Quick Navigation

Report Overview

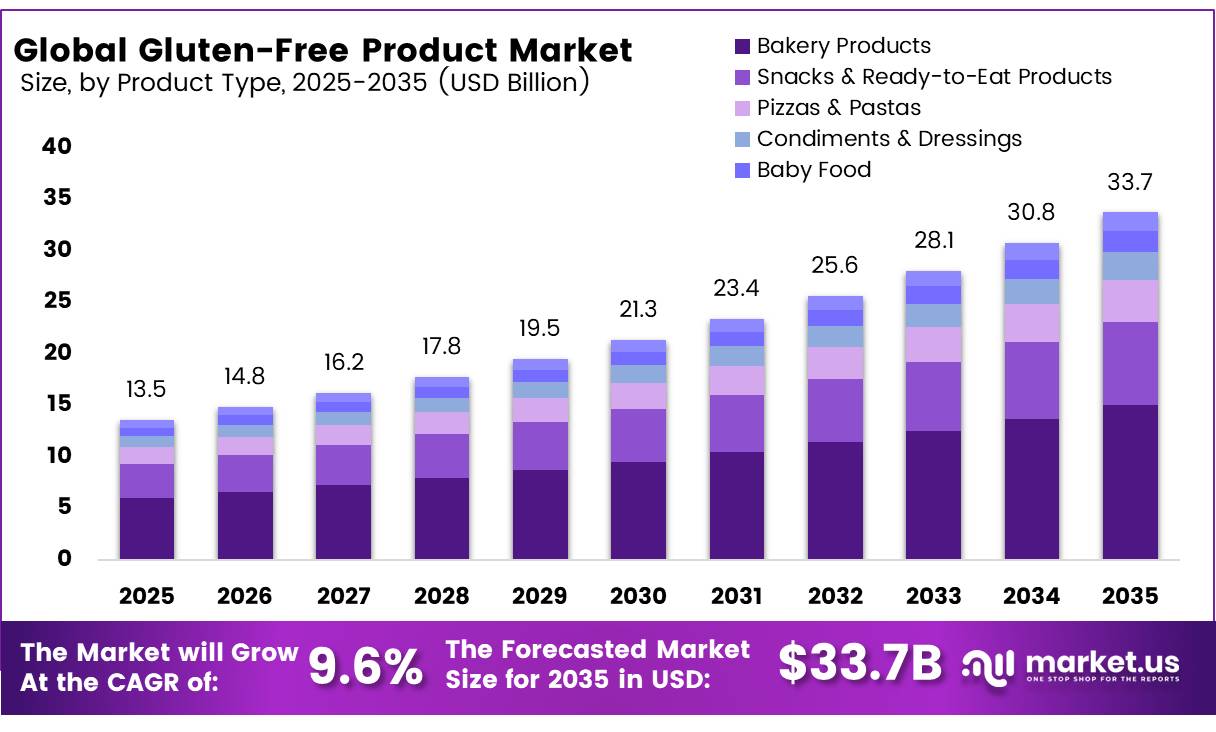

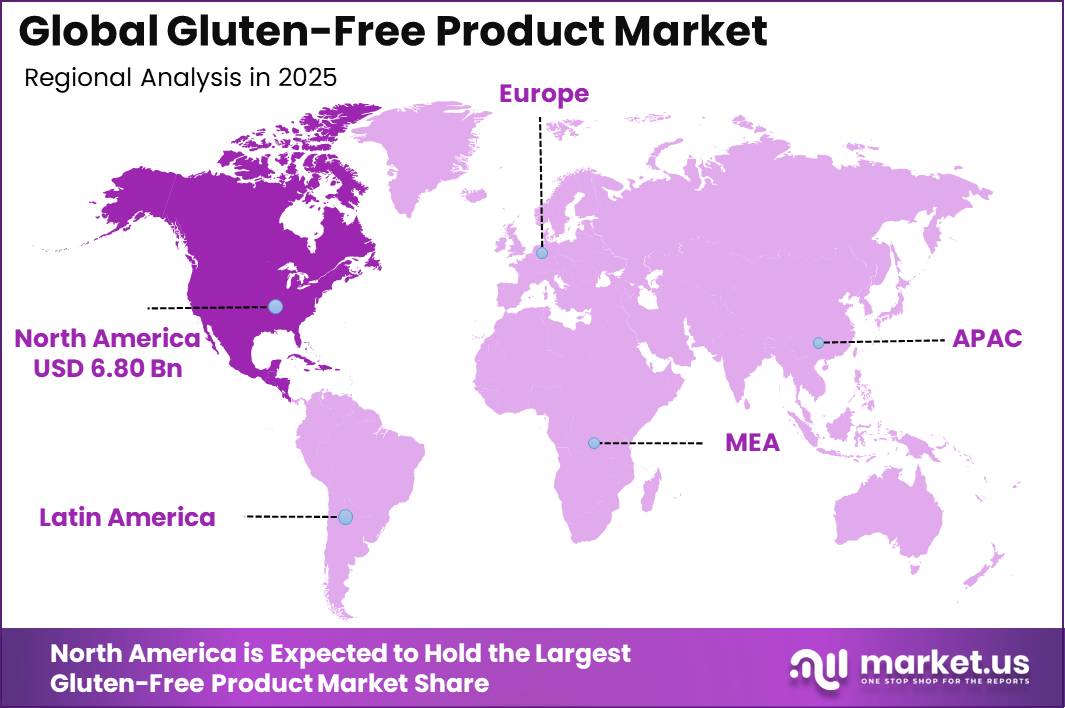

The Global Gluten-Free market was valued at USD 13.5 billion in 2025 and is expected to grow to USD 33.7 billion in 2035. Between 2025 and 2035, this market is estimated to register a CAGR of 9.6%. In 2025, North America led the market, achieving over 50.4% share with a revenue of US$ 6.80 billion.

The global gluten-free products sector has evolved into a distinct segment within the wider food and beverage industry, driven primarily by the medical needs of consumers with celiac disease and non-celiac gluten sensitivity as well as by broader health-conscious lifestyles.

Scientific reviews estimate the worldwide prevalence of celiac disease at about 0.7% of the general population, with some regions reporting ranges up to around 2.9%, which underpins a structurally recurring demand for strictly gluten-free foods across categories such as bakery, snacks, cereals, and convenience meals.

Public and regulatory institutions, including the Codex Alimentarius Commission and national food authorities, have established harmonized standards requiring gluten levels in foods labeled “gluten-free” to remain at or below 20 milligrams per kilogram (20 parts per million), thereby shaping industrial practices in sourcing, processing, segregation, and testing.

These rules, combined with rising diagnostic rates and improved awareness among healthcare professionals and consumers, are encouraging manufacturers and retailers in multiple regions outside India to expand gluten-free portfolios, invest in dedicated production lines, and innovate in taste and nutritional quality, positioning the category for continued long-term growth within mainstream retail and foodservice channels.

Key Takeaways

- The Gluten Free Products Market was valued at US$ 13.5 billion in 2025.

- The Gluten Free Products Market is projected to grow at a CAGR of 9.6% and is estimated to reach US$ 33.7 billion by 2035.

- In terms of product type, Bakery Products dominate the market with a share of 44.6%, followed by Snacks & Ready-to-Eat Products at 24.0%.

- By form, Solid products dominate with a share of 90.3%, followed by Liquid products at 9.7%.

- By distribution channel, Conventional Stores (Supermarkets/Hypermarkets) dominate with a share of 71.7%, followed by Specialty Stores, Drugstores & Pharmacies, Online Retail, and Others.

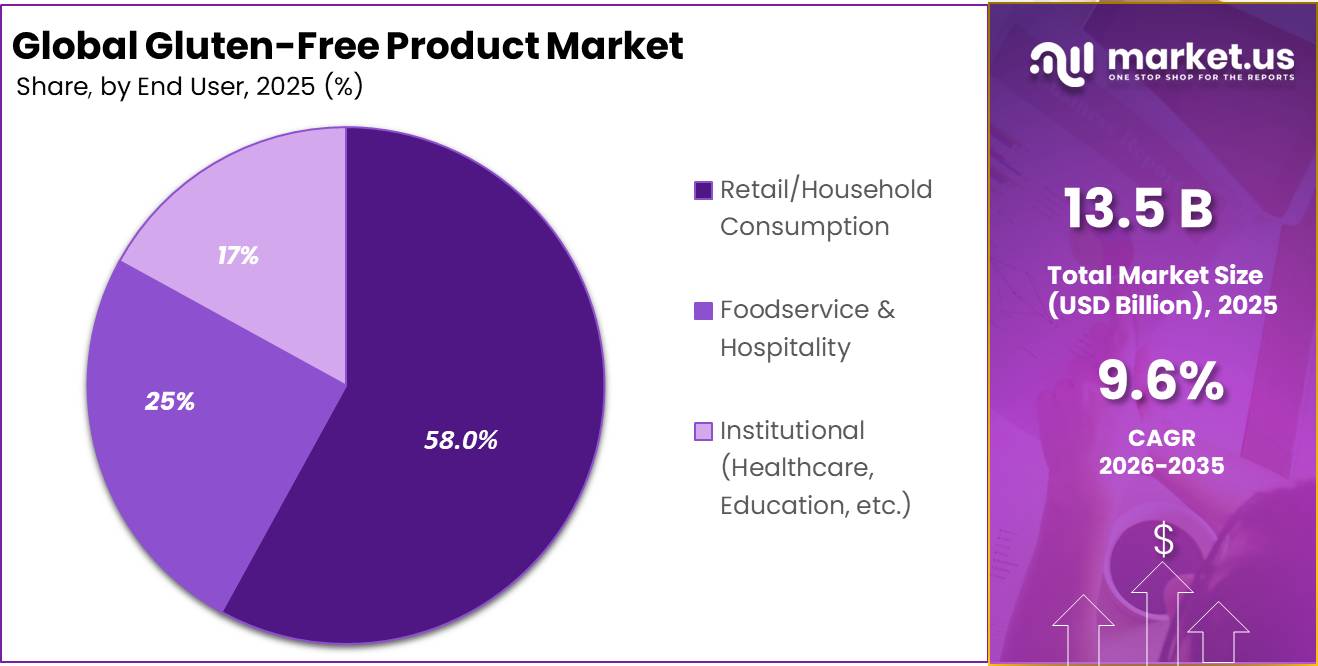

- In terms of end-user, Retail/Household Consumption dominates with a share of 58.0%, followed by Foodservice & Hospitality and Institutional users.

- In 2025, North America dominated the market, accounting for more than 50.4% of the total share.

By Product Analysis

Bakery Products dominate the global gluten-free products market with a 44.6% share, driven by high consumer demand for gluten-free bread, biscuits, pastries, and muffins among health-conscious individuals and people with celiac disease. The dominance of this segment is mainly due to the strong consumption of bakery-based staples and continuous product innovation that improves taste, texture, and similarity to traditional wheat-based products.

The fastest-growing segment in the market is Snacks & Ready-to-Eat (RTE) Products with a 24.0% share, driven by changing lifestyles, rising demand for convenient on-the-go food options, and increasing preference for gluten-free snacking alternatives. This segment is witnessing rapid expansion as manufacturers introduce innovative gluten-free snack products that cater to busy consumers seeking both health benefits and convenience.

By Form Analysis

As per format type analysis, Solid products dominate the global gluten-free products market with a 90.3% share, driven by strong consumer preference for bakery items, snacks, cereals, and other solid food alternatives that replicate traditional gluten-containing foods. The dominance of this segment is mainly due to higher consumption of convenient, ready-to-eat solid food products and continuous innovation in texture and taste that closely match conventional products.

The dominance of solid formats is further supported by their wide availability across supermarkets, specialty stores, and online retail platforms, making them easily accessible to consumers following gluten-free diets. Increasing awareness of gluten intolerance and the growing demand for healthier dietary options have also contributed significantly to the strong performance of solid gluten-free products globally.

Distribution Analysis

As per distribution channel analysis, Conventional Stores (Supermarkets/Hypermarkets) dominate the global gluten-free products market with a 71.7% share, driven by their strong retail presence, wide product assortment, and consumer preference for physically inspecting food products before purchase. The dominance of this segment is mainly due to the convenience of one-stop shopping, promotional pricing strategies, and easy availability of gluten-free products alongside regular grocery items.

The fastest-growing segment in the market is online retail (e-retail), driven by increasing digital adoption, rising preference for home delivery, and expanding availability of niche gluten-free products through e-commerce platforms. Growing convenience, wider product variety, and attractive online discounts are further accelerating the shift toward online purchasing channels among health-conscious consumers.

End Use Analysis

As per end-user analysis, Retail/Household Consumption dominates the global gluten-free products market with a 58.0% share, driven by rising at-home consumption, increasing health awareness, and strong availability of packaged gluten-free products across retail channels.

This particular segment plays a critical role in the market share of gluten-free products, making up 58.0% because of an increase in the consumption of such products at home. The reasons behind the rise in the consumption of these products have been an increase in awareness regarding the need for healthy products, an increasing number of people suffering from gluten intolerance, and availability through retail outlets as well as online sources.

Key Market Segments

By Product type

- Bakery Products

- Snacks & Ready-to-Eat (RTE) Products

- Pizzas & Pastas

- Condiments & Dressings

- Baby Food

- Others

By Form

- Solid

- Liquid

By Distribution Channel

- Conventional Stores

- Specialty Stores

- Drugstores & Pharmacies

- Online Retail

- Others

By End-user

- Retail/Household Consumption

- Foodservice & Hospitality

- Institutional

Market Dynamics

Drivers

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diagnosis of celiac and gluten sensitivity | +2.0% | North America, Europe, Asia Pacific | Short term (≤ 2 years) |

| Clean label and wellness positioning of gluten-free | +1.2% | Global | Short term (≤ 2 years) |

| Expansion of gluten-free bakery and snacks | +1.0% | North America, Europe | Medium term (2 to 4 years) |

| Improved taste and texture via specialty ingredients | +0.8% | North America, Europe, selected Asia Pacific | Medium term (2 to 4 years) |

| Retail penetration in mainstream grocery and e-commerce | +0.7% | Global urban markets | Short term (≤ 2 years) |

| Standardized gluten-free labeling frameworks | +0.5% | US, EU, select OECD markets | Long term (≥ 4 years) |

Rising diagnosis of celiac and gluten sensitivity

Epidemiological data from North American, European, and emerging Asia Pacific health systems indicate that diagnosed celiac disease prevalence has increased from roughly 0.5 to 1.0% of the population to closer to 1.0 to 1.5% in many urban cohorts over the past decade, with non celiac gluten sensitivity cases adding 1 to 3% of consumers who are advised by physicians or nutritionists to avoid gluten containing grains such as wheat, barley, and rye.

This expanding medically indicated patient base translates into recurrent demand for gluten-free staples, with household baskets shifting 10 to 20% of their cereal, bakery, and snack spend toward certified gluten-free products, raising per capita annual unit volumes by several kilograms equivalent of gluten-free flour, bread, and packaged foods.

As health insurers, specialty clinics, and gastroenterology practices increasingly document gluten related disorders in electronic health records and issue diet guidance, mainstream retailers respond by allocating an additional 1 to 2 linear shelf meters per store to gluten free lines, and manufacturers retool lines to maintain gluten content below the 20 ppm threshold defined in US and EU labeling schemes, supporting a structural uplift of approximately +2.0% to the baseline gluten free market CAGR while compressing margins for legacy wheat based SKUs that lose a portion of their volume share.

Restraints

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing versus conventional products | -1.5% | Global | Short term (≤ 2 years) |

| Limited availability in emerging market retail | -0.9% | Asia Pacific, Latin America, Africa | Medium term (2 to 4 years) |

| Tariffs and import dependence on specialty grains | -0.7% | Import-dependent economies | Short term (≤ 2 years) |

| Consumer skepticism about health halo | -0.6% | North America, Europe | Medium term (2 to 4 years) |

| Complex cross-contact control costs | -0.5% | Global manufacturing hubs | Short term (≤ 2 years) |

| Regulatory non-compliance risk for labeling | -0.4% | US, EU, selected Asia Pacific | Long term (≥ 4 years) |

Premium pricing versus conventional products

Gluten free products typically carry a retail price premium of approximately 20 to 80% versus conventional counterparts because of higher ingredient costs for specialty grains such as sorghum, millet, amaranth, and rice, smaller batch production, and incremental quality assurance testing to verify gluten levels below 20 ppm.

This premium materially constrains addressable demand in price-sensitive segments, as household food budgets in many markets allocate less than 10 to 15% of income to packaged foods, making it difficult for non medically required consumers to justify paying 2 to 3 times more for gluten-free bread or pasta every week.

For manufacturers and retailers, the need to sustain gross margins of at least 25 to 30% on gluten-free lines to cover specialized production, certification audits, and potential recall reserves leads to cautious SKU expansion and slower rollout into discount and mass channels, reducing the baseline market CAGR by an estimated 1.5% as premium positioning caps volume growth even in markets with high awareness.

Challenges

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Volatile supply of gluten-free grains | -1.3% | Global exporters and importers | Medium term (2 to 4 years) |

| Manufacturing line segregation complexity | -1.0% | Global | Medium term (2 to 4 years) |

| Technical challenges in product quality | -0.9% | Global | Short term (≤ 2 years) |

| Inconsistent enforcement of gluten thresholds | -0.7% | Emerging markets | Long term (≥ 4 years) |

| Limited specialized R and D talent | -0.6% | Global | Long term (≥ 4 years) |

| Logistics and storage constraints for niche SKUs | -0.5% | Global retail chains | Short term (≤ 2 years) |

Volatile supply of gluten-free grains

Global cereal supply chains for corn, rice, sorghum, and other gluten-free compatible grains face weather-related yield volatility and trade policy shocks, with some exporting countries introducing tariffs or export restrictions that can swing landed costs by 10 to 25% year on year for processors dependent on imported raw materials.

Because gluten-free product formulations often rely on specific starch and protein profiles, manufacturers cannot always substitute local grains without reformulation and sensory testing, so a 5 to 10% disruption in supply of a key grain can translate into 2 to 3 weeks of production delays, elevated safety stocks, and increased working capital tied up in inventory across multiple markets.

Over a planning horizon of 2 to 4 years, companies must diversify sourcing regions, enter into multi origin contracts, and invest in risk management tools such as commodity hedging and dual sourcing strategies, adding 1 to 2% to cost of goods sold but mitigating deeper margin shocks, while the residual uncertainty shaves an estimated 1.3% off the maximum attainable gluten free market CAGR by discouraging aggressive capacity expansion and limiting smaller firms’ ability to scale.

Opportunities

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Expansion into emerging Asia Pacific gluten free staples | +1.8% | Asia Pacific | Medium term (2 to 4 years) |

| Plant-based and gluten-free cross-innovation | +1.4% | Global | Short term (≤ 2 years) |

| Private label gluten free ranges in mass retail | +1.2% | North America, Europe, Latin America | Medium term (2 to 4 years) |

| Foodservice adoption in QSR and hospitality | +1.0% | Global urban markets | Long term (≥ 4 years) |

| Digital D2C subscription models for gluten free baskets | +0.9% | Global | Short term (≤ 2 years) |

| Fortified gluten-free products targeting micronutrient gaps | +0.8% | Global | Long term (≥ 4 years) |

Expansion into emerging Asia Pacific gluten free staples

This opportunity is untapped relative to current drivers because most gluten free penetration remains concentrated in North America and Europe, while large Asia Pacific markets with growing middle income populations and rising diagnosis of celiac disease still have gluten free products representing a low single digit share of packaged staples such as flour mixes, noodles, and bakery items.

By localizing gluten-free formulations around familiar staples, for example rice-based breads, millet rotis, or sorghum noodles, and leveraging regional grains already cultivated at scale, manufacturers can reduce ingredient cost per kilogram by 10 to 15% versus imported blends, while expanding distribution through modern trade and e-commerce to reach tens of millions of urban and upper middle income households over the next 2 to 4 years.

If companies achieve even a 3 to 5% share of relevant staple categories in these markets, with operating margins of 15 to 20% supported by localized sourcing and co-manufacturing, the incremental volume could add approximately +1.8% to the global gluten-free market CAGR above the 6.2% baseline, while meaningfully diversifying revenue away from mature Western markets.

Geopolitical Impact Analysis

Analysis of Geopolitical Effects on the Gluten-Free Products Market

A significant part of geopolitics regarding the market is the disruption of global logistics systems due to trade wars, military action, and other similar issues. Many products that have substitutes for gluten require the presence of ingredients like rice, corn, quinoa, millet, and other specialized grains imported from other countries.

In addition, increased levels of inflation coupled with fluctuating prices of commodities have contributed to the market by increasing the costs of raw materials, packaging materials, and transportation costs. Because gluten-free products are costly, further increases in costs may lead to unaffordability, limiting consumer demand, especially in price-sensitive markets.

Additionally, the changing trends in food safety regulations and international trade laws present challenges to the manufacturers. Regulatory bodies in several regions are adopting stringent labeling requirements, thus increasing the production costs for companies operating overseas.

Regional Analysis

The landscape of the Gluten-Free Products Market in the region is dominated by North America, accounting for 50.4% of the market share across the globe. The dominance can be attributed to heightened consumer awareness about gluten intolerance, rising popularity of health-conscious and clean-label foods, and easy availability of gluten-free food products. Presence of major market participants along with innovations within products will contribute towards the dominance.

Europe is considered a key regional market because of high consumer awareness about health, stringent labeling policies, and availability of markets for gluten-free products. Countries like the UK, Germany, and Italy contribute significantly to the growth of the European market owing to their increasing preference for specialty diets.

Key Regions and Countries Covered in this Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Gluten-Free Products Market exhibits fragmentation since it consists of many global food manufacturing firms as well as specialist health-food companies that compete with one another through innovations, pricing strategies, and increasing distribution channels. Leading firms such as General Mills dominate the industry on account of their established brands, wide distribution channels, and continuous research and development initiatives.

Nestle and General Mills enjoy significant market shares owing to the variety of their gluten-free products and widespread business across several countries. These firms benefit from their well-established distribution channels and increased consumer trust in branded food products aimed at improving consumers’ health.

Additionally, regional and private label brands become increasingly popular as a result of more competitive prices as well as consumer demand for local and organic products. Growth of e-commerce and allocation of larger shelf space in stores contribute to intensifying competition within the industry.

Major Players in the Industry

- The Kraft Heinz Company

- General Mills, Inc.

- Conagra Brands, Inc.

- The Hain Celestial Group, Inc.

- Kellanova

- Barilla G. e R. F.lli S.p.A.

- Raisio Oyj

- Mondelez International, Inc.

- PepsiCo, Inc.

- Nestlé S.A.

- Dr. Schär AG / SPA

- Enjoy Life Foods

- Bob’s Red Mill Natural Foods, Inc.

- Canyon Bakehouse, LLC

- Glutino (Mondelez International)

- Others

Key Development

- In December 2025, General Mills expanded its gluten-free product portfolio by strengthening its certification standards and introducing improved supply chain traceability for its gluten-free bakery and snack offerings, reinforcing consumer trust and product transparency in the global market.

- In February 2026, General Mills announced plans to expand its gluten-free and protein-rich cereal portfolio, including popular brands such as Cinnamon Toast Crunch and Lucky Charms. The company aims to strengthen its presence in the health-oriented breakfast segment by offering more nutritious and gluten-free options.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 13.5 Bn |

| Forecast Revenue (2035) | USD 33.7 Bn |

| CAGR (2026-2035) | 9.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product type (Bakery Products, Snacks & Ready-to-Eat (RTE) Products, Pizzas & Pastas, Condiments & Dressings, Baby Food, Others), By Form (Solid, Liquid), By Distribution channel (Conventional Stores, Specialty Stores, Drugstores & Pharmacies, Online Retail, Others), By End User (Retail/Household Consumption, Foodservice & Hospitality, Institutional) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa, & Rest of MEA |

| Competitive Landscape | The Kraft Heinz Company, General Mills, Inc., Conagra Brands, Inc., The Hain Celestial Group, Inc., Kellanova, Barilla G. e R. F.lli S.p.A., Raisio Oyj, Mondelez International, Inc., PepsiCo, Inc., Nestlé S.A., Dr. Schär AG / SPA, Enjoy Life Foods, Bob’s Red Mill Natural Foods, Inc., Canyon Bakehouse, LLC, Glutino (Mondelez International), Others |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, we can provide further customization to meet your requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |