older are living with Alzheimer’s in 2026 up from 7.0 million in 2021 and projects that annual health and long-term care costs for dementia patients will reach USD 409 billion in 2026 alone, rising towards USD 1 trillion by 2050.

The fastest growth pockets within this driver are China, India, and their South Asian and Western Pacific neighbours, where the elderly population is expanding at rates that outpace even Western demographic transitions, creating a geographically distributed demand corridor that supports long-term CAGR accretion of approximately +1.8 percentage points above the market baseline.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Rising Dementia Burden driving chronic cognitive-health supplementation demand | +1.8% | Global core; APAC dominant (China, Japan, South Korea); North America secondary | Long term (≥ 4 years) |

| Pharmaceutical-Grade Clinical Validation | +1.2% | China primary (approved GDLM); EU well-established use; North America emerging pathway | Medium term (2–4 years) |

| Regulatory Dual-Classification Pressure | +0.9% | EU27 (Germany, France epicentre); UK post-Brexit corridor; South America spill-over | Medium term (2–4 years) |

| TCM Standardisation Drive | +1.1% | China supply-side core; ASEAN, Japan, EU import corridors | Short term (≤ 2 years) |

| E-Commerce & Direct-to-Consumer Nutraceutical Channels accelerating access and personalised cognitive wellness formats | +0.7% | North America, EU (D2C); APAC e-commerce corridors (India highest CAGR) | Short term (≤ 2 years) |

| Preventive Healthcare Shift | +0.8% | Global; India AYUSH policy corridor; North America & EU consumer-health mainstream | Medium term (2–4 years) |

Restraint Analysis

EU drug-like reclassification of GbE

The progressive reclassification of monograph-compliant Ginkgo biloba dry extract as a functional medicinal product in key EU jurisdictions structurally lifts compliance and lifecycle costs, as illustrated by the German Federal Administrative Court’s 2022 confirmation that products at 100 mg/day should be treated as medicines rather than food supplements. This reclassification forces manufacturers to move from relatively low-cost food law regimes into full medicinal licensing, where dossier preparation, pharmacovigilance systems, and periodic safety updates can add an estimated 4–7 percent of annual sales as recurring regulatory overhead and up to 1.5–2.0 percent of sales in one-off dossier and clinical bridging work over the first 3–5 years of transition.

The combined effect is a structural margin squeeze, where gross margins that might have sat in the 45–55 percent band for high-volume supplement SKUs can trend down to the low 40s once mandatory pharmacovigilance, batch release testing to European Pharmacopoeia standards, and medical detailing costs are fully loaded into unit economics, justifying an estimated 1.8 percentage point drag on otherwise healthy mid-single-digit global CAGR baselines through 2030.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU drug-like reclassification of GbE | -1.8% | EU core, UK adjacency | Long term (≥ 4 years) |

| Quality variance and pharmacopoeial non-compliance | -1.5% | EU, North America core, export-oriented APAC | Medium term (2–4 years) |

| Regulatory scrutiny of cognitive health claims | -1.3% | North America core, EU, high-income APAC | Medium term (2–4 years) |

| China-origin supply concentration risk | -1.1% | APAC corridors, EU, North America | Short–Medium term (≤ 4 years) |

| Herbals GMP and labelling enforcement tightening | -1.0% | North America core, EU, India | Medium term (2–4 years) |

| Clinical evidence ambiguity for dementia indications | -0.9% | Global, strongest in reimbursed EU markets | Long term (≥ 4 years) |

Opportunity Analysis

Quality-certified premiumization

NIST’s continuing work on botanical dietary supplement measurement standards, including reference materials for Ginkgo biloba leaves, extract, and ginkgo-containing tablets, provides an institutional backbone for premium SKUs that could justify 12% to 22% higher pricing and 300 to 600 basis points of gross-margin expansion by lowering batch rejection risk, private-label QA costs, and retailer compliance friction, particularly in North America, Japan, South Korea, and the EU where quality assurance has stronger commercial signaling value.

For manufacturers, even if only 25% to 30% of volume migrates into verified-standardized SKUs, the revenue mix effect can outpace unit growth because retailers and e-commerce platforms increasingly reward lower complaint rates and cleaner certificates of analysis; the modeled result is around +1.6 percentage points of CAGR upside, driven less by new users than by monetizing trust deficits that the baseline market has not yet captured.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Evidence-led stroke rehab adjacencies | +1.9% | China core, wider APAC, selective EU | Medium term (2-4 years) |

| Quality-certified premiumization | +1.6% | North America core, EU, Japan, South Korea | Short term (≤ 2 years) |

| Rx-to-supplement channel arbitrage | +1.4% | EU, North America, Australia | Medium term (2-4 years) |

| Functional format expansion | +1.2% | APAC urban, North America, GCC | Short term (≤ 2 years) |

| Supply-chain localization roll-ups | +1.7% | India, China, EU processing hubs, U.S. | Long term (≥ 4 years) |

| Regulated cognitive-aging services | +2.1% | Japan, South Korea, Germany, U.S. private clinics | Long term (≥ 4 years) |

Challenges Analysis

Adverse toxicology and risk perception

Emerging toxicological assessments and safety reviews are creating a slow‑burn drag on demand by elevating perceived risk among regulators, physicians, and risk‑averse consumers, particularly in higher‑income markets where supplement penetration is already high. Recent comprehensive reviews have highlighted that long‑term or high‑dose Ginkgo biloba use can be associated with adverse effects, drug interactions, and toxicities linked to compounds such as ginkgotoxin, while a 2025 Health Canada draft assessment proposes that Ginkgo biloba extract may be harmful to human health in certain ingested and dermal products due to potential associations with liver cancer and developmental effects.

Over a 4–6‑year horizon, this ongoing risk narrative forces firms to increase post‑marketing surveillance, run more rigorous real‑world evidence studies, and invest in pharmacoepidemiology collaborations with academic centres, while also reallocating 5–10% of annual marketing budgets toward risk communication and physician education; without these adjustments, heightened risk perception in oncology, neurology, and geriatrics‑focused channels will continue to depress uptake and shave about 1.2 percentage points from otherwise attainable market growth.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Fragmented safety regulation signal | -1.4% | North America, EU regulatory hubs | Medium term (2-4 years) |

| Adverse toxicology and risk perception | -1.2% | North America, EU, Canada, developed APAC | Long term (≥ 4 years) |

| Quality standardization and assay variance | -1.0% | China production belts, EU pharma channels, US supplements | Medium term (2-4 years) |

| Botanical supply and agro-climatic volatility | -0.9% | East Asia cultivation zones, EU import corridors | Long term (≥ 4 years) |

| Compliance overhead for multi-use applications | -1.1% | EU regulatory hubs, North America, Canada | Medium term (2-4 years) |

| Litigation, recall, and enforcement overhang | -0.8% | United States, Canada, selected EU states | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Global Supply Chain Interruptions and Regulatory Differences Affecting the Ginkgo Biloba Extract Market.

The market for ginkgo biloba extract across the world is being significantly influenced by geopolitics, international trading policies, and disruptions in the supply chain concerning botanical raw materials and natural medicines. The geopolitical turmoil happening around the globe such as the war between Russia and Ukraine and trade wars between leading economies has resulted in price fluctuations concerning shipping expenses, raw material sourcing, energy, and international logistics.

Further, the various laws governing the production of herbal supplements, botanicals, and nutraceuticals also impact the industry. The differences in the laws that govern imports, quality control, labeling, and approvals may present problems to those who are involved in international business. Moreover, the increased attention to safety issues and clinical trials has resulted in the manufacturing companies focusing on quality assurance and alternative sourcing of materials.

In addition to this, there is a growing number of governments around several nations who are supporting the use of traditional medicine and herbal health care research and nutraceutical production within their domestic territory to become less dependent on imports and to build up healthcare resilience. Investments into sustainable agriculture, in-house extraction units, and modern botanical technology will help to create stability for the supply chain and promote growth in the ginkgo biloba extract market around the world.

Regional Analysis

North America Accounted for the Largest Portion of the global Ginkgo Biloba Extract Market.

The North American region was leading the global market for ginkgo biloba extract in 2025, contributing about 34.3% of the overall market share. The key driving factor behind the leadership of the North American market is that the consumers here are very aware of their diet as well as healthcare and natural health products. The existing robust nutraceutical industry, the increasing geriatric population, and growing expenditure of consumers on cognitive health and aging are further driving the high demand for the product in the market.

Europe is a significant market for herbal medicinal products due to rising demand for plant-based extracts in medicines and cosmetics and a preference for natural health care. Meanwhile, the Asia Pacific region is experiencing market growth from strong traditional herbal practices and investments in nutraceutical production, particularly in China, Japan, South Korea, and India. Latin America and the Middle East & Africa are emerging markets driven by increased healthcare awareness.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The ginkgo biloba extract market across the world can be said to be moderately concentrated with competition being based on the following factors: product standardization, quality of extraction, regulation compliance, formulation expertise, and global distribution capabilities. The competitive environment within the sector arises due to growing consumption of health products, supplements for cognitive well-being, clean label nutraceutical ingredients, and scientifically-proven herbal supplements.

There are also growing partnerships in the market among botanically sourced raw material providers, nutraceuticals firms, scientific bodies, and healthcare enterprises in developing clinically tested herbal products and improving the effectiveness of their products. Investments in organic products, labeling, and other measures that enhance their quality will likely increase competition among industry players in the global ginkgo biloba extract market.

Market Key Players

- Hunan NutraMax Inc.

- BIOLANDES Group

- Bruker Corporation

- Croda International Plc

- Danaher Corporation

- Hallstar

- Thermo Fisher Scientific Inc.

- Indena S.p.A.

- Lucas Meyer Cosmetics

- Provital Group

- Rahn AG

- A. Herbal Bioactives LLP

- Shimadzu Corporation

- SILAB Inc.

- Waters Corporation

Key Development

- In October 2025, Waters Corporation highlighted LC–MS and UPLC solutions for routine quality control of herbal supplements, including profiling flavone glycosides and terpene lactones in standardized Ginkgo biloba extracts, enabling manufacturers to verify label‑claim potency.

- In May 2025, Indena S.p.A. highlighted its expanded botanical extract manufacturing capabilities and portfolio for brain and liver health at international nutraceutical events, underscoring its role as a leading supplier of standardized herbal extracts, including Ginkgo biloba‑based ingredients, to the global cognitive health segment.

- In October 2025, Bruker Corporation promoted high‑resolution NMR and MS platforms for characterization of complex botanical extracts, supporting advanced fingerprinting and adulteration detection in Ginkgo biloba extract supply chains.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.6 Bn |

| Forecast Revenue (2035) | USD 2.6 Bn |

| CAGR (2026-2035) | 4.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Standardized Extract and Non-Standardized Extract), By Application (Dietary Supplements, Pharmaceuticals, Cosmetics & Personal Care, and Others), By End Use (Nutraceutical Companies, Pharmaceutical Companies, and Cosmetic Manufacturers), By Form (Powder and Liquid), By Distribution Channel (Direct Sales, Distributors, and Online Platform) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Hunan NutraMax Inc., BIOLANDES Group, Bruker Corporation, Croda International Plc, Danaher Corporation, Hallstar, Thermo Fisher Scientific Inc., Indena S.p.A., Lucas Meyer Cosmetics, Provital Group, Rahn AG, S.A. Herbal Bioactives LLP, Shimadzu Corporation, SILAB Inc., Waters Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |