Quick Navigation

Report Overview

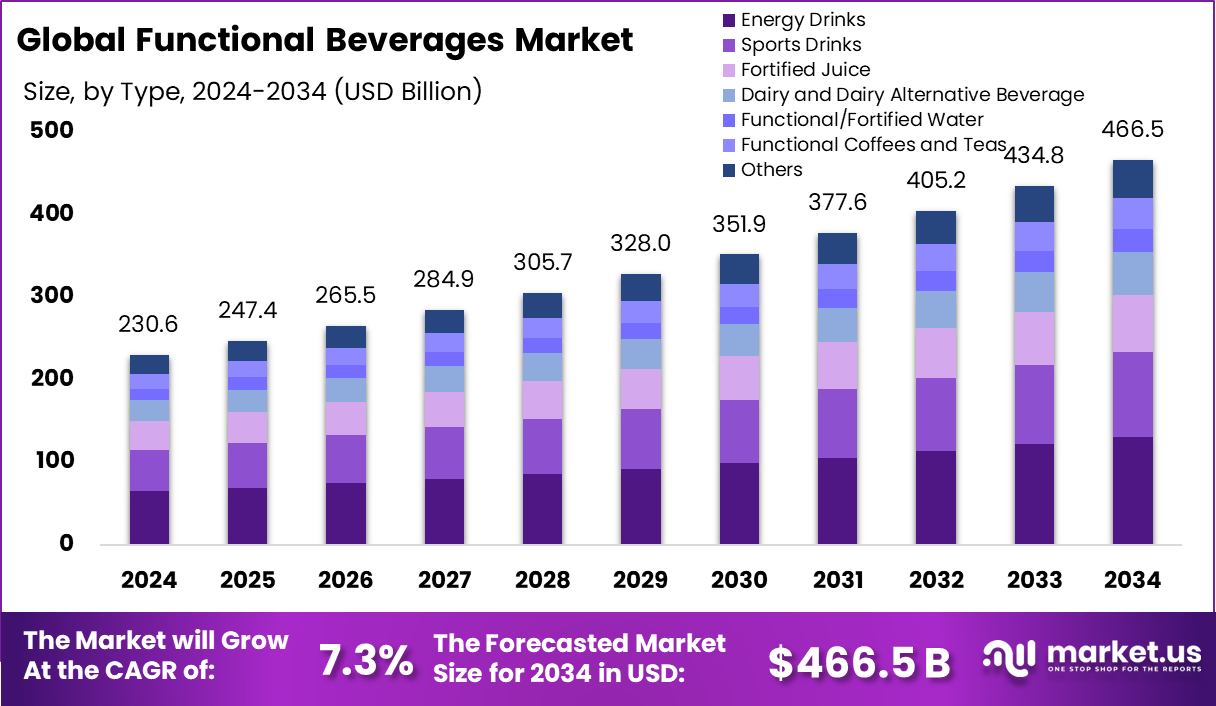

Global Functional Beverages Market is expected to be worth around USD 466.5 billion by 2034, up from USD 230.6 billion in 2024, and grow at a CAGR of 7.3% from 2025 to 2034. With a market value of USD 104.2 Bn, North America leads in functional beverage consumption and innovation.

Functional beverages are drinks enhanced with health-boosting ingredients like vitamins, minerals, herbs, amino acids, or probiotics. Unlike regular soft drinks or juices, they serve specific benefits, such as boosting immunity, improving digestion, enhancing energy, or reducing stress. These beverages are often consumed as part of a wellness-focused lifestyle, appealing to health-conscious individuals looking for alternatives to traditional sugary drinks.

The functional beverages market is growing steadily as people shift towards preventive health habits. With increasing awareness around chronic diseases and lifestyle-related conditions, consumers are more inclined to choose products that offer nutritional benefits along with hydration. The market includes a range of drinks such as fortified water, energy drinks, dairy-based beverages, and plant-based options—each designed to serve different wellness needs.

One major growth factor is the rising interest in personalized health and wellness. Consumers now actively seek beverages aligned with their daily routines—whether for energy, focus, digestion, or relaxation. Urban lifestyles, hectic schedules, and fitness trends further push the demand for convenient, on-the-go solutions.

In the functional beverages market, Celsius Holdings acquired Alani Nutrition for $1.8 billion, enhancing its sports and energy drink portfolio. Meanwhile, Cure Hydration secured $5.6 million in Series A funding, reflecting investor confidence and growing consumer demand for health-focused hydration solutions within the rapidly expanding functional beverage space.

Key Takeaways

- Global Functional Beverages Market is expected to be worth around USD 466.5 billion by 2034, up from USD 230.6 billion in 2024, and grow at a CAGR of 7.3% from 2025 to 2034.

- Energy drinks dominate with a 28.40% share due to the high demand for instant energy boosts.

- Antioxidant-infused drinks hold 27.30% due to rising awareness of cell protection and immunity.

- Athletes represent a 46.10% share, relying on functional beverages for hydration, stamina, and recovery.

- Supermarkets/Hypermarkets dominate sales at 48.20% due to visibility, accessibility, and wide product assortment.

- With a market value of USD 104.2 Bn, North America leads in functional beverage consumption and innovation.

By Type Analysis

Energy drinks dominate functional beverages with a strong 28.40% market share.

In 2024, Energy Drinks held a dominant market position in the By Type segment of the Functional Beverages Market, with a 28.40% share. This segment was chosen due to the rising demand for instant energy solutions, especially among young adults, athletes, and working professionals.

The growing adoption of fast-paced lifestyles and increased participation in fitness and sports activities have fueled the consistent consumption of energy-boosting drinks. Consumers preferred these beverages for their convenience and ability to enhance alertness and stamina.

Following energy drinks, functional waters and probiotic drinks showed significant momentum, driven by their perceived benefits in hydration and gut health. However, neither of these segments surpassed the performance of energy drinks, which maintained a broader consumer base across urban markets.

The strong positioning of energy drinks was also supported by increasing retail visibility, easy availability in convenience stores, and expansion in ready-to-drink formats. Additionally, flavor diversification and the inclusion of natural stimulants such as green tea extract and ginseng further contributed to segment growth.

By Ingredient Type Analysis

Antioxidants lead ingredient preferences, holding a 27.30% share in functional beverages.

In 2024, Antioxidants held a dominant market position in the By Ingredient Type segment of the Functional Beverages Market, with a 27.30% share. This strong lead was driven by increasing consumer awareness around oxidative stress and its connection to aging, chronic diseases, and immune health. Antioxidants, known for neutralizing free radicals, became a preferred ingredient in beverages targeted at health-conscious individuals seeking daily wellness support.

The demand for antioxidant-rich beverages was particularly high among urban populations, where pollution and lifestyle stressors heightened interest in preventive health measures. Beverages infused with ingredients like vitamin C, vitamin E, polyphenols, and plant-based extracts gained traction across various age groups. These drinks were favored not only for their health benefits but also for their clean, natural, and plant-derived appeal.

The segment’s success was further supported by its alignment with the broader clean-label and functional nutrition trends. Consumers increasingly chose antioxidant-based drinks as part of their daily hydration routine, particularly in juices, teas, and enhanced waters. While other ingredients, such as probiotics and adaptogens, are gaining visibility, antioxidants maintained a broader consumer reach in 2024 due to their strong association with immunity and vitality, securing their top position in this segment.

By End-use Analysis

Athletes represent a 46.10% share, indicating strong adoption of performance-enhancing drinks.

In 2024, Athletes held a dominant market position in the by-end-use segment of the Functional Beverages Market, with a 46.10% share. This leadership was primarily driven by the consistent demand for performance-enhancing hydration and recovery solutions tailored to athletic needs. Functional beverages catering to this group were formulated with electrolytes, proteins, amino acids, and energy-boosting compounds, making them an essential part of pre- and post-workout routines.

The segment benefited from the growing fitness culture and expanding gym memberships, particularly among young adults and professionals balancing work and physical activity. Athletes consistently prioritized beverages that supported endurance, muscle recovery, and sustained energy, contributing to high repeat purchases and brand loyalty within this group.

Moreover, the increasing participation in marathons, sports clubs, and recreational fitness programs pushed demand for ready-to-consume beverages that met specific training goals. The popularity of clean-label and low-calorie options among performance-focused individuals further strengthened this segment’s appeal.

By Distribution Channel Analysis

Supermarkets/hypermarkets dominate sales with 48.20% functional beverage market share.

In 2024, Supermarkets/Hypermarkets held a dominant market position in the By Distribution Channel segment of the Functional Beverages Market, with a 48.20% share. This dominance was attributed to their wide product assortment, high consumer footfall, and the convenience of one-stop shopping experiences. Consumers preferred purchasing functional beverages from these outlets due to easy accessibility, promotional pricing, and the ability to compare multiple brands on the shelf.

The segment’s strong performance was also driven by the increasing presence of organized retail across urban and semi-urban areas. Supermarkets and hypermarkets provide better visibility for functional beverage products through dedicated wellness sections and refrigerated displays. In-store promotions and sampling further influenced purchase decisions, especially among new customers exploring the functional beverage category.

Bulk buying options and regular discounts in these retail formats made them more appealing to frequent buyers, such as fitness enthusiasts and families. While online channels are steadily gaining momentum, particularly for niche or subscription-based health drinks, supermarkets and hypermarkets retained their edge due to the immediate availability and tactile shopping experience.

Key Market Segments

By Type

- Energy Drinks

- Sports Drinks

- Fortified Juice

- Dairy and Dairy Alternative Beverages

- Functional/Fortified Water

- Functional Coffees and Teas

- Others

By Ingredient Type

- Antioxidants

- Minerals

- Amino Acids

- Probiotics

- Prebiotics

- Vitamins

- Super-Fruit Extracts

- Others

By End-Use

- Athletes

- Fitness Lifestyle Users

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Pharmacies/Health Stores

- Convenience Stores

- Online Retail Stores

- Others

Driving Factors

Health Awareness Surge Boosting Functional Beverage Demand

One of the top driving factors in the functional beverages market is the rapid rise in health awareness among consumers. People today are more informed about how diet impacts their energy, immunity, and overall well-being. This shift is pushing many to replace sugary or carbonated drinks with functional options that offer added health benefits.

Whether it’s for gut health, immunity, energy, or hydration, shoppers now look for drinks that do more than just quench thirst. This trend is especially visible among younger consumers and urban populations who actively seek natural, low-sugar, or nutrient-rich drinks.

Restraining Factors

High Product Cost Limits Consumer Accessibility Globally

One major factor holding back the functional beverages market is their high price compared to regular drinks. Many of these beverages contain special ingredients like vitamins, probiotics, or plant extracts that cost more to make. On top of that, companies spend a lot on research, packaging, and branding to stand out in a competitive market.

This drives up the final price, making it hard for average consumers—especially in developing countries—to buy these drinks regularly. While health-conscious people in urban areas may still afford them, others see them as luxury products.

This limits widespread usage and keeps growth slower in price-sensitive regions. For the market to grow faster, more affordable options will be needed for broader access.

Growth Opportunity

Rise in Demand for Immunity-Boosting Drinks

The demand for immunity-boosting functional beverages is a significant growth opportunity in the market. With increasing awareness about health and wellness, consumers are increasingly turning to drinks that offer more than just hydration.

Functional beverages, such as those fortified with vitamins, minerals, and probiotics, are becoming popular due to their perceived benefits in enhancing immune health, especially in light of global health concerns.

As consumers seek healthier alternatives, brands that offer beverages with ingredients like vitamin C, zinc, and adaptogens stand to benefit. The trend is expected to continue, driven by a growing focus on preventative healthcare and a rising preference for natural and functional ingredients.

Latest Trends

Increased Demand for Plant-Based Functional Beverages

One of the latest trends in the functional beverages market is the growing demand for plant-based drinks. As more people adopt vegan, vegetarian, or plant-based diets, the popularity of plant-based beverages has surged.

Consumers are looking for drinks made from natural, plant-derived ingredients like coconut water, almond milk, and herbal extracts. These beverages often come with added health benefits, such as improved digestion or immune support, making them a preferred choice for health-conscious individuals.

Companies are responding to this trend by introducing more plant-based options with functional benefits like energy-boosting or stress-relieving properties. This shift toward plant-based functional drinks reflects broader dietary changes and growing awareness about the benefits of plant-based nutrition.

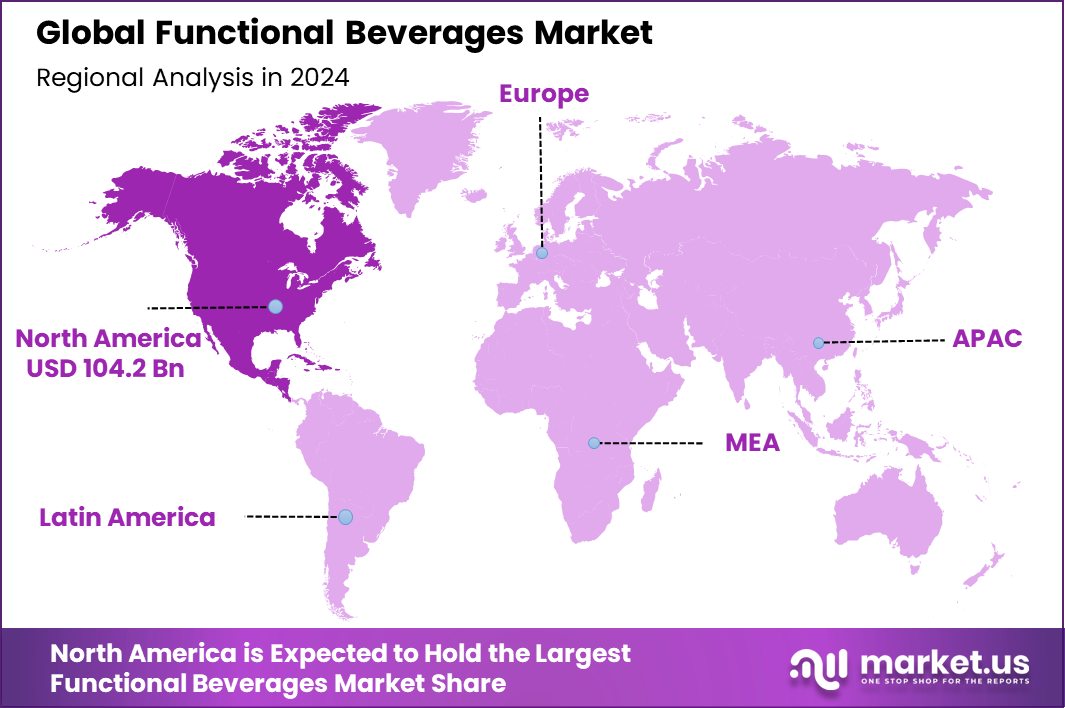

Regional Analysis

North America accounts for 45.20% of the functional beverages market, valued at USD 104.2 Bn.

The Functional Beverages Market is witnessing substantial growth across various regions, with North America leading the charge. North America holds the largest market share at 45.20%, valued at USD 104.2 Bn. This region’s dominance is driven by increasing consumer awareness regarding health and wellness, leading to rising demand for functional drinks such as energy beverages, sports drinks, and those with added nutritional benefits.

Europe follows closely, with growing trends in plant-based and functional beverages, particularly in health-conscious countries like the UK and Germany. The market in Europe is expanding as consumers shift towards natural, organic options. The Asia Pacific region, however, is expected to show the highest growth rate due to increasing disposable incomes and a rising middle-class population, with countries like China, India, and Japan playing a significant role in driving market demand.

In the Middle East & Africa, the market remains in a nascent stage but is witnessing growth due to increasing health awareness and product innovation. Latin America, though smaller in market share, is showing potential, especially with demand rising in countries like Brazil and Mexico due to the growing health trend.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, key players like Coca-Cola Company, Dr Pepper Snapple Group, and Glanbia PLC are expected to play pivotal roles in shaping the global functional beverages market. Coca-Cola, a dominant player, has made significant strides in expanding its functional beverage portfolio, particularly in the health and wellness sector.

Through innovations like Coca-Cola Plus and the launch of new product lines enriched with functional ingredients like probiotics and vitamins, the company aims to meet the increasing consumer demand for beverages that offer added health benefits. With a strong global distribution network and established brand recognition, Coca-Cola is well-positioned to maintain its leadership in the market.

Dr Pepper Snapple Group, now part of Keurig Dr Pepper, is also capitalizing on the functional beverage trend. The company has focused on diversifying its offerings to include functional drinks such as enhanced waters, energy drinks, and fortified beverages.

With a deep understanding of consumer preferences and established retail partnerships, Dr Pepper Snapple is effectively tapping into emerging trends, such as low-sugar and plant-based functional drinks, to strengthen its position in North America and beyond.

Glanbia PLC, a major player in the nutritional supplements market, has been leveraging its expertise to penetrate the functional beverages space. The company is focusing on products that promote physical performance and overall well-being, such as protein-based beverages and drinks that support digestive health.

Top Key Players in the Market

- Coca-Cola Company

- Dr Pepper Snapple Group

- Glanbia PLC

- Alltricks

- Lucozade Ribena Suntory

- Monster Beverage Corporation

- Nestlé S.A.

- Otsuka Holdings Co., Ltd.

- PepsiCo

- Red Bull GmbH

- Suntory Group

- The Coca-Cola Company

- The Kraft Heinz Company

- Unilever

Recent Developments

- In February 2025, The Coca-Cola Company expanded its functional beverages lineup by introducing Simply Pop, a prebiotic soda available in five flavors: Citrus Punch, Fruit Punch, Lime, Pineapple Mango, and Strawberry. This launch aligns with the growing consumer interest in gut health and positions Coca-Cola alongside brands like Olipop and Poppi in the prebiotic soda.

- In 2024, Glanbia PLC, a leading nutrition company, will operate in the functional beverages sector through its Glanbia Performance Nutrition (GPN) division. GPN offers consumer brands that cater to active lifestyles and health-conscious individuals. GPN was achieved, reflecting a 0.5% growth from the previous year, with an EBITDA increase of 8.3% on a constant currency basis.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 230.6 Billion |

| Forecast Revenue (2034) | USD 466.5 Billion |

| CAGR (2025-2034) | 7.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Energy Drinks, Sports Drinks, Fortified Juice, Dairy and Dairy Alternative Beverage, Functional/Fortified Water, Functional Coffees and Teas, Others), By Ingredient Type (Antioxidants, Minerals, Amino Acids, Probiotics, Prebiotics, Vitamins, Super-Fruit Extracts, Others), By End-use (Athletes, Fitness Lifestyle Users, Others), By Distribution Channel (Supermarkets/Hypermarkets, Pharmacies/Health Stores, Convenience Stores, Online Retail Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Coca-Cola Company, Dr Pepper Snapple Group, Glanbia PLC, Alltricks, Lucozade Ribena Suntory, Monster Beverage Corporation, Nestlé S.A., Otsuka Holdings Co., Ltd., PepsiCo, Red Bull GmbH, Suntory Group, The Coca-Cola Company, The Kraft Heinz Company, Unilever |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |